ID : MRU_ 432244 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

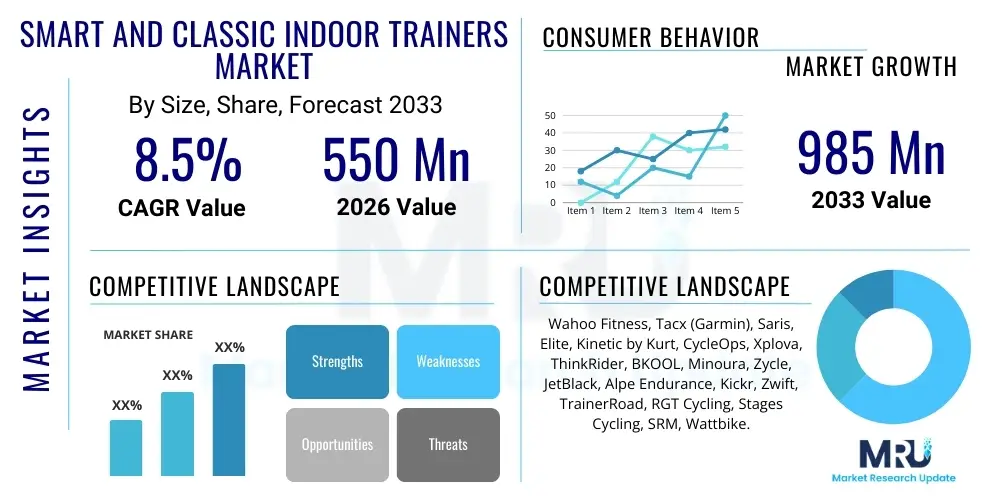

The Smart and Classic Indoor Trainers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 550 Million in 2026 and is projected to reach USD 985 Million by the end of the forecast period in 2033.

The Smart and Classic Indoor Trainers Market encompasses devices designed to allow cyclists to ride their bicycles indoors, simulating real-world cycling conditions for training, fitness, and entertainment purposes. Classic trainers, historically dominant, utilize basic resistance mechanisms such as magnetic or fluid systems, offering reliable but fundamentally static resistance curves, typically focused on simple resistance adjustment via manual levers. Conversely, smart trainers represent the technological evolution of indoor cycling, integrating advanced features like built-in power meters, variable electronic resistance controlled by external software, and comprehensive connectivity options (ANT+, Bluetooth) to interact seamlessly with virtual training platforms like Zwift, TrainerRoad, and RGT Cycling. This bifurcation caters to both budget-conscious users seeking fundamental fitness solutions and performance-driven athletes demanding high fidelity simulation and data accuracy.

Major applications of these trainers span across professional athletic training, rehabilitation, general fitness maintenance, and competitive virtual cycling (esports). The proliferation of high-quality streaming services and the subsequent rise of virtual racing have significantly broadened the market appeal of smart trainers, shifting them from niche training tools to mainstream consumer electronics. The core benefits derived from using these products include time efficiency, safety from external traffic and weather hazards, and the ability to execute structured, data-driven workouts crucial for targeted physiological improvements. The integration of sophisticated sensors in smart trainers provides instantaneous feedback on metrics such as power output, cadence, and speed, which is indispensable for serious training regimens.

Key driving factors accelerating the market include global fitness trends emphasizing personalized and data-backed exercise, the increasing normalization of remote training modalities, and continuous technological advancements improving trainer accuracy and road feel simulation. Furthermore, the accessibility and community aspect provided by virtual cycling ecosystems encourage higher engagement and continuous equipment upgrades, particularly within the smart trainer segment. Manufacturers are continually innovating to reduce noise, enhance portability, and improve the realism of the cycling experience, ensuring sustained growth across diverse geographic and demographic segments.

The Smart and Classic Indoor Trainers Market is characterized by robust growth, primarily fueled by the accelerating adoption of smart connectivity and virtual training platforms. Business trends indicate a strategic focus on ecosystem integration, where hardware manufacturers are increasingly partnering with or acquiring virtual software providers to offer comprehensive, subscription-based user experiences. This convergence necessitates high capital investment in Research and Development (R&D) to maintain accuracy standards (often measured by power meter variance, typically +/- 1%) and enhance features such as grade simulation, inertia control, and silent operation. The market sees strong competition, pushing prices down in the entry-level smart trainer segment while premium models retain high margins through superior specifications like maximum wattage and simulated incline.

