ID : MRU_ 431428 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

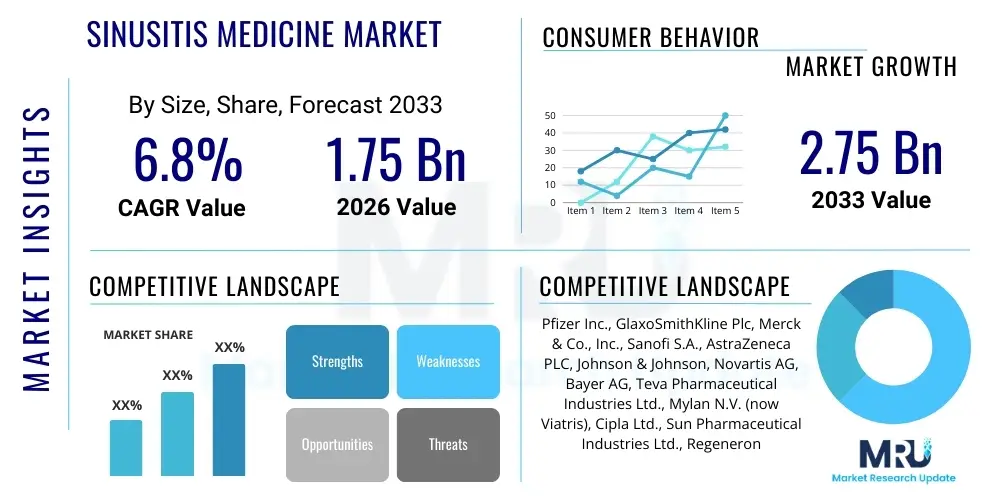

The Sinusitis Medicine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 1.75 Billion in 2026 and is projected to reach USD 2.75 Billion by the end of the forecast period in 2033.

The Sinusitis Medicine Market encompasses a wide range of pharmaceutical products designed for the treatment and management of sinusitis, an inflammatory condition affecting the lining of the sinuses. Sinusitis, often classified as acute (lasting less than four weeks), subacute (four to twelve weeks), or chronic (lasting twelve weeks or more), is typically caused by viral, bacterial, or fungal infections, or allergic reactions. The primary objective of sinusitis treatment is to reduce mucosal inflammation, promote drainage, manage pain, and eliminate the underlying infection. The therapeutic landscape includes over-the-counter (OTC) decongestants and pain relievers, along with prescription medications such as antibiotics, nasal corticosteroids, antihistamines, and increasingly, specialized biologics for severe chronic cases. The necessity for effective treatments is underscored by the high global prevalence of respiratory allergies and upper respiratory tract infections, which serve as major precursors to sinusitis.

The driving factors for market expansion are multifaceted, anchored significantly in rising air pollution levels worldwide, which exacerbate respiratory symptoms and inflammation, leading to chronic sinus issues. Additionally, growing awareness regarding the adverse effects of untreated sinusitis, which can potentially lead to severe complications like orbital cellulitis or intracranial infections, is boosting diagnostic rates and treatment seeking behavior. Product development focuses heavily on improving drug delivery systems, particularly nasal sprays that offer targeted action with fewer systemic side effects, thereby enhancing patient compliance and therapeutic efficacy. Key applications of these medicines span primary care settings, specialized ENT clinics, and critical care units, catering to a broad demographic susceptible to seasonal and environmental triggers.

The benefits derived from advanced sinusitis medicines include rapid symptomatic relief, improved quality of life by reducing facial pain and nasal congestion, and preventing the transition from acute to chronic disease states. The ongoing shift toward combination therapies, pairing nasal steroids with saline rinses or long-term macrolides, represents a strategic move to manage complex chronic rhinosinusitis (CRS). Furthermore, the introduction of novel biological agents targeting specific inflammatory pathways (like IgE or IL-5 inhibitors) in patients with severe, often eosinophilic, CRS, is opening lucrative opportunities for high-value segments within the market. This innovation landscape, coupled with the increasing global geriatric population more susceptible to respiratory infections, solidifies the market's trajectory of consistent growth.

