ID : MRU_ 435656 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

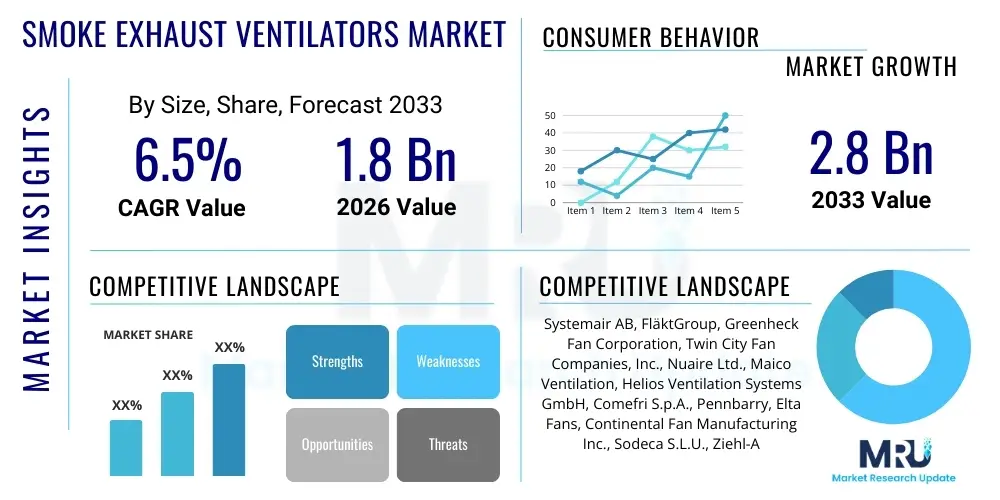

The Smoke Exhaust Ventilators Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 1.8 Billion in 2026 and is projected to reach USD 2.8 Billion by the end of the forecast period in 2033.

The Smoke Exhaust Ventilators Market encompasses the design, manufacturing, installation, and maintenance of mechanical systems crucial for smoke control and heat ventilation in occupied structures. These specialized ventilators are engineered to withstand high temperatures and operate reliably under emergency conditions, effectively removing combustion products such as toxic smoke and heat. Key product types include axial flow fans, centrifugal fans, and jet fans, each tailored for specific architectural requirements and smoke reservoir configurations, such as tunnels, car parks, and high-rise atriums. The fundamental purpose of these systems aligns directly with global fire safety standards, focusing on preserving tenable conditions for occupant evacuation and facilitating search and rescue operations by emergency services.

Major applications driving market demand span across critical infrastructure sectors, including commercial buildings (malls, offices, hotels), industrial facilities (factories, warehouses), transportation infrastructure (underground rail systems, road tunnels), and institutional complexes (hospitals, educational centers). The effectiveness of these systems is not only measured by air volume displacement but also by their integration capability within broader Building Management Systems (BMS) and compliance with performance-based design standards like EN 12101, NFPA 92, and relevant ISO protocols. The inherent benefits derived from advanced smoke exhaust solutions include significantly enhanced life safety, reduced structural damage from heat build-up, and minimized business interruption following a fire incident, thereby making them indispensable investments in modern construction projects.

Driving factors primarily revolve around the tightening of fire safety regulations mandated by governmental and international standardization bodies. Rapid urbanization, especially the construction boom in developing economies involving complex, high-density structures, mandates sophisticated smoke control strategies. Furthermore, increasing public awareness regarding workplace and residential safety, coupled with technological advancements in fan efficiency, sensor technology, and fire modeling software (Computational Fluid Dynamics - CFD), accelerate the adoption of superior smoke exhaust solutions. The replacement and retrofitting of aging ventilation infrastructure in established markets also provide substantial growth opportunities, ensuring continuous market momentum throughout the forecast period.

The global Smoke Exhaust Ventilators Market is experiencing robust expansion, characterized by strong business trends centered on regulatory compliance and technological integration. Commercial and infrastructural development, particularly in Asia Pacific and the Middle East, is fueling demand for high-capacity, high-temperature resistance fans. Key business trends show a shift towards service-based models, where installation, commissioning, maintenance, and regular system testing services contribute significantly to revenue streams, moving beyond pure product sales. Furthermore, consolidation among mid-sized manufacturers specializing in components like motors, impellers, and control panels is observed, aiming for integrated, full-system solutions that streamline procurement and installation processes for major construction contractors.

