ID : MRU_ 434012 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

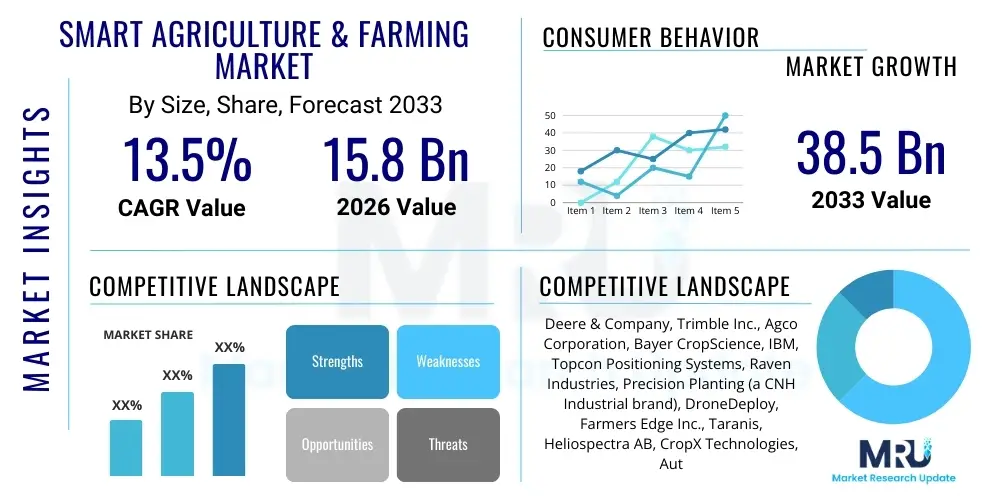

The Smart Agriculture & Farming Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.5% between 2026 and 2033. The market is estimated at USD 15.8 Billion in 2026 and is projected to reach USD 38.5 Billion by the end of the forecast period in 2033.

The Smart Agriculture and Farming Market encompasses the utilization of advanced technological systems—including Internet of Things (IoT), sensors, robotics, artificial intelligence (AI), and data analytics—to enhance agricultural productivity, efficiency, and sustainability. This market addresses critical global challenges such as increasing food demand driven by population growth, resource scarcity, and the need for climate-resilient farming practices. Key products within this domain include precision farming equipment, monitoring systems, soil health sensors, yield mapping software, and fully automated irrigation and fertilization systems. The core objective of these technologies is to transform traditional, often inefficient, agricultural methods into data-driven, optimized operations, ensuring higher yields with minimal environmental impact.

Major applications of smart farming technologies span across crop management, livestock monitoring, aquaculture, and greenhouse cultivation. In crop management, applications include variable rate technology (VRT) for precise nutrient and pesticide application, and sophisticated drone-based surveillance for early detection of pests and diseases. For livestock, wearable sensors and integrated barn systems monitor animal health, behavior, and location, optimizing feeding schedules and identifying sick animals rapidly. The primary benefits realized by adopting these systems include significant reduction in water usage, lower labor costs due to automation, optimized input expenditure (fertilizers and pesticides), and improved quality and uniformity of agricultural output, contributing directly to increased farmer profitability and operational resilience.

Driving factors for the robust growth of this market are multifaceted, anchored primarily by governmental initiatives promoting sustainable farming and the increasing penetration of high-speed internet and affordable sensing technology in rural areas globally. Furthermore, the rising adoption of cloud-based platforms facilitates the seamless collection and analysis of massive datasets generated by farm operations, enabling farmers to make real-time, informed decisions. The demographic shift towards mechanized farming, particularly in developing economies facing labor shortages, further accelerates the demand for robotics and autonomous vehicles tailored for field operations, solidifying the market's positive growth trajectory throughout the forecast period.

The global Smart Agriculture & Farming Market is undergoing rapid technological integration, characterized by intense investment in digital infrastructure and predictive analytics. Business trends highlight a strong movement towards integrated platform solutions, moving away from disparate hardware components. Key industry participants are focusing on strategic partnerships and mergers to offer comprehensive farm management systems (FMS) that combine hardware, software, and consultancy services, enabling end-to-end data flow from soil preparation to harvest logistics. Furthermore, there is a notable rise in Subscription-as-a-Service (SaaS) models for software platforms, making advanced analytics more accessible to small and medium-sized farms by lowering upfront capital investment barriers and ensuring continuous software updates and support.

