ID : MRU_ 431949 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

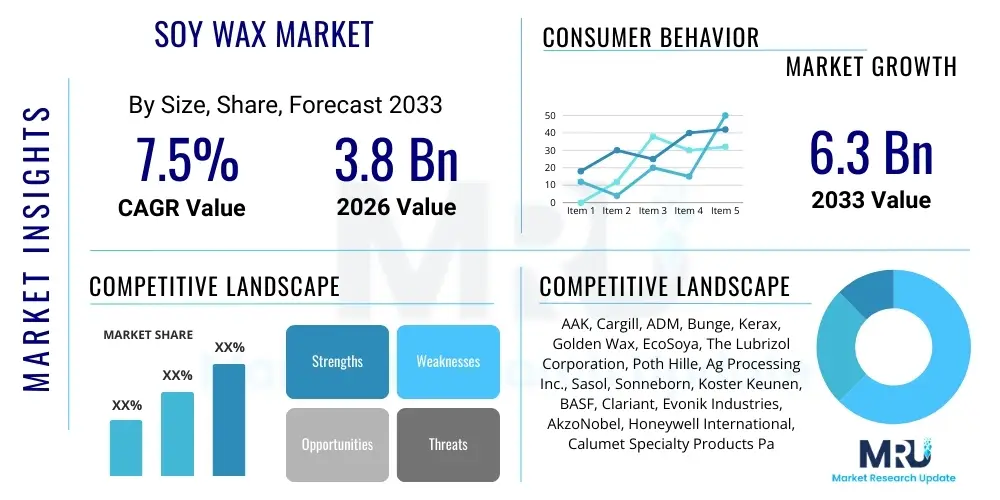

The Soy Wax Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2026 and 2033. The market is estimated at USD 3.8 Billion in 2026 and is projected to reach USD 6.3 Billion by the end of the forecast period in 2033.

The Soy Wax Market encompasses the production, distribution, and consumption of wax derived from soybean oil. This natural, renewable, and biodegradable product is primarily utilized as a base material for candle making, offering a cleaner, slower burn compared to traditional paraffin waxes. The market is characterized by increasing consumer preference for eco-friendly and sustainable products, driving demand across household and commercial sectors. Soy wax often comes in various forms, including pure soy wax and blended formulations, designed to meet specific application requirements such as improved scent throw or structural integrity in freestanding candles.

The primary product is a hydrogenated form of soybean oil, which is solidified and processed into flakes or pellets. Major applications span the home fragrance industry, cosmetics, and specialized industrial uses. In cosmetics, it serves as an emollient or stabilizing agent in lip balms, lotions, and massage candles. Key benefits driving market adoption include its non-toxic nature, excellent fragrance retention capacity, and the fact that it is a vegetable byproduct, appealing to vegan and environmentally conscious consumers. The low melting point of soy wax also makes it safer and easier to handle during manufacturing processes.

Driving factors for the market expansion include the exponential growth in the global home décor and aromatherapy industries, particularly post-pandemic, as consumers invest more in creating calming and pleasant indoor environments. Furthermore, stringent environmental regulations in North America and Europe concerning petrochemical derivatives, coupled with robust marketing emphasizing the sustainable origin of soy products, are cementing soy wax's position as a premium alternative to synthetic waxes. Technological advancements in hydrogenation and blending techniques are also enabling the creation of advanced soy wax formulas that overcome previous performance limitations.

The Soy Wax Market is poised for robust expansion, fundamentally driven by shifts in consumer behavior towards sustainability and natural ingredients, particularly within the candle and personal care segments. Business trends highlight strategic partnerships between large agricultural processors and specialized wax manufacturers to ensure stable sourcing and quality control. There is a noticeable trend towards premiumization, where niche brands emphasize the purity (100% natural) and ethical sourcing of their soy wax, commanding higher price points and driving market value growth. Furthermore, manufacturers are investing heavily in research and development to enhance the technical characteristics of soy wax, such as improving melt pools and increasing compatibility with complex fragrance oils, addressing previous performance gaps relative to paraffin.

