ID : MRU_ 435532 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

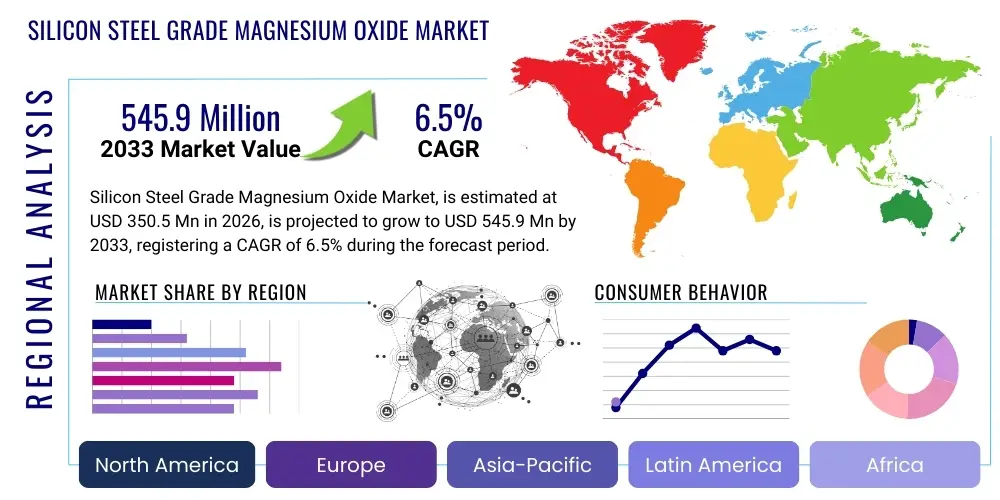

The Silicon Steel Grade Magnesium Oxide Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 350.5 Million in 2026 and is projected to reach USD 545.9 Million by the end of the forecast period in 2033.

The Silicon Steel Grade Magnesium Oxide (MgO) market focuses on highly specialized magnesium oxide used primarily as an insulating and protective coating during the annealing process of electrical steel, specifically grain-oriented electrical steel (GOES). This specialized MgO acts as a separating agent, preventing adjacent layers of silicon steel from welding together during high-temperature annealing. Crucially, the magnesium oxide reacts chemically with the silicon content in the steel to form a thin, highly resistive layer of forsterite (Mg2SiO4). This forsterite film is essential as it imparts the necessary insulation resistance required to minimize eddy current losses within transformer cores, thereby enhancing the overall energy efficiency of electrical infrastructure.

The primary benefit derived from utilizing high-purity, silicon steel grade MgO is the significant improvement in the magnetic properties of the finished electrical steel. The resultant forsterite film creates beneficial mechanical tension on the steel surface, which aids in optimizing the domain structure of the silicon steel crystals, leading to reduced core losses and improved permeability. Applications are predominantly centered around the manufacturing of high-efficiency transformers, large power generators, and various electromagnetic devices where minimizing energy waste is paramount. The increasing global focus on reducing carbon footprints and transitioning to smarter, more efficient electrical grids directly fuels the demand for premium quality grain-oriented electrical steel, consequently boosting the market for specialized MgO.

Driving factors for this market include stringent energy efficiency regulations implemented worldwide, particularly the Minimum Energy Performance Standards (MEPS) for transformers. Furthermore, rapid global urbanization and the continuous expansion and modernization of power transmission and distribution infrastructure necessitate substantial quantities of high-performance electrical steel. The development of Ultra-High Voltage (UHV) transmission networks in major economies like China and India requires exceptionally low-loss transformer cores, demanding the highest grades of Silicon Steel Grade Magnesium Oxide. The stability, consistency, and purity of the MgO powder are critical requirements that differentiate key market players.

The Silicon Steel Grade Magnesium Oxide market demonstrates robust growth, primarily propelled by global investment in energy-efficient power infrastructure and regulatory pressures mandating higher efficiency standards for electrical equipment. Business trends indicate a strong emphasis on product customization, with manufacturers increasingly offering tailored MgO grades optimized for specific silicon steel chemistries and annealing procedures (e.g., standard annealing versus high-permeability annealing processes). Consolidation among major electrical steel producers influences procurement strategies, favoring large-scale, reliable suppliers capable of ensuring consistent quality and global supply chain resilience. Innovation focuses on improving the dispersibility and specific surface area of the MgO powder to ensure a uniform coating, which is crucial for achieving superior magnetic properties in the final steel product.