Regionally, North America and Europe currently dominate the market due to early adoption of precision farming techniques, robust regulatory support for technological integration, and the presence of major technology providers. However, the Asia Pacific (APAC) region is projected to exhibit the highest growth rate during the forecast period, driven by large agricultural economies like China and India, which are rapidly transitioning to mechanized farming to boost food security and productivity. Government subsidies in APAC focusing on water efficiency and modernization of irrigation systems are acting as powerful catalysts for adoption. Meanwhile, Latin America shows increasing potential, particularly in large-scale soybean and grain operations, benefiting from advancements in satellite imagery and localized weather prediction services.

Segment trends reveal that the Precision Farming segment, encompassing guidance systems, remote sensing, and variable rate technology, remains the largest revenue generator, primarily due to its proven impact on input cost optimization. Within components, software and services are experiencing faster growth compared to hardware, emphasizing the increasing value placed on data interpretation and decision support systems powered by AI and machine learning algorithms. Based on application, field monitoring and crop scouting applications dominate, driven by the need for real-time health assessment and yield estimation, paving the way for fully autonomous farm operations in the long term.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Smart Agriculture & Farming Market predominantly revolve around three critical themes: efficiency improvements through predictive modeling, the economics of adoption for smaller farms, and the implications for labor displacement and required skill sets. Users frequently ask about the accuracy of AI-driven yield prediction models, the effectiveness of computer vision in identifying subtle plant diseases or nutrient deficiencies before visible symptoms appear, and how machine learning algorithms optimize resource allocation, specifically water and fertilizer usage. There is also significant concern and interest regarding how AI platforms can integrate diverse data sources—such as drone imagery, satellite data, weather reports, and soil sensor readings—to provide truly holistic and actionable farm management advice, ensuring maximal Return on Investment (ROI) for advanced technology purchases.

The analysis of these common user questions indicates high expectations for AI to solve complex, non-linear agricultural challenges, such as optimizing multi-crop rotation strategies under variable climate conditions and automating complex tasks like robotic harvesting and autonomous weed control. Key concerns center on data privacy, the cost barrier associated with sophisticated AI hardware and software licenses, and the necessity for reliable connectivity in remote agricultural areas to support real-time processing and decision-making. These inquiries underscore the market's shift from basic data collection to advanced cognitive computing, where AI acts as the central brain of the smart farm ecosystem, driving operational excellence and sustainability goals simultaneously.

Furthermore, users seek assurance that AI models are adaptable to localized soil types, microclimates, and specific crop varieties, confirming that a generalized AI solution is insufficient for precision agriculture. This demand for highly customized, localized AI solutions is compelling market players to invest heavily in robust data training and regional partnerships, ensuring that the AI impact is universally beneficial across various farm sizes and geographical contexts, thus stabilizing food production chains globally against increasing environmental volatility.

The market growth is primarily driven by the escalating global demand for food security, requiring intensive and highly efficient production methods, coupled with technological advancements that make smart farming solutions more reliable and cost-effective. Key drivers include supportive governmental policies offering subsidies for technology adoption, the necessity to conserve increasingly scarce natural resources like water and arable land, and the competitive pressure on farmers to optimize input costs. These drivers are amplified by the growing awareness of environmental sustainability, pushing farmers towards practices that minimize pollution and carbon footprint, aligning perfectly with the capabilities of precision agriculture technologies.

However, significant restraints impede the rapid widespread adoption of smart farming solutions. High initial capital investment required for sophisticated hardware (sensors, autonomous tractors, drones) and software licensing represents a major barrier, especially for small-scale farmers in developing regions. Furthermore, the lack of standardized communication protocols and data formats across different vendors creates interoperability challenges, complicating the integration of various systems on a single farm. A major enduring constraint is the lack of reliable high-speed internet connectivity in many rural agricultural areas globally, which is essential for transmitting and analyzing the massive volumes of data generated by modern smart farming equipment in real time, thereby limiting the efficacy of cloud-based solutions and remote monitoring capabilities.

Opportunities for growth are vast, centered on the expansion of smart livestock management systems, the proliferation of vertical and indoor farming (especially in urban environments), and the development of open-source platforms that lower the entry barrier for small technology providers. The rising trend of utilizing Big Data and advanced geo-spatial analytics to offer customized, hyper-local farming advice presents a lucrative avenue for software and service providers. Impact forces are moderately high, driven primarily by intense competition among technology vendors leading to rapid price erosion and product innovation, balanced against the slow pace of adoption stemming from the conservative nature of the agricultural industry and the required farmer education and training necessary to utilize these complex tools effectively.

