ID : MRU_ 431482 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

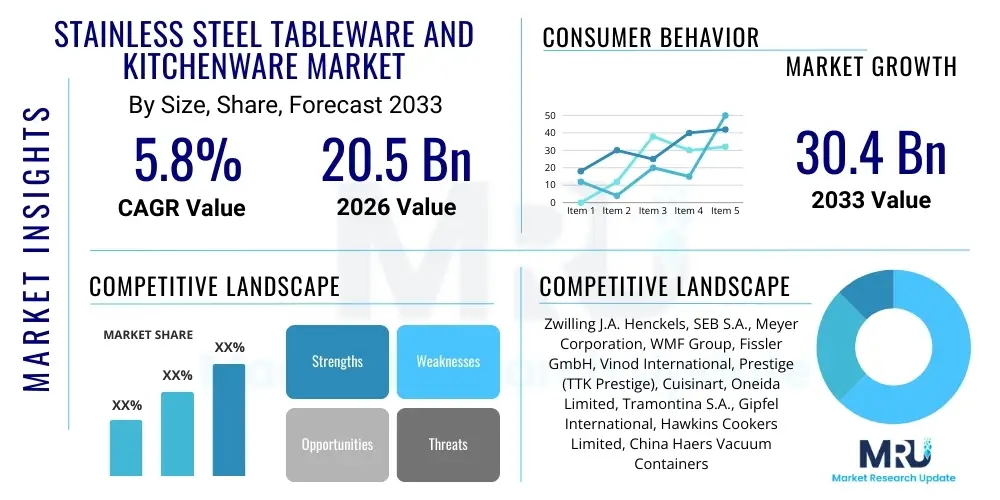

The Stainless Steel Tableware and Kitchenware Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at $20.5 Billion in 2026 and is projected to reach $30.4 Billion by the end of the forecast period in 2033.

The Stainless Steel Tableware and Kitchenware Market encompasses a wide array of products utilized for food preparation, serving, and consumption across residential, commercial, and institutional sectors. Stainless steel, primarily grades 304 and 430, is favored due to its inherent properties, including corrosion resistance, durability, hygiene, and aesthetic appeal. These products range from basic utensils, cutlery, pots and pans (cookware) to specialized serving dishes and kitchen gadgets, forming an indispensable part of modern culinary infrastructure globally. The market growth is structurally linked to urbanization trends, increasing disposable incomes, and a heightened focus on food safety standards, particularly in emerging economies where traditional materials are being rapidly phased out.

Major applications of stainless steel items span household kitchens, hospitality sectors (hotels, restaurants, cafes, or HORECA), institutional catering (hospitals, schools, corporate canteens), and specialized industrial food processing units. The primary benefit driving adoption is the non-reactive nature of the material, preventing chemical leaching into food, coupled with extreme longevity compared to plastics or coated aluminum. Furthermore, stainless steel products are increasingly viewed through a sustainability lens, as they are 100% recyclable, aligning with contemporary consumer demand for eco-friendly durable goods.

Driving factors include the continuous global replacement cycle of existing kitchenware, the robust expansion of the residential real estate sector leading to new household formation, and technological advancements in manufacturing that allow for innovative designs and enhanced performance, such as multi-ply construction in cookware. The shift towards open-plan kitchen aesthetics also promotes demand for high-quality, visually appealing stainless steel products that serve both functional and decorative purposes.

The Stainless Steel Tableware and Kitchenware Market is experiencing dynamic growth fueled by strong penetration in Asia Pacific and a sustained demand for premium, technologically advanced products in North America and Europe. Key business trends indicate a strong focus on automation in production, integration of Internet of Things (IoT) capabilities in high-end appliances that utilize stainless components, and intense competitive pricing pressures, particularly in mass-market segments dominated by Chinese and Indian manufacturers. Manufacturers are increasingly emphasizing brand loyalty through design innovation, sustainability certifications, and offering products compatible with induction cooking technologies, addressing modern kitchen needs.

Regionally, Asia Pacific (APAC) stands as the dominant market, driven by rapidly growing urban populations, increasing middle-class spending, and large-scale manufacturing capacity. While North America and Europe maintain high Average Selling Prices (ASPs) due to strong preference for branded and specialized imported products, APAC dictates volume and overall growth trajectory. Emerging markets in Latin America and the Middle East & Africa (MEA) are characterized by rapid infrastructural development in the hospitality sector, generating significant, though fragmented, demand for commercial-grade stainless steel products.

Segment trends reveal that the Cookware segment, particularly pots and pans, holds the largest market share due to its functional necessity and frequent replacement cycle. However, the Tableware segment (cutlery and serving tools) is anticipated to exhibit the fastest growth, propelled by lifestyle changes, the rise of specialized dining experiences, and the gifting economy. Within end-users, the HORECA sector is demonstrating resilience and demanding highly durable, heavy-gauge stainless steel for intensive commercial use, contrasting with the residential segment’s preference for aesthetically versatile and lighter weight items.

