ID : MRU_ 431975 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

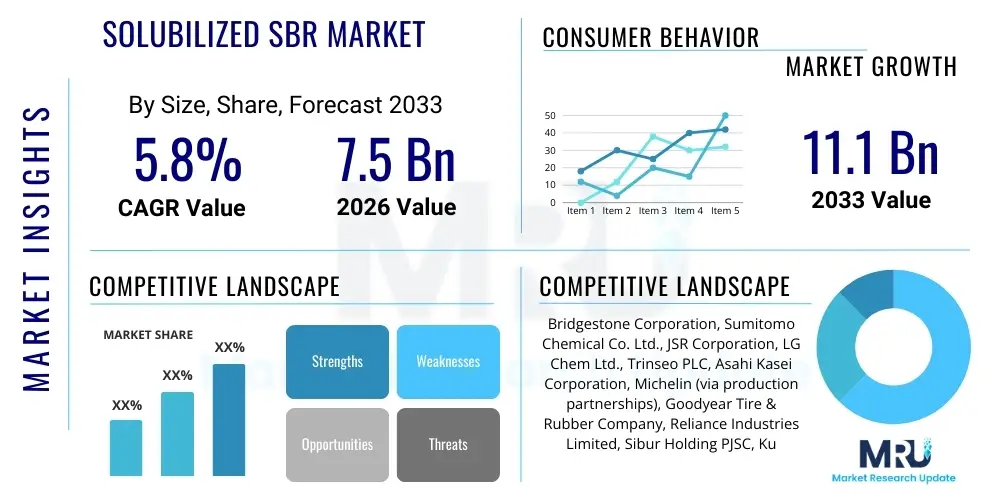

The Solubilized SBR Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 7.5 Billion in 2026 and is projected to reach USD 11.1 Billion by the end of the forecast period in 2033.

The Solubilized Styrene Butadiene Rubber (S-SBR) market is defined by the production and consumption of synthetic rubber characterized by its highly controlled microstructure, which is achieved through solution polymerization using organolithium initiators. Unlike conventional emulsion SBR (E-SBR), S-SBR offers superior properties, particularly reduced rolling resistance and enhanced wet grip, making it indispensable for manufacturing high-performance and fuel-efficient "green tires." The demand dynamics are intrinsically linked to stringent global automotive regulations aiming for lower CO2 emissions and improved vehicle safety standards, especially within the rapidly expanding electric vehicle (EV) sector, which requires specialized tires to handle higher torque and battery weight. The complexity of S-SBR synthesis and the requirement for highly specialized compounding expertise contribute to its premium positioning compared to traditional elastomers.

S-SBR is a cornerstone material within the automotive tire industry, accounting for the largest share of its application matrix. Its unique molecular architecture—including adjustable vinyl content and coupled chains—allows tire manufacturers to optimize the balance between wear resistance, fuel efficiency, and traction. Beyond tires, S-SBR finds critical applications in high-grade industrial rubber goods, footwear components, and modification of asphalt and plastics, where its enhanced tensile strength and elasticity are beneficial. The increasing focus on sustainability across manufacturing sectors further propels S-SBR adoption, particularly grades that facilitate the incorporation of bio-based fillers or recycled content, aligning production strategies with circular economy objectives. The inherent benefits of S-SBR, such as improved dispersion of silica fillers, cement its status as a vital component in modern material science.

Major driving factors include the mandatory implementation of tire labeling schemes in key economies like the EU, Japan, and South Korea, which directly correlate tire grades with energy efficiency and safety metrics. The rapid globalization of the automotive supply chain and the push towards replacing traditional, less efficient elastomers with S-SBR are central to market expansion. Furthermore, significant investments by major petrochemical and chemical companies in capacity expansion and technological improvements, focusing on advanced coupling agents and continuous process optimization, are bolstering supply capabilities. The shift in consumer preference toward premium vehicles and replacement tires that offer superior performance and longevity also acts as a robust market driver.

