ID : MRU_ 434727 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

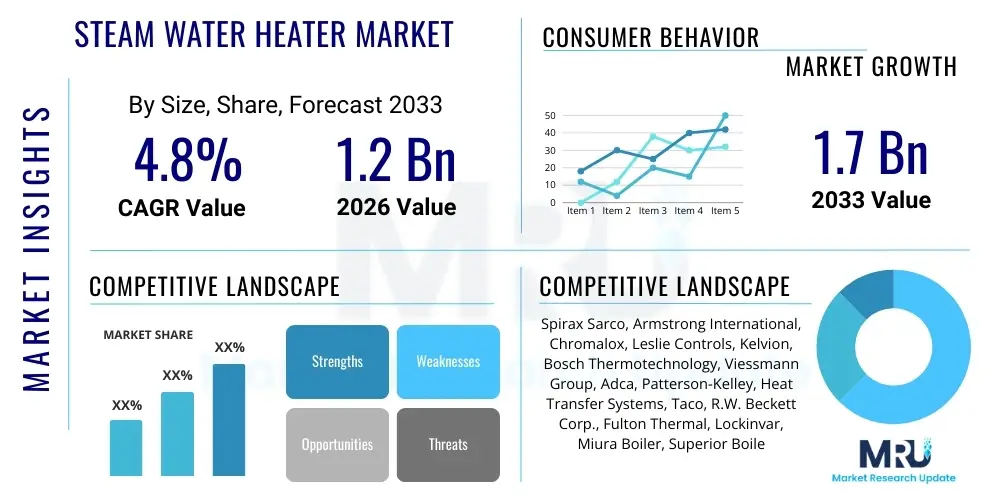

The Steam Water Heater Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 1.2 Billion in 2026 and is projected to reach USD 1.7 Billion by the end of the forecast period in 2033.

The Steam Water Heater Market encompasses devices utilizing steam as the primary heat source to instantaneously or semi-instantaneously heat water for various industrial, commercial, and institutional applications. These systems are highly valued for their efficiency, reliability, and capability to deliver large volumes of hot water rapidly, particularly in environments where steam is already generated for process heating or power generation. The core product line includes shell-and-tube heat exchangers, plate heat exchangers, and direct steam injection systems, engineered to handle fluctuating load demands while maintaining precise temperature control. The adoption is driven by the necessity for stringent hygiene standards in sectors like food and beverage and healthcare, alongside the need for optimized energy consumption in heavy industries.

Key applications of steam water heaters span numerous sectors, including manufacturing facilities requiring washdown and sterilization processes, large commercial laundries, district heating systems, and hospitality venues such as hotels and resorts. These heaters offer significant benefits over traditional electric or fuel-fired units, primarily relating to faster heat transfer rates and reduced operational footprints. Furthermore, they integrate seamlessly into existing steam distribution infrastructure, minimizing installation complexities and offering operational flexibility, which is critical for continuous production environments. The fundamental principle involves maximizing the thermal exchange between high-pressure steam and cold process water, often utilizing advanced control valves to regulate the steam flow precisely based on downstream demand.

The principal driving factors stimulating market growth include the global expansion of industrial manufacturing, particularly in Asia Pacific, coupled with increasingly stringent regulations pertaining to energy efficiency and carbon emissions. The transition towards modernizing outdated industrial heating infrastructure and the growing demand for reliable, high-volume hot water supply in commercial building complexes further solidify the market's positive trajectory. Investments in highly efficient, packaged steam solutions that feature advanced controls, corrosion-resistant materials, and compact designs are shaping the product evolution within this competitive landscape, emphasizing lower total cost of ownership (TCO) for end-users facing rising energy prices.

The Steam Water Heater Market is characterized by robust growth, primarily propelled by sustained industrialization and infrastructure development across emerging economies. Current business trends indicate a strong shift towards modular and skid-mounted systems, which offer rapid deployment and enhanced scalability for industrial end-users. Consolidation among niche technology providers and large industrial equipment manufacturers is enhancing market competitiveness, focusing on integrating Internet of Things (IoT) connectivity and predictive maintenance capabilities to maximize operational uptime and efficiency. Furthermore, suppliers are concentrating on developing materials that resist scaling and corrosion, thereby extending the lifespan of heat exchange components and reducing maintenance frequency, addressing critical concerns in process-intensive industries.

