ID : MRU_ 433747 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

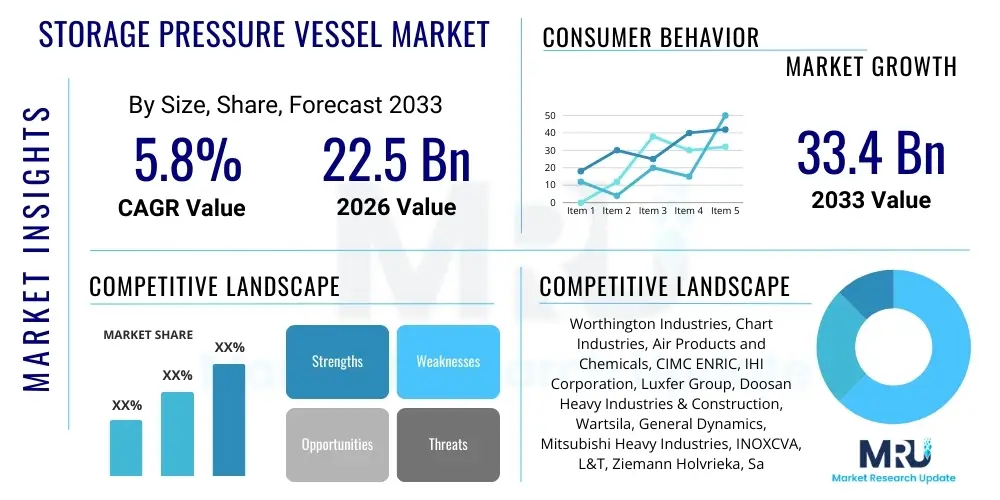

The Storage Pressure Vessel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 22.5 Billion in 2026 and is projected to reach USD 33.4 Billion by the end of the forecast period in 2033.

Storage pressure vessels are enclosed containers designed to hold gases or liquids at a pressure substantially different from the ambient pressure. These critical components are foundational to various industrial processes, including energy production, chemical synthesis, and infrastructural development. The market encompasses a wide range of vessels categorized by material (steel, composite), type (boilers, reactors, separators, storage tanks), and operational parameters (high pressure, low temperature). The robust design and manufacturing adherence to rigorous international safety standards, such as those set by ASME (American Society of Mechanical Engineers) and PED (Pressure Equipment Directive), ensure reliability and operational safety across demanding environments.

The core function of these vessels involves safe containment and transportation of hazardous or high-value materials, which drives their indispensable role in sectors like Oil and Gas, where they are used for refining and processing hydrocarbons; in the Chemical industry for reaction processes; and in Power Generation, particularly in nuclear and thermal plants. Furthermore, the burgeoning demand for cleaner energy sources, such as Liquefied Natural Gas (LNG) and hydrogen, is rapidly expanding the application scope for specialized cryogenic and high-pressure storage solutions. The fundamental benefits these vessels offer—enhanced safety, efficiency in material handling, and process optimization—cement their essential contribution to global industrial infrastructure.

Driving factors propelling market expansion include the sustained growth in energy consumption, necessitating increased storage capacity for fuels and raw materials, and significant investments in downstream chemical processing facilities, particularly across developing economies in the Asia Pacific region. Regulatory mandates emphasizing operational safety and emission control also compel industries to upgrade to newer, more resilient vessel technologies. The transition toward renewable energy and the associated need for advanced energy storage mediums, such as hydrogen fuel cells and large-scale battery components that often utilize pressure vessels for thermal management, further catalyze market growth.

The global Storage Pressure Vessel Market is characterized by steady expansion driven by massive capital expenditure in the petrochemical sector and the accelerating global energy transition. Business trends highlight a strong focus on lightweight composite materials for transportation applications (Type IV vessels) and digital transformation initiatives, including the integration of IoT sensors for predictive maintenance and enhanced safety monitoring. The competitive landscape remains moderately consolidated, dominated by manufacturers capable of adhering to highly stringent international codes and offering customized, high-specification products tailored for extreme operating conditions prevalent in deep-sea exploration and ultra-high-pressure chemical synthesis. Strategic mergers and acquisitions aimed at integrating advanced manufacturing technologies and expanding geographic footprint, particularly into regions with rapid infrastructure development, are defining commercial strategies.