Regionally, North America and Europe dominate the market due to high discretionary income, established cycling cultures, and early adoption of virtual fitness technology. However, the Asia Pacific (APAC) region is demonstrating the fastest growth trajectory, driven by increasing disposable incomes in emerging economies and rising awareness of indoor fitness benefits, particularly in densely populated urban areas where outdoor cycling is challenging. Governments and private entities in these regions are increasingly investing in cycling infrastructure and promoting healthy lifestyles, further supporting market expansion, although infrastructure limitations sometimes favor indoor training solutions.

Segment trends reveal a significant shift from classic trainers to smart trainers, which now command the majority of market value. Within smart trainers, direct-drive systems are preferred over wheel-on variants due to their superior power accuracy, reduced tire wear, and generally quieter operation. The end-user segment is evolving, with commercial applications (e.g., dedicated indoor cycling studios and fitness centers) expanding their fleet of smart trainers to host group classes and virtual events. Distribution channels are favoring online retail, which provides ease of comparison, detailed product specifications, and direct-to-consumer sales, though specialty cycling stores remain crucial for expert advice and installation services.

User inquiries regarding AI's impact on indoor trainers predominantly center on personalized training optimization, performance predictability, and the realism of virtual environments. Users are keen to understand how AI can move beyond simple pre-set workout protocols to dynamically adjust resistance based on real-time physiological metrics (heart rate variability, fatigue level), optimizing training load to maximize performance gains while minimizing the risk of overtraining. There is also significant interest in AI-driven simulation realism, questioning whether AI algorithms can generate more adaptive and nuanced virtual road feel, wind resistance modeling, and interaction within multi-user virtual worlds, thereby blurring the line between indoor and outdoor cycling experiences.

The application of Artificial Intelligence (AI) and Machine Learning (ML) is fundamentally transforming the value proposition of smart indoor trainers, shifting the focus from mere data collection to sophisticated data utilization. AI algorithms are now deployed to analyze vast datasets of user performance, comparing individual metrics against aggregated peer groups to identify optimal training zones and detect subtle plateaus or improvements. This personalization ensures that every training session is precisely tailored to the cyclist's current physical state and specific goals (e.g., improving sprint power or aerobic capacity), creating highly engaging and effective training pathways that were previously only accessible through expensive, one-on-one coaching.

Furthermore, AI significantly enhances the user experience in virtual cycling ecosystems. ML models are used for advanced cheat detection in competitive virtual racing, ensuring fair play and maintaining the integrity of esports events. On the hardware side, predictive maintenance algorithms utilize sensor data to forecast potential mechanical failures in the trainer's resistance unit or power meter, prompting timely alerts and reducing downtime. The future trajectory involves integrating AI-powered biomechanical analysis via attached cameras or sensors, offering real-time feedback on pedaling efficiency and saddle position, further optimizing user health and performance outcomes in the indoor environment.

The Smart and Classic Indoor Trainers Market is subject to a complex interplay of Drivers, Restraints, and Opportunities (DRO), collectively forming significant impact forces shaping its trajectory. The primary driver is the global emphasis on health and preventative wellness, amplified by the convenience and safety offered by indoor training, especially in densely populated or climate-challenged regions. However, this growth is restrained by the high initial cost barrier associated with premium smart trainers and the required supplementary equipment, coupled with user fatigue arising from subscription overload necessary to access quality virtual content. The market is constantly exposed to the opportunity of expanding into complementary markets, such as corporate wellness programs and physical therapy, alongside leveraging 5G and metaverse technologies to create deeply immersive virtual training experiences.

Impact forces are predominantly driven by technological parity and digital integration. As smart trainer technology matures, core features like high accuracy (+/- 1% power) and high maximum resistance become standardized, intensifying competitive pressures on price and ecosystem integration. Companies that successfully merge hardware excellence with intuitive, engaging, and cost-effective software ecosystems (e.g., offering proprietary training content included with hardware purchase) gain a substantial competitive advantage. The market also faces external impact from the cyclical nature of cycling participation and the introduction of competing indoor fitness equipment, such as high-end treadmills and rowing machines, which vie for the same consumer spending on home fitness solutions.

