ID : MRU_ 431626 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

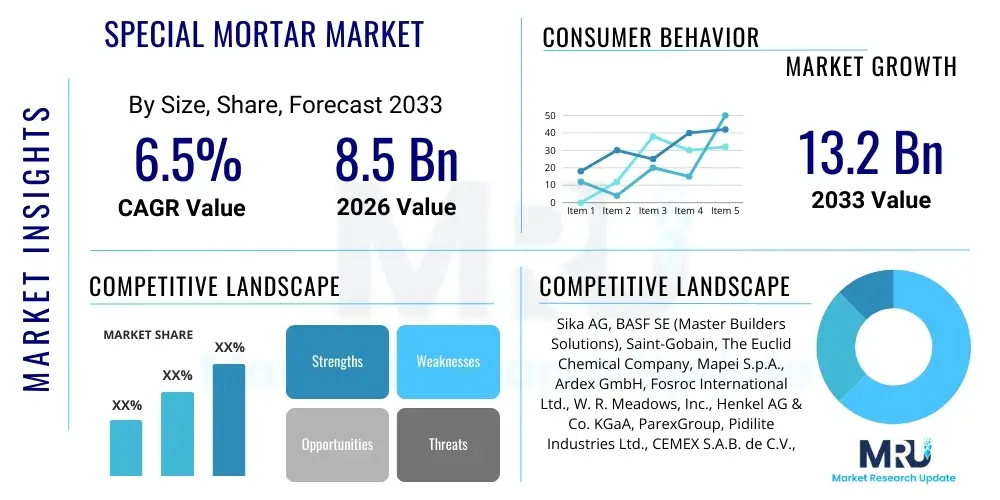

The Special Mortar Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at $8.5 Billion in 2026 and is projected to reach $13.2 Billion by the end of the forecast period in 2033.

The Special Mortar Market comprises high-performance, cement-based materials enhanced with specialty polymers, chemical admixtures, and meticulously graded aggregates to achieve tailored performance characteristics for demanding construction applications. These specialized formulations often include characteristics such as rapid setting times, high mechanical strength, superior bond strength, impermeability to water and corrosive agents, and enhanced durability under extreme conditions. Unlike traditional mortars, special mortars are engineered solutions designed to address specific challenges in construction, renovation, and repair, including structural rehabilitation, specialized tiling, precision grouting, thermal insulation, and fire protection. The demand is intrinsically linked to the longevity and sustainability goals of modern infrastructure projects worldwide, ensuring structures remain resilient against environmental degradation and heavy operational loads over prolonged periods.

Key product categories within this highly technical market segment include repair mortars, self-leveling mortars, tile adhesives and grouts, polymer-modified mortars, and decorative finishes. Repair mortars are particularly vital, utilized extensively in the remediation of concrete structures like bridges, tunnels, and high-rise buildings, where structural integrity has been compromised due to aging, corrosion, or mechanical damage. The shift towards polymer modification enhances flexibility and adhesion, making these materials indispensable in applications subject to movement or thermal stress. Furthermore, the specialized nature of these products requires rigorous quality control and precise mixing protocols, often supplied as pre-bagged dry mixes, which ensures consistent performance on site and minimizes application errors, thereby improving overall project quality and efficiency in complex construction environments globally.

Major applications driving market expansion involve rapid urbanization in developing economies, coupled with significant governmental investment in infrastructure maintenance and expansion in mature markets. The benefits derived from using special mortars—including reduced downtime for repairs, extended service life of structures, and adherence to stringent building codes—underscore their economic value proposition. Driving factors include the increasing complexity of architectural designs demanding versatile and aesthetic finishing materials, the growing trend of retrofitting and renovation of historical structures, and the escalating regulatory pressure to adopt environmentally compliant and high-durability construction materials that minimize lifecycle costs and environmental impact, thereby supporting the transition towards more resilient and sustainable building practices across the globe.