Regionally, Asia Pacific maintains its dominance as the fastest-growing market, largely due to unprecedented industrialization, urbanization, and state-backed infrastructure projects in China, India, and Southeast Asian nations, particularly focusing on LNG terminals and refinery expansions. North America and Europe, while mature, exhibit high demand for replacement vessels and advanced materials used in carbon capture utilization and storage (CCUS) projects and green hydrogen production facilities. These regions prioritize innovation in material science and digitalization to enhance operational efficiency and regulatory compliance, whereas Latin America and MEA are experiencing growth fueled by new exploration activities and developing gas infrastructure.

Segment-wise, the high-pressure segment, particularly vessels operating above 100 bar, is experiencing significant growth, fueled by hydrogen mobility and advanced petrochemical processes. Material trends indicate a shift toward specialized alloys and composite materials (FRP/GRP) offering superior corrosion resistance and weight reduction compared to traditional carbon steel. Furthermore, the application segment of oil and gas continues to hold the largest market share, but the emerging application of new energy storage (including thermal energy storage and cryogenics for hydrogen) is poised to register the highest Compound Annual Growth Rate over the forecast period, reflecting global efforts to decarbonize energy systems.

Common user questions regarding AI's influence on the Storage Pressure Vessel Market frequently revolve around how artificial intelligence can enhance structural integrity monitoring, optimize manufacturing processes, and improve compliance with complex regulatory standards. Key concerns focus on the potential for AI-driven predictive maintenance to reduce catastrophic failures, questions about the integration cost of complex sensing systems, and the ability of machine learning models to accurately interpret non-destructive testing (NDT) data for defect detection. Users are also keen to understand how AI can optimize the design phase, particularly in topology optimization for complex geometries and stress simulation under varied operational loads, thereby minimizing material usage while maximizing safety margins. The overriding expectation is that AI will transition the industry from reactive or scheduled maintenance toward truly predictive, condition-based asset management, leading to significant reductions in downtime and operational expenditure.

The adoption of AI and machine learning algorithms is fundamentally transforming the lifecycle management of storage pressure vessels. In manufacturing, AI optimizes welding processes by analyzing real-time sensor data, adjusting parameters to ensure weld quality and reducing human error, leading to higher throughput and reduced rework rates. For operational assets, AI leverages data collected from integrated IoT sensors (measuring temperature, pressure, strain, and acoustic emissions) to build sophisticated predictive models. These models calculate the remaining useful life (RUL) of the vessel components, identifying potential degradation mechanisms like stress corrosion cracking or fatigue propagation long before they reach critical levels, thereby enabling precise, timely intervention and maximizing asset utilization.

Furthermore, AI is crucial in navigating the complex regulatory landscape. Machine learning models can be trained on vast datasets of compliance codes (ASME, API, ISO) and historical inspection records to automate the generation of compliance documentation and flag potential design or operational deviations. This automation significantly reduces administrative overhead and ensures higher levels of audit readiness. In the design phase, generative AI tools are beginning to assist engineers by proposing novel, safe, and materially efficient designs that human engineers might overlook, especially for highly customized vessels used in niche applications such as aerospace or highly corrosive environments. This synergistic approach between AI and engineering expertise is accelerating innovation in high-integrity vessel construction.

The Storage Pressure Vessel Market is primarily driven by escalating global energy demand and the corresponding expansion of oil, gas, and chemical infrastructure, particularly in fast-industrializing nations. Simultaneously, the global commitment to sustainable energy necessitates substantial investments in new vessel types, specifically cryogenic tanks for LNG and high-pressure tanks for hydrogen storage, creating a robust opportunity pathway. However, the market faces significant restraints, including the inherent high capital expenditure associated with custom-built, high-specification vessels and the intense volatility of essential raw material prices, such as nickel, chrome, and specialty steels, which directly impact manufacturing costs and project timelines. These dynamic forces—Drivers, Restraints, and Opportunities (DRO)—collectively define the market's trajectory, while external impact forces like stringent safety regulations and technological advancements shape the operational environment and competitiveness.

