ID : MRU_ 438750 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

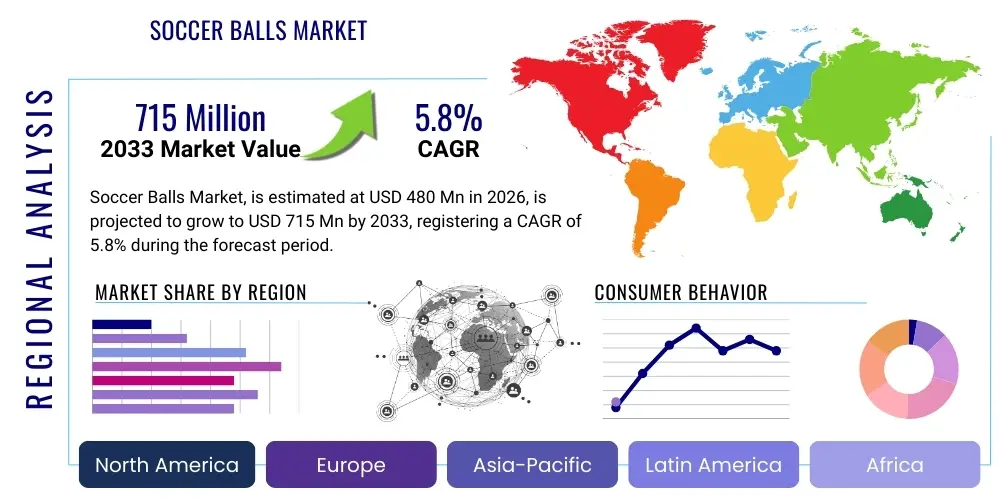

The Soccer Balls Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 480 Million in 2026 and is projected to reach USD 715 Million by the end of the forecast period in 2033. This consistent expansion is underpinned by the increasing global participation in soccer, both at professional and recreational levels, coupled with rising consumer demand for high-performance and technologically advanced equipment. The cyclical nature of major international soccer tournaments, such as the FIFA World Cup and continental championships, provides significant impetus for sales, driving replacement demand and promotional activities across key demographics.

Market size determination is further influenced by innovation in material science, focusing on enhanced durability, reduced water absorption, and improved aerodynamics. Manufacturers are continually investing in research and development to create balls that meet stringent regulatory standards set by governing bodies like FIFA. The shift toward sustainable manufacturing practices, incorporating recycled or bio-based materials, is emerging as a critical factor shaping market valuation, appealing to environmentally conscious consumers and organizations. This focus on material innovation translates directly into higher average selling prices (ASPs) for premium match balls, contributing substantially to overall market value growth.

The Soccer Balls Market encompasses the global production and distribution of spherical inflatable objects specifically designed and manufactured for the sport of soccer (football). These products vary widely based on material composition, size, weight, intended application (match play, training, or recreation), and construction method (hand-stitched, machine-stitched, or thermally bonded). The core product is generally regulated by international standards, primarily those set by the Fédération Internationale de Football Association (FIFA), ensuring uniformity in official competition. Major applications span professional leagues, amateur clubs, school sports programs, and recreational activities in parks and community centers globally. The essential utility of the soccer ball makes it indispensable for participation, cementing its position as a staple in the sporting goods sector.

Key benefits driving market adoption include improved performance attributes, such as superior flight stability, predictable trajectory, and optimal feel and control, especially in premium-grade balls used for competitive matches. Technological advancements, particularly in thermal bonding techniques, have significantly enhanced the impermeability and shape retention of balls, extending their lifespan and maintaining consistency across varied weather conditions. Driving factors for market growth include the robust globalization of soccer, massive investment in youth development programs worldwide, and the substantial rise in disposable income in emerging economies, enabling greater consumer expenditure on sporting equipment. Furthermore, aggressive marketing strategies employed by major sports brands, often involving endorsements by world-renowned athletes and exclusive sponsorship deals with major leagues and tournaments, substantially fuel demand.

The Soccer Balls Market demonstrates robust growth, primarily fueled by the increasing popularity and accessibility of the sport globally, coupled with significant technological advancements in product manufacturing. Key business trends indicate a strong move towards thermal bonding techniques, replacing traditional stitching methods to offer superior water resistance and aerodynamic performance, especially in professional-grade balls. The competitive landscape is dominated by a few major global sportswear giants who leverage strong brand recognition, exclusive sponsorships, and extensive distribution networks to maintain market share. Sustainability is an emerging trend, with manufacturers exploring eco-friendly materials and ethical supply chain practices to cater to evolving consumer preferences and regulatory pressures across developed markets.

