ID : MRU_ 431650 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

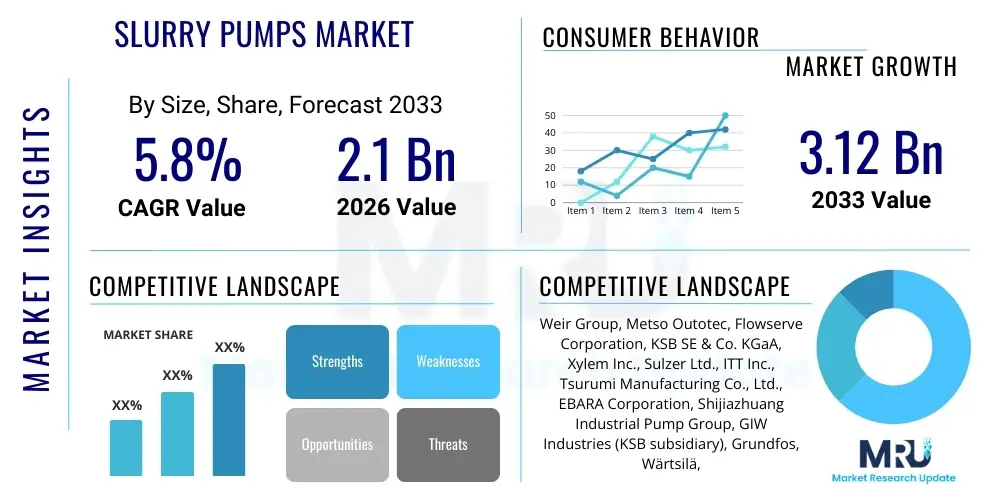

The Slurry Pumps Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 2.1 Billion in 2026 and is projected to reach USD 3.12 Billion by the end of the forecast period in 2033.

The Slurry Pumps Market encompasses specialized industrial equipment designed for transporting solid-liquid mixtures (slurries) containing abrasive, corrosive, or high-viscosity materials. These pumps are fundamentally distinct from clean water pumps, utilizing robust construction materials like high-chrome alloys, elastomers, and specialized ceramics to withstand harsh operating environments characterized by particle abrasion and chemical attack. Key features include large internal passages, heavy-duty bearings, and sacrificial wear parts that are easily replaceable, ensuring minimal downtime in continuous process operations. The primary product types include horizontal, vertical, and submersible configurations, each tailored for specific installation constraints and application demands, such as high-head or high-flow requirements.

Major applications driving the demand for slurry pumps span critical industrial sectors, most notably mining (ore processing, tailings disposal), construction (dredging, tunnel boring), and power generation (ash handling, flue gas desulfurization). The core benefit of modern slurry pumps is their efficiency in managing high-concentration solids while minimizing energy consumption and maximizing mean time between failures (MTBF). These benefits are crucial for maintaining profitability in high-volume, low-margin sectors like mineral extraction, where reliable equipment performance directly influences operational throughput and safety compliance.

The market’s expansion is primarily driven by escalating global demand for mined commodities, including iron ore, copper, and gold, which necessitates increased mineral processing activities. Furthermore, significant investments in infrastructure development, coupled with stringent environmental regulations promoting efficient handling and disposal of industrial waste and municipal sludge, contribute substantially to market growth. Technological advancements focusing on impeller design, material science breakthroughs (e.g., polyurethane liners), and smart monitoring systems are continually enhancing pump longevity and predictive maintenance capabilities, solidifying the market's long-term upward trajectory.

The Slurry Pumps Market exhibits robust growth, primarily fueled by sustained demand in the global mining and mineral processing sectors, particularly across the Asia Pacific region due to rapid industrialization and urbanization. Business trends indicate a strong move toward integrating sophisticated monitoring systems—such as Industrial IoT (IIoT) sensors—into pump systems to enable predictive maintenance, reduce operational costs, and optimize energy usage, thereby transitioning the market from capital expenditure to total cost of ownership models. Key manufacturers are focusing on developing high-efficiency, abrasion-resistant materials and modular designs to improve interchangeability and reduce inventory requirements for end-users operating in remote locations, reflecting a greater emphasis on reliability and lifecycle cost management over initial purchase price.

