ID : MRU_ 434025 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

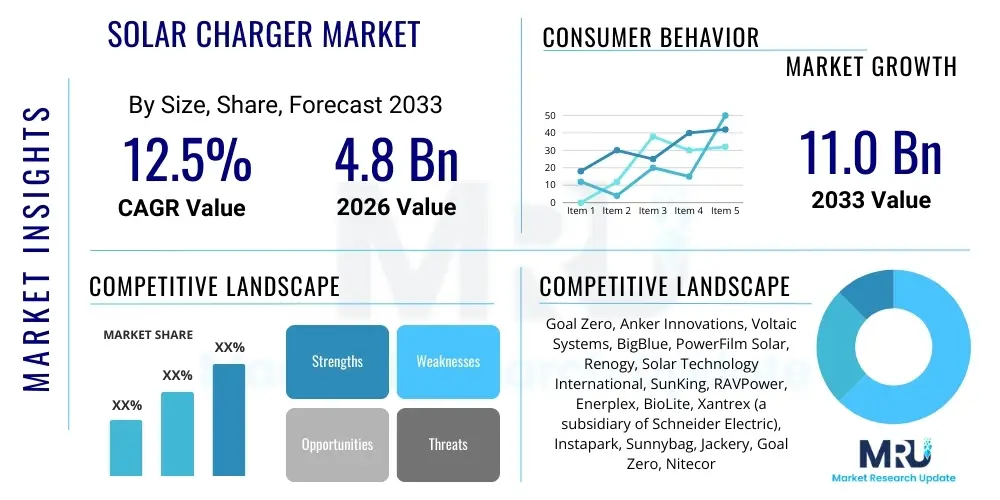

The Solar Charger Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at USD 4.8 Billion in 2026 and is projected to reach USD 11.0 Billion by the end of the forecast period in 2033.

The Solar Charger Market encompasses devices that convert solar energy into electrical power, primarily utilized for charging portable electronic devices such as smartphones, tablets, laptops, and specialized off-grid equipment. These products range from small, highly portable folding panels for consumer use to rugged, integrated solutions designed for military, emergency response, and remote industrial applications. The core product incorporates photovoltaic (PV) cells, a charge controller (often utilizing Maximum Power Point Tracking, or MPPT, technology), and sometimes an integrated battery storage unit, enabling power conversion and efficient energy delivery regardless of grid access.

Major applications for solar chargers are concentrated in the consumer electronics sector, supporting outdoor enthusiasts, travelers, and individuals residing in areas with unreliable electricity infrastructure. Furthermore, industrial applications include powering remote sensors, monitoring equipment, and providing backup power for critical communication devices. The primary benefits driving adoption include energy independence, environmental sustainability through reduced reliance on fossil fuels, and enhanced portability, ensuring users maintain connectivity during emergencies or extended off-grid expeditions. This focus on decentralized power generation aligns with global sustainable development goals and the increasing demand for resilient charging solutions.

Key driving factors accelerating market expansion involve the exponential growth in global smartphone and IoT device penetration, coupled with the decreasing manufacturing costs of photovoltaic materials, particularly high-efficiency crystalline silicon and thin-film cells. Government initiatives promoting renewable energy infrastructure, alongside increasing consumer awareness regarding sustainable practices, further solidify the market's growth trajectory. Technological advancements in flexible solar panels, coupled with improvements in battery storage capacity (lithium-ion and solid-state), are continuously enhancing the performance and practicality of solar charging solutions, making them a viable alternative to traditional power banks.

The Solar Charger Market is poised for substantial expansion, driven fundamentally by robust business trends emphasizing portability, efficiency, and integration with smart energy management systems. Key business trends include aggressive vertical integration by established electronics manufacturers seeking to control the entire supply chain from PV cell fabrication to final product assembly, alongside intense focus on developing aesthetically pleasing and lightweight designs that appeal to the mass consumer market. Strategic collaborations between solar technology providers and major smartphone accessory brands are crucial for expanding retail reach and standardizing charging interfaces, particularly around USB-C Power Delivery standards. Furthermore, the market sees a continuous shift towards bundled solutions that include high-capacity integrated power banks, addressing the need for charging during low light conditions.

Regionally, the Asia Pacific (APAC) dominates the market due to its large population base, high penetration of mobile devices, and significant presence of manufacturing hubs, particularly in China and Southeast Asia, driving both production and consumption. North America and Europe exhibit high growth rates, primarily driven by strong consumer interest in outdoor recreational activities (glamping, hiking) and stringent environmental regulations promoting sustainable consumer goods. Emerging economies in Latin America and the Middle East & Africa (MEA) present significant opportunities, characterized by large underserved populations lacking reliable grid access, making off-grid charging solutions essential for basic communication and lighting needs. Market maturity varies significantly, with developed regions focusing on high-efficiency, premium products, while developing regions prioritize cost-effective, high-durability solutions.