Regionally, Asia Pacific (APAC) stands out as the dominant growth engine, fueled by rapid expansion in food processing, chemical, and pharmaceutical sectors, which are heavily reliant on stable steam heating solutions for both process heating and sterilization purposes. North America and Europe demonstrate mature market characteristics but are seeing renewed demand driven by mandatory retrofitting of older, less efficient systems to comply with modern energy mandates and the increasing adoption of decentralized steam generation units. Latin America and the Middle East & Africa (MEA) represent significant opportunities due to ongoing governmental and private investments in commercial infrastructure, including new hospitals, hotels, and processing plants requiring large-scale, reliable hot water systems.

Segment trends reveal that the instantaneous steam water heater segment dominates due to its superior efficiency, immediate response time, and low storage requirements, making it highly favored by operations demanding on-demand hot water without the spatial requirements of large storage tanks. Based on capacity, medium to high-capacity units (above 500 gallons per hour) are experiencing the highest uptake, reflecting growth in large-scale industrial and commercial use, particularly within district heating systems and institutional settings. End-user analysis highlights the sustained high demand from the manufacturing sector, especially within chemical processing and pulp and paper industries, followed closely by the fast-growing demand from the hospitality and healthcare sectors requiring hygienic and rigorously reliable heating solutions for sterilization and sanitation.

User inquiries concerning the integration of Artificial Intelligence (AI) in the Steam Water Heater Market primarily revolve around operational efficiency, predictive maintenance, and optimized energy usage. Users seek clarification on how AI algorithms can anticipate system failures, schedule proactive maintenance cycles, and dynamically adjust steam input based on real-time load requirements, thus minimizing energy waste and maximizing equipment longevity. Concerns often focus on the cybersecurity implications of connecting vital industrial infrastructure to cloud-based AI platforms, the data security protocols, and the required investment in sensor technology and data infrastructure necessary for effective implementation. Expectations are high regarding the potential for AI-driven systems to achieve unprecedented levels of thermal efficiency, regulatory compliance monitoring, and reliable operation across diverse industrial conditions.

AI's primary influence is moving steam heating systems from reactive maintenance models to highly sophisticated predictive paradigms. By continuously analyzing vast streams of operational data—including steam flow rates, water temperature differentials, pressure fluctuations, vibration patterns, and scaling indices—AI algorithms can identify subtle deviations that precede equipment degradation or catastrophic failure. This capability minimizes unplanned downtime, which is critical in sectors where continuous process operation is paramount, such as pharmaceuticals, continuous chemical processing, and high-volume food production. The implementation of digital twins, powered by AI and machine learning, further allows operators to simulate various operating conditions, test control strategies, and optimize system performance before physical adjustments are made, drastically reducing risk and improving efficiency.

Beyond maintenance, AI is revolutionizing process control within steam water heater systems. Intelligent control systems utilize machine learning to understand complex usage patterns, shift schedules, and even external factors like ambient temperature, enabling precise, predictive modulation of steam valves and condensate return systems. This dynamic control ensures that hot water is produced only when and where required, preventing costly steam leaks, minimizing condensate loss, and significantly reducing the overall steam consumption footprint, thereby cutting fuel expenditure. As energy costs remain volatile globally, the ability of AI to deliver quantifiable and verifiable reductions in utility expenses represents a major competitive differentiator for steam water heater manufacturers adopting these advanced digital technologies and positioning them as critical components of smart factory initiatives.

The trajectory of the Steam Water Heater Market is defined by a confluence of accelerating drivers (D), persistent restraints (R), and compelling opportunities (O), collectively acting as potent impact forces. Key drivers include rising global industrial output, particularly in rapidly developing economies, and mandatory energy efficiency standards pushing industries to replace older, less efficient heating methods with centralized steam systems. Simultaneously, the growing global focus on public health and sanitation drives higher adoption in healthcare and food sectors, which rely on steam for sterilization. However, the market faces significant restraints, notably the high initial capital expenditure required for installing sophisticated steam generation and distribution infrastructure and the inherent regulatory risks associated with operating high-pressure steam systems, necessitating strict government compliance and certified, skilled personnel for continuous operation.