Key drivers include the global expansion of refining and petrochemical capacities, where pressure vessels are integral to distillation, separation, and reaction processes. Furthermore, infrastructural development in pipelines and storage terminals necessitates standardized vessels for intermediate storage. The shift towards cleaner fuels is a potent driver; the surge in global liquefied natural gas (LNG) trade demands advanced cryogenic storage and transportation vessels, while the rapidly developing hydrogen economy requires entirely new classes of Type III and Type IV composite pressure vessels capable of withstanding extreme pressures (700 bar and above). The replacement cycle for aging infrastructure in mature economies, often mandated by stricter safety codes, also provides a stable source of demand.

Restraints center on the formidable entry barriers created by the need for specialized certification and adherence to complex international standards (e.g., ASME Section VIII, EN 13445), which restrict competition to highly capitalized and experienced manufacturers. The customization inherent in large-scale vessel manufacturing often leads to long lead times, which can delay major infrastructure projects. Furthermore, opportunities are substantial in emerging technologies, particularly Carbon Capture, Utilization, and Storage (CCUS), which requires large, high-integrity vessels for CO2 capture and sequestration. Modular vessel construction, driven by the desire for rapid deployment and cost efficiency in remote locations, also presents a significant growth avenue. The principal impact forces involve constantly evolving material science breakthroughs, increasing the performance envelopes of vessels, and the overwhelming regulatory pressure focusing on mandatory integrity management and risk-based inspection methodologies to minimize environmental and safety hazards.

Drivers:

Restraints:

Opportunities:

Impact Forces:

The Storage Pressure Vessel Market is systematically segmented based on Type, Material, Application, and Operating Parameters (Pressure and Temperature). This segmentation provides a granular view of market dynamics, revealing specific demand pockets driven by technological requirements and end-user needs. By Type, the market includes Heat Exchangers, Reactors, Boilers, and Separators, each serving distinct functional roles within industrial processes. The Material segmentation, comprising Carbon Steel, Stainless Steel, Alloy Steels, and Composites, highlights the importance of corrosion resistance and strength requirements dictated by the contained media.

The application segment is dominated by the Oil and Gas and Chemical sectors, reflecting their heavy reliance on high-integrity containment solutions. However, the emerging segments of Power Generation (nuclear and thermal) and new energy sources (hydrogen, LNG) are projected to exhibit the fastest growth trajectory, driven by infrastructure upgrades and clean energy mandates. Furthermore, classification by Operating Pressure—Low, Medium, and High—and Operating Temperature—Cryogenic, Refrigerated, and High-Temperature—is critical, as these parameters define the complexity, design specifications, and manufacturing cost of the final vessel, with high-pressure and cryogenic vessels representing the most technically challenging and lucrative segments.

The value chain for the Storage Pressure Vessel Market begins with the upstream sourcing of specialized raw materials, primarily high-quality steel plates (carbon, stainless, and clad steels) and composite fibers (carbon fiber, fiberglass) from global metal producers and chemical suppliers. This stage is crucial as the integrity and longevity of the final product depend heavily on material specifications and traceability. Key upstream challenges include managing price volatility and securing consistent supply of materials that meet stringent metallurgical standards required for high-pressure and corrosive environments. Strategic partnerships between vessel manufacturers and certified material suppliers are essential to mitigate risks associated with quality and supply chain disruption, ensuring all inputs conform to required design codes like ASME material specifications.

The midstream segment involves the core manufacturing, which includes detailed engineering design, material preparation, forming (rolling, bending), complex welding, and final assembly. This stage is highly specialized, requiring massive fabrication facilities, advanced non-destructive testing (NDT) capabilities, and certified personnel. Regulatory compliance is paramount, with third-party inspections occurring throughout the fabrication process. Distribution channels are typically direct for large, custom-built industrial vessels, often involving significant logistical planning for oversized transportation. However, smaller, standardized vessels (e.g., compressed air tanks) may utilize indirect channels through industrial distributors or engineering procurement and construction (EPC) contractors who integrate the vessels into larger plant projects.

Downstream activities involve installation, commissioning, operation, and maintenance. Given the high-risk nature of the assets, the downstream focus is heavily on integrity management, regular inspections (utilizing advanced NDT techniques), and servicing. Direct sales channels are favored when the manufacturer provides comprehensive after-sales support, including repair, retrofitting, and lifecycle management services. The reliance on EPC firms often means the vessel manufacturer acts as a sub-supplier, with the EPC managing the ultimate relationship with the end-user. The indirect channel complexity ensures the vessel is delivered and integrated seamlessly into highly specific plant layouts, requiring close coordination across multiple engineering disciplines.