Regionally, Asia Pacific (APAC) is projected to exhibit the highest growth rate, driven by massive population density, increasing investment in sports infrastructure (particularly in India, China, and Southeast Asia), and rising middle-class engagement with organized sports. North America and Europe remain foundational markets, characterized by high ASPs and consistent demand for replacement and high-specification match balls, sustained by established professional leagues and robust youth participation structures. Segment trends highlight that synthetic leather remains the material of choice due to its balance of cost, durability, and performance. The application segment sees match play balls generating the highest revenue, although the training and recreational segments represent the largest volumetric demand, driven by everyday use and attrition.

Common user inquiries regarding AI’s impact on the Soccer Balls Market center on three primary themes: how AI can optimize manufacturing efficiency, whether AI technology will be integrated into the balls themselves for performance tracking, and how predictive analytics might influence inventory management and seasonal sales forecasting. Users are keenly interested in the application of machine learning for defect detection during the thermal bonding process, ensuring high quality and consistency across mass production runs. There is also significant curiosity about 'smart ball' technology, where embedded micro-sensors (potentially analyzed using AI algorithms) could provide real-time data on spin rate, velocity, and trajectory, enhancing training methods and referee decisions. Manufacturers are leveraging AI-driven supply chain models to anticipate demand spikes linked to major tournaments, thereby minimizing overstocking and stockouts, optimizing distribution logistics, and improving overall market responsiveness.

The dynamics of the Soccer Balls Market are shaped by a complex interplay of Drivers, Restraints, and Opportunities (DRO), which collectively exert significant impact forces on market trajectory. The primary driver is the enduring and expanding global participation base for soccer, reinforced by demographic shifts, substantial investment in sports infrastructure, and the continuous globalization of major leagues which elevates the sport’s commercial profile. Furthermore, the mandatory replacement cycle for professional match balls, which are often replaced several times per season to maintain optimal competitive standards, ensures sustained demand in the premium segment. However, the market faces significant restraint from the proliferation of counterfeit and low-quality imitation products, particularly in developing markets, which erode the revenue potential of genuine manufacturers and undermine brand integrity.

Restraints also include volatility in raw material prices, particularly for synthetic leather (PU and PVC) and rubber bladders, which directly impacts manufacturing costs and profit margins. Moreover, stringent regulations concerning fair labor practices and environmental standards in manufacturing regions impose compliance burdens, necessitating potentially higher operational expenditures. Opportunities for growth are abundant, notably through geographical expansion into untapped markets in Africa and specific parts of Asia where organized soccer is rapidly professionalizing. Innovation in sustainable materials and the integration of smart technologies (IoT and RFID) into soccer balls present significant avenues for premiumization and technological differentiation, attracting a higher willingness to pay from niche segments focused on data-driven performance analysis. The overall impact force is generally positive, driven by the strong cultural foundation of the sport globally, making the market relatively resilient to minor economic fluctuations, though heavily influenced by major tournament cycles.

The Soccer Balls Market is meticulously segmented based on material, size, application, and distribution channel, providing a granular view of consumer preferences and operational dynamics. Segmentation by material is crucial as it dictates the price point, durability, and performance characteristics of the ball, differentiating between high-end match balls (typically PU/Synthetic Leather with thermal bonding) and mass-market training or recreational balls (often PVC or durable synthetic rubber). Analyzing these segments allows manufacturers to tailor their production lines and marketing strategies to specific consumer needs, whether they are focused on professional performance, rigorous durability for training, or simple affordability for recreational play.

Application segmentation differentiates between match balls, training balls, and recreational balls, reflecting the different performance expectations and usage frequencies. Match balls require FIFA-approved standards and contribute the highest ASP, while training balls emphasize robustness and longevity. Furthermore, size segmentation (Size 5 for adults, Size 4 for juniors, and smaller sizes) ensures products meet the requirements of various age groups and skill levels, supporting youth development initiatives globally. The distribution channel breakdown, encompassing both online and traditional brick-and-mortar retail, is vital for optimizing market reach, with e-commerce rapidly gaining traction due to convenience and direct-to-consumer models, though physical stores remain critical for product testing and immediate purchase.