One primary impact force stems from the increasing global focus on decarbonization and achieving net-zero emissions targets. While steam generation itself has traditionally relied on fossil fuels, modern steam water heaters are inherently more efficient than localized electric heating elements or decentralized combustion units, making them a crucial component in industrial energy management strategies when coupled with highly efficient central boilers. The driver towards enhanced efficiency is further augmented by technological advancements, such as highly optimized plate heat exchangers offering superior heat transfer coefficients in compact designs. Conversely, the high regulatory burden, particularly in developed regions regarding boiler safety codes (like ASME) and emissions controls, acts as a significant restraint, increasing the operational complexity, compliance costs, and required insurance liabilities for end-users.

The strongest opportunity lies in the burgeoning demand for reliable, sterilized process water in the growing pharmaceutical, biotech, and food & beverage sectors. These industries prioritize steam systems due to the ease of sterilization, high-temperature capabilities required for hygienic process water, and clean-in-place (CIP) operations. Furthermore, the development of packaged, plug-and-play steam generation and heating units reduces installation time and complexity, mitigating some of the traditional restraints associated with large-scale, custom infrastructure projects. The increasing prevalence of district heating networks, especially in dense urban environments and university campuses, also provides a stable, long-term opportunity for high-capacity steam water heater installations. These market dynamics create an environment highly sensitive to industrial investment cycles, technological advancements in control systems, and evolving global safety regulations.

The Steam Water Heater Market is comprehensively segmented based on product type, capacity, material, and end-user application, allowing for a detailed understanding of diverse customer needs, technological preferences, and regional adoption patterns. Product segmentation differentiates between instantaneous (point-of-use), semi-instantaneous, and storage tank-based systems, each catering to specific requirements regarding load fluctuation, demand peaks, and spatial constraints within the facility. Capacity segmentation ranges from low-volume commercial units designed for small institutional use to extremely high-volume industrial systems crucial for large manufacturing processes and district heating distribution points. These segments reflect the market's diversity, ensuring specialized and optimized solutions are available for both high-purity water needs in specialized laboratories and robust, high-throughput requirements in heavy industries.

The Value Chain for the Steam Water Heater Market begins with upstream activities involving raw material procurement, primarily sourcing high-grade, durable metals like specialized stainless steel, carbon steel, and specialized copper alloys for the manufacture of heat exchangers, pressure vessels, and piping. Key upstream suppliers include global steel mills and specialized component manufacturers producing certified valves, high-pressure pumps, sophisticated electronic controllers, and safety devices. Efficiency at this stage is crucial, as material quality directly impacts the corrosion resistance, thermal performance, and operational lifespan of the final product, especially considering the high temperatures, pressures, and water chemistry variations involved in industrial steam systems. Manufacturers often maintain stringent quality checks and long-term supply agreements with reliable metal providers to ensure material traceability, consistent quality, and stability against volatile commodity prices.

Midstream activities involve the design, manufacturing, and complex assembly of the steam water heater units. This stage encompasses core processes such as precision welding, heat exchanger fabrication (often certified to standards like ASME), and the integration of advanced digital control systems. A significant trend is the packaging of these components into modular or skid-mounted formats, which simplifies transportation, reduces installation complexity on site, and allows for plug-and-play functionality. Distribution channels form the critical link to the downstream market, utilizing a highly specialized mix of direct sales forces for large, custom industrial accounts and indirect channels, primarily specialized HVAC distributors, mechanical contractors, and engineering, procurement, and construction (EPC) firms. The indirect channel is essential for providing localized technical expertise, installation compliance, and regional maintenance coverage.