The primary end-users and buyers of storage pressure vessels are major industrial entities whose core operations involve chemical reactions, fluid separation, or energy storage under non-ambient conditions. These customers are typically large, multinational corporations engaged in capital-intensive projects where safety, reliability, and regulatory compliance are non-negotiable operational prerequisites. The purchasing decision is heavily influenced by total cost of ownership (TCO), lifespan, and the vendor’s proven track record in meeting specific process design requirements and navigating complex global certification processes. These customers usually procure vessels either directly from specialized fabricators or indirectly through major Engineering, Procurement, and Construction (EPC) companies.

The largest consumer base resides within the Oil and Gas sector, spanning upstream exploration, midstream transport and storage (LNG terminals, pipeline booster stations), and downstream refining and petrochemical operations. These entities require everything from massive reactor vessels and distillation columns to standardized storage tanks and separators. The second major consumer segment is the Chemical industry, covering the production of bulk chemicals, specialty chemicals, and pharmaceuticals, where highly corrosion-resistant materials are mandated for handling aggressive media. Investment cycles in these sectors, driven by global commodity prices and demand projections, dictate the overall market demand for large-scale vessel fabrication.

Emerging key potential customers include utility companies and independent power producers focusing on decarbonization and energy transition projects. This includes operators of nuclear power plants requiring high-integrity containment structures and component housings, as well as companies investing heavily in green hydrogen infrastructure, which demands specialized high-pressure composite tanks. Furthermore, industrial gas suppliers (e.g., oxygen, nitrogen, argon) consistently require cryogenic vessels for storage and transportation. These sophisticated end-users demand rigorous quality assurance, advanced material traceability, and manufacturers capable of providing comprehensive lifecycle support and engineering analysis for highly specialized, often unique, containment challenges.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 22.5 Billion |

| Market Forecast in 2033 | USD 33.4 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Worthington Industries, Chart Industries, Air Products and Chemicals, CIMC ENRIC, IHI Corporation, Luxfer Group, Doosan Heavy Industries & Construction, Wartsila, General Dynamics, Mitsubishi Heavy Industries, INOXCVA, L&T, Ziemann Holvrieka, Samuel Pressure Vessel Group, Steelhead Composites, Tenaris, Bosch, Babcock International. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Storage Pressure Vessel Market is rapidly evolving, driven primarily by the need for enhanced safety, improved efficiency, and adaptation to extreme operating conditions, particularly in the emerging hydrogen and cryogenic sectors. A core technology advancement is the development and increasing adoption of composite pressure vessels (CPVs), especially Type IV vessels, which utilize a plastic liner wrapped in carbon fiber or fiberglass composites. This technology significantly reduces vessel weight compared to traditional steel vessels, making them ideal for mobile applications, such as hydrogen fuel cell vehicles and specialized transportation modules, while maintaining very high-pressure tolerance (up to 700 bar). Furthermore, the manufacturing processes for steel vessels are being optimized through advanced welding techniques like narrow-gap welding and friction stir welding, reducing residual stresses and improving weld integrity, critical for long-term fatigue resistance.

Digital transformation plays a significant role in modern pressure vessel technology. This includes the integration of advanced Non-Destructive Testing (NDT) methods, such as Phased Array Ultrasonic Testing (PAUT) and Acoustic Emission Testing (AET), which provide highly detailed, real-time assessments of material integrity both during fabrication and throughout the vessel’s operational life. Coupled with this is the deployment of Industrial Internet of Things (IIoT) sensors directly embedded into or attached to the vessel structure. These sensors monitor key operational parameters—temperature gradients, strain, vibration, and corrosion indicators—transmitting data to a centralized digital twin model. This digital representation allows operators to run simulations and conduct risk-based inspection (RBI) planning more accurately and frequently than traditional scheduled shutdowns, maximizing asset uptime and reducing the likelihood of catastrophic failure.

Finally, material science breakthroughs continue to push the boundaries of performance. High-strength, corrosion-resistant exotic alloys, such as duplex and super duplex stainless steels, are increasingly used in highly corrosive environments prevalent in the chemical processing and acidic gas handling sectors, offering superior resistance to stress corrosion cracking. For high-temperature applications, advanced high-nickel alloys provide structural stability and creep resistance. Innovation is also focused on the cladding and lining processes, where thin layers of expensive, corrosion-resistant materials (like titanium or Hastelloy) are metallurgically bonded to cheaper carbon steel base materials, providing a cost-effective solution for handling aggressive media while maintaining structural integrity. The combination of advanced materials, smart monitoring, and optimized manufacturing processes defines the competitive edge in the contemporary storage pressure vessel industry.

