ID : MRU_ 435937 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

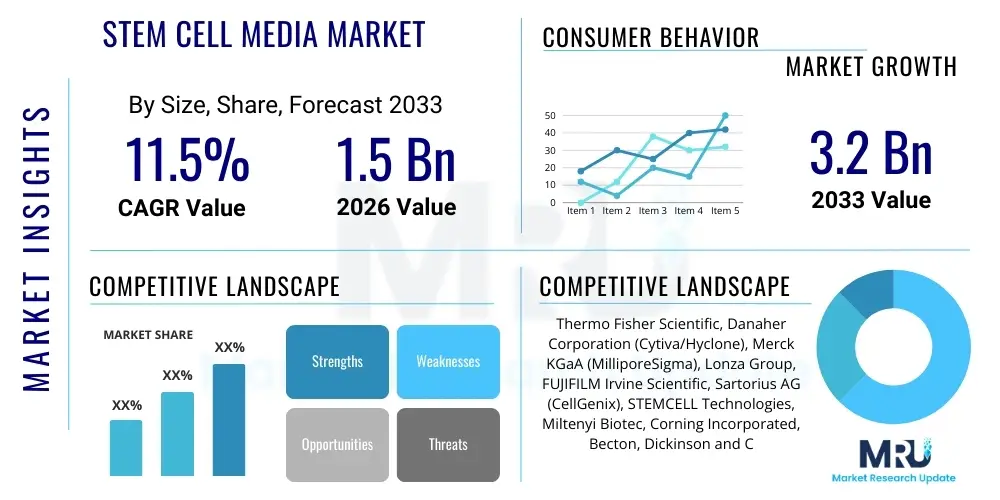

The Stem Cell Media Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2026 and 2033. The market is estimated at USD 1.5 Billion in 2026 and is projected to reach USD 3.2 Billion by the end of the forecast period in 2033.

The Stem Cell Media Market comprises specialized nutrient formulations essential for the in vitro cultivation, maintenance, proliferation, and controlled differentiation of various stem cell populations, including induced pluripotent stem cells (iPSCs), embryonic stem cells (ESCs), and mesenchymal stem cells (MSCs). These complex biological solutions provide the necessary physiological cues, growth factors, vitamins, and minerals required to mimic the natural cellular environment, ensuring cell viability and directed lineage commitment, which are critical for both fundamental research and clinical translation in regenerative medicine. The market is primarily driven by the exponential growth in cell and gene therapy clinical trials, demanding high volumes of clinical-grade, chemically defined, and xeno-free media to minimize variability and comply with stringent regulatory standards. Major applications lie in drug discovery screening, disease modeling, toxicology testing, and large-scale therapeutic manufacturing.

The Stem Cell Media Market is characterized by a strong shift toward defined and xeno-free formulations, reflecting heightened regulatory scrutiny and the industry's focus on clinical safety and reproducibility. Business trends indicate aggressive mergers and acquisitions (M&A) among established life science tool providers to capture specialized media technologies, alongside significant investment in automation and large-scale bioreactor technologies which mandate highly optimized media performance. Regionally, North America maintains market dominance due to robust biotechnology infrastructure and heavy R&D expenditure, while the Asia Pacific region is poised for the fastest growth, fueled by government initiatives promoting stem cell research and establishing localized cell therapy manufacturing hubs. Segment trends highlight the increasing prominence of induced Pluripotent Stem Cell (iPSC) media, given their versatility in personalized medicine, and a strong commercial preference for custom media formulations tailored specifically for high-efficiency clinical manufacturing processes under Good Manufacturing Practice (GMP) guidelines.

Common user questions regarding AI's influence in the Stem Cell Media Market focus on its ability to rapidly optimize complex, multi-component formulations, reduce the labor involved in traditional empirical testing, and predict optimal conditions for large-scale cell expansion. Users frequently inquire about the integration of AI platforms with high-throughput screening and automated bioprocessing systems. The key theme is the expectation that AI and Machine Learning (ML) will transition media development from a trial-and-error process to a precise, data-driven design strategy, significantly accelerating the discovery of novel, high-performance growth factors and reducing the overall cost and variability associated with therapeutic cell production. This predictive capability is seen as essential for scaling cell therapy manufacturing globally.