The Sinusitis Medicine Market is experiencing robust growth driven by high incidence rates of allergic rhinitis and upper respiratory tract infections, particularly in densely populated and industrialized regions. Key business trends indicate a significant strategic shift away from broad-spectrum antibiotics due to rising antimicrobial resistance, favoring targeted anti-inflammatory agents and personalized medicine approaches. The market sees increased investment in nasal drug delivery technologies, including novel pressurized sprays and mucoadhesive gels, enhancing bioavailability and reducing systemic exposure. Pharmaceutical companies are focusing on lifecycle management of established brands while simultaneously investing in biologics development to address the recalcitrant subset of chronic rhinosinusitis patients unresponsive to conventional treatments. Mergers and acquisitions are common, aimed at consolidating niche expertise in respiratory drug formulation and expanding geographic distribution networks, particularly into emerging economies where infrastructure development is accelerating healthcare accessibility.

Regionally, North America and Europe maintain dominance owing to sophisticated healthcare infrastructure, high healthcare expenditure, and established guidelines for sinusitis management. However, the Asia Pacific region is forecast to demonstrate the highest Compound Annual Growth Rate, spurred by escalating levels of air pollution, urbanization, and a large patient pool coupled with improving diagnosis rates and increasing affordability of generic medication. The regulatory environment in major markets, particularly the U.S. and E.U., plays a crucial role, influencing the speed of approval for new combination drugs and advanced delivery systems. Regional trends also show varying levels of reliance on traditional herbal and complementary medicines for symptomatic relief, creating unique competitive dynamics that necessitate localized marketing and product positioning strategies for multinational corporations.

Segment trends reveal that the corticosteroids drug class segment holds a substantial share, primarily due to their proven efficacy in reducing inflammation, a core component of sinusitis pathology. The growing concern over antibiotic overuse has restrained the growth of the antibiotic segment, pushing physicians toward emphasizing nasal irrigation and topical steroid use as first-line treatments. Furthermore, the chronic sinusitis segment is projected to grow faster than the acute segment, reflecting the long-term management needs and higher prescription volumes associated with persistent symptoms. Within distribution channels, retail pharmacies and drug stores remain pivotal, although the rise of e-commerce platforms and online pharmacy services is creating accessible alternatives for OTC products, particularly decongestants and saline rinses, catering to consumer convenience and driving indirect sales growth.

Common user questions regarding AI's impact on the Sinusitis Medicine Market revolve around its ability to revolutionize diagnosis, personalize treatment, and accelerate the discovery of new therapeutic compounds. Users frequently inquire if AI algorithms can accurately differentiate between viral, bacterial, and allergic sinusitis using imaging (CT scans) or patient symptom data, thereby mitigating the current reliance on empirical antibiotic prescribing. There is significant interest in how machine learning can analyze vast genomic and proteomic data sets associated with chronic rhinosinusitis (CRS) to identify novel biomarkers that predict disease severity or responsiveness to specific biologics, moving away from the often lengthy and trial-and-error approach currently prevalent. Furthermore, patients and healthcare providers seek clarification on AI-driven platforms for remote monitoring of symptom progression and adherence to complex medication regimens, aiming to improve long-term outcomes for chronic sufferers.

The application of Artificial Intelligence and machine learning in the sinusitis therapeutic area promises substantial improvements across the entire healthcare spectrum, from initial patient intake to long-term disease management. In diagnostics, AI algorithms are being trained on large datasets of CT scans and endoscopic images to rapidly identify mucosal thickening, polyps, and structural abnormalities characteristic of chronic sinusitis, often with greater consistency and speed than human review, leading to earlier and more accurate diagnosis. This improved diagnostic precision is vital for stratifying patients into appropriate treatment pathways, ensuring that antibiotics are reserved for confirmed bacterial infections and reducing unnecessary systemic exposure.

From a research and development standpoint, AI significantly enhances drug discovery processes by analyzing inflammatory pathway data and predicting the efficacy and toxicity profiles of potential new drug candidates targeting sinus inflammation. Specifically, generative AI models can help design novel molecules that interact optimally with identified disease targets, potentially leading to faster development cycles for next-generation nasal steroids or targeted biologic therapies. For treatment optimization, AI systems analyze patient history, environmental exposure, and response to previous treatments to recommend the most effective therapeutic plan, paving the way for truly personalized medicine in complex conditions like CRS with nasal polyps, thereby maximizing patient benefit and minimizing treatment costs associated with ineffective regimens.