Regionally, Asia Pacific maintains dominance, driven by extensive mining activities in China, Australia, and India, alongside large-scale infrastructure and dredging projects. North America and Europe demonstrate mature market characteristics, focusing primarily on replacement demand, efficiency upgrades, and adherence to increasingly strict environmental standards regarding tailings and wastewater management. Segments trends highlight the sustained leadership of the horizontal pump type due to its versatility and ease of maintenance, although submersible pumps are gaining traction in deep excavation and highly challenging environments. Material-wise, high-chrome iron alloys continue to dominate due to their superior resistance to highly abrasive slurries, but advancements in specialized rubber and polyurethane liners are increasingly preferred for fine particle applications where corrosion resistance is paramount.

Overall, the market is characterized by high operational criticality, meaning purchasing decisions are heavily influenced by proven reliability and maintenance efficiency rather than just acquisition cost. Strategic partnerships between pump manufacturers and major mining or EPC companies are becoming commonplace, ensuring customized solutions and guaranteed aftermarket service. The future trajectory suggests increasing consolidation among mid-tier players and further differentiation by top-tier companies through digitalization and advanced material science, securing market positions based on performance and technological leadership.

User queries regarding the impact of Artificial Intelligence (AI) on the Slurry Pumps Market center predominantly on themes of operational efficiency, predictive failure analysis, and design optimization. Common questions include how AI algorithms can predict pump wear life in real-time, whether AI-driven maintenance scheduling can eliminate unplanned downtime in critical mining operations, and how machine learning (ML) optimizes the hydraulic design of impellers for varying slurry characteristics. Users are keenly interested in moving beyond traditional scheduled maintenance to highly optimized, condition-based maintenance regimes enabled by AI analyzing vibration, temperature, and pressure data streams. Concerns often revolve around the cost of integration, the requirement for specialized sensor infrastructure, and the cybersecurity risks associated with networked industrial equipment.

AI is fundamentally transforming the lifecycle management of slurry pumps by moving system diagnostics from reactive troubleshooting to proactive intelligence. By applying machine learning models to vast datasets collected from Industrial IoT (IIoT) sensors embedded within the pump and surrounding infrastructure, operational variables such as flow rate, motor load, and slurry density can be analyzed holistically. This analysis enables the creation of highly accurate digital twins, simulating the remaining useful life of critical components like impellers and liners. This capability allows operators to schedule precise component replacements during planned outages, significantly extending the Mean Time Between Failures (MTBF) and achieving substantial reductions in maintenance labor and material costs. Furthermore, AI helps in optimizing pump speed and configuration dynamically based on fluctuating process requirements, directly translating to energy savings.

The integration of AI also extends into the design and manufacturing phase. Generative design tools powered by AI are being used to explore thousands of potential impeller geometries that maximize hydraulic efficiency and minimize abrasion hotspots under specific operating conditions, something computationally prohibitive for traditional CAD modeling. This innovation leads to the production of pumps with superior performance characteristics tailored specifically to the unique slurry conditions (e.g., highly corrosive vs. highly abrasive), speeding up product development cycles and enhancing competitive differentiation. While initial implementation requires significant capital investment in connectivity and data infrastructure, the long-term benefits in maximizing asset utilization and minimizing environmental impact (through better process control) solidify AI as a critical evolutionary force in the slurry pumps sector.

The Slurry Pumps Market is governed by a complex interaction of Drivers, Restraints, and Opportunities, which collectively determine the market trajectory and influence investment decisions across the value chain. Key drivers include the global resurgence in mining output driven by electrification and renewable energy demands (requiring vast amounts of copper and rare earth minerals), coupled with the indispensable role of slurry pumps in managing the associated waste tailings and mineral concentrate transportation. These drivers are bolstered by increasing global expenditure on municipal wastewater treatment and industrial infrastructure projects, particularly in developing economies, creating consistent demand across multiple application segments. The fundamental impact force of Drivers is high and sustained, ensuring ongoing market expansion irrespective of short-term commodity price fluctuations.