The market dynamics are primarily propelled by robust investment in regenerative medicine research, the expanding number of FDA-approved and late-stage clinical trials utilizing stem cells, and the crucial regulatory requirement demanding defined, xeno-free media for clinical applications to ensure patient safety and manufacturing consistency. Restraints include the high capital investment required for developing and validating clinical-grade media, supply chain vulnerabilities for specialized, proprietary components, and the inherent biological complexity of optimizing media for diverse and sensitive stem cell types. Opportunities are centered on developing highly specialized, low-cost, and scalable synthetic media substitutes, penetrating emerging Asian markets with increasing cell therapy infrastructure, and leveraging advanced manufacturing technologies like continuous bioprocessing which necessitate novel, high-concentration media formulations. The primary impact forces revolve around rapid technological substitution (moving from serum-containing to defined media) and intensive regulatory harmonization globally.

The Stem Cell Media Market is highly diversified, segmented across various parameters including product type, application, cell source, and end-user. Understanding these segments is crucial for strategic market positioning, as performance requirements vary significantly between academic research and clinical manufacturing. The shift towards proprietary, defined formulations drives high-value sales in the Product Type segment, while regenerative medicine and therapeutic manufacturing dominate the Application landscape due to the sheer volume requirements and premium pricing associated with clinical-grade products. Induced Pluripotent Stem Cells (iPSCs) are rapidly gaining market share within the Cell Source segment, reflecting their promise in personalized medicine and disease modeling, creating a high demand for specific iPSC maintenance and differentiation kits.

The value chain for stem cell media is complex, beginning with the upstream sourcing and manufacturing of highly specialized raw materials, primarily recombinant proteins, growth factors, proprietary peptides, and high-purity basal salts. Upstream analysis reveals intense reliance on a few key suppliers for high-grade, GMP-compliant components, leading to potential supply chain bottlenecks and high input costs. Specialized media manufacturers then formulate, test, and package these components, adhering to rigorous quality standards and often providing proprietary protocols. Distribution channels involve both direct sales, particularly for large clinical-stage clients who require custom logistics and technical support, and indirect sales through specialized global and regional distributors who handle logistics for academic and smaller research institutions. Downstream activities involve end-user consumption in high-throughput research laboratories and large-scale biomanufacturing facilities, where performance, scalability, and technical support dictate procurement decisions. Direct engagement allows manufacturers to gather crucial feedback for iterative product improvement and optimization for bioprocessing needs.

The primary consumers and buyers of stem cell media are institutions heavily invested in cell biology and translational research. Pharmaceutical and biotechnology companies are the largest segment, driven by their extensive pipelines in cell and gene therapy manufacturing, requiring high-volume, GMP-grade media for clinical trials and commercial production. Academic and government-funded research institutes constitute another major customer base, focusing on fundamental research, disease mechanism elucidation, and early-stage drug screening. Additionally, specialized contract research organizations (CROs) and Contract Development and Manufacturing Organizations (CDMOs) represent rapidly growing buyers, as they manage the outsourced production and testing of cell therapies for their clients. Cell banks and tissue engineering centers also depend on standardized media for long-term storage and expansion protocols.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 3.2 Billion |