The Smart Agriculture & Farming Market segmentation provides a granular view of market dynamics based on technological components, farm types, application areas, and geographical regions. This multi-dimensional segmentation allows stakeholders to target investment towards the highest-growth areas, particularly focusing on the rapid adoption of digital solutions over traditional hardware components. Key segments are analyzed based on their growth trajectory, market penetration, and sensitivity to factors such as government regulation and commodity price volatility, confirming that the future revenue generation will be increasingly dominated by software and data services rather than primary hardware sales, marking a transition towards Agriculture 4.0 paradigms globally.

The market is typically segmented by Component (Hardware, Software, and Services), Application (Precision Farming, Livestock Monitoring, Aquaculture, and Smart Greenhouse), Farm Type (Large, Medium, and Small Farms), and Geography. Hardware, while a foundational segment including sensors, drones, and GPS devices, faces margin pressure, whereas the Software segment, comprising Farm Management Systems (FMS), yield monitoring, and predictive analytics tools, demonstrates superior growth rates due to its recurring revenue potential and crucial role in decision making. The fastest-growing application segment is Precision Farming, specifically encompassing Variable Rate Technology (VRT) and yield mapping, which offer immediate and measurable ROI for farmers struggling with resource optimization challenges.

Geographically, while established markets in North America and Europe drive innovation and high-value product sales, the greatest volumetric growth is expected from emerging economies in the Asia Pacific region, driven by the sheer scale of arable land and governmental mandates aimed at improving food security and reducing agricultural imports. This regional disparity necessitates tailored solutions; for instance, connectivity solutions and low-cost sensor technologies are prioritized in APAC, while fully autonomous systems and integration with high-end machinery dominate the North American market, requiring strategic customization of product portfolios by key market participants.

The Smart Agriculture and Farming value chain is highly complex, involving multiple specialized stages, beginning with upstream technology providers and extending through to the final food consumers. The upstream segment is dominated by specialized manufacturers of foundational technologies, including chipmakers, sensor producers (e.g., soil moisture, nutrient, and weather sensors), satellite imagery providers, and telecommunications companies providing crucial connectivity infrastructure. Successful upstream operation relies heavily on continuous R&D investment to enhance sensor accuracy, battery life, and durability under harsh field conditions. Partnerships at this stage between hardware providers and data platform developers are critical for ensuring seamless data ingestion and reliable operation of integrated systems in real-world agricultural environments.

The midstream involves system integrators, Farm Management Software (FMS) developers, and agricultural robotics manufacturers who assemble the disparate hardware and software components into functional, customized solutions for farmers. Distribution channels are varied, incorporating direct sales models for large enterprises, partnerships with traditional agricultural equipment dealers, and specialized technology distributors. Direct channels are often utilized for complex, high-value systems requiring extensive installation and training, whereas indirect channels, leveraging established networks of agricultural dealers, are crucial for reaching smaller and medium-sized farms efficiently. Software and services are frequently delivered via cloud platforms, bypassing physical distribution entirely, highlighting the shift towards digital delivery models.

The downstream analysis focuses on the end-users—the farmers and agricultural enterprises—and the subsequent impact on the wider food supply chain. Smart farming technologies enable enhanced traceability and quality assurance, which are increasingly demanded by food processors, retailers, and final consumers. The outputs of smart farming—optimized crops and livestock—flow into processing plants, logistics providers, and retail outlets. The value captured downstream is primarily in premium pricing for sustainably produced, traceable products and reduced waste across the supply chain, emphasizing the role of smart technology in enhancing transparency and meeting stringent modern food safety and ethical standards.

The primary customers for Smart Agriculture & Farming technologies are agricultural enterprises, encompassing large commercial farms, medium-sized family farms transitioning to modern methods, and highly specialized operations like vertical farms and research institutions. Large commercial farms, especially in North America and Europe, are early and high-volume adopters, utilizing integrated systems for vast acreage management, including autonomous machinery and enterprise-level Farm Management Systems (FMS). These customers are primarily driven by the need for cost reduction through efficiency gains, maximizing yield potential, and meeting sustainability compliance requirements imposed by international trade regulations and supply chain partners.

Medium-sized family farms represent a substantial and rapidly growing customer segment, though their adoption drivers are focused more on accessibility and ease of use. For this group, solutions offered via SaaS models, affordable sensor packages, and localized advisory services based on collected data prove most attractive. They seek technologies that address specific pain points, such as labor shortages or optimizing fertilization application to counter rising input costs. The market successfully targets this segment by offering scalable, modular solutions that allow farmers to incrementally invest in technology, starting with high-ROI applications like soil monitoring or simple drone-based crop scouting, and expanding as their comfort and financial resources allow.