The Sinusitis Medicine Market's trajectory is primarily shaped by the interplay of persistent environmental triggers, escalating healthcare expenditure, and regulatory constraints surrounding antibiotic use. Drivers include the high global prevalence of allergic rhinitis and asthma, which strongly correlate with chronic sinusitis development, alongside increasing awareness and diagnosis rates facilitated by improved primary care access. Restraints largely center on the global public health crisis of antimicrobial resistance, which mandates cautious prescribing and limits the long-term viability of antibiotic-based therapies. High treatment costs, particularly associated with innovative biologic drugs used for severe refractory cases, also act as a constraint, limiting access in cost-sensitive markets. Opportunities lie chiefly in the realm of advanced drug delivery systems, particularly localized nasal therapies that offer improved efficacy and reduced systemic side effects, and the development of cost-effective, non-antibiotic treatments tailored for chronic inflammation management, such as immunomodulators.

Drivers: The sustained deterioration of air quality globally, driven by industrial emissions and traffic pollution, acts as a perpetual irritant to the nasal mucosa, significantly increasing the incidence and severity of sinusitis. Furthermore, demographic shifts, including the aging population becoming more susceptible to respiratory illnesses and compromised immune function, contribute to a larger pool of patients requiring both acute and long-term medication. The continuous innovation in diagnostic technology, such as improved endoscopic techniques and imaging, ensures that complex cases are identified earlier, leading to increased demand for specialized prescription medicines. Government initiatives and public health campaigns focused on respiratory health and the proper management of allergies also indirectly fuel the demand for effective sinusitis treatments, promoting timely consultation and adherence to therapeutic protocols.

Restraints: A significant challenge is the widespread misuse and overuse of antibiotics in treating acute sinusitis, which is predominantly viral, accelerating bacterial resistance and diminishing the effectiveness of first-line treatments. This necessity to curb antibiotic prescription forces providers to seek non-antibiotic alternatives, sometimes complicating acute management. Additionally, many OTC decongestants carry warnings about rebound congestion (rhinitis medicamentosa) following prolonged use, requiring careful patient education and limiting the sustained revenue generation from this subsegment. High research and development costs required for novel biologics mean that these highly effective treatments remain expensive, creating major accessibility barriers in developing nations and leading to payer resistance in established markets, which restricts overall market penetration.

Opportunities: The greatest potential for market growth resides in the development and commercialization of new generation biologics and monoclonal antibodies tailored for specific inflammatory endotypes of chronic rhinosinusitis, providing therapeutic options for patients who fail standard medical and surgical treatments. There is also a substantial opportunity in developing combination products that simplify treatment regimens, such as single-dose nasal sprays combining a corticosteroid and an antihistamine, enhancing patient compliance. Finally, leveraging telemedicine and digital health platforms offers opportunities for remote monitoring, personalized treatment adjustments, and direct-to-consumer educational campaigns about preventive measures and proper management of allergic triggers, thereby expanding the patient reach and fostering better long-term disease control.

The Sinusitis Medicine Market is extensively segmented based on Drug Class, Type, Route of Administration, and Distribution Channel, allowing for granular analysis of patient needs and market dynamics. The pharmaceutical landscape is highly diversified, reflecting the varied etiology and severity of sinusitis, ranging from mild acute episodes managed by OTC products to severe chronic conditions necessitating powerful prescription drugs. The efficacy and safety profile of each segment dictate its market share, with nasal corticosteroids currently dominating due to their potent anti-inflammatory action directly at the site of pathology, offering a superior risk-benefit profile compared to systemic alternatives.

Analysis by Type reveals that Chronic Sinusitis (CRS) represents a growing segment, driven by persistent environmental factors and increased life expectancy. CRS often requires continuous, long-term medication, leading to higher consumption rates and generating steady revenue streams, contrasted with the sporadic demand generated by Acute Sinusitis. The strategic emphasis of pharmaceutical companies is shifting towards developing treatments that address the underlying immunological dysfunctions in CRS, particularly those associated with nasal polyps, which often requires complex medical management including biologics, thereby driving the value proposition of specialty drugs.

Further segmentation by Distribution Channel highlights the crucial role of hospital pharmacies in dispensing high-value, specialized treatments (e.g., parenteral antibiotics or biologics), while retail pharmacies dominate the sales of high-volume, low-cost generic and OTC products (decongestants, oral analgesics, and generic nasal sprays). The increasing trend of self-medication for mild symptoms supports the strength of the OTC segment, although regulatory bodies are carefully scrutinizing the advertising and appropriate use of these products to prevent potential adverse effects or treatment delays for serious underlying conditions. This complex segmentation structure requires manufacturers to employ targeted marketing and supply chain strategies to effectively reach diverse patient populations and prescribers across different healthcare settings.