However, the market faces significant restraints, primarily revolving around high initial capital costs for heavy-duty, specialty-material pumps, and the substantial operating expenditure associated with energy consumption and frequent replacement of wear parts (impellers, liners). Furthermore, the highly specialized nature of the equipment and the requirement for skilled technicians for maintenance pose logistical and human capital challenges, especially in remote mining locations. Regulatory pressure, particularly regarding environmental protection (e.g., mandates for zero-discharge systems or high-solids handling to minimize water usage), also acts as a restraint by increasing complexity and compliance costs, although simultaneously driving innovation toward more efficient and robust systems. The combined impact of Restraints necessitates constant innovation in material science and efficiency improvements to maintain market viability.

Opportunities within the market are predominantly found in technological innovation, particularly the development of high-pressure, high-density slurry pump systems that reduce the need for water dilution, conserving scarce resources and lowering tailings volume. The rapid adoption of IIoT and AI for condition monitoring and predictive maintenance presents a massive opportunity for manufacturers to offer value-added services, transitioning from pure equipment providers to integrated solutions partners. Additionally, the growing focus on sustainable mining practices and the remediation of older tailings ponds globally offers specialized growth avenues for durable, reliable, and energy-efficient pumping solutions. These opportunities, particularly in digital transformation, promise to differentiate market leaders and create new revenue streams over the forecast period, positioning the combined Impact Forces as moderately positive and progressively stronger.

The Slurry Pumps Market is highly segmented based on critical operational and design parameters, allowing manufacturers to cater to the extreme variability inherent in slurry characteristics (abrasiveness, particle size, acidity, viscosity). Understanding these segments is vital for strategic positioning, as the choice of pump type, material, and size is entirely dictated by the specific application’s duty cycle and fluid properties. The primary segmentation dimensions include the Type of pump (Horizontal, Vertical, Submersible), the Material of Construction (Hard Metal, Rubber/Elastomer, Ceramic), the Power Source (Electric, Diesel), and the End-User Industry (Mining & Mineral Processing, Construction, Metals, Power Generation, Chemical & Manufacturing).

Analyzing these segments reveals dynamic growth patterns. While the mining industry remains the undisputed largest end-user, accounting for the highest volume and value demand, the power generation and construction segments are demonstrating accelerated growth, driven by environmental mandates (ash handling, flue gas desulfurization) and global infrastructure development (dredging, deep foundation excavation). Within the pump type segment, Horizontal slurry pumps command the largest market share due to their widespread versatility, scalability, and ease of maintenance, making them the default choice for major processing circuits. However, the Submersible pump segment is experiencing the fastest growth, primarily due to their increasing necessity in challenging environments such as deep pits, sumps, and dredging operations, where dry installation is impractical or impossible.

Furthermore, material segmentation reflects the constant battle against wear and corrosion. Hard Metal (typically High-Chrome Iron alloys) dominates applications involving coarse, extremely abrasive solids like iron ore or coarse sand. Conversely, Elastomers (natural rubber, synthetic rubber, polyurethane) are critical for handling finer, corrosive, or slightly abrasive materials, offering superior flexibility and impact resistance. Manufacturers are strategically investing in R&D to blend these material characteristics, introducing composite materials that offer optimized wear life across a broader range of complex slurries, thereby blurring the traditional lines between material segments and enhancing pump performance across highly volatile operating conditions.

The value chain for the Slurry Pumps Market begins with upstream activities centered on raw material procurement, particularly specialized metallurgical components like high-grade iron ore, chromium, and synthetic rubber polymers, necessary for manufacturing durable wear parts. This stage is crucial, as the performance and longevity of a slurry pump are heavily dependent on the quality and composition of its materials of construction. Leading manufacturers maintain strong relationships with specialized foundries and elastomer suppliers to ensure material integrity and batch consistency. Research and Development (R&D) forms a significant early stage, focusing on hydraulic design optimization, wear testing, and the integration of smart technologies (sensors, IIoT modules) into the pump unit, which adds significant intellectual property value before manufacturing.

Mid-stream activities involve the core manufacturing processes: casting, machining, assembly, and rigorous testing. Given the large size and highly customized nature of many slurry pump installations, manufacturers often maintain flexible production lines capable of handling bespoke orders alongside standard models. The key value addition here lies in precision engineering, ensuring tight tolerances for components like impellers and casings, which directly impact hydraulic efficiency and minimize cavitation. Effective inventory management of high-wear parts (which constitute a major portion of the aftermarket revenue) is also a critical function in the mid-stream, ensuring quick turnaround times for maintenance and repairs globally.