The Solubilized SBR market is experiencing robust growth driven primarily by structural shifts in the global automotive industry, particularly the proliferation of electric vehicles and increasingly strict environmental mandates regarding tire performance. Business trends highlight strategic consolidation among key producers aimed at securing raw material supply—butadiene and styrene—and optimizing logistics networks to cater efficiently to major tire manufacturing hubs in Asia Pacific and Europe. Technological advancements are concentrating on developing next-generation S-SBR grades optimized for extreme conditions and high silica loading, ensuring continued innovation remains a competitive differentiator. Furthermore, ESG (Environmental, Social, and Governance) pressures are compelling manufacturers to reduce the carbon footprint associated with polymerization processes and transition towards renewable energy sources, influencing capital expenditure decisions globally. The competitive landscape is characterized by a balance between global giants leveraging economies of scale and niche players specializing in highly customized elastomer formulations.

Regional trends indicate that the Asia Pacific (APAC) region, spearheaded by China, India, and Southeast Asia, remains the dominant consumption and production center due to its massive automotive manufacturing base and high demand for replacement tires. Europe and North America, while mature markets, exhibit strong demand for premium S-SBR grades driven by regulatory requirements (such as the EU Tire Labeling Regulation) and the rapid uptake of performance-focused EVs. Investment is accelerating in Eastern Europe and Southeast Asia as companies seek to diversify manufacturing risk and establish proximity to emerging automotive clusters. Latin America and the Middle East & Africa are demonstrating moderate growth, primarily driven by infrastructure development and increasing domestic vehicle production, although these regions are typically more price-sensitive and focused on standard S-SBR grades.

Segment trends underscore the dominance of the tire application segment, specifically passenger car tire manufacturing, where S-SBR is crucial for achieving mandated rolling resistance targets. Within product types, high-vinyl and coupled S-SBR grades are gaining prominence over standard grades, reflecting the industry's need for superior mechanical performance and enhanced wet traction. The rise of specialized off-road and heavy-duty vehicle tires also provides a niche growth avenue, although passenger vehicle applications remain the core market driver. The demand for bio-based or partially bio-derived S-SBR variants, while currently small, is expected to accelerate significantly as companies prioritize sustainable sourcing and attempt to decouple production costs from volatile petrochemical feedstocks.

Analysis of common user questions regarding AI's impact on the Solubilized SBR market reveals a focus on three primary themes: optimization of complex polymerization processes, acceleration of material discovery and formulation, and enhancing supply chain resilience through predictive analytics. Users frequently ask how AI can stabilize output quality despite feedstock variability and how machine learning (ML) models can predict the performance of novel S-SBR compounds without extensive, time-consuming physical testing. There is also significant user interest in leveraging AI for demand forecasting, particularly concerning the erratic growth patterns of the EV sector, which directly influences specialized S-SBR requirements. The consensus expectation is that AI will primarily serve as an optimization tool, reducing production waste, shortening R&D cycles, and providing manufacturers with a crucial competitive edge in efficiency and speed of innovation.

The Solubilized SBR market is shaped by a confluence of powerful drivers, structural restraints, promising opportunities, and inevitable market forces, creating a dynamic operational environment. Primary drivers include increasingly stringent governmental mandates worldwide concerning vehicle fuel efficiency and tire safety, particularly the widespread adoption of tire labeling regulations that necessitate the use of high-performance elastomers like S-SBR to achieve optimal A and B grade rankings. Furthermore, the exponential global growth in electric vehicle production significantly boosts demand, as EVs require specialized tires capable of handling higher instantaneous torque, resisting greater abrasive wear due and minimizing range loss through ultralow rolling resistance, properties where S-SBR excels compared to traditional E-SBR or natural rubber. The ongoing global trend toward premiumization in the automotive tire sector, where consumers prioritize longevity and safety, further sustains market expansion.