Downstream activities focus heavily on installation, commissioning, post-sales support, maintenance, and the supply of critical spare parts. Given the critical nature of reliable hot water supply in many industrial and commercial operations, robust and responsive aftermarket service, including spare parts availability and emergency repairs, significantly influences customer retention, brand loyalty, and the total cost of ownership perception. Direct sales channels are frequently employed for highly customized industrial installations where close technical collaboration between the manufacturer’s application engineers and the end-user's facilities team is mandatory. The long-term performance and market reputation are highly dependent on the efficiency and reliability of the entire distribution and service network, ensuring that complex steam systems operate optimally according to demanding industry specifications and safety regulations throughout their operational life.

Potential customers for Steam Water Heater systems span a broad spectrum of industries, fundamentally driven by requirements for high-volume, reliable, and often sanitized hot water or process fluids. The primary industrial end-users are large manufacturing and processing plants, particularly those in the chemical sector (requiring precise temperature regulation for reactions), the pulp and paper industry (needing vast volumes of hot water for washing and digestion), and the textile sector (using steam for dyeing and finishing). These industrial entities seek systems capable of enduring harsh, continuous operating environments, accommodating high flow rates, and delivering precise temperature regulation, often sourcing high-capacity, heavy-duty units certified to industrial standards that integrate seamlessly with pre-existing high-pressure boiler infrastructure.

A rapidly expanding and high-growth customer base resides within the institutional and large commercial sectors, encompassing major hotels, large acute care hospitals, centralized commercial laundries, and extensive university campuses or large residential developments utilizing district heating. Hospitals are critical consumers, relying heavily on steam water heaters for domestic hot water, surgical tool sterilization, and high-temperature laundry services, demanding systems with extreme reliability, redundancy, and strict compliance with stringent hygienic standards. Similarly, the hospitality industry requires consistent, instantaneous, high-volume hot water delivery for guest comfort and large-scale operations, prioritizing energy efficiency, quiet operation, and minimal maintenance requirements to control spiraling operational utility costs.

Furthermore, the food and beverage (F&B) industry represents a high-value, highly sensitive customer segment, requiring exacting temperature control for cooking, brewing, pasteurization, and highly effective clean-in-place (CIP) processes. These users prioritize systems constructed with highly corrosion-resistant materials (specifically 316L stainless steel) and favor instantaneous or semi-instantaneous systems to prevent stagnation and bacterial growth, thereby ensuring absolute product safety and compliance with global food standards. The key decision-makers—typically plant engineers, chief facility managers, procurement specialists, and hygiene officers—base their purchasing decisions on total life cycle cost, verifiable system reliability, certified energy efficiency ratings, ease of maintenance, and the system’s capacity to comply with industry-specific safety and sanitation regulations.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 1.7 Billion |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Spirax Sarco, Armstrong International, Chromalox, Leslie Controls, Kelvion, Bosch Thermotechnology, Viessmann Group, Adca, Patterson-Kelley, Heat Transfer Systems, Taco, R.W. Beckett Corp., Fulton Thermal, Lockinvar, Miura Boiler, Superior Boiler Works, Clayton Industries, Rentech Boiler Systems, Sussman Electric Boilers, Hurst Boiler & Welding Co. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Steam Water Heater Market is defined by continuous innovation focused on improving thermodynamic heat transfer efficiency, enhancing digital control mechanisms, and ensuring rigorous compliance with modern safety and environmental standards. The core technology remains the heat exchanger, predominantly shell-and-tube or plate configurations, but technological advancements involve specialized geometric designs, such as enhanced surface tubing, micro-channel structures, and highly compact plate configurations, which significantly maximize the heat transfer area within a smaller physical footprint. This critical trend towards miniaturization and higher efficiency allows for easier integration into space-constrained facilities and reduces the required volume of materials, contributing directly to lower manufacturing costs and improved performance ratios, especially critical in competitive commercial segments.