The regulatory environment, particularly concerning data privacy (due to the collection of sensitive biometric data) and standardized power meter calibration, represents a moderate but critical impact force. Standardization efforts, such as those promoted by industry bodies regarding ANT+ and Bluetooth protocols, reduce fragmentation and enhance user experience, thereby indirectly driving adoption. Furthermore, sustainability and material sourcing are emerging forces, pushing manufacturers towards using recyclable materials and reducing the carbon footprint of production and transportation, appealing to environmentally conscious consumers and influencing brand reputation.

The Smart and Classic Indoor Trainers Market is highly differentiated across several critical axes, enabling manufacturers to target distinct consumer profiles ranging from budget-conscious casual riders to professional endurance athletes. Segmentation by Product Type (Smart vs. Classic) is the most impactful division, reflecting a divergence in price point, functionality, and connectivity. Smart trainers, which command premium pricing, are further segmented by resistance mechanism, notably direct-drive models dominating the performance sector due to their superior accuracy and road feel simulation, contrasted with wheel-on models which offer affordability and ease of bike mounting but sacrifice accuracy.

Segmentation by End-User distinguishes between the large Individual (Home Fitness) market and the rapidly expanding Commercial (Gyms, Studios, Performance Centers) segment. While the individual segment drives volume and technological adoption, the commercial segment demands trainers built for extreme durability, high utilization rates, and networked compatibility for group training software. Furthermore, geographic segmentation reveals stark differences in market maturity, with developed Western markets focusing on smart trainer replacement cycles and high-end features, while APAC markets are undergoing initial adoption phases, balancing price sensitivity with connectivity needs.

The analysis of these segments is vital for strategic market entry and product positioning. For instance, the Fluid Resistance mechanism, a subsegment of Classic Trainers, continues to hold relevance for users seeking a low-maintenance, progressive resistance system without the complexities of electronic calibration, maintaining a niche market share. Meanwhile, the Connectivity segment (ANT+, Bluetooth, Wi-Fi) is critical for smart trainer differentiation, as seamless dual-band connectivity is now a prerequisite for hardware success in an integrated software environment, enabling simultaneous data transmission to multiple devices like cycling computers and virtual platforms.

The value chain for the Smart and Classic Indoor Trainers Market is defined by high specialization in upstream component manufacturing and a growing reliance on digital ecosystems downstream. Upstream analysis reveals that core components—such as specialized magnets (for magnetic resistance), high-precision sensors (for power meters), electronic control units (ECUs), and bespoke resistance flywheel assemblies—are often sourced globally from highly specialized manufacturers in Asia. Companies like Wahoo and Tacx focus heavily on proprietary design and assembly but rely on established supply chains for semiconductors, firmware development, and complex mechanical components, where quality control and scale are paramount for maintaining the competitive edge in power accuracy and simulated road feel.

The distribution channel is increasingly bifurcated between direct and indirect routes. Direct distribution, primarily through dedicated e-commerce platforms and brand websites, allows manufacturers to maintain higher margins, gain direct consumer insights, and control the brand message and post-sales support experience. Indirect channels, encompassing specialty cycling stores and large online retailers (like Amazon or REI), remain essential for market reach, physical demonstration, and providing expert technical advice, especially for high-value smart trainers requiring initial setup assistance. Specialty stores also play a critical role in local community engagement and fulfilling immediate product needs.

Downstream value creation is significantly influenced by the complementary services and software ecosystem. The user experience is heavily dependent on interoperability with third-party software (Zwift, TrainerRoad), which adds substantial value post-purchase. This reliance means hardware manufacturers must maintain rigorous compliance with standard protocols (ANT+, Bluetooth) and continuously update firmware. Furthermore, the downstream phase includes critical support services such as technical troubleshooting, warranty fulfillment, and the provision of dedicated mobile applications for calibration and data management, all contributing to long-term customer satisfaction and brand loyalty.

The potential customer base for Smart and Classic Indoor Trainers is highly diversified, spanning from elite endurance athletes seeking quantifiable, structured training to casual fitness enthusiasts prioritizing convenience and entertainment. The core end-users, or buyers, can be categorized into three primary groups. Firstly, the performance-focused cyclist represents the high-value segment, demanding top-tier direct-drive smart trainers with exceptional power accuracy, realistic road feel, high maximum resistance, and dedicated integration with advanced training software. These individuals are typically engaged in competitive road cycling, triathlon, or virtual esports and prioritize data precision over initial cost.