Regional trends highlight the Asia Pacific (APAC) region as the undisputed leader in both consumption and production. China, being the world's largest producer and consumer of grain-oriented electrical steel, dominates the market landscape. Significant infrastructural projects in India and Southeast Asian countries further contribute to APAC’s rapid growth. North America and Europe, while mature markets, show steady demand driven by the replacement of aging power grids with new, highly efficient transformers, coupled with the ongoing expansion of renewable energy generation facilities requiring reliable grid connection components. Regulatory frameworks such as the European Union's Ecodesign Directive continuously reinforce the demand for high-grade insulation materials like Silicon Steel Grade MgO.

Segmentation trends reveal that the High Purity Grade segment is experiencing faster adoption compared to the Standard Grade. This shift is a direct response to the technological evolution of electrical steel toward higher permeability grades (Hi-B steel) and the associated need for materials that guarantee minimal impurities which could negatively affect magnetic performance. Application-wise, Grain-Oriented Electrical Steel (GOES) remains the core demand driver, accounting for the vast majority of consumption due to its essential role in transformer core manufacturing. Furthermore, there is a subtle but growing trend towards specialty applications requiring highly reactive MgO, driving research and development into novel synthesis methods such as precipitation and calcination techniques optimized for controlled particle morphology.

Common user questions regarding AI's impact on the Silicon Steel Grade Magnesium Oxide market often center on whether artificial intelligence can revolutionize the quality control processes, optimize complex synthesis routes for higher purity MgO, or predict demand fluctuations tied to global transformer production cycles. Users are keen to understand how machine learning models can be utilized to analyze input raw material composition (e.g., magnesite ore) and instantly adjust calcination parameters (temperature, duration, atmosphere) to ensure the ultra-high consistency required for electrical steel applications. Furthermore, there is interest in using AI for predictive maintenance in the complex annealing furnaces where the MgO coating is applied, thus reducing material wastage and downtime. The overarching expectation is that AI integration will lead to unprecedented levels of material consistency, supply chain predictability, and reduced production costs, making high-grade MgO manufacturing significantly more efficient and reliable.

The market dynamics are governed by a complex interplay of internal and external forces. Key drivers include mandatory global energy efficiency directives (like those from the IEC and various national bodies) compelling utility companies and transformer manufacturers to adopt low-loss materials. The massive global push for grid modernization, particularly in developing economies, further accelerates the demand. However, the market faces significant restraints, primarily the extreme sensitivity of global steel production to economic cycles, leading to volatile demand patterns for specialty raw materials. Furthermore, the capital-intensive nature and energy consumption inherent in high-purity MgO production present barriers to entry. Opportunities lie in developing ultra-low-dust MgO formulations and integrating circular economy principles into raw material sourcing and waste reduction.

The foremost impact forces shaping this market are technological evolution within the electrical steel industry and geopolitical stability affecting trade routes for key raw materials (magnesite ore). Technological advancements, such as the increasing utilization of amorphous metals or alternative insulation techniques in certain transformer types, pose a long-term substitution threat, though the GOES/MgO system remains dominant for large power transformers. Geopolitical risk impacts the supply chain, as high-grade natural magnesite is geographically concentrated. The competitive landscape is characterized by intense focus on purity and particle characteristics, where failure to meet stringent specifications leads to immediate rejection by steel mills, demonstrating the high impact of quality control on market share.

The reliance on the performance of the final product—the transformer—means that even minor deviations in MgO quality can lead to significant financial losses for the steel manufacturer. This zero-tolerance approach to quality elevates the impact of consistency and reliability among suppliers. Additionally, environmental, social, and governance (ESG) factors are exerting increasing influence. Customers are prioritizing suppliers who demonstrate sustainable mining practices and lower carbon footprints during the calcination process. This trend forces producers to invest in energy-efficient furnaces and traceable raw material sourcing, fundamentally altering operating procedures and investment priorities within the sector.

The Silicon Steel Grade Magnesium Oxide market is segmented based on the product characteristics (Type), its intended use in the steel manufacturing process (Application), and the ultimate purchaser in the electrical ecosystem (End-User). Segmentation by Type, dividing the market into High Purity Grade and Standard Grade, reflects the varying requirements of electrical steel producers. High Purity Grade MgO, characterized by minimal impurities (especially boron, sulfur, and iron oxides) and optimized particle size distribution, is essential for manufacturing the most advanced, high-permeability GOES used in premium power transformers where minimizing core losses is critical. Standard Grade MgO caters to general-purpose GOES and other specialized non-oriented electrical steel applications where performance requirements are slightly less stringent.

