ID : MRU_ 433698 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

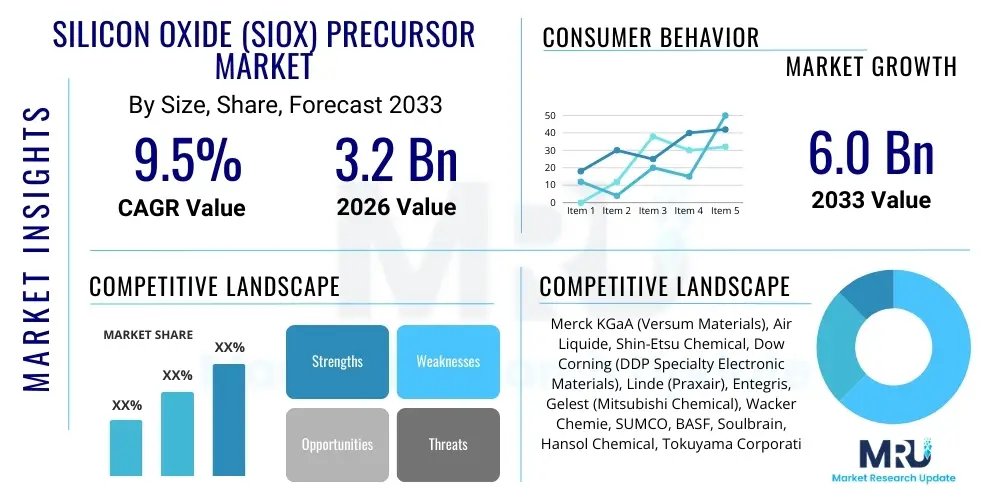

The Silicon Oxide (Siox) Precursor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 3.2 billion in 2026 and is projected to reach USD 6.0 billion by the end of the forecast period in 2033.

The Silicon Oxide (SiOx) Precursor Market encompasses specialty chemical compounds primarily utilized for depositing thin films of silicon dioxide (SiO2) in high-technology manufacturing processes. These precursors are critical components in the semiconductor industry, specifically for insulation layers, diffusion barriers, and passivation layers, as well as in the production of advanced solar cells, display panels, and optical coatings. The quality, purity, and deposition characteristics of these precursors—such as Tetraethyl Orthosilicate (TEOS), Tetramethoxysilane (TMOS), and other customized silanes—directly influence the performance and yield of microelectronic devices, making their supply chain a strategic focus for advanced economies.

Product description highlights the need for ultra-high purity (UHP) chemical delivery systems, especially for sub-10 nm semiconductor nodes. SiOx precursors facilitate the formation of dense, uniform, and conformal SiO2 films via techniques like Chemical Vapor Deposition (CVD), Plasma-Enhanced CVD (PECVD), and Atomic Layer Deposition (ALD). The shift towards ALD-compatible precursors, which offer superior step coverage and precise thickness control required for 3D NAND and advanced logic chips, is a defining trend in the market. Major applications include interlayer dielectrics (ILDs), shallow trench isolation (STI), hard masks, and gate oxide layers.

Key driving factors accelerating market growth include the relentless demand for smaller, faster, and more powerful electronic devices, necessitating greater density in memory and logic chips. Benefits derived from using these specialized precursors involve enhanced device reliability, reduced power consumption due to superior dielectric properties, and optimization of manufacturing costs through high-yield deposition processes. The global expansion of data centers, 5G technology, and the automotive sector's transition to electric vehicles further amplify the need for advanced SiOx thin films.

The Silicon Oxide Precursor Market is characterized by robust growth driven fundamentally by the scaling challenges in the semiconductor sector and significant investments in advanced manufacturing capacity, particularly in Asia Pacific. Business trends show a strong emphasis on R&D collaborations between precursor manufacturers and leading semiconductor foundries to develop novel chemistries that meet the thermal budget constraints and conformality requirements of highly complex 3D structures like 3D NAND flash and Gate-All-Around (GAA) FETs. Consolidation among specialty chemical suppliers focused on electronic materials is also evident, aiming to secure high-purity supply chains and intellectual property related to next-generation deposition techniques.