The value chain for the Soccer Balls Market begins with the upstream segment, which involves the sourcing and processing of core raw materials, primarily synthetic leather (PU and PVC), rubber for bladders, various textiles for inner linings, and chemical bonding agents. Key activities at this stage include the production of high-quality synthetic sheets that meet specific specifications for texture, thickness, and color fastness. Manufacturers often engage in long-term contracts with specialized chemical and material suppliers to ensure a stable supply of consistent quality inputs. Optimization at the upstream level is critical for cost management, as raw material costs constitute a significant portion of the final product’s cost, particularly for premium match balls where performance standards necessitate specialized materials.

The midstream phase focuses on manufacturing, encompassing panel cutting, graphic printing, internal lining application, bladder insertion, and the crucial process of assembly, which can involve hand stitching, machine stitching, or the increasingly dominant thermal bonding technique. Quality control and testing (including bounce, weight, water absorption, and shape retention tests) are integral parts of the manufacturing process to ensure compliance with FIFA standards. Downstream activities involve warehousing, logistics, marketing, and distribution. Distribution channels are bifurcated into direct sales (brand-owned stores, dedicated e-commerce) and indirect sales (third-party wholesalers, sporting goods retailers, and large format department stores). The growing reliance on e-commerce necessitates sophisticated logistics management to handle global fulfillment efficiently.

The effectiveness of the value chain is highly dependent on streamlined supply chain management and efficient utilization of both direct and indirect distribution methods. Direct channels allow manufacturers tighter control over branding, pricing, and customer experience, often used for new product launches or high-end items. Indirect channels, primarily relying on established global and regional sports retailers, offer vast market reach and volume sales, particularly crucial for training and recreational segments. Successful companies invest heavily in optimizing the link between high-tech manufacturing centers (often located in Asia for cost benefits) and global consumer markets, using advanced IT infrastructure to manage complex inventory movements and forecast retail uptake across diverse geographical territories.

The potential customer base for the Soccer Balls Market is remarkably broad, spanning professional entities, organized amateur associations, educational institutions, and individual recreational players. Professional soccer clubs and international governing bodies represent the high-value segment, as they procure large volumes of premium, certified match balls frequently throughout the season for official use and training, prioritizing performance and FIFA certification over cost. Amateur and semi-professional clubs and leagues constitute the volume segment, demanding durable training balls and moderately priced match balls suitable for varied field conditions.

Educational institutions, including schools, colleges, and universities, are major buyers, focusing on durability, bulk purchasing, and standardized sizes for physical education classes and organized university sports. Individual consumers, ranging from aspiring young players enrolled in youth academies to adult recreational enthusiasts, form the largest segment volumetrically. These end-users typically purchase balls for personal training, casual play, or as gifts, and their purchasing decisions are heavily influenced by brand loyalty, perceived durability, and accessibility through retail channels. The growth in youth soccer programs globally is continuously replenishing and expanding the base of potential customers demanding appropriate size and quality balls for development.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 480 Million |

| Market Forecast in 2033 | USD 715 Million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Adidas, Nike, Puma, Wilson, Mitre, Select Sport, Decathlon, New Balance, Under Armour, Molten, Umbro, Diadora, Kelme, Lotto, Joma, Penalty, Kipsta, Sondico, Mikasa, Vizari. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Soccer Balls Market is undergoing continuous transformation, shifting away from traditional hand-stitching towards highly automated and precision-based manufacturing techniques. The most significant technological advancement is the widespread adoption of thermal bonding, where the panels are heat-fused rather than sewn together. This process eliminates seams, resulting in a perfectly spherical ball that offers superior water resistance, reduced weight fluctuation in wet conditions, and enhanced durability. Thermal bonding ensures consistent flight characteristics and predictability, which is paramount for professional match play, driving major brands to invest heavily in specialized machinery and proprietary bonding agents. This technology is crucial for achieving the rigorous quality standards mandated by governing bodies like FIFA for official competition use.

Material science innovation also plays a critical role, focusing on advanced polyurethane (PU) formulations layered over compressed foam or rubber bladders. Modern soccer balls utilize multi-layered construction, often involving specialized backing materials that help maintain the ball's shape and provide the desired 'soft touch' feel without compromising structural integrity. Manufacturers are integrating micro-textured surfaces, sometimes using embossed dimples or geometric patterns, which are engineered through computational fluid dynamics (CFD) to optimize aerodynamics, reducing drag and ensuring stable flight paths, thereby minimizing the knuckle-ball effect sometimes associated with older designs. These surface technologies enhance grip and control for the player, regardless of the weather conditions encountered during play.

