ID : MRU_ 432421 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

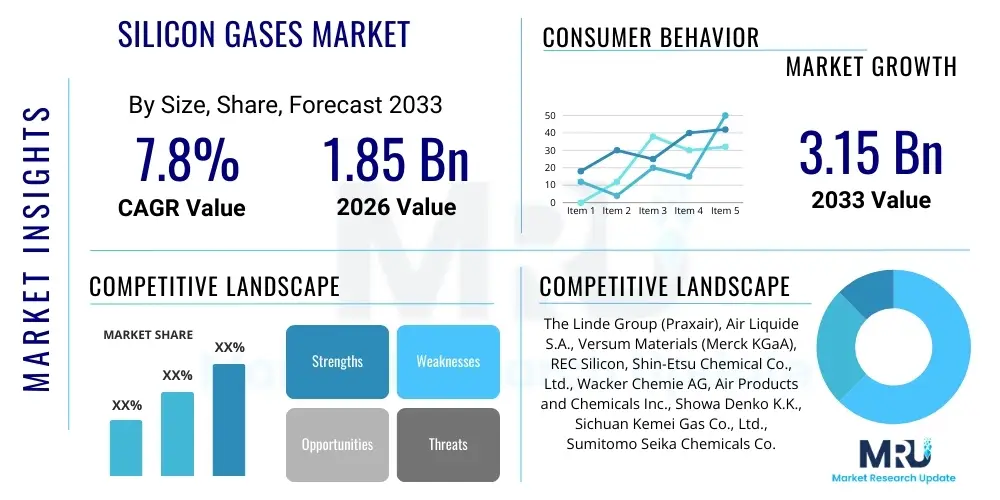

The Silicon Gases Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at $1.85 Billion in 2026 and is projected to reach $3.15 Billion by the end of the forecast period in 2033.

The Silicon Gases Market encompasses a diverse range of specialized gas compounds containing silicon, primarily used as precursors or doping agents in high-technology manufacturing processes. Key products include Silane (SiH4), Disilane (Si2H6), Chlorosilanes (e.g., Monochlorosilane, Dichlorosilane, Trichlorosilane), and Tetrafluorosilane (SiF4). These ultra-high purity gases are foundational raw materials in the production of electronic components, solar photovoltaic (PV) cells, and specialized display technologies. Their chemical versatility allows for precise deposition of silicon thin films through processes like Chemical Vapor Deposition (CVD) and Plasma Enhanced Chemical Vapor Deposition (PECVD), driving performance improvements in end products.

Major applications of silicon gases span across the semiconductor industry, where Silane is critical for depositing epitaxial silicon, gate oxides, and passivation layers in integrated circuits (ICs) and memory chips. The solar industry utilizes these gases extensively for the production of high-efficiency amorphous silicon and polycrystalline silicon thin-film PV cells, which constitute a significant portion of global renewable energy infrastructure expansion. Furthermore, the burgeoning demand for high-resolution displays, particularly OLED and advanced LCD panels, relies on the consistent quality and precise deposition capabilities offered by specialized silicon gas precursors. The benefits of using silicon gases include enhanced material purity, improved manufacturing scalability, and superior electronic properties in the final device structure.

The market expansion is fundamentally driven by the accelerating global digitization trend, necessitating massive investments in semiconductor fabrication facilities (fabs) for AI, 5G, and IoT infrastructure. The aggressive growth targets in renewable energy deployment, particularly in Asia Pacific nations, further amplify the demand for high-purity silicon feedstock used in solar PV manufacturing. Regulatory mandates promoting low-carbon energy sources and the constant technological evolution towards smaller, more powerful, and energy-efficient electronic devices are key factors sustaining the high growth trajectory of the silicon gases sector. Continuous innovation in gas handling and purification technologies ensures the supply meets the stringent purity requirements of advanced lithography and deposition techniques.

The Silicon Gases Market demonstrates strong resilience, underpinned by robust business trends centered on global semiconductor capacity expansion and renewable energy mandates. Current business trends indicate a significant shift towards establishing regional supply chain independence, prompting massive capital expenditure in high-ppurity gas production facilities in North America and Europe, countering the historical dominance of Asian suppliers. Strategic mergers and acquisitions among leading industrial gas producers and specialty chemical companies are consolidating market expertise and vertically integrating the supply chain from raw silicon refinement to ultra-pure gas delivery, ensuring quality control and stable supply to sensitive electronics manufacturing clients. Furthermore, there is an increasing focus on developing sustainable production methodologies, including recycling waste silicon gases (such as SiF4) to reduce environmental footprint and raw material costs, becoming a central theme in long-term corporate strategy.