Regional trends indicate that the Asia Pacific region, primarily South Korea, Taiwan, China, and Japan, maintains overwhelming dominance due to the massive concentration of fabrication plants (fabs) and outsourced semiconductor assembly and test (OSAT) facilities. While North America and Europe continue to be crucial hubs for research and development and the manufacturing of high-end equipment, the bulk of precursor consumption remains anchored in APAC. However, recent geopolitical initiatives focusing on domestic semiconductor supply resilience (e.g., the US CHIPS Act and EU Chips Act) are beginning to spur significant investment in new fab construction in North America and Europe, projecting faster localized growth rates in these regions in the latter half of the forecast period.

Segment trends underscore the supremacy of the semiconductor application segment, which demands the highest purity levels and drives precursor innovation. Within types, high-performance silanes suitable for ALD and cyclic CVD processes are experiencing the fastest uptake, displacing traditional bulk chemicals like standard TEOS in advanced processing. The coating and thin film segment, while smaller, shows steady growth fueled by demand for anti-reflective and protective layers in solar photovoltaic (PV) modules and specialized industrial optics, requiring different purity and formulation characteristics compared to electronic-grade precursors.

Common user questions regarding AI's impact on the SiOx precursor market center around how generative AI and machine learning (ML) are optimizing manufacturing yields, predicting material performance, and accelerating the discovery of new precursor chemistries. Users frequently inquire about the integration of AI in R&D pipelines for designing molecules that offer better thermal stability or higher deposition rates. The key themes revolve around yield optimization, predictive maintenance of deposition equipment, and the massive underlying demand created by AI hardware itself. AI's requirement for immense computational power necessitates continuous advancement in chip density and performance, directly translating into higher demand for ultra-pure SiOx films used as high-quality dielectrics and isolation layers in advanced AI accelerators (GPUs, TPUs).

The implementation of predictive analytics and industrial internet of things (IIoT) frameworks in semiconductor fabs allows for real-time monitoring of precursor delivery systems and deposition chambers. This sophisticated monitoring minimizes material waste, detects micro-contaminants early, and stabilizes process parameters, thereby maximizing the utilization efficiency of expensive, high-ppurity SiOx precursors. Furthermore, AI-driven simulations can model the reaction kinetics and surface adsorption behaviors of new precursor molecules faster than traditional laboratory testing, significantly shortening the material qualification cycle necessary for next-generation manufacturing nodes.

While AI does not change the chemical properties of SiOx precursors directly, it fundamentally alters the economics and speed of their use and development. By enabling tighter tolerances and higher yields in the fabrication process, AI supports the scaling of advanced semiconductor architectures (such as stacked logic and high-bandwidth memory, HBM), which inherently require more intricate and perfectly deposited SiOx layers, sustaining the high growth trajectory of the precursor market.

The SiOx Precursor market is primarily driven by the exponential growth in global data generation and consumption, compelling semiconductor manufacturers to continuously innovate and increase chip density, which relies heavily on high-quality SiOx films. Restraints include the significant capital expenditure required for maintaining ultra-high purity standards throughout the supply chain and the complexity of synthesizing novel precursors that balance performance and stability. Opportunities lie in the emerging fields of advanced packaging (2.5D/3D integration), flexible electronics, and the deployment of wide-bandgap semiconductors (like SiC and GaN), where specialized SiOx protective layers are increasingly required. These forces combine to create a highly competitive yet lucrative environment where technological differentiation is paramount for market survival and growth.

Driving forces center on Moore's Law extension, specifically the shift to 3D architectural scaling (FinFET to GAA) and vertical NAND stacking, both of which require superior gap-fill and step coverage achievable only through advanced precursors used in ALD and cyclical deposition techniques. The massive global rollout of 5G infrastructure and the proliferation of IoT devices further expand the total addressable market for foundational semiconductor materials. Furthermore, environmental regulations encouraging the use of less hazardous or more efficient deposition processes also spur innovation toward precursors that react at lower temperatures or reduce hazardous byproduct generation.

Key restraints include volatility in the raw material supply chain (e.g., source silanes), extreme sensitivity to contamination requiring multi-billion-dollar purification facilities, and the high switching costs for semiconductor fabs once a precursor chemistry is qualified. The geopolitical risk associated with concentrated manufacturing capacities in East Asia also poses a structural vulnerability to the global supply of finished precursors. The long qualification cycles (often several years) for new electronic materials act as a significant barrier to entry for potential new suppliers, thus limiting competition and maintaining the stronghold of established players.

