ID : MRU_ 438350 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

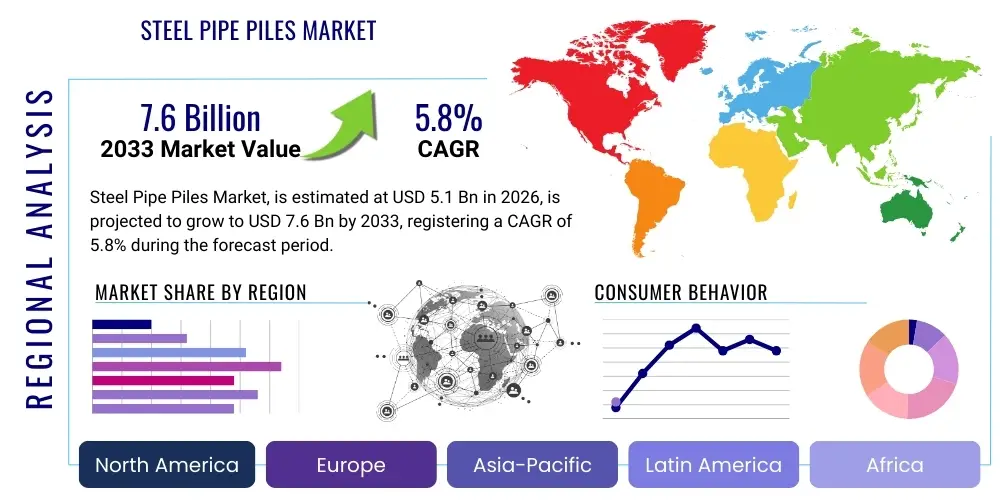

The Steel Pipe Piles Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at $5.1 Billion in 2026 and is projected to reach $7.6 Billion by the end of the forecast period in 2033.

The Steel Pipe Piles Market encompasses the manufacturing, distribution, and utilization of high-strength steel tubular structures primarily used for deep foundation construction. These piles are essential components in transmitting heavy loads from superstructures, such as bridges, high-rise buildings, and offshore platforms, down to deep, stable soil layers or bedrock. The inherent strength, versatility, and ease of splicing and handling steel pipe piles make them preferred choices in demanding geotechnical environments, including seismic zones and marine applications where lateral and uplift forces are significant. The product's robustness against driving stresses and the ability to be filled with concrete further enhance its load-bearing capacity and overall structural integrity, ensuring long-term performance across diverse infrastructure projects.

Product descriptions typically involve various specifications based on diameter, wall thickness, steel grade (e.g., ASTM A252, API 5L), and joint configurations (open-ended or closed-ended). Major applications span critical infrastructure sectors, including civil engineering projects like coastal protection, deepwater ports, and large-scale transportation networks. The increasing global focus on developing resilient infrastructure that can withstand extreme weather conditions and escalating urbanization mandates the use of reliable deep foundation solutions, positioning steel pipe piles as indispensable components in modern construction paradigms.

Key benefits driving market adoption include their high compressive and tensile strength, minimal soil displacement during installation (especially for open-ended piles), and suitability for various corrosive environments when protective coatings or cathodic protection systems are applied. Furthermore, their seamless integration with existing construction techniques and the potential for rapid installation timelines contribute significantly to project efficiency. Driving factors are predominantly linked to government investments in infrastructure rehabilitation, the surge in offshore wind farm development requiring robust foundation support, and the continuous growth of megacities requiring stable foundations for increasingly tall structures.

The Steel Pipe Piles Market is characterized by robust growth, primarily fueled by massive infrastructure spending across Asia Pacific and steady recovery in European and North American civil engineering sectors. Business trends indicate a strong focus on advanced steel grades offering superior yield strength, allowing for thinner walls and optimizing material consumption, thereby enhancing cost-efficiency and sustainability profiles. Furthermore, the market is witnessing increased integration of digital technologies, such as Building Information Modeling (BIM) for precise pile planning and installation monitoring systems, contributing to improved operational accuracy and reduced project risk. Strategic mergers and acquisitions among major steel producers and foundation contractors are reshaping the competitive landscape, aiming for vertical integration and enhanced supply chain control, particularly in high-demand regions like Southeast Asia.