Regional trends indicate North America and Europe as the dominant markets, primarily due to high environmental awareness, established cosmetic and home fragrance industries, and favorable regulatory frameworks promoting bio-based products. However, the Asia Pacific region, led by China and India, is emerging as the fastest-growing market segment. This accelerated growth is attributed to increasing disposable incomes, rapid urbanization, and the nascent adoption of Western lifestyle trends, including the use of scented candles and organic cosmetic products. Latin America and MEA are focused on developing domestic soybean processing capabilities to reduce import reliance, offering long-term growth opportunities in these regions.

Segmentation trends reveal that the candle application segment remains the largest revenue contributor, specifically container candles, favored for their ease of use and long burn times. Within product type, the blended soy wax segment holds a significant share, balancing cost-effectiveness and performance, although 100% natural soy wax is gaining momentum due to strong consumer demand for purity claims. The commercial end-user segment, encompassing hotels, restaurants, and retail spaces, is projected to show accelerated growth as these establishments increasingly adopt high-quality, non-toxic aromatic solutions to enhance customer experience and align with corporate sustainability goals.

User queries regarding AI’s influence on the Soy Wax Market primarily center on supply chain efficiency, predictive modeling for volatile raw material costs (soybean oil), and enhancing product development through computational chemistry. Consumers and industry stakeholders are keen to understand how AI can mitigate price fluctuations, a major restraint in this market, and optimize global logistics, particularly concerning shipping bulk raw materials and finished products across continents. Another prominent theme revolves around AI-driven customization; users ask if machine learning can predict regional scent preferences or suggest optimal wax blends based on specific temperature and humidity profiles of target markets, thereby reducing R&D cycles and enhancing market responsiveness.

Furthermore, significant user interest focuses on AI’s role in automating and optimizing the manufacturing processes, specifically the hydrogenation and refining stages of soy wax production. Stakeholders are exploring AI-powered vision systems for quality control, detecting minor impurities or inconsistencies in wax color and texture before packaging. The application of generative AI in marketing and consumer engagement—creating hyper-personalized scent recommendations or optimizing e-commerce interfaces for candle and cosmetic sales—is also a highly discussed topic, indicating a shift towards intelligent consumer interaction and demand forecasting for seasonal products.

The adoption of AI and machine learning tools is expected to revolutionize production forecasting and demand planning within the Soy Wax ecosystem. By integrating real-time agricultural data, commodity market indices, and consumption patterns, AI algorithms can provide highly accurate predictions, allowing manufacturers to optimize inventory levels and hedge against soybean oil price volatility. This predictive capability translates directly into improved operational margins and enhanced competitiveness. For the consumer-facing sector, AI-driven data analytics offer unparalleled insights into scent profiles and aesthetic preferences, leading to faster product innovation cycles and highly targeted marketing campaigns, ultimately enhancing consumer satisfaction and driving market penetration.

The Soy Wax Market dynamics are shaped by a complex interplay of growth drivers and persistent challenges. A primary driver is the accelerating consumer shift towards sustainability, demanding natural, non-toxic, and renewable ingredients, especially in the home and personal care categories. This ethical purchasing behavior provides a significant structural advantage to soy wax over synthetic alternatives like paraffin. Coupled with this is the robust expansion of the global aromatherapy and wellness industry, where soy wax is favored for its clean burn and superior scent throw characteristics, particularly for expensive essential oils. However, this growth is significantly constrained by the inherent volatility in the price of raw soybean oil, which is linked directly to agricultural yields, geopolitical factors affecting trade, and energy costs, creating unpredictable manufacturing expenses and hindering stable long-term pricing strategies.

Opportunities in the market center on diversification beyond the traditional candle sector. There is significant untapped potential in the industrial lubricants and specialized coating sectors, where the biodegradability and low environmental impact of soy wax offer solutions to replacing mineral oil-based products in sensitive environments. Furthermore, continuous innovation in blending technology allows manufacturers to overcome inherent limitations, such as frosting or poor hot throw, creating high-performance soy-paraffin and soy-coconut blends that offer the best of both worlds—sustainability combined with technical stability. These opportunities rely on continued research into modifying the crystalline structure of the wax to expand its functional applicability across various temperature ranges and curing times.