The SiOx precursor market segmentation offers a granular view of material utilization across different technological platforms, helping suppliers align R&D efforts with end-user demands. The market is primarily categorized based on chemical type (defining the material formulation), application (the device or process where the precursor is used), and deposition method (the specific equipment and technique employed). Understanding these segments is crucial as the performance requirements, such as conformal coverage, etch selectivity, and thermal budget constraints, vary widely between, for example, a high-density logic chip (requiring ALD) and a bulk solar cell (often using PECVD).

Segmentation by Type is essential as it reflects the technical maturity and cost profile of the precursors. Traditional liquid precursors like TEOS still hold significant volume in mature applications (older node devices, bulk coatings) due to their low cost and ease of handling. However, the rapidly growing segment involves proprietary, high-k precursors optimized for advanced deposition techniques, often requiring customized ligands to achieve specific film properties (density, stress, and low carbon content) essential for complex integration schemes found in 3D structures.

The Application segmentation clearly highlights the dominance of the Semiconductor industry, which acts as the innovation engine for the entire market, consuming the most technologically advanced and highest-purity materials. Growth rates in this segment are invariably higher than in other industrial applications. The Photovoltaics segment provides a secondary, high-volume market driven by global renewable energy policies, primarily utilizing SiOx precursors for anti-reflective coatings and passivation layers, though the purity requirements are less stringent than microelectronics.

The value chain for SiOx precursors is highly integrated and dependent on rigorous purification steps, beginning with the production of raw source materials, primarily metallurgical-grade silicon and chlorosilanes. The upstream analysis focuses on the few primary chemical manufacturers who synthesize and purify the basic silane intermediates (e.g., trichlorosilane, monochlorosilane). This stage requires heavy infrastructure investment and highly specialized chemical engineering expertise. Consolidation and control over raw material sourcing are critical factors influencing supplier pricing and stability, especially concerning ultra-high purity electronic-grade materials, where contamination at this initial stage is extremely difficult and costly to remove later.

The core of the value chain involves the synthesis of the final SiOx precursors (like TEOS or proprietary siloxanes) by specialty chemical companies. This middle stage includes complex purification processes, formulation tailored for specific deposition equipment (CVD or ALD), and specialized packaging (often in stainless steel canisters or bubblers) to maintain purity during transport. Quality control and rigorous analytical testing for parts-per-trillion impurities are defining features of this segment. Suppliers often work closely with equipment manufacturers (like Applied Materials or Lam Research) to ensure optimal delivery compatibility.

The downstream analysis centers on the end-users, primarily semiconductor foundries, memory manufacturers, and solar cell producers. Distribution channels are typically direct for large volume, electronic-grade products, emphasizing a secure, just-in-time delivery model due to the precursors’ sensitivity and limited shelf life. Indirect channels, involving specialized chemical distributors, cater mainly to smaller research labs, universities, or industrial coating applications. The trend towards regionalized manufacturing and shorter supply chains is influencing distribution logistics, promoting greater warehousing and localized buffer stocking near major semiconductor clusters.

The primary customers in the SiOx precursor market are large, vertically integrated electronics manufacturers and specialized fabrication facilities that rely on high-volume, high-precision thin-film deposition. These customers prioritize material performance metrics such as conformity, purity, and low process temperature compatibility over price, reflecting the enormous economic value tied to high semiconductor yields. Major buyers include integrated device manufacturers (IDMs) like Intel and Samsung, and pure-play foundries like TSMC, which continuously seek novel precursor chemistries to enable aggressive geometric scaling.

Secondary customer segments include advanced packaging houses and specialty component manufacturers. Companies involved in 2.5D/3D stacking require SiOx films for micro-bumping, redistribution layers (RDL), and through-silicon via (TSV) insulation. Additionally, the increasing demand for high-efficiency solar cells drives purchases in the photovoltaic sector, where SiOx precursors are used to form durable anti-reflection and surface passivation layers to maximize light capture and efficiency. These customers typically purchase precursors in larger bulk quantities but may tolerate slightly lower purity standards compared to sub-10nm logic fabs.