Regionally, Asia Pacific (APAC) remains the undisputed epicenter of demand, driven primarily by South Korea, Taiwan, China, and Japan, which host the majority of global semiconductor foundries and major solar PV manufacturing hubs. However, North America and Europe are exhibiting above-average growth rates, fueled by government incentives (like the CHIPS Act in the US and similar initiatives in the EU) aimed at revitalizing domestic microelectronics manufacturing, thereby increasing the localized requirement for precursor gases like Silane and Chlorosilanes. The Middle East and Africa (MEA) and Latin America currently represent nascent but strategically important markets, particularly regarding potential solar farm deployments, though demand for ultra-high purity semiconductor-grade gases remains concentrated in established manufacturing zones.

Segment-wise, the Silane segment dominates the market due to its indispensable role in mainstream CMOS fabrication and thin-film solar panel production. The fastest-growing segment, however, is Disilane and related higher silanes, driven by advanced semiconductor applications requiring lower deposition temperatures and higher film quality, essential for next-generation memory (DRAM, NAND) and logic devices using FinFET or GAA (Gate-All-Around) structures. The application segmentation clearly highlights semiconductors as the primary revenue generator, followed closely by the solar PV sector, which provides high volume demand. LCD and emerging display technologies, while smaller in volume, drive high value due to the extreme purity requirements needed for backplane transistor formation.

Common user questions regarding AI's impact on the Silicon Gases Market revolve around two core themes: whether AI-driven manufacturing optimizations will reduce gas consumption per unit, and critically, how the surging global demand for AI-specific hardware (e.g., high-performance computing GPUs, TPUs) will influence the overall volume and purity requirements for silicon gases. Users frequently inquire about the correlation between AI accelerator fabrication complexities and the increased need for specialty silicon precursors (like Disilane or high-k precursors derived from silicon gases). The key themes suggest an expectation that AI will optimize supply chains and production efficiency, but simultaneously act as a monumental demand driver due to the necessity of building immense, power-intensive data centers requiring cutting-edge semiconductor nodes, all dependent on highly specialized silicon gas feedstock. The overarching concern is ensuring the supply chain can scale rapidly enough to meet AI-induced demand spikes while maintaining the stringent quality required for advanced nodes.

The market is primarily driven by the robust and continuous global expansion of semiconductor manufacturing capacity, particularly the shift towards advanced logic and memory nodes that rely heavily on high-purity silicon precursors for precise thin-film deposition. This driver is powerfully reinforced by government policies globally that subsidize and incentivize localized semiconductor production, ensuring sustained high demand regardless of short-term economic fluctuations. Coupled with the semiconductor boom is the massive, long-term global transition to renewable energy, which necessitates significant volumes of silicon gases, primarily Silane, for the ongoing production of both wafer-based and thin-film solar photovoltaic cells. These macro-level forces create a strong foundation for continuous market expansion, necessitating substantial capital investment in production infrastructure.

However, the market faces significant restraints, chiefly concerning the high capital intensity and complex technological requirements for producing and handling ultra-high purity silicon gases. These gases, particularly Silane, are pyrophoric and toxic, demanding specialized infrastructure, rigorous safety protocols, and intricate logistical networks, which inflate operational costs and restrict entry for new competitors. Furthermore, the volatility in raw material (polysilicon) prices and the intense global competition within the highly consolidated industrial gas sector pose challenges to maintaining stable profitability margins. Any disruption to major polysilicon production sites or transportation routes can immediately impact the availability and pricing of silicon gases, leading to supply chain fragility.

Opportunities in the silicon gases market are significant, revolving around technological advancements in novel deposition techniques, such as Atomic Layer Deposition (ALD), which require next-generation silicon precursors to achieve atomic-level film thickness control, especially crucial for next-generation 3D NAND and GAA transistors. The untapped potential in emerging markets, especially in Southeast Asia and India, which are increasingly investing in electronics assembly and solar manufacturing capabilities, represents fertile ground for market penetration. Moreover, the focus on closed-loop systems and sustainable manufacturing practices, including the development of effective recycling technologies for process waste gases, presents opportunities for specialized firms to offer environmentally compliant and cost-effective solutions. The impact forces are overwhelmingly positive, driven by digitalization (pushing semiconductor demand) and climate policy (pushing solar demand), overshadowing the inherent risks associated with handling hazardous materials.