The market is also influenced by critical impact forces, which determine the bargaining power and competitive intensity. The bargaining power of suppliers is moderate to high, as the primary raw material (soybean oil) is a globally traded commodity dominated by a few large agricultural conglomerates (e.g., ADM, Cargill, Bunge), meaning input costs are highly sensitive to market concentration and global supply dynamics. Conversely, the bargaining power of buyers is increasing, driven by the proliferation of small and medium-sized candle and cosmetic brands that demand high-quality, certified soy wax at competitive prices, leading to strong price competition among wax processors. The threat of substitutes, primarily paraffin wax (low cost) and beeswax (premium natural alternative), remains significant, compelling soy wax manufacturers to continuously justify their value proposition based on sustainability and performance characteristics. Regulatory landscapes, particularly around GMO labeling and environmental certifications, act as potent external forces affecting market access and consumer trust.

The Soy Wax Market is structurally segmented based on product type, application, and end-user, providing a multifaceted view of market dynamics and targeted growth areas. The segmentation analysis reveals the concentration of value in the consumer-facing industries, specifically home fragrance and cosmetics, while simultaneously highlighting the potential for industrial expansion. Understanding these segments is crucial for manufacturers developing targeted product lines, such as specialized wax blends for specific candle container sizes or high-purity, certified organic wax for premium cosmetic formulations. Geographical segmentation remains paramount, defining specific regulatory and cultural preferences that impact purchasing decisions and market entry strategies across different regions.

The analysis shows that product innovation often occurs at the intersection of segment requirements; for instance, developing low-shrinkage soy wax tailored for pillar candles (application) that also meets the stringent non-GMO certification (type) demanded by high-end household end-users. This integrated approach allows companies to differentiate themselves in a competitive landscape. The market growth rate differs substantially across applications; while the established candle segment offers stable demand, the cosmetics and food-grade wax segments exhibit higher CAGRs driven by newer product introductions and expanding regulatory acceptance of soy-derived ingredients in these sensitive areas, indicating future investment hotspots.

The Soy Wax value chain begins with the upstream segment involving soybean cultivation and harvesting, primarily concentrated in major agricultural regions such as the US, Brazil, and Argentina. This stage is followed by the crushing and refining of soybeans to extract crude and refined soybean oil. The specialized step occurs when refined soybean oil undergoes catalytic hydrogenation, transforming the liquid oil into solid, usable soy wax. Upstream suppliers, dominated by major agricultural processors, exert significant influence due to their control over raw material quality and pricing, necessitating stable long-term supply agreements for wax manufacturers.

The midstream segment comprises the core manufacturing processes: hydrogenation, purification, blending, and crystallization, carried out by specialized wax producers (e.g., AAK, Golden Wax, Kerax). These companies add value by ensuring the wax meets specific technical parameters (melting point, oil content, color) required by diverse applications. Distribution channels for soy wax are multifaceted. Direct distribution is common for large-volume industrial buyers, where manufacturers ship directly to major candle or cosmetic brands. Indirect distribution involves specialized chemical and ingredient distributors who handle smaller quantities, providing logistics support and technical advice to SMEs and hobbyist buyers, particularly important in fragmented markets.

The downstream segment includes the end-product manufacturers (candle makers, cosmetic formulators, industrial compounders) who integrate soy wax into their final offerings. The value chain concludes with retail and consumer channels. For candles, this includes mass market retail, specialized boutique stores, and a rapidly expanding e-commerce sector. The growth of direct-to-consumer (DTC) models by craft candle makers has significantly shortened the distance between the soy wax manufacturer and the ultimate consumer, placing greater pressure on manufacturers to ensure ingredient transparency and ethical sourcing claims, thereby integrating sustainability metrics throughout the entire value chain.

The primary potential customers and end-users of the Soy Wax Market are highly diversified, spanning from large multinational consumer goods corporations to micro-businesses specializing in artisan products. The largest volume buyers are established candle manufacturing companies, globally recognized for home fragrance products, demanding consistent quality and large-scale bulk supply for automated production lines. These buyers prioritize cost efficiency, stable supply, and adherence to specific regulatory standards regarding burn time and emissions. A secondary, but rapidly growing, customer base consists of natural and organic cosmetics brands that utilize soy wax as an effective, plant-based alternative to petrochemical waxes in their lotions, balms, and makeup formulations, focusing heavily on sustainability certifications and non-GMO claims.