Other vital, though smaller, potential customers encompass manufacturers of advanced display technologies, particularly those utilizing OLED or MicroLED panels, where SiOx layers are essential for thin-film transistor (TFT) backplanes and encapsulation to protect sensitive organic layers from moisture and oxygen. The consistent global investment in these high-end display technologies ensures sustained, albeit specialized, demand for application-specific SiOx precursors. Research institutions and universities also constitute a minor but important customer base, driving early-stage adoption of experimental precursor chemistries.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.2 Billion |

| Market Forecast in 2033 | USD 6.0 Billion |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Merck KGaA (Versum Materials), Air Liquide, Shin-Etsu Chemical, Dow Corning (DDP Specialty Electronic Materials), Linde (Praxair), Entegris, Gelest (Mitsubishi Chemical), Wacker Chemie, SUMCO, BASF, Soulbrain, Hansol Chemical, Tokuyama Corporation, Adeka Corporation, JSR Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the SiOx precursor market is inextricably linked to advancements in thin-film deposition equipment, specifically the evolution of Chemical Vapor Deposition (CVD) techniques. Traditional CVD methods utilizing precursors like standard TEOS were foundational but are now increasingly supplemented or replaced by advanced variants such as Plasma-Enhanced CVD (PECVD) and High-Density Plasma CVD (HDPCVD). These variations allow for lower processing temperatures, which are critical for preserving the integrity of underlying metallic interconnects, and enable superior gap-fill capabilities required for features above 40nm technology nodes. The optimization of precursor stability and flow characteristics within these high-volume CVD processes remains a key area of incremental innovation for maximizing throughput and minimizing cost per wafer.

The most disruptive technological shift influencing the precursor landscape is the widespread adoption of Atomic Layer Deposition (ALD) and its cyclical variants (e.g., cyclical CVD). ALD relies on sequential, self-limiting surface reactions, offering unparalleled control over film thickness (down to atomic scale precision) and achieving near-perfect conformality, essential for filling the increasingly high-aspect-ratio features of 3D NAND flash memory (up to 200+ layers) and advanced logic gates (GAA architecture). This demand drives the need for entirely new classes of SiOx precursors that are highly reactive with the surface, possess suitable volatility, and are thermally stable during the sequential pulsing process, often requiring specialized, more expensive silicon compounds like DADBS or customized trisilanes.

Furthermore, significant R&D efforts are focused on developing materials compatible with area-selective deposition (ASD) and low-temperature processing. ASD is viewed as a crucial future technology for reducing complexity in patterning and etching processes, potentially requiring SiOx precursors with novel ligands that can react preferentially on specific surface chemistries. Low-temperature deposition, vital for flexible substrates and advanced packaging, pushes suppliers to synthesize precursors that can yield high-quality SiO2 films below 150°C, a considerable challenge given the energy typically required for Si-O bond formation. Success in these high-value segments determines future market leadership and dictates long-term chemical innovation strategies.

The Silicon Oxide Precursor market exhibits distinct consumption and manufacturing dynamics across key geographical regions, largely mirroring the global distribution of semiconductor manufacturing capacity.

The primary driver is the ongoing technological transition in semiconductor manufacturing towards 3D structures, specifically 3D NAND stacking and Gate-All-Around (GAA) logic transistors. These complex architectures require ultra-conformal and defect-free dielectric films, necessitating specialized precursors compatible with Atomic Layer Deposition (ALD).

The shift towards ALD forces manufacturers to develop proprietary precursors with higher volatility, precise thermal stability, and better surface reactivity than traditional CVD materials. This requires significant R&D investment and leads to higher average selling prices (ASPs) for these high-performance electronic-grade chemicals.

The Asia Pacific (APAC) region, driven by major semiconductor manufacturing hubs in Taiwan, South Korea, and China, overwhelmingly dominates the global consumption of SiOx precursors due to the high concentration of fabrication plants (fabs) and memory production facilities.

Purity is paramount; electronic-grade SiOx precursors must achieve parts-per-trillion (ppt) impurity levels. Even trace metallic contaminants can cause device failure and drastically reduce fabrication yields, making ultra-high purity synthesis and handling the most significant technological barrier and cost driver.