Regional trends highlight Asia Pacific's dominance, driven by extensive port expansions in countries like China and India, coupled with massive railway and highway corridor developments. North America exhibits consistent demand, primarily due to the refurbishment of aging bridge infrastructure and energy pipeline projects. Europe is characterized by stringent environmental regulations, pushing for sustainable sourcing and manufacturing processes, while simultaneously seeing significant demand from the burgeoning offshore renewable energy sector, especially for monopile foundations utilizing large-diameter steel pipes. The Middle East and Africa (MEA) region shows accelerating growth, catalyzed by large-scale urban development projects and expansion of oil and gas terminal facilities requiring deep foundations.

Segment trends underscore the rising preference for higher-strength steel grades (e.g., Grade 50 and above) to meet extreme load requirements in complex structures. The open-ended pipe pile segment maintains a lead in volume due to cost-effectiveness and versatility, although closed-ended piles are essential in specific deep driving conditions or highly abrasive soil profiles. Application-wise, the Marine & Ports segment is experiencing the fastest growth, directly correlating with global trade volume increases and the necessity for deeper berths to accommodate larger vessels. Concurrently, the increasing complexity of geotechnical challenges necessitates specialized piling solutions, leading to higher average selling prices (ASPs) for custom-fabricated steel pipes.

Users frequently inquire about how Artificial Intelligence (AI) can enhance the efficiency and safety of steel pipe pile installation and structural integrity monitoring. Key themes revolve around leveraging machine learning for predictive maintenance, optimizing driving sequences based on real-time geotechnical data, and automating quality control processes during fabrication. Concerns often touch upon the initial investment required for sophisticated AI-driven sensors and analytical platforms, and the necessity for specialized personnel to manage these systems. Expectations are centered on AI reducing material waste, predicting potential foundation failures early, and significantly speeding up the design-to-installation cycle, ultimately lowering overall project costs and minimizing environmental impact through optimized resource utilization.

The Steel Pipe Piles Market is shaped by a powerful confluence of Driving forces, Restraints, and Opportunities (DRO), which collectively dictate market trajectory and investment appeal. Key drivers include expansive global infrastructure initiatives, particularly in emerging economies focused on rapid urbanization and transportation connectivity, alongside the critical demand generated by the offshore energy sector. Restraints primarily involve the volatile pricing of raw steel materials and the inherent complexities of deep foundation construction, often necessitating specialized, expensive equipment and facing stringent environmental permitting processes. Opportunities lie significantly within the adoption of advanced steel alloys offering lighter weight and higher strength, and the application of innovative corrosion protection technologies extending asset lifespan, especially in hostile marine or chemically aggressive soil conditions. These factors create powerful impact forces that influence procurement decisions and technological development within the sector.

The impact forces influencing the market are multifaceted, encompassing macroeconomic stability, regulatory shifts, and technological advancements. Regulatory impacts are particularly strong, as mandates for seismic resistance and sustainable construction practices often favor high-integrity materials like steel pipe piles. Economically, the market is highly sensitive to interest rate fluctuations and government capital expenditure cycles; infrastructure spending directly correlates with market revenue. Technologically, the push towards automated welding techniques, faster installation methods (e.g., vibrating hammers), and robust non-destructive testing (NDT) methodologies exert pressure on manufacturers to continuously innovate and enhance product reliability and installation efficiency. Furthermore, the competitive impact force from alternative deep foundation methods, such as concrete bored piles, compels continuous price and performance optimization for steel solutions.

The balance between high infrastructure demand (Driver) and the challenge of material cost volatility (Restraint) defines the operational environment for key market players. Exploiting the shift towards sustainable engineering and renewable energy infrastructure (Opportunity) is crucial for long-term growth. The increasing complexity of foundation requirements, especially for structures built on marginal lands or in deep water, reinforces the high-performance attributes of steel pipe piles, mitigating the restrictive forces. Successfully managing the external impact forces—such as ensuring a resilient supply chain in the face of global trade tensions—is paramount for companies seeking to capitalize on the sustained global need for reliable deep foundations.

The Steel Pipe Piles Market segmentation provides a granular view of demand distribution across various dimensions including Material, Type, Application, and End-Use Sector. This structure enables stakeholders to identify high-growth niches and tailor their product offerings to specific project requirements, ranging from small diameter utility foundation supports to massive monopiles for offshore wind farms. The material segment is defined by the steel grade and coating applied, directly influencing the pile's strength and corrosion resistance, which are crucial factors in determining project longevity and maintenance costs. The Type segmentation distinguishes between open-ended and closed-ended configurations, reflecting different installation methods and soil conditions, where open-ended piles are often preferred for driving through cohesive soils and rock, while closed-ended piles are suitable for minimizing soil disturbance and utilizing a concrete plug.