Segmentation trends highlight the increasing dominance of portable solar chargers, particularly those utilizing thin-film and flexible technologies, due to their superior size-to-power output ratio. By capacity, models featuring higher wattage output (20W+) are gaining traction as users seek to charge larger devices, such as laptops and drones. The end-user analysis reveals strong demand from the consumer segment, followed closely by the defense and government sectors, which require reliable, field-deployable power sources. Innovations in Maximum Power Point Tracking (MPPT) controllers are a critical technology trend, optimizing energy harvest from fluctuating solar irradiance levels, thereby enhancing the overall value proposition of high-end solar charging devices across all major segments.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Solar Charger Market predominantly focus on how AI can optimize energy management, predict power needs, and enhance device longevity. Users are concerned with whether AI algorithms can improve the efficiency of Maximum Power Point Tracking (MPPT) under rapidly changing weather conditions, thereby maximizing usable energy harvest. Key themes also center on the potential for AI to personalize charging profiles based on device usage patterns and historical solar irradiance data, ensuring critical devices maintain charge levels. Furthermore, consumers anticipate AI integration to improve fault detection, predict maintenance needs, and intelligently balance solar input with integrated battery discharge, thereby extending the lifespan of the entire charging system and simplifying the user experience through automated energy decisions.

The Solar Charger Market’s trajectory is heavily influenced by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO). Major drivers include the increasing global adoption of portable electronics and the burgeoning outdoor recreation industry, both of which necessitate reliable, off-grid power solutions. Furthermore, the imperative for sustainable energy solutions and the rapid decline in the cost of photovoltaic materials are making solar chargers more economically viable for mass consumer segments. The market is also propelled by government and non-governmental organization (NGO) initiatives aimed at electrifying remote areas where grid expansion is costly or impractical, often relying on solar charging systems for basic necessities and communication.

Conversely, significant restraints hinder growth, predominantly the intermittency and variability of solar irradiance, which directly impacts the charging speed and reliability of these devices. Consumer perception issues regarding the current speed limitations compared to wall charging, particularly for high-capacity devices, remain a challenge. Furthermore, the overall efficiency of energy conversion and storage, though improving, still presents a bottleneck, as does the competitive pressure from traditional, high-density battery banks that offer immediate power availability without relying on daylight. Regulatory complexities concerning the disposal of lithium-ion batteries integrated into many solar charging systems also pose environmental and logistical hurdles for manufacturers.

Opportunities for market growth are abundant, centered on integrating solar chargers with advanced connectivity features, such as Bluetooth and Wi-Fi, enabling remote monitoring and smart energy management. The development of high-efficiency perovskite solar cells and flexible organic PV technology promises lighter, more durable, and aesthetically superior products, opening doors to integration into clothing, backpacks, and urban infrastructure. The expansion of niche applications, including military reconnaissance, disaster relief kits, and IoT device powering in remote industrial settings, represents high-value growth segments. The primary impact force driving the market is the substitution threat from traditional grid power and large battery banks, compelling manufacturers to continually innovate in terms of efficiency, portability, and price point to maintain a competitive advantage in decentralized power generation.

The Solar Charger Market is segmented based on device type, panel technology, wattage, and end-use application, providing a granular view of market dynamics and targeted consumer needs. Device segmentation differentiates between portable solar chargers (designed for consumer electronics and ease of transport), solar charging stations (larger, fixed or semi-fixed systems for camps or group charging), and solar backpacks (integrated solutions blending portability with storage). Panel technology segmentation is crucial, distinguishing highly efficient crystalline silicon (polycrystalline and monocrystalline) from lightweight thin-film technologies (amorphous silicon, CIGS), each catering to different performance and portability requirements. Wattage categories, ranging from low-power 1–5W units to high-power 20W+ units, reflect the capability to charge various classes of electronic devices, from basic phones to power-intensive laptops and specialized drone batteries.

The end-use application segment separates the extensive Consumer Electronics sector, which includes outdoor enthusiasts, hikers, and general travelers, from the highly specialized and demanding Military and Defense sector, which requires extremely rugged and reliable power sources. Other significant segments include Emergency & Disaster Relief, where rapid deployment and dependable power are critical, and Industrial/Remote Monitoring, focusing on powering sensors and communication equipment in isolated locations. This segmentation analysis is vital for stakeholders to allocate resources effectively, targeting segments where product specifications, such as weatherproofing, shock resistance, and certified efficiency, provide the greatest competitive differentiation and return on investment.