While traditional bulk TEOS is being replaced by advanced silanes in critical, sub-10nm feature depositions, TEOS remains highly relevant and widely used for non-critical, high-volume applications like blanket deposition, thick oxide layers, and applications where cost-efficiency and established processes are prioritized over atomic-scale conformality.

The rapid expansion of the global electronics sector, coupled with intense technological innovation in material science, ensures that the Silicon Oxide Precursor Market will remain a strategically important, high-growth segment within the broader specialty chemicals and electronic materials industry. Future market performance will be heavily influenced by the speed of global fab expansions and the success of material suppliers in developing new, cost-effective chemistries that meet the thermal and geometric constraints of next-generation logic and memory devices. Strategic alliances between chemical suppliers, equipment manufacturers, and foundries are expected to define the competitive landscape and technological breakthroughs in the coming decade, particularly concerning ALD and extreme high-aspect ratio processing required for 3D integration. Environmental concerns and the push for greener chemistries will also drive innovation towards precursors that allow for lower processing temperatures and utilize less toxic reaction byproducts, maintaining the market's dynamic nature. The integration of AI and machine learning into R&D processes is set to shorten the development lifecycle for these specialized materials, providing a competitive edge to companies capable of leveraging advanced data analytics to predict material behavior and optimize manufacturing processes within their supply chains. The long-term trajectory is overwhelmingly positive, tied inextricably to the foundational role of silicon dioxide films in all modern microelectronic devices. The critical nature of these materials means that supply chain resilience and assured access to high-purity precursors will remain a top priority for governments and large semiconductor conglomerates globally.

The demand for high-performance computing (HPC) and the build-out of crucial enabling infrastructure, such as fiber optics and high-speed data centers, further solidify the market's outlook. SiOx precursors are vital not only for the active silicon chips but also for passive components and protective coatings within the infrastructure ecosystem. As computing demands shift towards the edge and IoT devices become ubiquitous, the sheer volume of chips manufactured, regardless of node complexity, will necessitate substantial quantities of precursor materials. Furthermore, the specialized market segments like MEMS fabrication and sensors, which require highly precise thin films for critical functional layers, offer niche but rapidly growing opportunities for customized precursor formulations. Manufacturers who can diversify their offerings across high-end logic, bulk memory, and specialty component fabrication are best positioned to capitalize on the multifaceted growth drivers present across the market landscape. Successful navigation of strict regulatory hurdles, maintenance of intellectual property related to proprietary chemistries, and robust quality control systems are non-negotiable prerequisites for sustained success in this highly sophisticated materials market.

Future growth will hinge on breakthroughs related to low-temperature processing, enabling the integration of high-quality SiOx films onto temperature-sensitive substrates, opening doors to new applications in flexible displays and bio-integrated electronics. Specifically, the development of ALD precursors that can achieve high deposition rates while maintaining conformality at temperatures below 200°C is a major R&D focus. Market competitors are constantly investing in advanced purification techniques, such as distillation and chromatography, to push the limits of purity beyond parts-per-trillion levels, essential for mitigating defect density in sub-3nm chip production. The strategic importance of the SiOx precursor market is recognized globally, leading to increased domestic production initiatives across North America and Europe, aiming to mitigate dependency on the concentrated supply base in Asia, thereby influencing capital investment and technology transfer activities globally over the forecast period.

The segmentation by Type, encompassing liquid and gas phase delivery systems, will continue to evolve, with liquid precursors (such as advanced TEOS variants and siloxanes) remaining dominant due to easier handling and higher deposition yields in certain processes. However, the use of gaseous silanes, often specialized for vapor-phase deposition, will see accelerating growth in highly selective etching and deposition steps. The interplay between precursor chemistry and deposition hardware capabilities drives market dynamics, necessitating close collaboration between chemical suppliers and major equipment vendors like ASML, TEL, and KLA. This synchronized development ensures that new chemical solutions are immediately compatible with next-generation processing platforms, accelerating time-to-market for advanced nodes. Furthermore, sustainability considerations are increasingly impacting precursor selection, favoring materials with lower global warming potential (GWP) or those that enable processes that minimize water and energy consumption in the fab environment. This environmental consideration is becoming a significant competitive differentiator.