The global Special Mortar Market is witnessing robust expansion, driven primarily by accelerating infrastructure development, particularly in Asia Pacific, and the critical need for structural rehabilitation across aging assets in North America and Europe. Business trends indicate a strong focus on innovation, with manufacturers heavily investing in R&D to develop eco-friendly, low-VOC, and sustainable formulations, such as geopolymers and bio-based additives, catering to green building certifications and evolving environmental mandates. Furthermore, strategic mergers and acquisitions remain prevalent as global players seek to consolidate market share, expand their specialized product portfolios, and gain access to regional distribution networks. The competitive landscape is characterized by a mix of large multinational chemical companies and specialized regional producers, all vying for dominance in high-value application segments like waterproofing and structural repair. The transition towards digital construction methods, including the use of Building Information Modeling (BIM) and automated application equipment, is also influencing product design and delivery logistics.

Regional trends highlight the Asia Pacific (APAC) as the epicenter of growth, fueled by massive public spending on transportation networks, commercial complexes, and residential housing, particularly in rapidly urbanizing nations like China, India, and Southeast Asian countries. While APAC focuses on new construction, North America and Europe exhibit strong demand centered on maintenance, repair, and overhaul (MRO) activities. European trends emphasize sustainability and energy efficiency, propelling the demand for thermal insulation mortars and specialized façade systems. Meanwhile, the Middle East and Africa (MEA) market demonstrates significant growth, tied to large-scale mega-projects and the necessity for materials resistant to extreme heat and high salinity, driving the uptake of highly durable and chemically resistant special mortars. Regulatory divergence across these regions concerning safety and environmental standards dictates specific product customization and market entry strategies for international manufacturers.

Segmentation trends show that the repair mortar segment holds a dominant market share due to the global aging infrastructure problem and increased awareness regarding preventative maintenance protocols. However, the fastest growth is anticipated in specialized tile adhesives and grouts, correlating with the boom in aesthetic and luxury residential and commercial interior finishes. Technology-wise, dry-mix mortars are preferred for their ease of use, consistency, and reduced logistical complexity on construction sites compared to wet mixes. The application segment is heavily skewed towards the infrastructure sector (bridges, tunnels, marine structures) due to the demanding performance requirements in these critical assets, followed closely by the residential sector which values aesthetic flexibility and long-term durability provided by these specialized materials. Future growth is strongly tied to the integration of nanotechnology to further enhance material performance, particularly focusing on self-healing properties and extreme durability.

User queries regarding AI's influence on the Special Mortar Market predominantly revolve around three key themes: optimization of complex mortar formulations, predictive maintenance applications in construction, and streamlining supply chain logistics for specialized materials. Users are keen to understand how AI-driven simulation tools can rapidly test and refine new polymer-cement combinations, reducing R&D costs and accelerating time-to-market for novel products with specific performance traits (e.g., tailored fire resistance or self-cleaning capabilities). Another major concern is the application of machine learning for analyzing structural sensor data, allowing contractors and asset managers to predict precisely when and where specialized repair mortars are needed, transitioning from reactive to predictive maintenance strategies. Finally, users inquire about AI's role in optimizing the production process, managing raw material variability, and improving inventory accuracy for specialized, high-cost mortar components, ensuring timely delivery and minimizing waste across global construction projects.

The integration of Artificial Intelligence and Machine Learning (ML) is poised to fundamentally transform the manufacturing, testing, and application of special mortars. AI algorithms can process vast datasets related to material properties, climate conditions, and structural load behaviors, enabling the development of 'smart' mortars designed specifically for unique project parameters. This precision engineering reduces material over-specification and ensures optimal performance, leading to substantial cost savings and environmental benefits by minimizing material usage. Beyond formulation, AI significantly enhances quality control processes in manufacturing by using computer vision to inspect aggregate grading and mixer uniformity in real-time. This ensures that the high-quality standards expected of special mortars are consistently met across diverse production facilities, a critical factor given the sensitivity of these materials to minute variations in component ratios and mixing dynamics, thereby elevating the overall reliability of these essential construction products.

The Special Mortar Market dynamics are shaped by powerful Drivers, significant Restraints, vast Opportunities, and interconnected Impact Forces. The primary drivers include the escalating global focus on infrastructure durability and the burgeoning demand for high-performance materials in structural repair and restoration projects, especially concerning aging assets such like bridges and historical buildings. These drivers are bolstered by increasing urbanization rates globally, requiring rapid, durable, and aesthetic construction solutions, particularly in residential and commercial high-rise development. Conversely, the high cost of raw materials, especially specialty polymers and chemical additives, poses a significant restraint, making special mortars less viable for budget-constrained projects. Furthermore, the lack of standardization and variability in application techniques across different regions complicates market penetration and necessitates extensive technical support from manufacturers, which acts as a frictional force slowing universal adoption.