The value chain for the Sinusitis Medicine Market is inherently complex, starting with the upstream processes involving extensive research and development (R&D) and the sourcing of high-quality active pharmaceutical ingredients (APIs) and excipients. Upstream activities require significant investment in clinical trials, particularly for novel drugs like biologics, and strict adherence to global good manufacturing practices (GMP) for API synthesis. Key challenges in this phase include securing reliable raw material supply chains and navigating intellectual property hurdles. For small molecule drugs (like antibiotics or steroids), API manufacturing is often outsourced to specialized chemical suppliers, particularly in cost-effective regions like India and China, creating dependency but lowering overall production costs for the finished product.

The midstream segment involves formulation, manufacturing, and packaging of the final dosage forms, ranging from solid oral tablets to sophisticated metered-dose nasal spray devices. Formulation expertise is critical, especially for nasal delivery systems, which require precise particle size control and stability to maximize local efficacy and minimize systemic absorption. Direct manufacturing involves converting the API into the finished product, including quality assurance checks and regulatory compliance documentation. Companies must maintain highly sterile environments, particularly for injectable biologics and sterile nasal preparations, further adding to the operational complexity and capital expenditure requirements in the manufacturing stage.

Downstream activities focus on distribution, marketing, and sales, linking manufacturers to end-users via both direct and indirect channels. The distribution channel involves wholesalers, distributors, and logistics providers responsible for the safe and temperature-controlled delivery of medicines, crucial for sensitive biologics. Direct distribution channels are often utilized for specialized, high-cost prescription drugs marketed directly to hospitals and specialty clinics, allowing manufacturers greater control over pricing and education. Indirect channels, primarily involving large pharmaceutical distributors and retail pharmacy networks, handle the high volume of generic and OTC sinusitis medicines. Effective market access relies heavily on regulatory approval, payer negotiations for inclusion in formularies, and targeted marketing campaigns aimed at primary care physicians and otolaryngologists, emphasizing product differentiation and clinical superiority.

The potential customers for sinusitis medicines are broadly categorized into three main groups: healthcare providers who prescribe the medications, institutions that dispense and administer them, and the individual patients who utilize the treatments. The primary end-users are patients suffering from acute or chronic inflammation of the sinuses, a condition highly prevalent across all age groups but particularly affecting those with underlying allergies, asthma, or immune deficiencies. Patient demographics include children requiring mild, palatable formulations, adults seeking rapid relief to minimize work disruption, and the elderly who often require careful dosing due to comorbidities and polypharmacy. These diverse patient needs necessitate a wide array of dosage forms and medication classes.

Hospitals and specialty clinics, particularly those housing Otolaryngology (ENT) departments, represent a major segment of institutional buyers. These facilities are critical for the diagnosis and management of severe or complicated sinusitis, and they typically utilize high-value prescription products, including injectable antibiotics, specialized combination nasal sprays, and the increasingly important biological therapies for refractory chronic rhinosinusitis with nasal polyps. Purchasing decisions in this setting are influenced by hospital formularies, procurement agreements, and the need for reliable stock of essential, sometimes emergency, medications. Their purchasing volume for specialized drugs makes them attractive targets for direct sales and institutional pricing contracts offered by pharmaceutical companies.

The largest volume of transactions occurs within the retail sector, encompassing traditional brick-and-mortar pharmacies, retail drug stores, and increasingly, burgeoning online pharmacy platforms. These channels serve the mass market, distributing both prescription drugs (e.g., standard antibiotics and nasal corticosteroids) and high-volume, readily available over-the-counter products such as oral decongestants, saline nasal rinses, and simple analgesics. Pharmacists play a critical role as gatekeepers and counselors, advising customers on the appropriate use of OTC products and reinforcing adherence to prescribed treatments. Therefore, successful market penetration requires strong relationships with retail chains and effective patient-focused education materials provided at the point of sale to maximize customer conversion and loyalty.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.75 Billion |