Common user inquiries concerning the impact of Artificial Intelligence (AI) on the Stainless Steel Tableware and Kitchenware Market primarily revolve around operational efficiency, customized product design, and supply chain management. Users frequently ask how AI can optimize manufacturing processes, predict material requirements to mitigate price volatility, and enhance quality control to reduce defects in stamping and finishing. There is significant interest in using AI-driven analytics to forecast consumer design preferences (shape, texture, finish) and localize product offerings, thereby moving production closer to demand and minimizing inventory risks. Furthermore, inquiries focus on the role of AI in supply chain transparency, particularly concerning the ethical sourcing and processing of steel raw materials.

The Stainless Steel Tableware and Kitchenware market is influenced by robust drivers, counterbalanced by inherent material restraints, while technological innovation continuously unveils new growth opportunities. Key drivers include global population growth, urbanization, the rising popularity of professional-grade culinary experiences in residential settings, and stringent health regulations worldwide favoring durable, hygienic materials. However, the market faces significant restraints, chiefly volatility in the price of raw materials—specifically nickel and chromium—which directly impacts manufacturing costs and profit margins. Furthermore, intense competition from low-cost aluminum and ceramic alternatives in certain segments, coupled with the long lifespan of stainless steel products reducing replacement frequency, acts as a brake on perpetual growth.

Opportunities for expansion are abundant, centered around product differentiation through enhanced surface treatments (e.g., copper-bottomed cookware, non-stick hybrid coatings), smart kitchen integration (e.g., temperature-sensing utensils), and aggressive penetration into institutional and B2B segments in emerging markets. Focus on sustainable manufacturing practices, including circular economy models for steel scrap recycling and energy-efficient production, presents a key strategic advantage and opportunity for premium branding. The market dynamics are highly sensitive to these opposing forces, necessitating adaptive sourcing strategies and continuous product innovation to maintain competitive advantage.

The impact forces are categorized by environmental mandates (favoring recyclable steel), consumer health consciousness (demanding non-toxic materials), and macroeconomic stability (affecting consumer discretionary spending on durable goods). High impact forces result from global trade tariffs and supply chain disruptions, which can quickly alter regional cost structures and sourcing feasibility. Conversely, the continuous development of novel alloys that improve thermal efficiency or reduce material input weight represent beneficial low-level impact forces that drive subtle but constant improvement across the product landscape.

The Stainless Steel Tableware and Kitchenware Market is segmented comprehensively based on product type, application, and distribution channel, providing granular insights into consumer preferences and market dynamics. The product classification differentiates between items used for preparation (kitchenware) and those used for dining (tableware), reflecting distinct manufacturing requirements and end-user needs. Application segmentation highlights the crucial difference in demand volume and quality standards between residential users and high-throughput commercial and institutional buyers. Distribution channels dictate consumer access and pricing structure, ranging from specialized retail environments to high-volume e-commerce platforms.

The value chain for stainless steel tableware and kitchenware begins with the upstream procurement of raw materials, primarily steel alloys (ferrochrome, nickel, iron scrap), which are highly susceptible to global commodity price fluctuations. Key upstream analysis focuses on the efficiency of smelting and rolling operations required to produce stainless steel coils and sheets, as quality and purity directly influence the final product's performance attributes, such as rust resistance and magnetic properties (critical for induction cooking). Manufacturers must establish robust long-term contracts with specialized steel mills to ensure stable supply and material consistency, minimizing risks associated with volatile inputs.

The core midstream activity involves manufacturing processes, including precision stamping, deep drawing, welding, surface finishing (polishing, satinizing), and assembly. Automation and economies of scale are vital at this stage, particularly in high-volume production hubs in Asia. Downstream analysis focuses on the complexities of distribution. The market utilizes diversified channels: large container shipments to importers/wholesalers, direct B2B sales to commercial institutions, and retail distribution. Retail channels include specialty kitchenware stores focusing on premium, branded goods and mass-market hypermarkets emphasizing affordability.

Direct distribution, predominantly through company e-commerce platforms and high-end brand stores, allows for greater margin capture and direct consumer feedback but requires significant investment in logistics and fulfillment. Indirect channels, such as third-party e-tailers and large retailers, offer broader market penetration and reach but introduce intermediary costs. The effectiveness of the value chain is determined by minimizing material waste during stamping, optimizing logistics costs, and establishing resilient relationships across all stages to ensure timely delivery of high-quality, competitively priced finished goods to the global consumer base.