Application analysis highlights the dominant role of civil infrastructure, where steel pipe piles provide critical support for bridges, elevated highways, and retaining structures. The Marine and Ports segment is particularly dynamic, driven by global logistics requirements and the expansion of maritime trade routes, necessitating robust foundations for jetties, piers, and breakwaters. Furthermore, the burgeoning demand from the renewable energy sector, specifically for offshore wind turbine foundations, has introduced requirements for extremely large diameter and high-specification steel pipes, creating a premium market sub-segment. Understanding these application nuances is key for predicting localized demand surges and adapting manufacturing capabilities accordingly.

End-Use segmentation categorizes buyers into sectors such as Civil Engineering Contractors, Oil & Gas Operators, and Power Generation entities. Civil contractors remain the largest consumer base, involved in the vast majority of government-led infrastructure projects. However, the Oil & Gas sector, requiring foundations for complex platforms, terminals, and pipelines, demands specialized, often coated, corrosion-resistant pipes. The Power Generation sector's shift towards offshore wind and coastal power plants ensures consistent, high-specification demand, requiring piles capable of resisting dynamic loads and severe environmental exposure over long operational lifetimes. This detailed segmentation aids market participants in resource allocation and strategic market penetration.

The value chain for the Steel Pipe Piles Market begins with upstream activities, centered on the sourcing and processing of raw steel, specifically iron ore, coking coal, and scrap metal, which feed into steel mills specializing in plate and coil production. This stage is dominated by large, integrated steel manufacturers whose operational efficiency and capacity utilization directly impact the base cost of pipe piles. Quality control and the selection of specialized steel grades (e.g., high-tensile strength alloys) are critical upstream inputs that dictate the performance characteristics of the final product. Volatility in global commodity prices at this stage introduces significant cost risks downstream, necessitating robust hedging strategies among pipe manufacturers.

The midstream phase involves the specialized fabrication of the steel plates into tubular sections, typically through electric resistance welding (ERW), seamless rolling, or spiral welding processes, followed by cutting, splicing, and coating application. Pipe pile manufacturers often engage in custom fabrication to meet specific project demands regarding length, diameter, and wall thickness. Distribution channels are complex, involving both direct sales to major foundation contractors and indirect channels utilizing large civil engineering supply houses or specialized construction material distributors. Direct sales are prevalent for large-scale infrastructure and offshore projects requiring extensive technical consultation and specialized logistics planning, whereas indirect channels support smaller to mid-sized commercial projects.

Downstream activities focus on the installation and utilization of the piles. This involves geotechnical engineers, foundation contractors, and heavy equipment providers specializing in pile driving or drilling techniques. The integration of digital tools, such as real-time monitoring and advanced planning software, optimizes installation efficiency and minimizes risk. End-users, including government agencies (for public works) and private developers (for commercial projects), derive value from the long-term structural integrity and stability provided by the steel pipe foundations. The market dynamics are highly influenced by the relationship between steel manufacturers and large-scale EPC (Engineering, Procurement, and Construction) firms, who serve as the critical nexus connecting supply and final installation.

The primary customers for steel pipe piles are entities engaged in large-scale construction and infrastructure development where deep, reliable foundations are mandatory. The largest segment of buyers comprises major Civil Engineering and General Construction Contractors specializing in complex foundation work. These customers purchase piles in bulk for projects such as the construction of bridges, elevated roadways, mass transit systems, and large public works. Their purchasing decisions are driven by factors including material cost, delivery timelines, ease of handling, and adherence to rigorous quality and safety standards mandated by project owners and governmental bodies.

Another significant customer base includes specialized operators within the Marine and Offshore industries, such as Port Authorities, Offshore Wind Farm Developers, and Oil & Gas Exploration companies. These entities require steel pipe piles, often of very large diameters and with specialized anti-corrosion treatments, to withstand extreme environmental conditions inherent to marine and subsea installations. For instance, offshore wind farm developers are heavy consumers of large monopiles and jacket foundations, which require high-grade, heavy-wall steel pipes capable of resisting immense cyclic loading over several decades. Performance specifications and verifiable structural integrity are often prioritized over marginal cost savings in these high-stakes applications.