Downstream activities focus on market penetration, distribution, installation, and aftermarket service. Distribution channels are typically a combination of direct sales for large, complex mining projects (where technical consultation is essential) and indirect sales through specialized distributors and authorized service centers for standardized or smaller industrial applications. The aftermarket segment—including spare parts (liners, impellers, shaft sleeves) and service agreements—represents a substantial, high-margin revenue stream for manufacturers, often accounting for more than half of the total revenue over a pump’s lifespan. Strong regional service networks capable of rapid deployment and technical expertise are critical for maintaining customer loyalty and reducing equipment downtime, thereby maximizing lifecycle value.

Potential customers for slurry pumps are overwhelmingly concentrated in heavy industrial sectors where the continuous movement of abrasive or corrosive fluid mixtures is integral to the core production process. The largest customer segment is the Mineral Processing sector, encompassing mining operations for base metals (copper, iron, aluminum), precious metals (gold, silver), and bulk minerals (coal, phosphate). These operations rely heavily on slurry pumps for transportation of raw ore, feeding crushers, managing concentrator circuits (flotation, leaching), and, crucially, handling the massive volumes of tailings and wastewater generated.

Beyond mining, significant demand emanates from the Electric Power Generation industry, specifically coal-fired power plants that utilize these pumps extensively for Fly Ash and Bottom Ash handling systems, as well as Flue Gas Desulfurization (FGD) systems where limestone slurry is used to clean exhaust gases. The construction and infrastructure sector, particularly those involved in hydraulic filling, tunnel boring (TBM spoil removal), and large-scale dredging projects (port expansion, land reclamation), represent another substantial end-user segment demanding robust, high-capacity submersible and horizontal pumps designed for handling high concentrations of sand and aggregate.

Furthermore, chemical manufacturing facilities, fertilizer plants, and wastewater treatment municipalities serve as consistent, albeit smaller, segments. These customers typically require pumps manufactured from corrosion-resistant materials (e.g., rubber-lined or specialized alloys) to handle chemically aggressive slurries or municipal sludge. Purchasing decisions across all these customer segments are driven not just by price, but by established metrics of reliability, energy efficiency, ease of maintenance (accessibility of wear parts), and the manufacturer's proven track record in extreme operational environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 2.1 Billion |

| Market Forecast in 2033 | USD 3.12 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Weir Group, Metso Outotec, Flowserve Corporation, KSB SE & Co. KGaA, Xylem Inc., Sulzer Ltd., ITT Inc., Tsurumi Manufacturing Co., Ltd., EBARA Corporation, Shijiazhuang Industrial Pump Group, GIW Industries (KSB subsidiary), Grundfos, Wärtsilä, Pioneer Pump, Atlantic Fluid Power, Sandpiper Pumps, Dayton Superior, Tsurumi Pump, Multiflo (Weir), Schurco Slurry. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Slurry Pumps Market is continuously evolving, driven by the need to maximize operational efficiency, extend wear life, and reduce the total cost of ownership (TCO) in highly demanding applications. A foundational technological focus is on advanced materials science. This involves developing proprietary high-chrome alloys with specialized microstructures that offer superior hardness and corrosion resistance compared to standard materials, enabling pumps to handle tougher, more complex slurries. Furthermore, research into novel composite liners, combining the abrasion resistance of ceramics with the flexibility of elastomers, is gaining traction, particularly for highly variable mineral processing circuits where slurry properties fluctuate frequently. This material innovation is critical because component replacement frequency is the single largest determinant of operational downtime.

Another major technological pivot point is the integration of Industrial Internet of Things (IIoT) sensors and smart monitoring systems. Modern slurry pumps are increasingly being equipped with embedded sensors that capture real-time data on vibration levels, bearing temperatures, motor current draw, and hydraulic performance characteristics. This data is processed by advanced algorithms to monitor the rate of component wear, detect early signs of cavitation, and predict impending mechanical failure. This shift from reactive maintenance to condition-based and predictive maintenance fundamentally transforms asset management, ensuring maximum uptime and preventing catastrophic equipment failures that can shut down an entire processing plant for days.