Furthermore, the development of 'Smart Ball' technology represents a nascent but rapidly evolving segment. These balls incorporate embedded sensors, microchips, and low-power telemetry systems capable of tracking precise spatial and kinematic data, such as velocity, spin rate, and point of contact. This data is transmitted in real-time to external devices or analytic platforms. While currently more prevalent in high-level training and testing environments, the maturation of battery life and sensor miniaturization, coupled with AI analytics, is expected to expand their application into mainstream training and potentially revolutionize refereeing decisions, particularly concerning goal line technology and offside calls. This integration of IoT technology is moving soccer balls beyond simple sporting goods into complex electronic instruments.

Regional dynamics play a crucial role in shaping the Soccer Balls Market, influenced by population, cultural affinity for the sport, economic development, and investment in sports infrastructure. Asia Pacific (APAC) stands out as the fastest-growing region, driven by massive consumer bases in countries like China, India, and Indonesia. These nations are experiencing rising disposable incomes and governmental initiatives promoting sports participation, particularly youth soccer, leading to explosive growth in demand for both recreational and entry-level training balls. APAC is also a critical global manufacturing hub, contributing significantly to the supply chain efficiency of international brands, though domestic consumption is now increasingly becoming the primary growth driver.

Europe and North America collectively represent the largest revenue generators, characterized by mature markets, high consumer spending power, and established professional league structures (e.g., Premier League, Bundesliga, MLS). Demand in these regions is heavily focused on premium, high-ASP match balls that require frequent replacement, ensuring stable revenue streams for market leaders. Europe, with its deeply ingrained soccer culture, dictates global trends in performance and design standards. Conversely, Latin America, while having an intense passion for soccer, often faces economic challenges that favor slightly lower-priced, durable balls, though its contribution to global demand remains vital due to high participation rates.

The market is primarily driven by the expanding global participation base in soccer, encompassing professional, amateur, and recreational levels, coupled with the mandatory replacement cycles for high-performance match balls in professional leagues.

Thermal bonding is highly significant; it represents the current technological standard for premium match balls. It offers superior advantages such as optimal spherical shape retention, zero water absorption, and enhanced durability, surpassing the performance consistency of hand-stitched balls, making it crucial for FIFA certification.

Europe currently holds the largest revenue share in the Soccer Balls Market, sustained by high average selling prices for premium balls and the presence of numerous established professional leagues and tournaments that require frequent equipment renewal.

Environmental factors are increasingly important. Manufacturers are focusing on sustainable opportunities, including using recycled plastics, bio-based polyurethanes, and implementing ethical supply chain practices to meet consumer demand for eco-friendly sporting goods and comply with evolving global environmental regulations.

While not yet standard equipment for all tiers of play, smart soccer balls, equipped with IoT sensors for performance tracking and data analysis, are projected to become increasingly integrated into professional training and potentially refereeing systems. Their adoption rate depends on technological cost reduction and broader regulatory acceptance.

Size 5 is the official ball size used in professional and adult competitive matches, typically measuring 68-70 cm in circumference. Size 4 is specifically designed for junior players, usually ages 8 to 12, offering a smaller circumference and lighter weight to facilitate proper technique development during crucial developmental stages.

Counterfeit products pose a major restraint, particularly in emerging economies. They negatively impact the genuine manufacturers' revenue and reputation, undermine brand value, and often fail to meet safety and quality standards, confusing consumers and distorting market pricing mechanisms.

Synthetic leather, primarily polyurethane (PU), dominates the premium and match play segment due to its superior softness, water resistance, and ability to replicate the feel of natural leather while offering greater consistency and durability. PVC remains prevalent in the cost-sensitive recreational segment.

The average lifespan of a professional match ball can be relatively short under intense competitive conditions. While designed for durability, professional clubs often replace balls every few sessions or matches to maintain optimal performance characteristics, particularly shape retention and precise weight, leading to high replacement demand.

Aerodynamic advancements, often using computational fluid dynamics (CFD), focus on optimizing the outer panel configuration and surface texture (e.g., dimples or grooves) to reduce air resistance (drag) and ensure a stable, predictable flight path, thereby enhancing player control over trajectory and spin.

Major tournaments like the FIFA World Cup create significant sales spikes. They drive brand awareness through exclusive ball sponsorships, stimulate retail promotional activities, and generate massive replacement demand from professional and amateur clubs upgrading their equipment to align with current tournament standards and designs.

The online distribution channel, including e-commerce portals and direct-to-consumer (DTC) brand websites, is experiencing the fastest growth. This is driven by consumer preference for convenience, wider product selections, competitive pricing, and efficient direct fulfillment logistics.