The Silicon Gases Market is fundamentally segmented based on the product type, end-use application, and geographical region. Product segmentation reflects the varying levels of purity and chemical structure required for specific deposition processes, with Silane being the high-volume commodity precursor and Disilane representing the high-value specialty segment. The application analysis is critical as it dictates the required purity levels; semiconductor manufacturing demands the highest purity (electronic grade), significantly influencing pricing and production complexity. Understanding these segments is vital for suppliers to optimize production portfolios and tailor delivery logistics according to the end-user requirements, ranging from bulk transportation for large solar manufacturers to small, specialized cylinders for advanced IC fabs.

Further granularity in segmentation involves analyzing the market based on the grade of gas, distinguishing between solar-grade (SG) and electronic-grade (EG) silicon gases. The electronic grade segment typically commands a substantial price premium due to the rigorous purification processes required to remove trace impurities that could compromise IC performance. Geographic segmentation highlights the concentration of demand in specific manufacturing clusters, which influences strategic decisions regarding localized production and storage facilities. The synergy between segmentation analysis allows market players to accurately forecast demand shifts, allocate R&D resources toward high-growth application segments, and secure long-term supply agreements with major global semiconductor and solar manufacturers, thereby mitigating exposure to commodity price volatility and capturing niche, high-margin opportunities.

The value chain for silicon gases is intricate and begins with the upstream sourcing of metallurgical-grade silicon (MGS) or high-purity polysilicon, which are the fundamental raw materials. This upstream phase involves energy-intensive refining and purification processes, where major polysilicon producers dominate. The subsequent key step involves the complex chemical synthesis and distillation processes, often using MGS to generate Chlorosilanes (like Trichlorosilane), which are then further converted into high-purity Silane or used directly as precursors. This manufacturing stage requires specialized chemical plants and high-pressure processing equipment, placing a high barrier to entry and necessitating significant regulatory compliance, particularly concerning environmental emissions and hazardous material handling. Suppliers often employ integrated production models to maintain stringent quality control over purity specifications.

The middle segment of the value chain is dominated by large industrial gas companies or specialty chemical manufacturers responsible for further purification, analysis, packaging, and distribution. Ultra-high purity (UHP) requirements for electronic grade gases necessitate state-of-the-art purification techniques, often involving adsorption and cryogenic distillation, achieving purity levels exceeding 99.9999% (6N). The distribution channel is bifurcated into direct supply to large captive consumers (like massive semiconductor fabs or integrated solar facilities) and indirect sales through specialized gas distributors that manage smaller volumes, localized storage, and just-in-time delivery. Due to the hazardous nature of Silane and related gases, logistics require specialized, high-pressure cylinders or tube trailers, managed by experts in hazardous materials transportation, ensuring safety and gas integrity throughout the delivery route.

Downstream analysis focuses on the end-use applications, primarily semiconductor fabrication and solar PV manufacturing, which act as the final buyers. Direct sales typically involve long-term supply contracts between the gas producer and the fab owner, ensuring consistent material flow crucial for continuous high-volume production lines. Indirect distribution channels cater to smaller research facilities, pilot lines, or specialty chemical companies utilizing the silicon gases in niche applications. The performance and reliability of the silicon gas supply directly impact the yield and efficiency of the final electronic or solar devices, establishing a strong, interdependent relationship between the gas producers and the high-tech end-users, driving continuous collaborative efforts in quality improvement and process optimization.

The primary consumers of silicon gases are large-scale, capital-intensive manufacturing operations within the electronics and energy sectors, demanding consistent supply and ultra-high purity specifications. Within the semiconductor industry, potential customers include integrated device manufacturers (IDMs) like Samsung and Intel, and major pure-play foundries such as TSMC, which utilize electronic-grade Silane and Disilane for deposition processes critical to producing advanced microprocessors, memory chips, and analog devices. These companies represent the highest value segment due to the extreme purity requirements for 7nm nodes and beyond, where even trace impurities can lead to device failure. These customers often require specialized delivery systems and on-site gas management services provided by the silicon gas vendors.

Secondly, the rapidly expanding solar photovoltaic (PV) sector constitutes a massive volume-based customer base. Manufacturers of both crystalline silicon wafers (requiring Chlorosilanes for polysilicon production) and thin-film solar panels (requiring solar-grade Silane for amorphous silicon deposition) are significant buyers. Key customers include large Asian PV powerhouses like Trina Solar and LONGi Green Energy. While the purity requirements are slightly less stringent than the electronic grade, the volume demand is substantially higher, necessitating bulk gas transportation methods like large tube trailers or specialized rail cars. The cyclical nature of the solar industry means these customers' demand profiles can be sensitive to governmental subsidy programs and global trade policies.