The geographical distribution of the Storage Pressure Vessel Market reflects global industrial maturity and energy investment trends. Asia Pacific (APAC) currently holds the dominant market share and is expected to register the highest growth rate during the forecast period. This growth is intrinsically linked to massive urbanization, infrastructural expansion, and state-led initiatives in key economies like China and India, focusing heavily on building new chemical plants, expanding refinery capacity, and developing LNG import terminals. Regulatory environments are evolving rapidly, catching up with Western standards, which concurrently drives demand for higher quality, certified vessels. The strategic positioning of APAC as the global manufacturing hub further solidifies its dominance, attracting significant foreign direct investment into new industrial projects requiring substantial pressure containment infrastructure.

North America and Europe represent mature, high-value markets characterized by stringent safety regulations and a high replacement rate for aging infrastructure. In North America, demand is sustained by the revitalization of the petrochemical sector, fueled by abundant shale gas resources, and significant investment in new pipeline and midstream compression stations, all requiring robust pressure vessels and associated components. Europe, driven by its ambitious decarbonization goals, is witnessing a concentrated surge in demand for vessels specifically designed for emerging clean energy applications, including specialized components for green hydrogen production (electrolyzers, storage) and advanced thermal energy storage systems linked to renewable power generation. The emphasis in these regions is less on volume expansion and more on technological sophistication, materials innovation, and digital lifecycle management.

The Middle East and Africa (MEA), alongside Latin America (LATAM), represent high-potential growth markets driven by resource exploration and monetization. MEA’s demand is fundamentally linked to large-scale, long-term oil and gas mega-projects, especially those related to gas processing, liquefaction facilities, and petrochemical diversification strategies away from crude oil exports. LATAM, particularly Brazil and Mexico, presents strong opportunities due to upstream offshore oil exploration (e.g., Brazil's pre-salt fields) and necessary upgrades to aging national refinery complexes. While these regions often rely on imported technology and vessels from established manufacturers in the US, Europe, and Asia, increasing local content requirements and burgeoning domestic manufacturing capabilities are gradually reshaping the competitive dynamics, focusing on robust, desert-ready, or offshore-compliant vessels.

The design and manufacturing of industrial pressure vessels are primarily governed by the ASME Boiler and Pressure Vessel Code (BPVC), especially Section VIII, widely used in North America and globally. In Europe, the Pressure Equipment Directive (PED) 2014/68/EU establishes mandatory compliance standards. Other critical codes include API (American Petroleum Institute) standards for oil and gas, and specific ISO standards for material quality and testing protocols.

The green hydrogen economy is catalyzing immense growth in the high-pressure composite vessel segment. Demand is soaring for Type III and Type IV vessels, typically made of carbon fiber, which are capable of storing hydrogen safely at extremely high pressures (up to 700 bar) for use in transportation, refueling stations, and stationary power generation, driving material innovation and specialized fabrication techniques.

Key material trends include the shift toward advanced composites (carbon fiber reinforced polymers) for weight reduction and high-pressure tolerance, particularly in mobility applications. Furthermore, there is increasing utilization of specialized alloys, such as duplex and super duplex stainless steels, to enhance corrosion resistance and lifespan in highly acidic or harsh operating environments, reducing total lifecycle costs.

Digitalization involves integrating Industrial IoT sensors onto vessels to monitor crucial operational parameters (temperature, strain, pressure) in real time. This data feeds into digital twin models, enabling predictive maintenance, optimizing inspection schedules through Risk-Based Inspection (RBI) methodologies, and significantly improving overall asset safety and uptime compared to traditional scheduled inspections.

While the Oil and Gas sector remains the largest application segment by volume, the New Energy and Renewables application segment, specifically associated with Cryogenic Vessels for LNG and high-pressure tanks for hydrogen storage (H2), is projected to exhibit the highest Compound Annual Growth Rate (CAGR) due to global energy transition mandates and substantial government and private sector investment into decarbonization infrastructure.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.