Modern soccer ball bladders are primarily made from high-quality butyl rubber or latex. Butyl bladders are favored for their excellent air retention properties and durability, while latex bladders, though requiring more frequent inflation, offer a superior, softer touch preferred by some professional players.

In the recreational segment, the key differentiating feature is often extreme durability and resistance to harsh surfaces (such as concrete or abrasive grass). These balls typically utilize heavy-duty PVC or highly abrasion-resistant synthetic compounds, prioritizing longevity over peak aerodynamic performance.

Manufacturers ensure consistency through stringent quality control protocols, including automated weight and circumference checks, water absorption tests, rebound height measurements, and often utilizing AI-driven machine vision systems to monitor thermal bonding precision and panel alignment.

The Soccer Balls Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033, reflecting stable global demand and continued product innovation.

The rising popularity of specialized variants like futsal and beach soccer creates adjacent market opportunities for specific ball types (e.g., low-bounce futsal balls). While distinct, these trends collectively boost overall demand for organized soccer equipment and expand the consumer base familiar with performance-oriented sporting goods.

The primary constraint is the volatility and fluctuation in the prices of key petrochemical-derived raw materials, specifically polyurethane (PU) and polyvinyl chloride (PVC), which directly impacts operational costs and necessitates complex hedging strategies for manufacturers.

Africa is viewed as a significant opportunity due to its vast, young population, deeply rooted passion for soccer, increasing economic stability in key regions, and growing professionalization of domestic leagues, driving future volume demand for affordable and intermediate-grade equipment.

Upstream activities involve the initial sourcing and refinement of raw materials, including the production of specialized synthetic leather sheets, rubber for bladders, and chemical bonding agents necessary for the construction of the soccer ball.

The Match Play application segment generates the highest revenue due to the high average selling price (ASP) of FIFA Quality Pro certified balls and the frequent replacement demands imposed by professional clubs and elite competition standards.

Major brands secure dominance by leveraging exclusive sponsorship contracts with FIFA and continental bodies, extensive global distribution networks, massive brand recognition, and continuous investment in performance technology R&D and targeted athlete endorsements.

AI is used in quality control through machine vision systems that analyze images of the ball during thermal bonding or printing stages. These systems use learning algorithms to instantly identify and classify subtle defects, ensuring panel alignment accuracy and minimizing production flaws.

The FIFA Quality Pro standard is significant because it guarantees that a ball meets the most rigorous performance criteria, including high water repellency, minimal change in pressure, perfect shape retention, and consistent rebound. This certification is mandatory for use in professional matches and drives premium pricing.

Training balls are engineered for maximum durability and longevity, often using more robust synthetic materials and machine stitching to withstand extensive, repeated use. Match balls prioritize optimal aerodynamic performance, responsiveness, and touch, typically utilizing thermal bonding and specialized layered PU materials.

The sustainability trend manifests through the use of recycled or bio-based synthetic components, reducing volatile organic compounds (VOCs) in bonding agents, and implementing energy-efficient manufacturing processes, aiming to lower the overall environmental footprint of the product life cycle.

The primary challenge in developing markets is intense price competition, often exacerbated by the prevalence of unauthorized, low-cost counterfeit goods, which pressures genuine manufacturers to manage costs tightly while attempting to maintain adequate quality standards.

The foam layer, often compressed EVA or specialized foam, is highly important. It sits beneath the outer cover and provides critical cushioning, contributing to the ball’s soft touch and helping to distribute impact forces uniformly, which enhances control and accuracy during striking.

Factors contributing to the high replacement rate include the need to maintain pristine condition for professional performance, the abrasive nature of competitive play surfaces, minor structural damage or loss of optimal inflation pressure, and team sponsorship agreements that mandate the use of new equipment frequently.

CFD is utilized to simulate airflow patterns over the ball's surface geometry. This engineering technique helps designers optimize panel shapes and surface textures to reduce aerodynamic turbulence and drag, ensuring the ball maintains a straighter, more predictable flight path at high velocities.

Entry-level recreational balls typically use Polyvinyl Chloride (PVC) for the outer casing. PVC is highly cost-effective and offers excellent abrasion resistance, making it suitable for rougher playing surfaces where durability is prioritized over professional-grade touch and performance.

Downstream activities encompass all processes related to getting the finished product to the end consumer, including packaging, inventory management, global logistics, marketing and advertising campaigns, and the actual distribution through retail channels (both physical stores and e-commerce platforms).