The Application segmentation distinguishes the consumption based on the type of electrical steel being produced. Grain-Oriented Electrical Steel (GOES) dominates this segment, as MgO is indispensable in forming the necessary forsterite film that induces beneficial tensile stress for magnetic alignment. While Non-Grain-Oriented Electrical Steel (NGOES) typically uses alternative insulation coatings, there are specific NGOES grades or secondary industrial applications where MgO is utilized for surface conditioning or thermal stability. The overwhelming reliance on GOES ensures this segment remains the primary revenue generator and growth driver for the MgO market.

Analysis of the end-user base provides insight into the final demand structure. Transformer manufacturers are the dominant end-users, either directly purchasing MgO or, more commonly, indirectly through their demand placed on specialized steel mills. The increasing global need for replacement transformers due to aging grids, combined with the demand for new units to support renewable energy integration and grid expansion, solidifies this segment's importance. Power generation infrastructure (generators and reactors) and the specialized demands arising from the growing Automotive Industry (e.g., high-performance components for electric vehicle charging infrastructure) also represent niche but high-growth end-user segments.

The value chain for Silicon Steel Grade Magnesium Oxide is linear and highly dependent on upstream raw material quality and specialized processing. Upstream analysis begins with the mining and sourcing of high-purity natural magnesite (MgCO3) or the chemical synthesis of magnesium hydroxide. The quality of the raw ore is the single most critical factor, as impurities translate directly into defects in the final steel product. Suppliers must ensure rigorous beneficiation processes to remove undesirable elements like calcium and iron. This material then undergoes high-temperature calcination (sintering) to convert it into dead-burned or lightly-burned magnesium oxide (MgO), where precise temperature control is paramount for achieving the required crystal structure and reactivity suitable for electrical steel applications. Key upstream challenges include geopolitical risk associated with concentrated magnesite deposits and managing the high energy costs of calcination.

Midstream activities involve specialized processing, including precise milling and micronization to achieve the required particle size distribution (often in the nanometer to sub-micron range) and surface area, followed by rigorous packaging under moisture-controlled conditions. Distribution channels are highly specialized, often relying on direct sales or long-term supply contracts between the MgO producer and the major electrical steel mills (e.g., Nippon Steel, POSCO, ThyssenKrupp). Due to the technical nature and high volume requirement, indirect distribution through generalized chemical distributors is rare, emphasizing the direct relationship and technical support required between manufacturer and end-user. The indirect channel occasionally involves brokers for raw magnesite but rarely for the finished, specialized MgO powder.

Downstream analysis focuses entirely on the application process within the steel mill. The MgO is mixed into a slurry, applied uniformly to the surface of the cold-rolled silicon steel strip, and then subjected to the critical high-temperature annealing process. The quality of the MgO coating dictates the final magnetic performance and insulation characteristics of the GOES. End-users, predominantly transformer manufacturers, indirectly influence the specifications of the MgO by demanding electrical steel with increasingly lower core losses. The high cost of quality failure necessitates extremely tight integration and communication between steel mills and MgO suppliers regarding lot testing, material handling, and technical performance validation.

Potential customers for Silicon Steel Grade Magnesium Oxide are highly concentrated within the global metallurgical and electrical manufacturing industries. The primary buyers are large, integrated steel manufacturers specializing in the production of electrical steel, specifically those operating dedicated lines for Grain-Oriented Electrical Steel (GOES). These steel mills, such as those operated by major conglomerates in Asia and Europe, require vast quantities of consistently high-purity MgO to ensure the high-efficiency coating necessary for premium transformer cores. Their buying decisions are based less on price and overwhelmingly on material performance, stability of supply, and adherence to ultra-strict impurity standards, making them highly demanding customers requiring deep technical partnerships.

Secondary potential customers include smaller, specialized steel processors or rolling mills that might focus on non-oriented electrical steel (NGOES) for specialized motor cores or specific industrial heating elements, though their volume requirements are significantly lower than GOES producers. Furthermore, research institutions and pilot plants engaged in developing next-generation magnetic materials or advanced coating techniques represent niche customers for small-volume, highly specialized grades of MgO powder. The direct end-users, such as global transformer manufacturers (e.g., Siemens Energy, ABB, GE), are influential potential customers in an indirect sense, as their stringent requirements for transformer core loss performance dictate the quality specifications passed down through the steel supply chain, essentially acting as the ultimate determinant of demand quality.