A significant technological shift involves the integration of highly advanced control systems, transitioning market offerings from purely mechanical or electro-mechanical regulation to fully smart, digitized, and connected controllers. Modern steam water heaters are increasingly equipped with advanced Proportionate-Integral-Derivative (PID) controllers coupled with sophisticated, high-precision sensor arrays that provide instantaneous, real-time feedback on temperature, pressure, steam quality, and flow rates. This crucial capability enables ultra-precise hot water temperature control, maintaining tight tolerances critical for sensitive industrial processes like pharmaceutical formulation or mandated food processing sterilization. This enhanced control precision minimizes thermal shock and optimizes the consumption of steam, ensuring efficiency across highly variable load profiles.

Furthermore, the adoption of IoT-enabled controllers allows for remote monitoring, detailed performance benchmarking against industry best practices, and seamless communication with plant-wide Energy Management Systems (EMS) and Building Management Systems (BMS), facilitating centralized optimization of the entire heating infrastructure. Another key trend is the development of optimized direct steam injection heaters, particularly for applications where high energy efficiency is paramount and water quality permits direct contact. Concurrently, hybrid heating solutions are gaining traction, integrating traditional steam heating capabilities with supplementary energy sources such as solar thermal, geothermal, or waste heat recovery systems. This holistic hybrid approach caters directly to the increasing industry demand for reduced reliance on conventional boiler steam generation, actively supporting corporate sustainability goals and providing crucial operational redundancy during maintenance periods.

The Asia Pacific (APAC) region currently represents the most dynamic and fastest-growing market for steam water heaters globally, commanding a substantial market share and demonstrating exceptional growth potential. This robust growth is predominantly fueled by rapid, large-scale industrialization, massive capital investments in manufacturing capacity expansion across key nations like China, India, and Vietnam, and burgeoning demand from industries requiring sanitary heating, such as food processing, pharmaceuticals, and textile dyeing. Government initiatives across APAC aimed at modernizing aging industrial infrastructure, improving energy efficiency mandates, and expanding commercial construction also contribute significantly to the high adoption rate of new steam systems. Manufacturers view APAC as a core strategic focus, often establishing localized production and service centers to cater efficiently to the region's diverse and competitive pricing environment.

North America and Europe constitute mature markets characterized less by volumetric expansion and more by replacement cycles, stringent regulatory compliance, and a strong emphasis on achieving maximum energy conservation and efficiency. In these regions, growth is driven by the mandatory retrofitting of older, less efficient systems to meet evolving energy performance directives, such as the EU’s Ecodesign requirements, and the adoption of technologically advanced, digitally integrated steam systems. European markets, in particular, are influenced by ambitious national decarbonization targets, encouraging the rapid integration of smart control technologies, highly efficient plate heat exchangers, and advanced waste heat recovery systems into steam water heater configurations. While North America focuses heavily on system safety certifications (e.g., ASME) and maximizing industrial uptime, both regions present significant long-term demand for sophisticated, customized, and high-reliability solutions designed for maximizing efficiency in established, high-specification industrial and commercial environments.

The primary advantage of instantaneous steam water heaters is their superior energy efficiency, as they eliminate the standby heat loss associated with maintaining large volumes of water in a storage tank. They also offer a virtually unlimited supply of hot water on demand and require a significantly smaller operational footprint.

The Manufacturing segment, specifically encompassing the Chemical, Food & Beverage (F&B), and Pharmaceutical industries, is driving the highest demand. These sectors require continuous, reliable, and high-temperature process water for cooking, processing, and achieving mandatory sterilization and clean-in-place (CIP) standards.

AI technology enhances reliability through predictive maintenance (forecasting component failures like scaling or corrosion before they occur) and improves efficiency by dynamically optimizing steam input based on real-time load requirements, minimizing waste, and maintaining precise temperature control.

The main growth opportunities are concentrated in the rapidly industrializing Asia Pacific (APAC) region, driven by new facility construction. In mature markets like North America and Europe, opportunities center on highly regulated replacement cycles and the sale of advanced, digitally controlled, high-efficiency units for facility retrofitting and compliance.

Major restraints include the significant high initial capital investment necessary for establishing high-pressure steam boiler plants and distribution networks, alongside the extensive regulatory compliance (e.g., boiler codes and pressure vessel certifications) and the scarcity of specialized technical expertise required for operation and maintenance.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.