| Growth Rate | 11.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Thermo Fisher Scientific, Danaher Corporation (Cytiva/Hyclone), Merck KGaA (MilliporeSigma), Lonza Group, FUJIFILM Irvine Scientific, Sartorius AG (CellGenix), STEMCELL Technologies, Miltenyi Biotec, Corning Incorporated, Becton, Dickinson and Company (BD), Bio-Rad Laboratories, Takara Bio, PromoCell GmbH, General Electric (GE Healthcare), R&D Systems (Bio-Techne), ATCC, Cell Applications Inc., PeproTech (Bio-Techne), Sino Biological, HiMedia Laboratories. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The key technological advancements shaping the stem cell media market revolve around the move toward chemically defined, xeno-free, and animal-component-free (ACF) formulations. These media minimize safety risks, reduce immunological complications in therapeutic applications, and ensure regulatory compliance necessary for GMP manufacturing. Significant research is being dedicated to developing novel synthetic matrices and hydrogels that can be integrated into the media, providing three-dimensional culture environments that enhance cell functionality and expansion yield, particularly for complex tissues like organoids and spheroids. High-throughput screening (HTS) coupled with automated liquid handling systems is now standard for rapidly testing thousands of media component combinations, dramatically accelerating the optimization process. Furthermore, microfluidic technology is emerging as a critical tool for developing patient-specific media and conducting small-volume, highly controlled differentiation experiments, paving the way for personalized regenerative medicine protocols.

The global Stem Cell Media market exhibits significant regional variation in terms of adoption rates, research intensity, and regulatory environment. North America currently holds the largest market share, predominantly driven by the United States. This dominance is attributed to substantial government and private sector funding directed towards life sciences research, the presence of major pharmaceutical and biotechnology hubs, and a well-established regulatory pathway (FDA) that encourages the commercialization of cell and gene therapies. High adoption rates of advanced bioprocessing technologies and the concentration of key market players who pioneer defined media formulations further solidify this region's leadership. The stringent demand for GMP compliance in clinical manufacturing in the US ensures continued high-value consumption of premium, clinical-grade media.

Europe represents the second-largest market, characterized by strong academic research output, significant investments through organizations like the European Medicines Agency (EMA), and established consortia focused on regenerative medicine translation. Key countries such as Germany, the UK, and France are driving demand through clinical trials, particularly those involving CAR T-cell therapies and neurological disorder research. European regulatory focus often emphasizes ethical sourcing and xeno-free media, leading to early adoption of defined formulations. However, fragmentation across national healthcare systems presents certain challenges in rapid commercial scaling compared to the highly centralized North American market.

Asia Pacific (APAC) is projected to be the fastest-growing region during the forecast period. This rapid expansion is fueled by increasing government initiatives in China, South Korea, and Japan to establish domestic cell therapy manufacturing capabilities and dedicated regenerative medicine research parks. Growing healthcare expenditure, the establishment of favorable regulatory frameworks (e.g., Japan's expedited approval system for regenerative therapies), and a rising patient population needing advanced treatments are accelerating market penetration. Localized media manufacturing and strategic collaborations between international market leaders and regional academic institutions are defining the competitive landscape in APAC, targeting high-volume production at competitive pricing points.

Classical media typically contain fetal bovine serum (FBS), introducing high variability and contamination risks. Defined media are formulated using precise, known concentrations of synthetic components, eliminating animal-derived products (xeno-free) to ensure batch consistency and meet strict clinical regulatory standards (GMP).

Xeno-free media eliminates the risk of introducing animal pathogens and immunogenic components (such as non-human sialic acids) into therapeutic products. This regulatory necessity enhances patient safety, reduces variability, and simplifies the path to global regulatory approvals for commercial-scale cell therapies.

The Mesenchymal Stem Cell (MSC) media segment currently holds significant revenue due to the high volume of ongoing clinical trials utilizing MSCs for immunomodulation and regenerative repair. However, the Induced Pluripotent Stem Cell (iPSC) segment is projected to exhibit the fastest growth rate.

Automation, particularly high-throughput screening and robotics, allows researchers to test complex media formulations rapidly and systematically, identifying optimal components. This speeds up product development and ensures the scalability and quality control necessary for advanced biomanufacturing.

The Asia Pacific (APAC) region, specifically driven by countries like China and Japan, is forecasted to show the highest Compound Annual Growth Rate (CAGR) due to significant national investments in establishing domestic regenerative medicine infrastructure and expanding clinical research capabilities.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.