| Market Forecast in 2033 | USD 2.75 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Pfizer Inc., GlaxoSmithKline Plc, Merck & Co., Inc., Sanofi S.A., AstraZeneca PLC, Johnson & Johnson, Novartis AG, Bayer AG, Teva Pharmaceutical Industries Ltd., Mylan N.V. (now Viatris), Cipla Ltd., Sun Pharmaceutical Industries Ltd., Regeneron Pharmaceuticals, Inc., Roche Holding AG, Bristol-Myers Squibb Company, Eli Lilly and Company, Hikma Pharmaceuticals PLC, Perrigo Company plc, Prestige Consumer Healthcare Inc., and Bausch Health Companies Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The key technological advancements underpinning the Sinusitis Medicine Market are concentrated primarily in optimizing drug delivery mechanisms and leveraging biotechnological innovations to address complex chronic diseases. Significant focus is placed on enhancing nasal drug delivery to maximize the concentration of the therapeutic agent directly at the inflamed sinus mucosa while minimizing systemic absorption and side effects. This involves the development of specialized nasal spray devices, such as those employing metered-dose, pressurized technology or vibrating mesh nebulizers, which ensure precise dosing and improved penetration into the hard-to-reach sinus cavities. Furthermore, formulation science is crucial, with manufacturers developing mucoadhesive polymers and nanoparticle carriers that extend the residence time of the drug on the mucosal surface, improving treatment efficacy and reducing the frequency of dosing required, thereby boosting patient compliance.

Another crucial technological development lies within the realm of biological therapies. For patients with severe Chronic Rhinosinusitis with Nasal Polyps (CRSwNP) driven by Type 2 inflammation (eosinophilic inflammation), monoclonal antibodies represent a paradigm shift. Technologies enabling the targeted inhibition of specific cytokines, such as Interleukin-4, Interleukin-5, or IgE pathways, have emerged, offering highly effective, systemic treatment options where traditional steroids and surgery have failed. These biotechnological advances necessitate sophisticated manufacturing processes, including mammalian cell culture and purification techniques, ensuring the safety and potency of these high-value injectable drugs. This segment is characterized by high R&D investment and strong patent protection, differentiating it significantly from the generic small-molecule market.

Beyond therapeutics, diagnostic technology also plays a supporting role by ensuring accurate patient stratification. Advances in minimally invasive diagnostic tools, such as high-resolution flexible nasal endoscopes integrated with digital imaging capabilities, allow for real-time visualization of disease status and mucosal response to therapy. Furthermore, laboratory technologies capable of rapidly analyzing inflammatory biomarkers from nasal swabs or blood samples are being commercialized. These point-of-care diagnostics, often utilizing microfluidics or advanced immunoassay techniques, help clinicians quickly determine the inflammatory endotype of the patient, guiding the decision whether to initiate anti-inflammatory therapy, antibiotics, or potentially biologic intervention, ensuring a faster and more tailored therapeutic response and reducing diagnostic ambiguity.

The market growth is primarily driven by the increasing global prevalence of allergic rhinitis and asthma, which predispose individuals to chronic sinusitis. Further propulsion comes from rising levels of air pollution worldwide, which acts as a persistent respiratory irritant, coupled with continuous technological advancements in localized nasal drug delivery systems that enhance treatment efficacy and patient adherence.

Antibiotic resistance is significantly restraining the use of broad-spectrum antibiotics, especially for acute sinusitis, which is often viral. Healthcare providers are now prioritizing nasal corticosteroids, saline rinses, and symptomatic relief as first-line therapies, reserving antibiotics strictly for confirmed bacterial infections, thereby driving segment growth toward anti-inflammatory and non-antimicrobial agents.

The Corticosteroids segment, particularly nasal sprays, currently holds the largest market share. This dominance is due to their potent anti-inflammatory properties, providing targeted relief for mucosal swelling and congestion, a core pathology of both acute and chronic sinusitis. They are widely recommended as the cornerstone of long-term medical management for chronic rhinosinusitis.

Biologics, such as monoclonal antibodies targeting Type 2 inflammatory pathways (e.g., IL-4, IL-5), are reserved for the treatment of severe, recalcitrant Chronic Rhinosinusitis with Nasal Polyps (CRSwNP) that have failed standard medical treatments and surgery. Although a high-cost segment, biologics represent a high-growth opportunity, offering targeted immunological intervention to reduce polyp burden and improve sinonasal quality of life metrics.

The Asia Pacific region's high growth rate is attributed to several critical factors, including rapidly deteriorating urban air quality, increasing consumer disposable income, and exponential growth in healthcare access and infrastructure development across key emerging economies like China and India. These factors translate into a large, newly diagnosed patient pool demanding both generic and branded sinusitis treatments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.