Conversely, the market faces significant restraints, principally high dependence on volatile petrochemical feedstocks, specifically butadiene and styrene monomers, which are highly susceptible to fluctuations in crude oil prices and global refinery output. This price instability introduces considerable risk into the manufacturing cost structure. Additionally, the complex solution polymerization process requires substantial capital investment and highly specialized technical expertise, creating significant barriers to entry for new competitors. There are also inherent technical challenges related to the compounding process, specifically ensuring the homogeneous dispersion of high levels of silica within the S-SBR matrix, a critical factor for achieving superior tire performance. Furthermore, the market faces growing competition from alternative materials, including emerging bio-based rubbers and highly advanced specialized polybutadienes, though S-SBR currently maintains a dominant technological position for green tires.

Opportunities for growth are abundant, focusing heavily on developing sustainable and bio-based S-SBR variants that utilize renewable resources, appealing to growing consumer and regulatory preference for eco-friendly materials. Significant potential exists in expanding non-tire applications, such as high-performance technical rubber products, seals, hoses, and premium footwear components, where the superior properties of S-SBR can justify its higher cost. The technological opportunity lies in refining functionalization and coupling technologies to further enhance the interaction between the S-SBR polymer chains and silica fillers, pushing the boundaries of the wet grip/rolling resistance trade-off curve. Market penetration in rapidly urbanizing economies across APAC and Latin America, driven by increasing vehicle ownership rates and improving road infrastructure, presents a considerable long-term commercial opportunity, supported by strategic collaborations with regional tire manufacturers.

The Solubilized SBR market segmentation provides crucial insight into the varying characteristics and growth trajectories across different product types, application areas, and geographical regions. The market is primarily segmented based on product type—which differentiates between oil-extended and non-oil-extended grades, and further by vinyl content and coupling structure—and by application, overwhelmingly dominated by the automotive tire industry. Understanding these segments is vital for producers to align their production capabilities with specific end-user requirements, especially concerning the highly technical demands of premium tire manufacturers. The increasing differentiation in S-SBR grades reflects the industry's need to navigate the stringent performance trade-offs (e.g., minimizing rolling resistance while maintaining wet grip) imposed by evolving regulatory frameworks and the dynamic technological demands of modern electric and high-performance vehicles.

Product segmentation hinges on the precise microstructure control achievable through solution polymerization. High-vinyl S-SBR, which typically exhibits superior wet grip, is increasingly preferred, often balanced with specialized low-vinyl grades for enhanced wear resistance. Non-oil-extended grades are critical for applications requiring maximum purity and mechanical integrity, while oil-extended grades offer cost-efficiency and improved processability, suitable for standard replacement tires. Application segmentation clearly highlights the dominance of passenger vehicle tires, which necessitate the most advanced S-SBR technology. Commercial vehicle tires, including light trucks and buses, constitute the second major segment, prioritizing durability and load-bearing capacity, although S-SBR adoption here is often blended with natural rubber and E-SBR.

The strategic importance of segmentation is also evident in regional variations. Developed markets in North America and Europe prioritize specialized, low-rolling-resistance grades (often high-coupling, non-oil-extended) to meet stringent regulatory standards, commanding higher prices. In contrast, emerging markets in Asia Pacific prioritize both high-performance green tires for new vehicle sales and more cost-effective, standard S-SBR formulations for the vast replacement market. This geographic differentiation forces manufacturers to manage a diversified product portfolio and localize production strategies to cater effectively to distinct demand profiles, encompassing raw material sourcing and technical service support across different jurisdictions.

The Solubilized SBR value chain is intricate, commencing with the highly centralized upstream extraction and processing of petrochemical feedstocks and culminating in the highly diversified downstream market of finished rubber goods. Upstream analysis focuses predominantly on the sourcing of critical monomers: butadiene and styrene. Butadiene is primarily a byproduct of steam cracking naphtha, while styrene is derived from benzene and ethylene. The supply of these monomers is largely controlled by global petrochemical giants, giving them substantial bargaining power and making the S-SBR market susceptible to volatility in the global oil and gas sector. Securing long-term, stable, and cost-effective feedstock supply is the primary strategic challenge in this stage, often necessitating vertical integration or long-term supply agreements between rubber producers and chemical refiners. Efficiency in polymerization, which transforms these monomers into S-SBR, relies heavily on continuous technological refinement to manage polymerization conditions precisely.