Global economic conditions primarily influence the market through consumer spending on discretionary items like sporting goods. Economic downturns may lead consumers to choose cheaper recreational balls, while sustained growth fuels demand for premium, higher-ASP match balls in established markets.

DTC channels offer key advantages such as higher profit margins by eliminating intermediary costs, tighter control over brand messaging and customer experience, and direct access to valuable consumer data for inventory planning and personalized marketing strategies.

Size 3 balls are utilized almost exclusively for the youngest age groups, typically under 8 years old, in foundational youth soccer programs. Their minimal size and weight are crucial for teaching basic control skills without discouraging participation due to excessive difficulty or weight.

Stricter labor laws, particularly those related to working conditions and fair wages in major manufacturing hubs (e.g., Pakistan, China), necessitate compliance monitoring, potentially increasing production overheads but improving corporate social responsibility (CSR) ratings and brand image.

PU is preferred because it offers performance consistency that natural leather cannot match. Unlike leather, PU maintains its weight and shape in wet conditions, provides superior resistance to abrasion, and can be manufactured to precise specifications required for aerodynamic design.

RFID technology is used primarily in inventory management and anti-counterfeiting measures. Tags can be embedded into balls to track their authenticity, logistics movements through the supply chain, and retail stock levels, enhancing efficiency and protecting intellectual property.

Investment in youth soccer programs creates a stable, growing foundational demand for balls in sizes 3, 4, and 5. It ensures a continuous pipeline of participants who require age-appropriate equipment and establishes brand loyalty early in the consumer life cycle.

The primary motivation is to enhance the player's control and grip on the ball, especially in wet conditions, and to optimize the aerodynamic flow of air over the surface to achieve highly predictable, straight flight paths, satisfying both competitive and professional performance expectations.

The competitive landscape, dominated by a few giants like Adidas and Nike, leads to differentiated pricing strategies. Premium pricing is applied to officially sponsored match balls, while fierce price competition exists in the mid-range and recreational segments, often requiring promotional sales and high-volume output.

Asia Pacific benefits from highly developed manufacturing capabilities (especially in countries like Pakistan and China) offering cost-effective production for global brands. Simultaneously, massive population growth and rising incomes within the region fuel local consumption, making it dual-centric for both supply and demand.

Impact Forces refer to the collective influence and magnitude of the identified Drivers, Restraints, and Opportunities (DRO) on the market's trajectory, valuation, and competitive structure. They summarize the net effect of these external and internal pressures on growth prospects.

The market is gradually phasing out PVC in higher-end products due to environmental concerns and inferior performance compared to PU. Manufacturers are transitioning towards more advanced, eco-friendlier, and higher-performing synthetic leather composites and bio-based plastics where feasible.

The main logistical challenge is managing seasonal demand spikes and geographic disparities. High demand during tournament cycles requires swift scaling of distribution, while managing the efficient, cost-effective transport of bulky, relatively low-density inflatable goods globally remains a core complexity.

An indirect distribution channel, relying on wholesalers and large retailers, offers manufacturers the advantage of immediate, broad market penetration and reduced operational complexity by offloading storage, localized marketing, and regional retail sales management to established third parties.

Technological advancements, such as thermal bonding and specialized material compositions required for FIFA certification, substantially increase the cost of production and justify higher ASPs for premium match balls, driving overall revenue growth in the high-performance segment.

Machine stitching holds a moderate role, positioning itself between low-cost hand-stitched balls (often lower quality) and high-end thermal-bonded balls. It is typically used for intermediate-grade training and club match balls, offering a balance of durability, consistency, and moderate cost.

The individual recreational user and organized youth/amateur league segments are the most crucial for volumetric sales. They represent the largest number of consumers and require high volumes of replacement and training balls throughout the year.

Key players are strategically moving toward diversified and secured sourcing of specialized PU materials, often investing in collaborative development with chemical companies to ensure proprietary material formulations that offer a competitive edge in performance and sustainability.

The primary distinction lies in internal construction and material quality: the match ball uses superior, multi-layered PU and thermal bonding for optimal feel and aerodynamics, while the training ball uses more durable, often machine-stitched panels and heavier synthetic material for longevity and resistance to wear.

The increasing internet penetration presents the opportunity to expand e-commerce sales, directly reach consumers in remote locations, and utilize data analytics from online interactions to precisely forecast demand and tailor marketing efforts globally.

Consistency in weight and circumference is critical because minute variations can drastically alter the ball's flight characteristics and trajectory, affecting the precision required by professional athletes. FIFA standards mandate extremely tight tolerances for competitive fairness and performance reliability.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.