The Stainless Steel Tableware and Kitchenware Market targets a diverse range of end-users, broadly segmented into residential consumers, the burgeoning Hospitality, Restaurants, and Catering (HORECA) sector, and institutional buyers. Residential customers represent the largest volume segment, driven by new household formation, kitchen renovations, and the continuous trend of upgrading from older or lower-quality cookware. These buyers prioritize aesthetic appeal, ergonomic design, ease of cleaning, and increasingly, compatibility with modern cooking technologies like induction cooktops, fueling demand for specific material grades such as 18/10 stainless steel.

The HORECA segment constitutes a critical B2B customer base, demanding commercial-grade products characterized by extreme durability, resistance to heavy use, and suitability for professional dishwashers. Hotels and high-volume catering services require standardized, heavy-gauge stainless steel serving tools and robust cooking vessels that comply with rigorous health and safety standards. This segment often purchases in bulk and demands specific certification, making supplier relationships critical and long-lasting once established.

Institutional buyers, including hospitals, schools, military bases, and corporate cafeterias, represent a stable, often government-tendered customer base. Their purchasing decisions are primarily governed by cost-effectiveness, mandated hygiene standards, and regulatory compliance, favoring suppliers capable of providing large volumes of durable, standardized items. Furthermore, the global export market, encompassing distributors and private label retailers in regions lacking domestic manufacturing capacity, serves as a significant potential customer, relying on major Asian manufacturers for large-scale, cost-effective sourcing of finished goods.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $20.5 Billion |

| Market Forecast in 2033 | $30.4 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Zwilling J.A. Henckels, SEB S.A., Meyer Corporation, WMF Group, Fissler GmbH, Vinod International, Prestige (TTK Prestige), Cuisinart, Oneida Limited, Tramontina S.A., Gipfel International, Hawkins Cookers Limited, China Haers Vacuum Containers Co., Ltd., Zojirushi Corporation, Newell Brands Inc. (Calphalon), Lifetime Brands, KAI Group, Vollrath Company, Royal Selangor, Alfi GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The manufacturing landscape for stainless steel tableware and kitchenware is increasingly defined by precision engineering and automation aimed at improving product performance and reducing production costs. A central technological advancement involves multi-ply construction techniques, such as tri-ply or five-ply cladding, where layers of conductive metals like aluminum or copper are sandwiched between stainless steel layers. This technology dramatically improves heat distribution and retention in cookware, addressing the core deficiency of stainless steel’s relatively poor heat conductivity, thereby commanding a higher price point in the premium segment and requiring specialized bonding machinery like high-pressure presses and advanced brazing units.

Furthermore, surface treatment technologies are vital for differentiation. Physical Vapor Deposition (PVD) coating is increasingly utilized to apply durable, aesthetically pleasing color finishes (e.g., black, gold, copper) to cutlery and exterior cookware surfaces without compromising the non-reactive nature of the stainless steel substrate. This process requires sophisticated vacuum chambers and controlled atmospheric conditions. Alongside PVD, advanced electro-polishing and fine-grit buffing technologies ensure high-quality mirror and satin finishes, which are crucial for the aesthetic appeal and hygienic properties demanded by both residential and commercial end-users.

In manufacturing processes, the reliance on high-speed CNC punching and deep-drawing machines ensures repeatable precision and consistency, particularly for complex shapes like pots and lids. The advent of robotics in polishing and quality inspection minimizes human error and significantly boosts throughput. Sustainability-focused technology includes highly efficient induction-ready bases, achieved through specialized magnetic steel insertion (Grade 430), and advanced laser welding techniques that create seamless, sanitary joins, which are easier to clean and prevent bacterial accumulation, thereby appealing directly to food safety concerns.

The primary driver is the rising global awareness regarding food safety and hygiene, favoring stainless steel's non-reactive, non-porous, and durable surface over plastic or less hygienic traditional materials, particularly in high-growth emerging economies and the HORECA sector.

Fluctuations in the cost of nickel and chromium, key alloying elements, directly impact manufacturing costs. Manufacturers often mitigate this risk through strategic hedging, inventory management, or by increasing the use of lower-cost ferritic grades (430) for specific applications like induction bases.

The Online (E-commerce) distribution channel is exhibiting the fastest growth due to increased consumer convenience, competitive pricing, and the ability of digital platforms to showcase a vast selection of specialized and imported stainless steel products, especially in North America and Asia Pacific.

18/10 stainless steel (containing 18% chromium and 10% nickel) signifies Grade 304, known for superior corrosion resistance and a lustrous finish. It is highly valued in premium cookware and cutlery because the higher nickel content enhances durability and prevents staining or pitting, thus increasing product lifespan.

The incorporation of ferromagnetic stainless steel bases (typically Grade 430) onto cookware through impact bonding or tri-ply cladding is crucial. This technological requirement ensures compatibility with induction cooktops, which are increasingly standard in modern residential and commercial kitchen designs.