Secondly, the general fitness and recreational rider forms the largest volume segment. These consumers seek trainers that balance cost-effectiveness with fundamental smart functionality, such as basic connectivity to virtual apps for motivation and group riding. They often gravitate toward mid-range wheel-on smart trainers or entry-level direct-drive units, viewing the trainer primarily as a comprehensive home fitness solution for adverse weather or time constraints. Their purchasing decisions are heavily influenced by ease of setup, reliability, and positive online reviews regarding noise level and software compatibility.

The third group constitutes commercial and institutional buyers, including professional sports teams, fitness studios, physical therapy clinics, and corporate wellness programs. These buyers require robust, heavy-duty trainers capable of enduring constant, high-intensity use across multiple users. Key purchase criteria include fleet management capabilities, centralized control systems, minimal maintenance requirements, and long-term warranties, often leading them to purchase in bulk directly from the manufacturer or specialized commercial distributors.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 550 Million |

| Market Forecast in 2033 | USD 985 Million |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Wahoo Fitness, Tacx (Garmin), Saris, Elite, Kinetic by Kurt, CycleOps, Xplova, ThinkRider, BKOOL, Minoura, Zycle, JetBlack, Alpe Endurance, Kickr, Zwift, TrainerRoad, RGT Cycling, Stages Cycling, SRM, Wattbike. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Smart and Classic Indoor Trainers Market is dominated by advancements in electronic resistance control, data accuracy, and multi-protocol connectivity standards. The shift from simple magnetic or fluid resistance to sophisticated electromagnetic resistance units is foundational to smart trainers. These units utilize complex servo-mechanisms and powerful electromagnets to instantaneously adjust resistance based on virtual terrain gradients or prescribed workout intervals dictated by external software. This high-speed control loop, managed by onboard firmware, is critical for achieving a realistic "road feel" and accurate simulation of inertia, often requiring robust processors and optimized algorithms to manage power output up to 2500 watts and simulate inclines up to 25%.

Connectivity technology is a major differentiating factor, with the majority of smart trainers now supporting dual-band connectivity using ANT+ FE-C (Fitness Equipment Control) and Bluetooth Smart (BLE). ANT+ FE-C allows the trainer to be controlled by compatible devices and software, ensuring open-source compatibility across the industry, while BLE offers simplified pairing with mobile devices and tablets. Recent technological focus includes incorporating Wi-Fi capabilities for faster firmware updates and more stable data transmission in densely networked environments, addressing latency concerns critical for competitive virtual racing. Furthermore, companies are investing in improving internal power meters, utilizing strain gauges and calibration routines to achieve professional-grade accuracy, typically advertised as +/- 1% or better.

Beyond core resistance and connectivity, the technology landscape includes continuous innovation in noise reduction and physical design. Direct-drive trainers, which eliminate the rear wheel, are inherently quieter, but manufacturers are employing advanced belt drives, optimized internal dampening systems, and heavier flywheels (up to 7-10 kg) to minimize vibration and enhance the kinetic feel of the ride. Peripheral technologies, such as motion plates and rocker plates, are gaining traction. These accessories utilize specialized hinges, springs, or air bladders to introduce lateral movement, further simulating the natural sway of a bike outdoors, addressing a key limitation of traditional static indoor training.

Smart trainers feature electronic resistance controlled by external software and provide precise data (power, speed) via ANT+ or Bluetooth. Classic trainers use manual resistance mechanisms (fluid or magnetic) and do not offer software integration or automatic resistance adjustment.

Market growth is primarily driven by the proliferation of engaging virtual cycling platforms (e.g., Zwift), the increasing consumer demand for structured, data-driven training, and the inherent convenience and safety of indoor exercise regardless of weather conditions.

Direct-drive trainers are generally considered superior for serious training due to higher power accuracy (typically +/- 1%), reduced noise levels, and the elimination of wheel/tire slip and wear, though they carry a significantly higher initial cost than wheel-on variants.

AI is set to enhance personalized training by dynamically adjusting resistance based on real-time biometric data (fatigue, heart rate variability), creating optimal, highly efficient workouts, and improving the realism of virtual environment interactions.