Opportunities for market growth are substantial, particularly through the development and commercialization of sustainable and green mortar technologies, such as carbon capture mortars and those incorporating recycled content. The increasing adoption of passive house standards and energy-efficient building codes in Europe and North America presents a vast opportunity for specialized insulating and thermal bridging mortars. Furthermore, penetrating emerging markets in Southeast Asia and Latin America, where construction safety and durability standards are rapidly converging with global norms, provides significant untapped potential. Innovation in rapid-setting and cold-weather application mortars also presents a vital opportunity to extend the construction season and reduce project timelines, offering a competitive advantage over conventional materials and catering to highly specific project requirements, particularly in regions prone to extreme climatic variations.

The impact forces within this market are multifold. Regulatory compliance pressure is a critical force, mandating the use of specific high-performance or environmentally friendly materials in public works. Technological innovation acts as a disruptive force, continually introducing superior formulations that raise performance benchmarks and necessitate rapid adaptation from competitors. Economic volatility, particularly fluctuations in crude oil prices (affecting polymer costs) and global shipping costs, directly impacts the profitability and pricing structure of special mortars. The skilled labor shortage in the construction industry also acts as an impact force, driving demand for easier-to-apply, pre-mixed, and self-consolidating mortars that require less specialized expertise, thereby influencing product design toward user-friendliness and application efficiency across diverse geographical labor markets.

The Special Mortar Market is meticulously segmented based on product type, composition, application, end-user industry, and geography, reflecting the highly diverse requirements of the construction sector. Product segmentation is crucial, differentiating between hydraulic mortars, polymer-modified mortars, and specialized repair systems, each tailored for distinct performance envelopes. Composition segmentation often focuses on the binder type, distinguishing between cementitious, gypsum-based, and epoxy mortars, each possessing inherent advantages regarding strength, chemical resistance, and curing time. This detailed segmentation allows manufacturers to target specific niche markets, such as underground construction or chemical processing plants, with highly specialized, performance-guaranteed materials, ensuring optimal project outcomes and material longevity in demanding operational environments.

The application segmentation is particularly revealing, categorizing the market into tiling, structural grouting, repair and rehabilitation, external insulation finishing systems (EIFS), and waterproofing. The repair and rehabilitation segment dominates, driven by the global necessity to restore structural integrity to aging concrete assets, which demand mortars with exceptional dimensional stability and bond strength. End-user segmentation further clarifies demand patterns, dividing the market among Residential, Commercial, and Infrastructure sectors. While the Infrastructure segment requires the highest performance specifications and volumes for large-scale public works, the Residential and Commercial sectors prioritize aesthetics, ease of use, and integration with modern architectural designs, such as high-performance tile adhesives that accommodate large-format ceramics and glass tiles, which are sensitive to substrate movement and require superior bond strength.

The Special Mortar Market value chain is complex and involves sophisticated interactions starting from the sourcing of highly specific raw materials through to final application on the construction site. Upstream activities are dominated by specialty chemical manufacturers providing crucial high-cost components such as redispersible polymer powders (RDP), cellulose ethers, and various plasticizers and accelerators. The quality and stable supply of these specialty additives directly determine the performance characteristics and cost of the final mortar product. Basic raw materials, including high-grade cement and precisely graded sand/aggregates, are sourced from bulk suppliers, but the differentiating factor lies in the controlled quality and consistency of these inputs. Effective management of the upstream segment requires strong relationships with a limited number of global specialty chemical suppliers to ensure material integrity and timely delivery amidst global supply chain pressures and fluctuating commodity prices.

Midstream activities involve the core manufacturing process, where raw materials are precisely blended in highly automated dry-mix plants. Leading manufacturers focus heavily on proprietary blending techniques and quality assurance protocols to maintain the consistency required for high-performance specialty mortars. This stage also includes crucial R&D activities focused on optimizing formulations for specific regional climate conditions and regulatory standards. Downstream activities involve distribution and sales, which are critical due to the technical nature of the product. The distribution channel often relies on a hybrid model, utilizing direct sales channels for large infrastructure projects requiring technical consultation and a network of specialized construction material dealers and distributors for smaller commercial and residential projects. Technical sales support and on-site application training are indispensable parts of the downstream value chain, ensuring correct usage and optimal performance of the specialized material.