Furthermore, major industrial and utility companies represent a steady stream of demand. This includes power generation entities building new power stations or upgrading transmission infrastructure, as well as large manufacturing corporations constructing heavy industrial facilities and warehouses that require robust foundations to support substantial static and dynamic equipment loads. Potential customers consistently seek solutions that offer high load-bearing capacity, resilience in difficult soil conditions, and minimal installation disruption, reinforcing the appeal of standardized and easily installed steel pipe piling systems.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $5.1 Billion |

| Market Forecast in 2033 | $7.6 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ArcelorMittal, Nippon Steel Corporation, JFE Steel Corporation, EVRAZ plc, Tenaris S.A., TMK Group, VALLOUREC, Trinity Industries Inc., Sutor Group, Nucor Corporation, Zekelman Industries, Atlas Tube (Zekelman), Piling Products Ltd., ESC Steel Structures, Bauer Spezialtiefbau GmbH, Junttan Oy, L.B. Foster Company, SSAB AB, United Steel & Pipe Inc., PilePro Piling Products. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape in the Steel Pipe Piles Market is defined by continuous improvements in material science, fabrication processes, and installation techniques designed to enhance structural performance, durability, and cost-effectiveness. In fabrication, advanced welding technologies such as submerged arc welding (SAW) and high-frequency induction (HFI) welding are standard, ensuring seamless joints and structural integrity, especially for large-diameter offshore piles subject to extreme loads. Furthermore, the development and application of higher-strength, low-alloy (HSLA) steel grades are pivotal, allowing engineers to reduce the necessary wall thickness while maintaining or exceeding load-bearing capacity. This material optimization translates directly into reduced material costs and decreased weight per linear foot, simplifying transportation and handling on complex construction sites and reducing carbon footprint associated with steel production.

Installation technology represents another major area of innovation. Traditional impact hammers are increasingly being supplemented or replaced by hydraulic vibratory hammers and resonant driving systems. These newer systems offer significant advantages in speed, noise reduction, and reduced risk of pile damage, particularly crucial in urban or environmentally sensitive areas. Furthermore, advanced instrumentation technology is now routinely integrated into the driving process; sensors provide real-time data on driving resistance, hammer energy, and pile set, allowing engineers to verify bearing capacity instantly using methods like the Pile Driving Analyzer (PDA). This digitalization of the installation process ensures higher quality assurance and reduces the need for extensive post-installation testing.

A critical technological segment revolves around corrosion mitigation and long-term durability. High-performance protective coatings, including fusion-bonded epoxy (FBE), specialized polyurethanes, and even cementitious infills, are crucial, particularly for marine and coastal applications where the steel is exposed to corrosive saline environments and tidal zones. Cathodic protection systems, often utilized in conjunction with protective coatings, provide an additional layer of defense against corrosion, extending the operational lifespan of the foundation structures to meet demanding 50-to-100-year design life requirements common in modern infrastructure projects. Ongoing research is focused on smart coatings that self-heal or provide early warnings of compromised integrity, further solidifying the long-term reliability of steel pipe foundations.

The primary driver is global government expenditure on critical infrastructure projects, particularly the construction and refurbishment of bridges, highways, and marine facilities. Furthermore, the increasing global investment in offshore wind energy development necessitates robust, large-diameter steel pipe foundations, significantly boosting high-specification demand.

Open-ended pipe piles are typically preferred in dense soils and rock layers as they allow soil displacement through the center, reducing driving resistance and material usage. Closed-ended piles, featuring a conical shoe, displace soil laterally and are ideal for minimizing soil disturbance and utilizing the pile as a permanent form for concrete filling, maximizing end-bearing capacity.

Key challenges include managing noise and vibration impacts in urban settings, ensuring proper alignment in deep or deviated driving conditions, and mitigating potential corrosion, especially in aggressive marine or acidic soil environments. Solutions involve utilizing modern vibratory hammers, integrating real-time monitoring systems, and applying specialized coatings and cathodic protection.

Asia Pacific (APAC) currently holds the largest market share due to unparalleled infrastructure development, rapid urbanization, and extensive port capacity expansion projects in major economies such as China, India, and Southeast Asian nations. APAC is expected to maintain its leadership through the forecast period.

HSLA steel allows for the fabrication of piles with thinner wall thicknesses while maintaining superior load-bearing capacity and resilience. This material optimization reduces weight, lowers material costs, and simplifies logistics, making HSLA steel crucial for complex, high-demand projects like deep-water foundations where structural integrity and weight savings are paramount.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.