North America currently holds the largest market share in terms of value, owing to high adoption rates of connected fitness technology, strong purchasing power, and a mature infrastructure supporting virtual cycling ecosystems.

The preceding analysis represents a high-level strategic overview of the Smart and Classic Indoor Trainers Market, detailing current dynamics, technological inflection points, and key competitive factors shaping industry growth from 2026 through 2033. The convergence of cycling equipment manufacturing with advanced software services and AI integration is repositioning indoor trainers as indispensable elements of the broader connected fitness segment. Continued innovation in achieving higher levels of power accuracy, quieter operation, and deeper integration with VR/AR technologies will define success for leading market participants. Furthermore, expansion into Asia Pacific and the development of accessible, feature-rich entry-level smart trainers are crucial strategies for maximizing global market penetration over the forecast period.

The competitive landscape is characterized by established players defending their market share through robust hardware reliability and aggressive software development, juxtaposed against newer entrants focusing on niche technological improvements such as advanced kinetic simulation or hyper-accurate low-latency power measurement. Strategic mergers and acquisitions, exemplified by the integration of hardware firms into larger technology ecosystems, are expected to continue, consolidating market power and emphasizing the importance of end-to-end user experience. Regulatory scrutiny regarding data handling and competitive practices within the digital fitness ecosystem will become increasingly relevant as the market matures.

Future market resilience will be closely tied to the industry's ability to maintain high user engagement in virtual environments, mitigating 'subscription fatigue' through diversified content offerings and community building. The evolution of classic trainers, while declining in market share, serves as a vital entry point, providing essential basic training capabilities for budget-conscious consumers. However, long-term value generation overwhelmingly resides in the smart trainer segment, driven by the persistent demand for performance optimization, gamification, and remote training flexibility, making digital innovation the primary determinant of strategic advantage.

Investment outlook remains positive, especially for companies demonstrating clear differentiation in data reliability, user interface design, and ecosystem partnerships. Key areas for investor focus include firms specializing in advanced sensor technology, predictive AI coaching services, and hardware solutions that achieve exceptional noise suppression without compromising performance specifications. The synergy between hardware manufacturing and recurring software revenue models represents a highly attractive business structure, promising sustained financial performance beyond traditional equipment sales cycles.

In summary, the Smart and Classic Indoor Trainers Market is exiting a phase of rapid pandemic-driven growth and entering a period of refinement and technological deepening. Success hinges on mastering the seamless fusion of robust mechanical engineering with intelligent digital services, catering to a sophisticated consumer base that expects personalized, precise, and highly engaging fitness experiences year-round. Understanding regional adoption patterns and anticipating technological leaps, particularly in AI and connectivity standards, will be crucial for strategic decision-making in this dynamic sector.

The substantial investment required for high-fidelity road simulation, including complex flywheel mechanisms and responsive electronic braking systems, serves as a significant barrier to entry for new competitors lacking deep engineering expertise and capital. Established market leaders, therefore, maintain an edge through patent portfolios and economies of scale in component sourcing. The continuous enhancement of firmware, ensuring compatibility with evolving operating systems and third-party applications, demands dedicated R&D resources, further reinforcing the position of major industry players capable of maintaining long-term software support commitments.

The market also faces an evolving supply chain environment. Initial disruptions highlighted the fragility of relying on single-source suppliers for critical components like microprocessors and sensors. Moving forward, strategic resilience involves diversifying the supplier base and potentially near-shoring some assembly operations to mitigate geopolitical risks and improve time-to-market responsiveness. This strategic shift in manufacturing logistics, while increasing immediate operational costs, provides long-term stability essential for meeting unpredictable consumer demand fluctuations effectively and efficiently.

Finally, the sustainable lifespan and upgrade cycle of indoor trainers represent a critical consideration. As consumers invest heavily in smart trainers, they expect extended durability and feature upgrades through software updates, rather than forced hardware obsolescence. Companies that prioritize modular designs, facilitating easy maintenance and component replacement, will build greater consumer trust and foster brand loyalty, transforming the one-time purchase into a long-term relationship centered around performance and support. This focus on longevity and service efficiency will be a defining trend for market leaders in the latter half of the forecast period.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.