The distribution network is segmented into direct and indirect channels. Direct channels involve sales to major construction companies and government agencies, where the manufacturer provides extensive technical specifications, large volume supply, and application guidance. Indirect channels rely on wholesale distributors, specialized retail outlets, and building material merchants who stock the pre-bagged special mortars. Given the shelf-life constraints and the need for controlled storage environments, efficient inventory management and cold chain logistics (for specific polymer additives) are essential components of the distribution process. The success of a manufacturer often hinges on their ability to manage a wide and fragmented network while ensuring consistent product quality and offering rapid, localized technical expertise to solve on-site application issues quickly and effectively, thereby maintaining brand trust among professional users.

The primary consumers of special mortar products are highly diverse, spanning specialized contractors, large civil engineering firms, industrial maintenance operators, and housing developers. Specialized contractors, particularly those focused on concrete repair, restoration, and waterproofing, constitute a significant end-user group, requiring high-specification repair and grouting mortars for intricate structural work where material failure is unacceptable. Civil engineering firms engaged in large-scale infrastructure projects—such as the construction of high-speed rail lines, massive harbor facilities, and complex bridge structures—are major buyers, demanding specialty mortars for precision grouting, segment bonding, and protective coatings designed to withstand extreme environmental loading and vibration for decades.

Another major segment comprises industrial end-users, including chemical processing plants, power generation facilities, and wastewater treatment centers. These environments subject construction materials to aggressive chemical attack, high temperatures, and severe abrasion, necessitating the use of specialized epoxy or polymer-modified mortars with exceptional chemical resistance and durability. The maintenance departments within these industrial facilities are continual buyers, utilizing these mortars for routine equipment grouting, protective flooring, and tank lining repairs, focusing heavily on materials that minimize operational downtime and ensure regulatory compliance regarding structural safety and containment integrity.

Furthermore, residential and commercial developers and their affiliated sub-contractors represent a rapidly growing customer base. In the residential sector, the demand is fueled by the popularity of large-format tiles, underfloor heating systems, and specialized façade designs, requiring high-flexibility tile adhesives and thermal insulation mortars to meet modern comfort and energy efficiency standards. For the commercial sector, customers include shopping mall developers, hotel chains, and office tower constructors who require aesthetic, durable, and quick-setting mortars for flooring, architectural finishes, and fireproofing applications, prioritizing materials that contribute to faster project completion and low long-term maintenance costs, thus making the specialized nature of these products indispensable for high-quality modern construction.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $8.5 Billion |

| Market Forecast in 2033 | $13.2 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Sika AG, BASF SE (Master Builders Solutions), Saint-Gobain, The Euclid Chemical Company, Mapei S.p.A., Ardex GmbH, Fosroc International Ltd., W. R. Meadows, Inc., Henkel AG & Co. KGaA, ParexGroup, Pidilite Industries Ltd., CEMEX S.A.B. de C.V., Holcim Group, Custom Building Products, Bostik SA (Arkema Group), CPI Mortars, Rockwool International A/S, Schwenk Zement KG, Baumit GmbH, Franklin International. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Special Mortar Market is highly dynamic, driven by the continuous pursuit of superior performance, ease of application, and environmental compliance. A core technology involves advanced polymer modification, utilizing high-performance redispersible polymer powders (RDPs) such as vinyl acetate-ethylene (VAE) copolymers and styrene-butadiene rubber (SBR) latices. These polymers significantly enhance key material properties, including adhesion strength, flexibility, water resistance, and freeze-thaw durability, crucial for specialized applications like exterior wall insulation and flexible tile systems. Recent innovations focus on developing RDPs that offer improved workability and extended open times without compromising the final mechanical strength, addressing common application challenges faced by construction crews, particularly in high-temperature or low-humidity environments where rapid drying is a major concern for material integrity.