The rapidly expanding Electric Vehicle (EV) supply chain is emerging as a new potential customer base. While the core GOES market remains focused on utility-scale transformers, the increasing need for high-performance, compact transformers and inductors used in fast-charging infrastructure, high-frequency motor cores, and high-density power converters creates a specialized demand segment. These applications require electrical steel designed for different operating conditions (e.g., higher frequencies), potentially necessitating custom MgO grades optimized for these unique surface reactions and insulation requirements. Therefore, manufacturers focused on the electrification movement represent a future high-growth segment for specialized MgO formulations.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 350.5 Million |

| Market Forecast in 2033 | USD 545.9 Million |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Magnezix GmbH, Israel Chemicals Ltd. (ICL), Kumasas Magnesite Industry Inc., Magnesita Refratários S.A., Martin Marietta Materials, Inc., Premier Magnesia LLC, RHI Magnesita N.V., Sibelco, Grecian Magnesite S.A., Ube Industries, Ltd., Konoshima Chemical Co., Ltd., Liaoning Chaoyang Magnesite Co., Ltd., Puyang Refractories Group Co., Ltd., Dandong Jinyi Chemical Co., Ltd., Jinchuan Group Co., Ltd., Calix Limited, Nedmag B.V., Xinghai Magnesium Materials. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for Silicon Steel Grade Magnesium Oxide centers primarily on achieving ultra-high purity, controlling particle morphology, and ensuring high reactivity. The core technology involves the specialized calcination of raw magnesite or synthetic precursors. Advanced rotary kilns and shaft furnaces are employed, utilizing precise temperature profiles (often exceeding 1600°C for dead-burned magnesia) and controlled atmospheres to yield the desired crystalline phase and density. Modern advancements focus on minimizing impurities, especially trace elements like boron, which severely hinder the formation of the desired forsterite layer and negatively impact magnetic properties. Techniques such as selective flotation and acid leaching are increasingly used upstream to purify raw magnesite before the calcination stage, thereby enhancing the final product quality.

Another critical technological area is particle size engineering. Silicon steel applications require MgO particles that are uniformly sized and distributed, typically in the range of a few micrometers, to ensure a homogeneous coating layer on the steel surface. This uniformity is achieved through advanced grinding and classification technologies, including specialized jet mills and air classifiers, which prevent agglomeration and maintain a narrow size distribution profile. Manufacturers are also developing surface modification technologies, sometimes involving minor doping elements (though rare for pure GOES applications), to enhance the dispersibility of the MgO powder in aqueous or solvent-based slurries used in the steel coating process. This ensures better adhesion and minimal defects during the critical annealing step.

The technology landscape is increasingly integrating automation and analytical chemistry. High-precision X-ray diffraction (XRD) and scanning electron microscopy (SEM) are standard tools used for real-time quality assurance, ensuring that the crystal structure (periclase content), particle shape, and absence of impurities meet the exceptionally tight specifications demanded by electrical steel mills. Furthermore, the development of synthetic magnesium oxide, produced through chemical precipitation methods (e.g., from magnesium chloride brines or seawater), represents a technological path toward potentially higher, more controllable purity levels than achievable with natural magnesite. While synthetic routes are often more costly, they offer guaranteed consistency, which is invaluable for high-end GOES production, driving technological investments in precipitation chemistry and subsequent drying processes.

The primary function of Silicon Steel Grade Magnesium Oxide (MgO) is to act as a separator coating during the high-temperature annealing of grain-oriented electrical steel (GOES). It reacts with the silicon in the steel to form a thin, highly insulative forsterite layer (Mg2SiO4), which minimizes eddy current losses, enhances magnetic properties, and improves overall transformer energy efficiency.

High purity is crucial because impurities, particularly boron, sulfur, and iron oxides, interfere with the desirable formation of the forsterite layer and negatively affect the surface tension and magnetic properties of the GOES. Ultra-high purity MgO ensures uniform insulation resistance, which is vital for achieving the lowest possible core losses in premium transformers.

The Asia Pacific (APAC) region, specifically China, dominates the consumption of Silicon Steel Grade Magnesium Oxide. This is attributable to APAC being the global hub for grain-oriented electrical steel production and experiencing massive, ongoing investments in power transmission and distribution infrastructure projects.

Key technological challenges include achieving ultra-fine, uniform particle size distribution for homogeneous coating, maintaining extreme chemical purity by eliminating trace elements (like boron) that act as inhibitors, and managing the high energy costs and environmental footprint associated with high-temperature calcination processes.

Future growth is primarily driven by the High Purity Grade segment, fueled by the rising global demand for ultra-high permeability electrical steel (Hi-B steel) necessary for meeting increasingly stringent energy efficiency regulations (MEPS) for large power transformers and grid modernization projects globally.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.