Regional trends indicate North America and Europe retaining leadership in technological sophistication, prioritizing energy-efficient fans and systems integrated with smart building platforms for predictive maintenance. However, the highest growth trajectory is anticipated in the Asia Pacific region, driven by massive infrastructure investments in China, India, and Southeast Asian nations, necessitated by expanding metro systems, airport terminals, and skyscraper construction. The Middle East maintains significant demand due to stringent safety codes applied to large-scale, iconic architectural projects. Emerging trends across all regions emphasize standardization and modularity, facilitating easier customization and quicker deployment of certified smoke exhaust systems that meet diverse local fire codes.

Segment trends reveal a distinct preference for axial flow fans in tunnel and large open-space applications due to their high thrust and relatively compact design. Centrifugal fans, known for high-pressure capabilities, remain dominant in ducted systems within commercial high-rises. In terms of end-use, the transportation sector, including road and rail tunnels, represents a major revenue segment, requiring continuous operation and specialized robust construction. The market is also seeing increased segmentation in control systems, moving from simple two-speed control to variable frequency drive (VFD) controls, enabling precise airflow management tailored to evolving fire conditions, thereby optimizing performance and reducing energy consumption during standby modes.

User inquiries concerning the integration of Artificial Intelligence (AI) in the Smoke Exhaust Ventilators Market frequently address predictive maintenance capabilities, optimization of system performance under dynamic fire scenarios, and AI’s role in regulatory compliance and certification. Users express interest in how machine learning algorithms can analyze data streams from smoke detectors, temperature sensors, and ventilation controls to anticipate system failures before they occur, reducing downtime and maintenance costs. A significant area of concern and expectation lies in AI's potential to model complex smoke movement dynamics in real-time, allowing ventilation systems to adapt instantaneously, thereby optimizing smoke extraction effectiveness beyond static, pre-programmed responses, leading to superior life safety outcomes and significantly increasing operational efficiency of complex smoke management systems.

The application of AI extends into the design phase, where Generative Design algorithms can rapidly iterate through thousands of potential fan placements and duct layouts, factoring in complex aerodynamic principles and building geometry to achieve optimal smoke clearance rates while minimizing installation complexity and cost. Furthermore, during operational lifetime, AI-driven diagnostics utilize vibrational analysis and thermal signatures of fan components to schedule highly accurate, condition-based maintenance, replacing traditional time-based schedules. This shift not only prolongs equipment lifespan but also ensures continuous compliance with stringent operational readiness requirements mandated by fire safety authorities, directly impacting insurance liabilities and building certification status.

In the future, AI integration is expected to standardize compliance reporting by automatically generating audit trails and performance validation documents, leveraging continuous data logging and comparative analysis against fire simulation models. This automation reduces the administrative burden associated with fire safety management and enhances transparency. For manufacturers, AI assists in supply chain optimization, predicting component needs based on forecasted demand and historical failure rates, contributing to a more resilient and efficient manufacturing process for these critical safety components.

The dynamics of the Smoke Exhaust Ventilators Market are significantly influenced by a confluence of regulatory pressures (Drivers), high capital expenditure requirements (Restraints), and increasing demand for smart safety infrastructure (Opportunities), all interacting under strong Impact Forces related to global construction trends and climate change adaptation. Drivers predominantly stem from rigorous government mandates requiring fire safety compliance in new and existing large-scale construction, particularly high-rise commercial and residential complexes where smoke management is a principal concern. The increasing stringency of standards, such as those governing temperature resistance (F300, F400 ratings) and guaranteed operational periods, pushes manufacturers toward innovation and higher quality output. This regulatory environment creates a baseline demand that is resistant to typical economic downturns, positioning safety components as non-negotiable construction elements.

Restraints largely center on the high initial cost associated with certified, robust smoke exhaust systems, including specialized ductwork, high-temperature fans, and complex control panels. This high capital expenditure can sometimes deter smaller developers or lead to the adoption of non-compliant or cheaper alternatives in regions with lax enforcement. Furthermore, the specialized installation and maintenance requirements necessitate highly skilled labor, leading to higher operational costs and potential challenges in maintenance quality, particularly in less developed markets. Regulatory fragmentation across different countries or even regions within a country presents a persistent challenge, requiring manufacturers to maintain multiple product certifications and design variations, increasing complexity and time-to-market.