Beyond traditional field farming, specialized segments such as smart greenhouses, controlled environment agriculture (CEA), and aquaculture operations form a vital customer base. CEA operators, in particular, rely heavily on smart sensors, automated environmental controls, and AI-driven systems to precisely manage temperature, humidity, and nutrient delivery year-round, maximizing crop cycles and minimizing resource usage in dense urban settings. Furthermore, governmental agricultural bodies, academic research institutions, and commodity traders act as indirect customers, utilizing data streams generated by smart farming solutions for policy formulation, breeding research, and sophisticated price forecasting, demonstrating the broad economic reach of this technology ecosystem.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 15.8 Billion |

| Market Forecast in 2033 | USD 38.5 Billion |

| Growth Rate | 13.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Deere & Company, Trimble Inc., Agco Corporation, Bayer CropScience, IBM, Topcon Positioning Systems, Raven Industries, Precision Planting (a CNH Industrial brand), DroneDeploy, Farmers Edge Inc., Taranis, Heliospectra AB, CropX Technologies, Autonomous Tractor Corporation, Valmont Industries. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Smart Agriculture & Farming Market is defined by the convergence of several high-growth digital and physical systems. At the core is the Internet of Things (IoT), where networks of interconnected sensors—measuring soil parameters, microclimate variables, and plant health—collect vast amounts of data in real time. These sensors range from simple moisture probes to sophisticated hyperspectral imaging devices deployed on aerial platforms (drones or satellites). The collected data is then transmitted via various communication protocols, including LPWAN (Low-Power Wide-Area Networks) and cellular networks (5G), ensuring pervasive connectivity even in large, remote fields, forming the essential foundation for data-driven farming decisions and remote operations.

A secondary, but increasingly crucial, layer involves geospatial technologies and automation systems. Global Navigation Satellite Systems (GNSS) and Geographic Information Systems (GIS) provide the necessary spatial accuracy for precision applications, enabling equipment guidance, field mapping, and variable rate application technologies (VRT). This geospatial framework is coupled with robotics and autonomous vehicle technology, which are transitioning from simple GPS-guided tractors to complex, fully autonomous field robots capable of planting, weeding, and harvesting with minimal human intervention. Key technology focus areas include machine vision for identifying individual weeds versus crops, and advanced path planning algorithms that optimize equipment movement across uneven terrain, thereby maximizing fuel and labor efficiency.

The final layer involves the analytical backbone, dominated by Artificial Intelligence (AI) and Machine Learning (ML). These computational technologies process the enormous, heterogeneous data streams from IoT and geospatial sources to generate predictive models—forecasting yield, optimizing pest control timings, and advising on optimal market sales windows. Cloud computing platforms provide the scalable infrastructure required to run these complex models, delivering actionable insights through user-friendly Farm Management Software (FMS) dashboards, transforming raw data into quantifiable operational improvements and enhancing overall farm profitability and resilience against climate variability.

The Smart Agriculture & Farming Market is projected to grow at a robust CAGR of 13.5% between 2026 and 2033, driven by increasing necessity for efficient resource management and rising technological integration on farms globally. This strong growth trajectory reflects the critical transition towards data-centric farming practices essential for future food security.

Precision agriculture growth is primarily driven by the convergence of Internet of Things (IoT) sensors for granular data collection, Artificial Intelligence (AI) for predictive analytics and decision support, and advanced geospatial technologies like GPS and remote sensing (drones and satellites). These components facilitate Variable Rate Technology (VRT) and yield monitoring, which are crucial for optimizing input use.

Smart farming significantly contributes to environmental sustainability by enabling precise resource application. Technologies such as smart irrigation and Variable Rate Technology (VRT) drastically reduce water and fertilizer runoff, minimizing pollution and conserving natural resources. Furthermore, AI-driven pest management reduces the overall volume of chemical pesticides required, supporting biodiversity and ecosystem health.

The main financial constraints are the high initial capital expenditure required for purchasing and implementing sophisticated hardware, such as autonomous equipment, advanced sensor networks, and high-resolution drone systems. Furthermore, ongoing costs associated with software licensing and data management platforms pose an additional barrier, particularly for small-scale agricultural operations with limited access to capital or financing.

The Asia Pacific (APAC) region is forecasted to exhibit the highest growth rate during the 2026–2033 period. This accelerated growth is primarily attributed to large-scale government modernization initiatives in major agricultural economies like China and India, focusing on improving yield, combating labor shortages through mechanization, and enhancing water use efficiency across vast farmlands.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.