Hydraulic design optimization represents the third core technological area. Computational Fluid Dynamics (CFD) modeling has become standard practice, allowing engineers to simulate flow patterns within the pump casing and impeller. This rigorous modeling helps minimize turbulence, reduce localized wear hotspots, and optimize the specific speed of the pump to handle higher solid concentrations with greater energy efficiency. Technologies facilitating high-pressure, high-density pumping—often involving piston diaphragm pumps or highly specialized centrifugal pumps designed for thickened tailings transport—are essential for meeting environmental regulations aimed at reducing water consumption and improving the stability of tailings storage facilities. These combined innovations ensure that new pump generations offer measurable improvements in longevity, efficiency, and environmental compliance.

The regional dynamics of the Slurry Pumps Market reflect global mining distribution, infrastructure investment trends, and localized regulatory environments. Asia Pacific (APAC) dominates the market both in terms of value and volume, primarily due to the extensive mining activities in Australia (iron ore, gold), China (coal, industrial minerals), and India (coal, infrastructure). This region also benefits from massive, ongoing urbanization and infrastructure development projects, including major dredging operations and wastewater treatment plant expansions, creating continuous demand for robust pumping solutions. Furthermore, the industrial backbone of APAC, involving metallurgy and power generation expansion, drives significant replacement and new equipment procurement, making it the most critical growth engine globally. Manufacturers focus heavily on establishing strong local distribution and service networks across APAC to capitalize on the sheer scale of the end-user requirements.

North America and Europe represent mature markets characterized by stringent safety and environmental regulations and a high focus on efficiency and automation. In North America, demand is driven by established mining operations (especially copper and gold) and significant investments in wastewater management infrastructure upgrades. The technological adoption rate for smart pumping systems (IIoT, predictive analytics) is highest here, as companies prioritize reducing labor costs and achieving optimal energy performance. Similarly, the European market, though constrained by lower domestic mining volumes, sees consistent demand from power generation (FGD systems) and chemical processing sectors. The core market activity revolves around replacing older, inefficient units with high-efficiency, compliant models, emphasizing durability and low lifecycle cost over initial purchase price.

Latin America and the Middle East & Africa (MEA) present high-potential growth opportunities driven by resource extraction and infrastructure development. Latin America, particularly Chile, Peru, and Brazil, holds vast reserves of copper and iron ore, making it indispensable for major global mining companies. The demand here is for extremely robust pumps capable of handling large volumes of abrasive material in challenging geographical environments, often necessitating customized high-pressure pump systems for transporting slurries over long distances across mountainous terrain. The MEA region, fueled by mining investment in South Africa and rapid industrialization and construction activities in the Gulf Cooperation Council (GCC) states (especially dredging and construction material handling), shows strong future growth potential. Investment in localized manufacturing and assembly plants within these regions is a strategic imperative for manufacturers seeking to reduce logistics costs and provide immediate aftermarket support to remote customer locations.

Market growth is primarily driven by escalating global demand for mined commodities (especially materials required for electrification like copper and lithium), substantial infrastructure spending (dredging and construction), and increasing stringency in environmental regulations requiring efficient industrial waste and tailings management globally.

Horizontal Slurry Pumps currently hold the largest market share due to their widespread versatility, robust design, ease of maintenance, and suitability for high-head applications across major end-user industries, particularly mining and mineral processing.

The material choice (e.g., High-Chrome Iron or Rubber/Elastomers) is crucial as it determines the pump's resistance to abrasion and corrosion. Hard metals are preferred for coarse, highly abrasive slurries, while elastomers are used for fine particles, corrosive fluids, and impact resistance, directly influencing pump longevity and wear life.

Digitalization, via Industrial IoT (IIoT) sensors and AI, is essential for transitioning to predictive, condition-based maintenance. This technology optimizes energy usage, minimizes component wear rate, and drastically reduces unplanned downtime, enhancing overall operational efficiency for end-users.

The Asia Pacific (APAC) region presents the highest growth opportunities, primarily fueled by extensive raw material mining operations, rapid infrastructural development, and substantial investment in water and waste treatment facilities across countries like China, India, and Australia.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.