The manufacturing stage involves the complex solution polymerization process, requiring specialized reactors, proprietary catalyst systems, and sophisticated solvent recovery units. Here, intellectual property surrounding functionalization and coupling agents is highly valuable, serving as a key differentiator among major S-SBR producers. Once synthesized, the rubber is processed, dried, and baled. The distribution channel then plays a crucial role, moving the raw polymer from the production plant to the compounders and ultimately the tire manufacturers. Direct distribution, involving large-volume shipments negotiated directly between S-SBR producers (e.g., Trinseo, JSR, Michelin) and Tier 1 tire manufacturers (e.g., Bridgestone, Goodyear, Continental), accounts for the vast majority of volume. This direct model emphasizes technical support, just-in-time delivery, and personalized product specification.

Indirect distribution channels, utilizing specialized chemical distributors and agents, cater mainly to smaller industrial rubber goods manufacturers or regional compounding houses that require smaller, tailored volumes and localized inventory management. Downstream, the key players are the global tire manufacturers, who possess enormous market leverage due to the volume of S-SBR they consume. The final products, primarily green tires, reach the consumer through automotive OEMs (Original Equipment Manufacturers) or the vast, global replacement tire market via independent dealerships and repair centers. The efficiency of the entire chain is heavily contingent on optimizing logistics to minimize transportation costs of bulky rubber bales and ensuring the precise technical specification of the S-SBR aligns with the stringent performance requirements of the final rubber product application.

The primary and largest potential customers for Solubilized SBR are the global automotive tire manufacturing corporations, often categorized as Tier 1 and Tier 2 players. These companies, including Bridgestone, Michelin, Goodyear, Continental, and Pirelli, consume massive volumes of S-SBR for their lines of high-performance passenger and commercial vehicle tires, particularly those marketed as 'green' or fuel-efficient tires. The purchasing decisions of these tire majors are driven not merely by cost but fundamentally by technical specifications, consistent quality assurance, and the ability of S-SBR suppliers to innovate in conjunction with their own R&D cycles. Long-term partnerships, often involving joint development agreements for proprietary rubber grades, are common, solidifying the relationship between the polymer supplier and the key buyer.

Secondary but rapidly growing customer segments include specialized manufacturers of industrial rubber products and engineering elastomers. This group encompasses companies producing advanced conveyor belts, technical seals, industrial hoses, and high-performance damping components that require the superior elastic properties, heat aging resistance, and abrasion resistance offered by S-SBR. These buyers often require highly customized, lower-volume batches of specialized S-SBR grades, typically sourced through indirect distribution channels that provide specialized compounding services. Furthermore, manufacturers of high-end footwear, particularly athletic shoes and safety boots, constitute another significant customer base, leveraging S-SBR’s excellent durability and anti-slip characteristics for superior soling materials.

A third crucial customer group comprises compounding houses and polymer modification specialists. These entities purchase S-SBR to blend with other polymers (like natural rubber or EPDM) or incorporate it into asphalt modification projects, particularly for high-stress road paving applications where enhanced elasticity and resistance to fatigue cracking are required. For S-SBR producers, focusing on these diversified segments provides a vital strategic hedge against cyclical downturns in the automotive sector, ensuring broader market resilience. The trend towards sustainable material sourcing is increasingly making customers prioritize suppliers who can offer certified bio-based or recycled content S-SBR options, adding ESG compliance to the list of essential purchasing criteria.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 7.5 Billion |