The competitive intensity in the SiOx precursor market is fundamentally driven by proprietary intellectual property (IP) surrounding the precursor molecule design and the purification techniques employed. Market leaders maintain their positions not just through volume capacity, but through patented chemistries that offer unique film properties—such as tunable dielectric constants, high density, and superior resistance to chemical etching—that are critical for specific steps in the semiconductor fabrication process. Pricing power remains skewed towards suppliers who provide qualified materials for the latest technology nodes, commanding a premium price due to the high barrier to entry and the extensive qualification costs borne by the foundries. This dynamic creates a dual market structure: a highly consolidated, high-margin market for ultra-pure, cutting-edge materials, and a more commoditized, cost-competitive market for standard, bulk-volume precursors used in legacy nodes and solar applications.

Regulatory scrutiny, particularly concerning chemical handling and transportation, presents a constant challenge. Given that many advanced silane precursors are highly volatile, pyrophoric, or toxic, adherence to strict global safety standards (e.g., REACH in Europe, OSHA in the US) adds significant operational overhead. Companies must invest heavily in specialized packaging, transportation logistics, and emergency response capabilities. The future success of market participants will therefore rely not only on scientific excellence in material synthesis but also on their ability to manage complex global supply chains that comply with varying international chemical control laws while ensuring zero tolerance for contamination throughout the delivery process to the end-user’s cleanroom environment. The long-term shift toward domestic manufacturing in North America and Europe will likely simplify logistical complexities but necessitates localized investment in the precursor purification and filling infrastructure.

The potential for market disruption also lies in the adjacent field of high-k dielectric materials. While SiOx remains the core insulation layer, alternatives or complementary materials (like hafnium oxide or aluminum oxide, also deposited using precursors) are crucial for specific applications (e.g., gate dielectrics). SiOx precursor manufacturers must continuously innovate to ensure compatibility and synergy with these co-deposited materials to maintain relevance across the complex, multi-layered chip architecture of modern electronic devices. The convergence of SiOx deposition with atomic layer etching (ALE) is another key technological area, where optimized SiOx films must exhibit precise etch selectivity, demanding meticulous control over the precursor reaction mechanisms and film density.

Investment in capacity expansion by key players is predominantly centered in strategic locations within Asia Pacific, particularly China, to service the growing local foundry market, and in regions where new geopolitical incentives are fostering fab construction. This capital expenditure is necessary to keep pace with the increasing wafer start volumes globally, which translates directly into higher consumption of all process chemicals, including SiOx precursors. Furthermore, the push for environmental, social, and governance (ESG) compliance is influencing R&D, favoring precursors that enable high yield while minimizing the environmental footprint of the semiconductor manufacturing process, for instance, by reducing the energy required for vacuum pumps or plasma generation during deposition. This holistic view of sustainability is becoming integral to vendor selection criteria among major semiconductor manufacturers.

The market analysis reveals a strong correlation between the capital expenditure (CapEx) cycle of global semiconductor manufacturers and the immediate demand for advanced SiOx precursors. When foundries announce and initiate construction of new fabs (a process taking 3-5 years), it creates a predictable future surge in demand for the specialized precursors necessary to ramp up production. Therefore, precursor suppliers must maintain proactive capacity planning and engage in long-term supply agreements to mitigate future bottlenecks. The sensitivity of the market to global macroeconomic conditions, trade disputes, and geopolitical tensions remains a critical risk factor, given the concentrated production base and the international nature of the final electronic product market. Successful companies must employ robust risk management strategies, including dual sourcing and geographically diversified manufacturing sites, to ensure business continuity.

Finally, the application segment outside of core semiconductors, such as advanced coatings for specialized optics and high-efficiency mirrors, provides a stabilizing factor against the volatile semiconductor cycle. These industrial applications, while having lower purity standards, offer high-volume, steady demand driven by sectors like aerospace, automotive lighting, and specialized consumer electronics displays. Continuous innovation in precursor chemistry tailored for low-temperature atmospheric pressure deposition (APD) or inkjet printing techniques is opening up new revenue streams in these diversified coating markets, further securing the market's long-term growth profile and diversifying the revenue base of key suppliers beyond the pure electronic materials sector.