Further analysis within the consumer segment shows increasing preference for highly foldable and durable materials, emphasizing ruggedness for outdoor applications. Technological advancements are steadily pushing the boundaries of what is considered 'portable,' with higher wattage chargers becoming increasingly compact. The market also observes a geographical preference for specific segment types: regions with high solar intensity favor high-wattage, dedicated panels, while urban markets show greater uptake of integrated solar backpacks and smaller emergency chargers. Understanding these nuanced preferences allows manufacturers to optimize product portfolios for specific demographic and environmental conditions, driving market saturation across diverse socioeconomic strata.

The value chain for the Solar Charger Market begins with upstream analysis, which is dominated by the sourcing and refinement of raw materials, primarily silicon (for crystalline cells) and specialized materials like copper, indium, gallium, and selenium (CIGS) for thin-film technologies. This phase also includes the manufacturing of essential electronic components, particularly the specialized microcontrollers and semiconductors used in the Maximum Power Point Tracking (MPPT) charge controllers and integrated battery management systems (BMS). Key upstream players are semiconductor manufacturers and specialized PV material suppliers, whose pricing strategies and technological innovations directly influence the final product cost and efficiency. Ensuring a robust supply of high-grade, cost-effective photovoltaic materials remains a critical challenge and a point of competitive differentiation within the upstream segment.

The core manufacturing and assembly stage constitutes the midstream analysis, where PV cells are laminated, wired, and integrated with the charge controller and battery components into the final charger housing. This stage demands high precision manufacturing, focused heavily on minimizing energy loss during conversion and ensuring durability, especially for ruggedized models. Downstream analysis focuses on the distribution channels, which are characterized by a highly fragmented yet rapidly consolidating landscape. Direct channels, such as manufacturer-owned e-commerce platforms and specialized B2B contracts (especially with military or industrial buyers), provide greater margin control. Indirect channels include major consumer electronics retailers, outdoor specialty stores (e.g., REI, camping supply stores), online marketplaces (Amazon, eBay), and specialized distributors targeting off-grid markets in developing regions. The efficiency of the downstream network, particularly in managing inventory and responding to seasonal demand peaks (e.g., summer travel), is vital for market penetration.

Direct distribution, favored by premium brands, allows for better brand control and immediate feedback loops regarding product performance and user satisfaction, which is highly valuable in the rapidly evolving consumer electronics space. Indirect distribution, leveraging major e-commerce platforms, provides unparalleled global reach and scalability, though it often involves significant price competition and requires robust anti-counterfeiting measures. The post-sales phase, including warranty service, recycling initiatives, and customer support, also forms a critical part of the value chain, particularly as consumers prioritize sustainability and long-term product reliability. Innovations in packaging and logistics, aimed at reducing the environmental footprint of product delivery, are increasingly influencing consumer choice, further emphasizing the need for comprehensive value chain optimization from raw material to end-of-life management.

The Solar Charger Market serves a diverse array of potential customers, segmented primarily by their reliance on portable, off-grid power solutions and their intended usage environment. The largest segment remains the general consumer market, comprising travelers, students, daily commuters, and homeowners seeking backup power. Within this segment, a critical sub-group is the outdoor recreation community—hikers, campers, backpackers, and drone enthusiasts—who require lightweight, durable, and reliable charging solutions to sustain their connectivity and operational needs in remote settings. These customers prioritize high portability, water resistance (IP ratings), and a favorable power-to-weight ratio, demanding high-efficiency monocrystalline panels and integrated protective cases to withstand challenging environments.

Another major segment encompasses organizations requiring robust, mission-critical power: the Military and Defense sectors, and governmental/non-governmental organizations involved in Emergency and Disaster Relief operations. These institutional buyers are end-users who necessitate extreme durability, specialized low-emissivity finishes (to avoid detection), high operational reliability under extreme temperature variance, and compatibility with specialized military communication equipment. Purchases in this segment are typically large-volume B2G contracts, focusing less on cost sensitivity and more on adherence to stringent performance specifications and long-term supply chain resilience, often demanding customized output voltage profiles.