Opportunities are substantially driven by the retrofitting market, where aging infrastructure in developed economies requires upgrades to meet modern fire codes, especially in tunnels and legacy commercial buildings. The burgeoning market for integrated smart building solutions presents another key opportunity, allowing manufacturers to combine smoke exhaust systems with overall HVAC, security, and smart fire detection networks, offering greater efficiency and centralized control. The Impact Forces of technological advancement are pushing the market towards more energy-efficient, quieter, and IoT-enabled systems, ensuring that future products not only meet safety needs but also align with sustainability goals. The increasing frequency of large-scale urban fires globally also acts as a socio-economic impact force, continually reinforcing the necessity for advanced and reliable smoke management technologies.

The Smoke Exhaust Ventilators Market is segmented based on critical technical and application parameters, providing a detailed view of product adoption across various end-use sectors. Key segmentation criteria include the type of fan technology utilized (axial, centrifugal, jet), the rated temperature resistance and operational time, the motor type and drive mechanism, and the distinct application verticals where these systems are deployed. Understanding these segments is crucial as procurement decisions often hinge on balancing performance metrics (such as airflow rate and pressure capacity) with the specific environmental demands (like size constraints and ducting requirements) of the project. The dominance of a particular fan type in a region often correlates directly with the prevailing type of infrastructure development, such as the use of jet fans being strongly linked to tunnel construction projects.

The product segmentation, particularly between axial flow and centrifugal fans, defines the market's technological landscape. Axial fans are favored for high-volume, straight-line ventilation requirements, often seen in large industrial bays or transportation arteries, due to their efficiency in moving air over long distances with minimal duct resistance. Centrifugal fans, conversely, excel in creating high static pressure, making them essential for multi-story buildings where air must be pushed through extensive, complex ductwork systems to reach remote smoke reservoirs. This functional distinction ensures that both technologies maintain substantial market share, catering to highly divergent architectural needs within the fire safety domain.

Further analysis of the end-use segmentation highlights the crucial role of infrastructure and commercial sectors in market growth. The regulatory requirements in transportation infrastructure (tunnels, subways) are particularly stringent, demanding the highest level of reliability and temperature resilience (F400 120 minutes), driving premium pricing and technological investment in this segment. Conversely, the high volume of construction in the residential and general commercial segments, while often employing slightly less complex systems, contributes significantly to the overall volume of installed units, ensuring steady demand across various product grades and certifications globally.

The value chain for the Smoke Exhaust Ventilators Market begins with sophisticated upstream activities involving the sourcing of high-grade, heat-resistant raw materials, including specialized steels, high-temperature composite materials for impellers, and fire-resistant electronic components for motors and controls. Key upstream suppliers include manufacturers of high-efficiency motors, specialized bearings, and providers of certified insulation materials. Quality control at this stage is paramount, as the final product must retain structural integrity and functionality at extreme temperatures (up to 400°C). Strategic relationships with reliable material suppliers who can ensure traceability and compliance with international standards (such as UL and CE) are essential for maintaining manufacturing certification and product reputation, as failure to comply leads to severe legal and financial repercussions in this safety-critical industry.

The manufacturing stage involves highly specialized production techniques, including precision casting, dynamic balancing of impellers to minimize vibration, and rigorous end-of-line testing, often including mandated physical stress tests and high-temperature simulations. Manufacturers often act as system integrators, assembling complex packages that include the fan unit, attenuators, VFDs, and sophisticated control panels. Distribution channels are typically complex and rely heavily on technical expertise. Direct channels are utilized for large, custom infrastructure projects (like major tunnel contracts), involving direct engagement between the manufacturer and the EPC contractor or government authority. Indirect channels involve networks of specialized distributors, value-added resellers (VARs), and authorized installers who possess the necessary fire safety certifications and engineering capability to specify and install compliant systems in commercial and residential developments.