Beyond the consumer sphere, industrial compounders and lubricant manufacturers represent key high-value potential customers. These industrial users leverage soy wax's unique physical properties—such as its capacity to act as a release agent, binder, or low-toxicity lubricant—for specialized manufacturing processes. Furthermore, the burgeoning DIY and hobbyist market, empowered by e-commerce platforms, constitutes a significant fragmented segment of potential buyers. This segment, serviced primarily through distributors and online retailers, demands smaller quantities, diverse wax types (blends), and comprehensive educational resources on usage, creating specific marketing challenges and opportunities for packaging innovation.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.8 Billion |

| Market Forecast in 2033 | USD 6.3 Billion |

| Growth Rate | 7.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | AAK, Cargill, ADM, Bunge, Kerax, Golden Wax, EcoSoya, The Lubrizol Corporation, Poth Hille, Ag Processing Inc., Sasol, Sonneborn, Koster Keunen, BASF, Clariant, Evonik Industries, AkzoNobel, Honeywell International, Calumet Specialty Products Partners, IGI Wax. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Soy Wax Market is fundamentally centered on optimizing the chemical conversion and subsequent modification of soybean oil to enhance its functional characteristics. The core technology remains catalytic hydrogenation, where the liquid unsaturated fatty acids in soybean oil are converted into saturated fats, yielding a solid wax structure. Recent technological advancements focus heavily on process control, employing specialized nickel catalysts and optimized reactor designs to achieve precise degrees of hydrogenation. This precision is critical for controlling the resulting wax melting point, hardness, and crystalline structure, which directly impact the performance attributes required for specific end-applications, such as achieving a smooth, flawless melt pool in container candles or ensuring sufficient stiffness for freestanding pillar candles.

A crucial area of innovation involves blending and modification techniques to overcome the inherent limitations of pure soy wax, such as its propensity for "frosting" (crystallization) or having a weaker "hot scent throw" compared to paraffin. Technologies include fractionated crystallization and specialized additive incorporation. Fractionated crystallization involves separating different triglyceride components of the oil to isolate fractions that offer better thermal stability or superior scent dispersion. Additive technologies utilize plant-derived or food-grade stabilizers and enhancers to improve fragrance binding and surface adhesion without compromising the natural label claim, allowing soy wax blends to match or exceed the performance of synthetic alternatives in demanding applications.

Furthermore, technology is being deployed to enhance sustainability and traceability. Advanced analytical chemistry techniques, such as High-Performance Liquid Chromatography (HPLC) and Gas Chromatography (GC), are essential for quality assurance, verifying the purity and composition of soy wax, which is particularly important for non-GMO and organic certifications. Automation and digitalization within manufacturing facilities, increasingly incorporating IoT sensors and AI-driven monitoring, ensure consistent production parameters, minimizing waste and energy consumption during the refining and hydrogenation phases, thus reinforcing the market’s core value proposition of environmental responsibility and efficiency.

North America: Market Dominance and High Consumer Awareness

North America currently holds the largest market share for soy wax, primarily driven by the United States. This dominance is attributable to the region’s strong consumer preference for natural, domestically sourced, and sustainable products, coupled with a robust, established home fragrance and artisanal candle market. High disposable incomes enable consumers to afford premium, clean-burning soy candles over cheaper paraffin alternatives. Furthermore, North America benefits from a readily available, large-scale domestic supply of raw soybean oil, facilitating localized production and minimizing logistical costs. Regulatory initiatives promoting bio-based materials further solidify the market position, encouraging continuous product innovation in both the household and commercial end-user segments.

Europe: Stringent Regulations and Cosmetic Application Growth

Europe is characterized by highly stringent environmental and health regulations, which naturally favor the adoption of biodegradable and non-toxic soy wax. The European market, particularly in Germany, the UK, and France, exhibits a strong trend towards certified organic and vegan cosmetic products. Soy wax is increasingly utilized in natural cosmetic formulations, such as body butters and lip care, capitalizing on the high consumer trust placed in natural European beauty brands. While the candle market is mature, growth is fueled by premiumization and shifts away from petrochemical-derived ingredients in line with the EU's Green Deal objectives. Market penetration is closely linked to clear labeling and certified sustainability claims.