Finally, the Industrial and Commercial segment represents a high-growth area, driven by the proliferation of remote monitoring systems, IoT sensors, and surveillance cameras deployed in areas without conventional grid infrastructure, such as pipelines, remote agricultural fields, and construction sites. These customers, often utility companies, oil and gas operators, or agricultural technology firms, seek fixed or semi-portable solar charging systems that offer continuous, low-maintenance power delivery for long durations. The buying decision here is centered on total cost of ownership (TCO), longevity, resistance to environmental contaminants (dust, corrosion), and seamless integration with existing telemetry and data collection infrastructure, making specialized industrial-grade solar charging stations their primary purchase requirement.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 11.0 Billion |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Goal Zero, Anker Innovations, Voltaic Systems, BigBlue, PowerFilm Solar, Renogy, Solar Technology International, SunKing, RAVPower, Enerplex, BioLite, Xantrex (a subsidiary of Schneider Electric), Instapark, Sunnybag, Jackery, Goal Zero, Nitecore, SolaReady, EcoFlow, Xiaomi |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Solar Charger Market is defined by continuous innovation across three main domains: photovoltaic materials, power management electronics, and integrated storage solutions. Advancements in photovoltaic materials are critical, with the ongoing development of highly efficient monocrystalline silicon cells maximizing power output in compact footprints. However, the rapidly emerging use of flexible and lightweight materials, such as Copper Indium Gallium Selenide (CIGS) and various Organic Photovoltaics (OPV) and Perovskite cells, is fundamentally changing product design, enabling solar charging to be seamlessly integrated into fabric, curved surfaces, and highly portable recreational gear, enhancing durability and reducing weight significantly compared to traditional rigid panels.

The crucial technology ensuring efficient operation is the Maximum Power Point Tracking (MPPT) controller. Modern solar chargers incorporate sophisticated digital MPPT algorithms, often utilizing microcontrollers to continuously adjust the electrical load to extract the maximum possible power from the solar panel under fluctuating irradiance, temperature, and partial shading conditions. This is essential for maximizing charging speed and minimizing energy waste. Furthermore, integrating smart battery management systems (BMS), often paired with the MPPT controller, allows for optimal charging and discharging of integrated lithium-ion or lithium-polymer batteries, protecting them from overcharge, over-discharge, and temperature extremes, thereby significantly extending the overall product life cycle and improving user safety.

Connectivity and smart functionality represent a major technological shift. High-end solar chargers now feature USB Power Delivery (USB-PD) standards, enabling fast charging for modern laptops and high-draw devices. Additionally, built-in communication protocols (like Bluetooth or specialized APIs) allow users to monitor real-time power output, battery status, and historical energy harvest data via dedicated mobile applications. Future technological evolution is expected to focus on further integrating AI/ML capabilities into MPPT and BMS systems for predictive performance optimization, alongside continued development of solid-state battery technology to provide safer, lighter, and higher-density integrated energy storage, addressing the long-standing consumer need for reliable power regardless of weather conditions.

Regional dynamics play a crucial role in shaping the demand, technology adoption, and competitive landscape of the Solar Charger Market, reflecting diverse economic conditions, climate patterns, and consumer behaviors globally.

The most critical factor is the efficiency of the photovoltaic (PV) cells themselves, typically measured as the percentage of sunlight converted into electricity. High-efficiency monocrystalline silicon cells, combined with sophisticated Maximum Power Point Tracking (MPPT) technology, are essential for maximizing energy yield, especially under suboptimal or intermittent solar conditions, ensuring faster charging times.

Flexible solar chargers, utilizing thin-film technologies like CIGS or amorphous silicon, offer superior portability, lighter weight, and greater durability against bending and shock compared to glass-covered rigid crystalline panels. While rigid monocrystalline panels often achieve higher peak efficiency per square meter, flexible panels are preferred for integration into backpacks, clothing, and curved surfaces, offering resilience and convenience for mobile users.

The wattage requirement is defined by the device being charged; a typical smartphone requires 5W–10W, while tablets often need 12W–18W. Modern laptops utilizing USB Power Delivery (USB-PD) can require 20W to 60W or more. Users seeking to charge multiple devices or laptops should prioritize high-wattage (20W+) solar chargers equipped with efficient charge controllers to handle the higher power demand effectively.

Yes, the Solar Charger Market is significantly benefiting from sustainable technology mandates and increasing global awareness of renewable energy. Governments and consumers worldwide are increasingly favoring decentralized power solutions and electronics that reduce reliance on grid electricity generated from fossil fuels, positioning solar chargers as a key component of the sustainable consumer electronics movement and disaster preparedness kits.

Integrated battery storage (power banks) is crucial, allowing the solar charger to accumulate energy throughout the day, ensuring power availability when sunlight is absent (e.g., at night or during cloudy periods). This integration converts the intermittent solar input into consistent, reliable power output, enhancing the overall utility and resilience of the solar charging solution for sustained off-grid operation.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.