Another pivotal technological advancement is the development of ultra-high performance (UHP) cementitious matrices, often incorporating micro-silica, nano-silica, and finely tuned fiber reinforcement (e.g., carbon or glass fibers). These UHP mortars exhibit compressive strengths significantly higher than conventional concrete, coupled with exceptional toughness and reduced permeability, making them ideal for structural rehabilitation, seismic retrofitting, and specialized industrial flooring applications that demand resistance to severe abrasion and heavy loading. Furthermore, self-consolidating and self-leveling mortar technologies are gaining prominence. These formulations are designed to flow freely and consolidate under their own weight without external vibration, drastically simplifying application, ensuring complete void filling in complex geometric areas (like grouting beneath machine bases), and delivering a perfectly level surface finish, thereby improving construction speed and reducing labor dependency and associated costs on demanding projects.

Sustainability-focused technological trends are also reshaping the market. This includes the development of geopolymer mortars, which utilize industrial by-products like fly ash and blast furnace slag as alkali-activated binders instead of traditional Portland cement, drastically reducing the material’s carbon footprint. Additionally, advancements in smart materials, such as self-healing mortars containing encapsulated bacterial spores or polymers that react to moisture ingress, are beginning to transition from research into commercial pilot projects, promising unprecedented longevity and reduced maintenance requirements for critical infrastructure assets. The deployment of precision dosing and mixing technologies within dry-mix production facilities ensures compositional accuracy, minimizing material variability and guaranteeing the highly specific performance characteristics required for specialized applications across the globe, maintaining a competitive edge through consistent quality control measures.

The global Special Mortar Market exhibits distinct regional consumption and growth patterns, heavily influenced by local construction spending, climatic conditions, and regulatory frameworks. Asia Pacific (APAC) stands as the largest and fastest-growing region, driven by unparalleled levels of urbanization and massive public and private investment in residential, commercial, and infrastructure projects across China, India, and Southeast Asian nations. The demand here is largely focused on new construction, requiring high-volume supplies of tile adhesives, grouting mortars, and general-purpose repair mortars to meet aggressive construction timelines, coupled with an emerging trend toward high-performance waterproofing systems due to monsoon climates and high humidity levels prevalent across the region.

North America and Europe represent mature, high-value markets where growth is predominantly driven by maintenance, rehabilitation, and strict adherence to energy efficiency standards. In Europe, the stringent requirements of the Energy Performance of Buildings Directive (EPBD) fuel the consumption of specialized thermal insulation mortars (EIFS/ETICS) and high-performance façade materials. North America, facing significant deterioration in its aging civil infrastructure (bridges, highways, tunnels), shows extremely high demand for specialized structural repair mortars, corrosion inhibitors, and high-strength non-shrink grouts necessary for critical rehabilitation projects, where failure prevention and long-term durability are the paramount concerns for governmental authorities and asset managers.

The primary drivers include the urgent global need for structural repair and rehabilitation of aging infrastructure, coupled with rapid urbanization in developing regions. Increased regulatory mandates for durable, high-performance, and sustainable construction materials also significantly boost demand, particularly for specialized products offering extended service life and reduced maintenance costs in complex projects.

PMMs incorporate specialized polymers (like VAE or SBR) that substantially improve flexibility, adhesion strength, water resistance, and crack bridging capabilities compared to traditional mortars. This modification makes PMMs suitable for demanding applications, such as large-format tiling, exterior wall systems, and dynamic structural repairs where material movement or moisture exposure is a concern.

The repair and rehabilitation application segment currently holds the largest market share. This dominance is due to the necessity of maintaining and extending the lifespan of existing infrastructure assets globally, including bridges, tunnels, and deteriorating concrete structures that require high-strength, durable, and chemically resistant repair solutions to ensure operational safety and compliance.

Key technological innovations include the development of geopolymers (cement-free, low-carbon binders), the integration of nanotechnology for enhanced material properties like self-healing capabilities and impermeability, and the increasing sophistication of dry-mix blending processes to ensure unparalleled consistency and ease of application on site.

The main challenges involve the high volatility and cost of specialty raw materials (polymers and chemical additives), strict and often diverging regional regulatory requirements regarding VOCs and sustainability, and the persistent shortage of skilled construction labor, which demands continuous innovation toward user-friendly, ready-to-use mortar systems.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.