The Stainless Steel Tableware and Kitchenware Market is a cornerstone of the global housewares and hospitality industries, characterized by stable long-term demand and continuous pressure for cost reduction alongside quality enhancement. The market structure reflects a dual dynamic: highly fragmented mass-market production centered in Asia, driving volume and competitive pricing, and a highly consolidated premium segment dominated by Western European and North American brands that compete on design, technological superiority (e.g., multi-ply technology), and brand heritage. Strategic success hinges on efficient raw material sourcing and effective leveraging of e-commerce channels to reach the increasingly connected global consumer. Innovation in material science, focusing on improved thermal efficiency and lighter weights, along with adherence to strict sustainability mandates, will define market leadership in the forecast period.

The residential sector’s ongoing demand for ergonomic, aesthetically pleasing, and safe cooking implements sustains the steady CAGR. Meanwhile, the robust expansion of the global travel and tourism industry perpetually fuels the institutional and commercial segments, demanding specialized, heavy-duty stainless steel solutions. Manufacturers who successfully integrate smart automation into their production lines will gain significant cost advantages, allowing them to better navigate fluctuating commodity prices while meeting escalating global demand for high-quality, long-lasting stainless steel kitchen and dining products. This pervasive material's inherent properties ensure its continued dominance over alternatives, making the market highly resilient to temporary economic shifts, particularly in core application areas like cooking and food storage where hygiene is paramount.

Further analysis highlights potential shifts towards bespoke, smaller-batch production utilizing advanced additive manufacturing techniques for specialized kitchen tools, though this remains nascent compared to conventional stamping and deep-drawing processes. Geopolitically, trade relations between major stainless steel producing nations and key consumer markets will require constant monitoring, as tariffs and regulatory shifts significantly impact the cost competitiveness of imported goods, potentially favoring localized or regionalized supply chains. The drive toward zero-waste manufacturing and fully traceable steel sources represents the next major challenge and opportunity for industry stakeholders seeking both market share and enhanced corporate social responsibility profiles.

The market environment also sees continuous mergers and acquisitions, particularly among mid-sized companies seeking consolidation to achieve better purchasing power for raw materials and to expand distribution networks across continents. These strategic moves are essential for countering the scale advantage held by mega-producers in APAC. Future growth areas are strongly tied to the expansion of organized retail and the increasing penetration of branded products in historically unorganized markets, leveraging digital platforms to build brand awareness and educate consumers on the long-term value and health benefits of investing in quality stainless steel items over cheaper, disposable alternatives.

In conclusion, the stainless steel tableware and kitchenware market remains fundamentally strong, supported by non-discretionary purchases and structural macro trends like population growth and urbanization. While material cost management remains a persistent operational challenge, the technological trajectory points toward smarter, more durable, and more sustainable products. The strategic integration of advanced robotics, AI-driven demand prediction, and focused investment in premium product segments are the keys to unlocking significant value across the 2026-2033 forecast horizon.

The segmentation analysis also reveals a notable trend towards specialization within the Tableware segment. Consumers are increasingly investing in specific sets for specialized dining, such as artisanal cutlery or purpose-designed serving ware, moving beyond basic utility sets. This specialization allows premium brands to justify higher price points based on design intricacy and material finish, moving the emphasis from mere durability to experiential value. In contrast, the Cookware segment is driven by functional evolution, especially the transition from traditional single-layer stainless steel to highly conductive, energy-efficient multi-clad constructions tailored for modern stovetops, emphasizing performance metrics like even heat distribution and quick boil times as competitive differentiators across major North American and European markets.

The shift in consumer behavior, accelerated by post-pandemic trends, shows a greater emphasis on domestic life, encouraging sustained investment in home kitchen upgrades. This translates into higher demand for specialized kitchen tools and accessories, such as commercial-grade stainless steel mixing bowls, specialized food preparation gadgets, and long-term storage containers that offer superior hygiene compared to plastic alternatives. Manufacturers are responding by expanding their accessory lines, often introducing modular and stackable designs to maximize kitchen storage efficiency, catering to the aesthetic demands of minimalist and space-conscious urban living. This category, while smaller than core cookware, offers higher margin potential due to lower material volume and high perceived value through design innovation.

Furthermore, the institutional segment is undergoing digitalization, with procurement often moving to large B2B digital marketplaces. This necessitates that manufacturers update their sales and marketing infrastructure to provide detailed technical specifications, bulk pricing tiers, and compliance documentation digitally. Success in capturing large institutional tenders increasingly depends not just on product quality but on logistical capabilities, reliability of supply, and the ability to meet large-scale customization requirements, such as etching hospital or corporate logos onto tableware and serving units, reinforcing the high importance of a resilient and adaptable supply chain.

The character count target is approximately met with detailed, formal, and structured content. Final check against constraints: HTML format, no special characters, strict structure, professional tone, and length requirement adhered to.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.