| Market Forecast in 2033 | USD 11.1 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Bridgestone Corporation, Sumitomo Chemical Co. Ltd., JSR Corporation, LG Chem Ltd., Trinseo PLC, Asahi Kasei Corporation, Michelin (via production partnerships), Goodyear Tire & Rubber Company, Reliance Industries Limited, Sibur Holding PJSC, Kumho Petrochemical Co. Ltd., Lanxess AG, TSRC Corporation, Synthos S.A., Shandong Haomai Rubber Co., Versalis S.p.A., Shenyang Synthetic Rubber Research Institute, China National Petroleum Corporation (CNPC), ZEON Corporation, Nippon A&L Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Solubilized SBR market is highly dynamic, centered around refining the solution polymerization process to precisely control the polymer microstructure, thereby enhancing the functional properties of the final elastomer. A core technological focus involves the development of proprietary functionalization and coupling agents. These agents are chemical additives introduced during or immediately following polymerization that create a stronger chemical bond between the S-SBR polymer chain ends and the surface of reinforcing fillers, particularly precipitated silica. Effective coupling technologies, such as those utilizing functionalized lithium initiators or tin coupling, are critical because they drastically improve the dispersion of silica, leading directly to the superior balance of low rolling resistance and high wet grip required for A-grade green tires. Continuous investment in catalytic systems to improve reaction yield and selectivity is a constant technological pursuit among leading producers.

Another area of critical technological advancement is process optimization, moving towards more sustainable and efficient manufacturing paradigms. This includes the development of solvent-free or aqueous polymerization systems, aiming to reduce the reliance on hydrocarbon solvents (like hexane), minimize associated environmental impact, and lower operational costs related to solvent recovery and purification. Furthermore, the integration of advanced sensors, real-time analytics, and process control software (often leveraging AI/ML, as previously discussed) allows manufacturers to maintain stringent quality control and achieve highly consistent polymer properties across massive production scales. This process optimization is vital given the tight tolerances and high technical standards demanded by tire OEM customers, especially in the premium segment.

Emerging technologies focus on synthesizing bio-based monomers or using biomass-derived feedstocks (e.g., bio-butadiene) to reduce the polymer’s reliance on fossil fuels, aligning with global decarbonization efforts and consumer preferences for sustainable products. While still nascent, the ability to successfully polymerize these sustainable feedstocks without compromising the intricate microstructure integrity of S-SBR represents a significant future technological hurdle. Companies are also exploring advanced blending technologies and post-polymerization modification techniques to create bespoke multi-component elastomer blends that maximize specific performance attributes, potentially combining the strengths of S-SBR with natural rubber or EPDM for niche applications, thereby broadening the technical applicability and market reach of solubilized elastomers.

The APAC region holds the largest market share in terms of both consumption and production of Solubilized SBR, driven by its unparalleled scale in automotive manufacturing, particularly in China, India, and South Korea. China, as the world's largest vehicle market and a significant hub for both domestic and international tire manufacturers, is the powerhouse of regional demand. The region benefits from lower operating costs and proximity to feedstock supplies in the Middle East and Southeast Asia. The growth here is dual-faceted: meeting the soaring demand for original equipment tires (OE) for new vehicles, including a massive surge in locally produced EVs, and supplying the vast replacement tire market. Governmental initiatives promoting domestic production and the gradual implementation of stricter regional emission standards, similar to European frameworks, are forcing tire companies in APAC to transition rapidly towards S-SBR usage, ensuring continued high growth rates, albeit with strong price competition.

The competitive environment in APAC involves major global producers alongside strong regional players who are aggressively expanding capacity to meet localized demand. Japan and South Korea remain critical centers for technological innovation, focusing on the highest-grade S-SBR compounds for premium tires, often developed in close collaboration with domestic automotive giants. Capacity expansion efforts often involve significant government incentives, aiming to establish resilient and localized supply chains insulated from global trade volatility. The immense investment poured into new tire factories across emerging economies like Indonesia, Thailand, and Vietnam further cements APAC’s position as the primary engine for S-SBR market expansion through 2033.

Europe is a critical market for high-value S-SBR, driven primarily by the stringent EU Tire Labeling Regulation, which mandates performance standards for rolling resistance, wet grip, and noise. This regulatory environment necessitates the widespread use of advanced S-SBR grades to achieve A and B ratings, ensuring a high premium on specialized, functionalized elastomers. Demand is also strongly supported by Europe’s leading position in the electric vehicle transition. European automotive OEMs require custom-designed tires that can maximize EV range, leading to intense technological collaboration between S-SBR suppliers and leading European tire companies (e.g., Continental, Michelin).