Downstream activities are dominated by installation, commissioning, and, crucially, post-sale service and maintenance. Installation requires specialized mechanical and electrical engineers trained in fire safety codes to ensure the system integrates correctly with the building's overall fire protection matrix. The long-term profitability often resides in the service contracts, which involve mandatory periodic inspection, cleaning, and performance testing (e.g., simulating fire conditions) to ensure the system remains compliant throughout the building's lifecycle. End-users, who are primarily the building owners, facility managers, or infrastructure operators, rely heavily on these downstream service providers to mitigate operational risks and maintain regulatory adherence, thereby closing the loop on a high-stakes, performance-driven value chain where reliability is the ultimate metric of success.

Potential customers for smoke exhaust ventilators represent a diverse range of public and private sector entities responsible for managing large, enclosed spaces where occupant safety is a critical concern. These customers are broadly categorized into major construction contractors, infrastructure developers, commercial real estate owners, and governmental bodies overseeing public safety and transportation networks. The primary buyers are not typically the end occupants, but rather the entities responsible for designing, constructing, and maintaining the building or infrastructure. For large commercial projects, the decision-making unit often includes fire safety consultants, mechanical, electrical, and plumbing (MEP) engineers, and project managers who specify the required performance standards based on local and international fire codes, leading to substantial procurement opportunities for specialized manufacturers.

A significant segment of the customer base includes operators of critical national infrastructure, such as metropolitan transit authorities, national highway agencies, and airport operators. These entities require robust, highly redundant systems capable of operating under extreme stress for extended periods, making them customers for premium, certified F400 systems and specialized jet fan installations. Procurement processes in this segment are often regulated by long-term public tenders, emphasizing long-term reliability, low maintenance burden, and guaranteed availability of spare parts and specialized maintenance services, creating market loyalty based on proven performance history and stringent certification standards.

Furthermore, facility management companies and corporate real estate firms that manage large portfolios of commercial and residential properties constitute a growing segment of potential customers, particularly in the aftermarket and retrofit domain. As fire codes evolve and buildings age, these managers require upgrades and replacements to ensure compliance, creating a consistent revenue stream for maintenance and system modernization. Their purchasing criteria often prioritize energy efficiency, noise reduction, and seamless integration with existing building management systems, seeking solutions that minimize operational disruption while maximizing safety compliance and occupant comfort within the confines of stringent safety mandates.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 2.8 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Systemair AB, FläktGroup, Greenheck Fan Corporation, Twin City Fan Companies, Inc., Nuaire Ltd., Maico Ventilation, Helios Ventilation Systems GmbH, Comefri S.p.A., Pennbarry, Elta Fans, Continental Fan Manufacturing Inc., Sodeca S.L.U., Ziehl-Abegg SE, Soler & Palau Ventilation Group, Howden Group, Ventmeca, Novenco, Dospel, Aldes Group, Vostermans Ventilation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Smoke Exhaust Ventilators Market is defined by innovation in materials science, motor efficiency, and advanced control systems, all geared toward maximizing reliability and performance under extreme conditions. A central focus is on enhancing the temperature resistance and operational lifespan of the fan components. This includes the use of specialized high-temperature bearings, optimized impeller designs forged from heat-resistant alloys, and the development of high-efficiency, fire-rated motors (often utilizing Class H or higher insulation) capable of maintaining full performance in environments exceeding 300°C for up to two hours. The integration of advanced computational fluid dynamics (CFD) modeling during the design phase is standard practice, ensuring that physical prototypes meet theoretical smoke extraction performance specifications under the most demanding regulatory scenarios, significantly reducing the time and cost associated with mandatory physical certification testing.

Another pivotal technological advancement involves the pervasive adoption of Variable Frequency Drive (VFD) systems. VFDs allow for precise control over fan speed and airflow, moving beyond simple on/off or two-speed operation. This modulation capability is critical for achieving pressure differential requirements in stairwells and lobbies, and for tuning the extraction rate in tunnels to maintain smoke stratification—a key safety requirement. VFDs also offer substantial energy savings during normal standby operation and reduce mechanical wear and tear during activation sequences. Furthermore, the integration of specialized sensors (vibration, temperature, and current monitoring) directly into the fan unit facilitates condition monitoring, feeding data to the building’s supervisory control and data acquisition (SCADA) system for proactive maintenance alerts, a precursor to full AI integration.