A third segment comprises manufacturers of advanced display technologies, specifically those producing high-resolution LCD and modern OLED panels. These companies utilize silicon gases for depositing amorphous silicon (a-Si) or polycrystalline silicon (poly-Si) films that form the backplane transistors driving the pixels. Display manufacturers, such as LG Display and BOE Technology, require moderate to high purity gases, balancing cost efficiency with the need for reliable film properties. Additionally, specialized chemical companies and optical fiber manufacturers (using SiCl4 or SiF4) are critical niche customers, contributing to the diversity of the silicon gases market customer landscape, each segment requiring unique technical support and customized packaging solutions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1.85 Billion |

| Market Forecast in 2033 | $3.15 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | The Linde Group (Praxair), Air Liquide S.A., Versum Materials (Merck KGaA), REC Silicon, Shin-Etsu Chemical Co., Ltd., Wacker Chemie AG, Air Products and Chemicals Inc., Showa Denko K.K., Sichuan Kemei Gas Co., Ltd., Sumitomo Seika Chemicals Co., Ltd., Mitsubishi Materials Corporation, Taiyo Nippon Sanso Corporation, American Gas Products, Suzhou Jinhong Gas Co., Ltd., Hangzhou Zhongtai Chemical Co., Ltd., Nankai Chemical Industry Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Silicon Gases Market is primarily defined by advancements in precursor purification, handling systems, and novel deposition methodologies utilized by end-users. Ultra-high purity (UHP) requirements necessitate sophisticated purification technologies, particularly for electronic-grade Silane and Disilane. Technologies like cryogenic distillation, proprietary adsorption techniques, and advanced chromatographic separation are continuously refined to achieve impurity levels in the parts per billion (ppb) or even parts per trillion (ppt) range, essential for avoiding defects in sub-10nm semiconductor fabrication processes. Furthermore, continuous in-line analysis and real-time monitoring using advanced spectroscopy and trace gas analyzers are becoming standard to ensure gas quality consistency throughout the supply chain, moving beyond traditional batch testing methods.

In terms of end-use applications, the evolution of deposition technologies significantly shapes the demand for specific silicon gases. Chemical Vapor Deposition (CVD) and Plasma Enhanced Chemical Vapor Deposition (PECVD) remain the workhorse processes for bulk film deposition in solar and older semiconductor nodes, primarily relying on Silane. However, the move to highly conformal, thin films required for 3D architecture (e.g., 3D NAND, Gate-All-Around FETs) has accelerated the adoption of Atomic Layer Deposition (ALD) and area selective deposition (ASD). ALD necessitates specialized, often liquid-phase silicon precursors that can be delivered efficiently via advanced vaporization systems, increasing the demand for complex silicon compounds beyond traditional Silane, such as Disilane and specific organosilicon precursors (e.g., Tris(dimethylamino)silane - TDMAS).

A crucial technological development concerns safety and sustainability. Due to the pyrophoric and highly reactive nature of gases like Silane, safety technologies, including advanced gas cabinet design, leak detection sensors, and emergency abatement systems (scrubbers), are continually being improved to meet stringent industrial safety standards. Moreover, the focus on environmental responsibility has spurred R&D into Closed-Loop Recycling Systems (CLRS), aimed at recovering unreacted or waste silicon precursors, particularly from etching processes (like SiF4), and converting them back into usable forms. This technological trend not only addresses environmental concerns but also offers a pathway to stabilize raw material costs in the long term, positioning sustainability technology as a core competitive differentiator.

The primary applications driving Silane gas demand are semiconductor manufacturing, where it is critical for depositing silicon films in integrated circuits, and the solar photovoltaic (PV) industry, where it is used to produce thin-film solar cells efficiently.

The shift to smaller nodes (e.g., 7nm and below) drastically increases purity requirements for silicon gases (Electronic Grade), often demanding parts per trillion (ppt) level purity, as trace impurities can cause device defects and reduce yield in complex 3D transistor structures.

Asia Pacific (APAC) dominates the consumption of silicon gases, primarily due to the massive concentration of leading semiconductor foundries (Taiwan, South Korea) and the world's largest solar photovoltaic production capacity (China).

While both are silicon precursors, Disilane is preferred in advanced semiconductor manufacturing because it allows for high-quality silicon film deposition at significantly lower process temperatures compared to Silane, which is essential for thermally sensitive substrates and next-generation device structures.

The Silicon Gases market faces regulatory challenges centered on the safe handling, storage, and transport of hazardous, pyrophoric materials like Silane, requiring strict compliance with global chemical safety standards and specialized facility investments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.