Asia Pacific (APAC): Fastest Growing Market Potential

The APAC region, specifically China, India, and Japan, represents the fastest-growing market for soy wax. This rapid expansion is spurred by increasing urbanization, rising disposable income, and the gradual Westernization of lifestyle trends, leading to higher adoption rates of scented candles and air care products in middle-class households. Although paraffin wax currently dominates due to its low cost, demand for premium, natural ingredients is accelerating, particularly in metropolitan centers. Manufacturers are establishing localized production facilities to meet this burgeoning demand, utilizing locally sourced soybean derivatives where possible. The cosmetics industry in South Korea and Japan provides a substantial avenue for high-purity soy wax adoption.

Latin America (LATAM): Focus on Domestic Production and Export

Latin America, particularly Brazil and Argentina, plays a critical role as the world's largest supplier of soybeans. While consumption of soy wax is still lower than in North America, the region’s market is rapidly developing, focusing on leveraging domestic raw material supply to create finished wax products for both local consumption and international export. The domestic market is gradually seeing an increase in sustainable product adoption, driven by local environmental campaigns and increasing awareness. The main strategy in LATAM involves integrating vertically, from soybean processing directly into wax production, aiming for cost leadership on a global scale.

Middle East and Africa (MEA): Niche Luxury and Industrial Application

The MEA region, while a smaller market, shows specific pockets of growth. In the Middle East, the demand is centered around the luxury segment, with high-end hotels, spas, and luxury retail utilizing premium soy-based candles for ambience, often tied to high-value real estate developments. In Africa, particularly South Africa, the growth trajectory is more focused on industrial applications and niche cosmetic manufacturing, where the push for locally manufactured, environmentally sustainable ingredients is gaining traction. Logistical challenges and fluctuating import costs remain key constraints, making local processing and strategic regional partnerships vital for expansion.

The primary factor driving the current growth of the Soy Wax Market is the accelerating consumer demand for sustainable, natural, and non-toxic ingredients in home and personal care products. Consumers are increasingly replacing traditional paraffin wax with soy wax due to its biodegradable nature, renewable sourcing, and cleaner burn characteristics, aligning with global environmental consciousness and wellness trends, making sustainability a core purchasing criterion across key regions like North America and Europe.

The volatility of soybean oil prices significantly impacts the profitability of soy wax manufacturers, as soybean oil constitutes the main raw material cost. Fluctuations driven by agricultural yield, weather conditions, and global commodity market speculation create unpredictable input costs. Manufacturers must employ sophisticated hedging strategies and optimized inventory management, often leveraging AI-driven predictive analytics, to mitigate these risks and maintain stable pricing margins, ensuring continuous supply while managing exposure to geopolitical and climatic variables affecting raw material availability.

Key technical challenges associated with 100% pure soy wax include its lower melting point, which can lead to rapid melting and potential structural instability (softness) in warmer climates. Furthermore, pure soy wax is susceptible to surface imperfections such as 'frosting' (a white crystalline coating) and may exhibit a comparatively weaker 'hot throw' (scent release intensity) than synthetic waxes. Manufacturers address these limitations through technological modifications like optimized blending with harder waxes (e.g., coconut or palm kernel derivatives) or specialized processing to improve its crystalline structure and fragrance binding capacity for enhanced consumer performance.

The Candle Application segment holds the largest market share in the Soy Wax Market, specifically container candles, due to high consumer adoption rates in residential settings and the commercial hospitality sector. This segment is expected to maintain its dominance throughout the forecast period, driven by sustained global interest in aromatherapy and home décor. While mature, its growth will be fueled by premiumization, where consumers trade up to larger, more aesthetically appealing soy wax candles featuring complex, high-quality fragrance profiles and certified natural ingredient claims, maintaining a steady, robust growth rate.

Asia Pacific (APAC) is strategically crucial as it is forecasted to be the fastest-growing regional market for soy wax. Its growth role is twofold: first, as an emerging consumer market driven by rising middle-class disposable income, leading to higher consumption of scented products; and second, as a potential manufacturing hub leveraging the region's agricultural resources and developing industrial infrastructure. Market strategies in APAC focus on localized product adaptations and addressing the cost-sensitivity of the market while emphasizing the luxury and health benefits of soy wax over cheaper, traditional waxes, paving the way for significant long-term market penetration.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.