The critical importance of the SiOx layer extends into the realm of advanced power electronics, particularly Silicon Carbide (SiC) and Gallium Nitride (GaN) devices, which operate under extreme voltage and temperature conditions. SiOx films are essential for gate oxide and passivation layers in these devices, requiring precursors that can form highly robust, thermally stable interfaces with these exotic substrates. The rapid adoption of SiC and GaN in electric vehicles and 5G power systems is creating a specialized, high-growth sub-segment within the SiOx precursor market. Manufacturers must develop specific chemistries optimized for these wide-bandgap materials, often requiring precursors capable of handling higher thermal budgets during deposition compared to standard silicon CMOS processes. This technological diversification ensures that the overall market remains highly resilient and adaptive to shifting electronic materials trends. The precision demanded in GaN and SiC passivation further validates the premium pricing strategy adopted by leading specialty chemical providers in this sector.

The role of specialized containers and delivery systems, managed by companies like Entegris, is equally critical to the precursor value chain. The precursor itself is only effective if it can be delivered to the deposition chamber with absolute purity and controlled flow. Therefore, innovation in advanced canisters (bubblers), purification filters, and fluid handling systems that prevent outgassing or contamination during storage and use are essential technological enablers. Suppliers of precursors often integrate these specialized delivery mechanisms into their product offering, creating a bundled solution that ensures performance consistency at the point of use. This highlights the interdependence between specialty chemical providers and fluid management solution experts in maintaining the stringent quality standards required by modern semiconductor fabs. The logistics of hazardous material transportation, especially across international boundaries, further elevates the complexity and costs associated with maintaining an efficient supply chain.

The competitive environment is characterized by intense focus on total cost of ownership (TCO) for end-users. While precursor purity drives the initial cost, factors such as deposition rate, material utilization efficiency, and the subsequent reduction in defect rates determine the TCO. Precursor manufacturers differentiate themselves by offering high-efficiency materials that enable faster process times and superior film properties, ultimately lowering the overall operational costs for the semiconductor manufacturer, despite a higher unit cost for the chemical itself. This focus on performance value over absolute material cost underscores the specialized nature of the electronic materials supply chain. This value proposition is especially relevant in mass memory production (3D NAND), where minor improvements in deposition speed or material efficiency can translate into millions of dollars in savings or added revenue due to increased output.

Finally, the market’s reliance on intellectual property protection remains a pivotal constraint and advantage. Patent portfolios covering novel precursor molecules, synthesis routes, and purification technologies serve as significant barriers to entry. Companies actively involved in cross-licensing and collaborative research with leading universities and national laboratories are better positioned to secure a competitive advantage. The ability to quickly iterate and qualify next-generation chemistries, often years ahead of the actual node requirement, is critical for securing future design wins with major foundries. As global competition intensifies and geopolitical factors emphasize localized manufacturing, the strategic importance of proprietary SiOx precursor technology becomes even more pronounced in maintaining national technological superiority in advanced microelectronics fabrication.

The demand stability in the photovoltaic (PV) segment, though less purity-demanding than electronics, provides essential scale. SiOx precursors are key in the manufacturing of passivated emitter rear contact (PERC) cells and more advanced heterojunction (HJT) and TOPCon cells, serving as effective passivation and anti-reflective coatings. The sustained global commitment to renewable energy deployment ensures that this segment will provide steady, high-volume consumption, balancing the cyclical nature of the microchip industry. The key requirement here is maximizing deposition throughput and minimizing cost, contrasting sharply with the ultra-high purity, low-volume requirements of leading-edge semiconductor nodes, forcing precursor suppliers to manage distinct product lines and cost structures effectively across their portfolio. This diversification buffers against slowdowns in any single end-user market.

In summary, the Silicon Oxide Precursor Market is a sophisticated intersection of advanced chemistry and materials engineering, inextricably linked to the trajectory of modern computing and electronics. Driven by complexity and sheer volume, the market demands continuous innovation, extremely stringent quality control, and robust, resilient supply chain management. The future growth will be dominated by precursors suitable for ALD and complex 3D structures, supported by massive global investment in new semiconductor fabrication capabilities spurred by both market demand (AI, 5G) and geopolitical strategy (supply chain resilience). Companies that master both the synthesis of novel, high-performance chemistries and the logistical complexities of global high-purity delivery will solidify their leadership position in this essential segment of the electronics materials industry.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.