The ongoing development of jet fan technology for enclosed vehicle spaces, such as car parks and road tunnels, represents a distinct technological niche. Modern jet fans leverage advanced aerodynamic principles to create high-velocity air streams (impulse) that push smoke directionally without the need for extensive conventional ducting, significantly simplifying installation and reducing construction costs. Recent innovations include reversible jet fans and those integrated with acoustic dampening materials to minimize noise pollution in noise-sensitive urban environments. The future technology trajectory emphasizes full network connectivity, enabling remote diagnostics, firmware updates, and seamless communication with external emergency response platforms, transforming the ventilator from a passive mechanical component into an active, intelligent node within the overall building safety ecosystem.

Regional dynamics play a crucial role in shaping the Smoke Exhaust Ventilators Market, driven by variances in construction standards, regulatory enforcement, and infrastructure investment cycles. North America (primarily the US and Canada) is characterized by highly matured fire safety regulations (NFPA standards) and a strong emphasis on performance-based design. The market here focuses heavily on technologically advanced, energy-efficient centrifugal systems for commercial high-rises and robust tunnel ventilation equipment. Replacement and refurbishment of existing systems constitute a major demand driver, complemented by the adoption of sophisticated digital control systems that integrate seamlessly with smart city infrastructure projects and complex building energy management systems.

Europe, governed by the stringent EN 12101 series of standards and the Construction Products Regulation (CPR), demonstrates high demand for F300 and F400 certified products. Western European countries are leaders in promoting sustainable building practices, leading to a preference for highly efficient fans with minimal noise output. The region is witnessing steady growth in urban transportation infrastructure, particularly cross-border rail and road tunnels, necessitating high-specification, redundant smoke control systems. Eastern Europe, while adopting Western European standards, provides opportunities driven by significant investments in modernizing commercial and industrial real estate, pushing demand for cost-effective, certified solutions.

The Asia Pacific (APAC) region stands out as the highest growth market globally, fueled by unprecedented rates of urbanization and infrastructure development in countries like China, India, and Southeast Asia. The construction of mega-cities, extensive metro networks, and the world's tallest buildings mandates the installation of complex, high-performance smoke exhaust systems. While regulatory compliance can vary, the adoption of international standards is increasing, particularly in high-value projects backed by foreign investment. The Middle East and Africa (MEA), especially the GCC nations (UAE, Saudi Arabia), require bespoke, ultra-high-specification systems for monumental architectural projects, often demanding the highest temperature ratings (F400 120 minutes) and specialized systems designed to operate reliably in harsh, arid climates, making it a critical, albeit niche, market for premium product offerings.

F300 fans are certified to operate at 300°C for a minimum of 60 minutes, whereas F400 fans are certified to operate at the higher temperature of 400°C for 120 minutes. F400 systems are mandatory for critical infrastructure like tunnels and key escape routes in very high-rise buildings where extended operational integrity is non-negotiable for safety and structural survival. The higher rating requires specialized materials and rigorous testing protocols to achieve certification.

VFD integration allows the fan system to modulate airflow speed and pressure precisely, moving beyond simple fixed-speed operation. This precision is vital for maintaining specific pressure differentials in safety zones (like pressurized stairwells) and optimizing smoke extraction based on real-time fire conditions, which significantly improves energy efficiency during standby and ensures adaptive compliance during an actual emergency event.

Computational Fluid Dynamics (CFD) modeling simulates smoke and heat movement within a building or tunnel structure under fire conditions. It allows engineers to predict the performance of the proposed ventilation system, optimize fan placement and size, and validate that the design meets performance-based fire codes, thereby reducing installation errors and ensuring system effectiveness prior to costly physical installation and commissioning.

The Asia Pacific (APAC) region, driven by extensive urbanization, massive infrastructure projects (metro systems, international airports), and a gradual harmonization towards international fire safety standards, is forecast to experience the highest Compound Annual Growth Rate (CAGR) due to the sheer volume of new construction requiring mandatory fire protection systems.

The market is predominantly governed by two major international frameworks: the European EN 12101 series (especially important for F-ratings and CE marking under the Construction Products Regulation - CPR) and the American NFPA 92 standard (Standard for Smoke Control Systems). Compliance with these standards is essential for market access and liability management across developed and developing economies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.