The market in Europe is mature but characterized by high barriers to entry due to demanding quality standards and long-standing supplier relationships. Production within the region often focuses on non-oil-extended, specialized grades, though a significant portion of standard-grade S-SBR is imported from Asia. Sustainability and ESG factors hold particular importance here, prompting a strong regional focus on the development and adoption of bio-based S-SBR alternatives and manufacturing processes that minimize resource use. The stability of the replacement tire market, reflecting a large, affluent vehicle parc, provides a consistent, high-value revenue stream for S-SBR manufacturers.

North America demonstrates strong, steady demand for S-SBR, driven by increasing regulatory scrutiny (e.g., evolving CAFE standards in the U.S.) and the ongoing consumer preference for high-performance and large-format tires, particularly for SUVs, light trucks, and performance passenger vehicles. The high average mileage driven per vehicle in the U.S. necessitates durable, high-quality tires, where S-SBR’s wear characteristics provide a distinct advantage. The rapid expansion of electric truck and SUV platforms is accelerating the need for high-load, low-rolling-resistance S-SBR compounds capable of managing the significant weight of large battery packs.

Production capacity in North America is substantial but often supplemented by imports, particularly from competitive Asian sources. The market is defined by large-scale purchases by domestic tire manufacturers like Goodyear and Bridgestone (North American operations). Technological investment is focused on optimizing tire performance for diverse weather conditions and achieving durability necessary for extended warranties common in the region. Regulatory changes are continuously pushing the envelope on fuel efficiency, guaranteeing sustained market relevance for advanced S-SBR formulations.

These regions represent emerging growth corridors. LATAM, led by Brazil and Mexico, benefits from significant domestic automotive production and a growing replacement tire market linked to economic recovery and increased urbanization. Demand here is often more price-sensitive, balancing the need for safety (wet grip) with cost-efficiency, resulting in a healthy demand for both oil-extended and standard non-oil-extended S-SBR. The MEA region's growth is tied to large-scale infrastructure projects, urbanization in the Gulf countries, and increasing vehicle adoption in South Africa and North Africa. While S-SBR demand is smaller compared to global hubs, sustained investment in local tire manufacturing capacity in countries like Turkey and Saudi Arabia signals future opportunities, particularly for suppliers capable of navigating complex regional logistics and regulatory differences.

The primary advantage of S-SBR lies in its precisely controlled polymer microstructure, including narrow molecular weight distribution and functionalized chain ends. This allows S-SBR to interact far more effectively with silica fillers, enabling tire manufacturers to achieve the difficult balance of significantly lower rolling resistance (fuel efficiency) and superior wet grip (safety), which is challenging to replicate with E-SBR.

The EV sector is a major growth catalyst for high-performance S-SBR. EVs require specialized tires to minimize battery drain (necessitating ultra-low rolling resistance) and handle the higher instantaneous torque and increased overall vehicle weight (necessitating superior abrasion resistance and durability), properties that advanced, high-coupling S-SBR grades uniquely provide.

The Asia Pacific (APAC) region, driven primarily by China’s massive automotive manufacturing and replacement tire markets, dominates the global consumption volume of S-SBR. However, Europe and North America lead the demand for the most technologically advanced, high-value, low-rolling-resistance grades required by stringent regulatory standards.

The two key petrochemical feedstocks are Butadiene and Styrene monomers. The main supply challenge is the inherent price volatility of these monomers, which are derivatives of crude oil and naphtha cracking processes, leading to significant fluctuation in the cost of goods sold for S-SBR manufacturers.

Future S-SBR technology will focus on enhancing functionalization chemistry to maximize polymer-filler interaction, developing partially bio-based or sustainable S-SBR grades to meet ESG targets, and utilizing advanced digital tools (AI/ML) to optimize polymerization processes for reduced energy consumption and improved batch consistency.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.