ID : MRU_ 431487 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

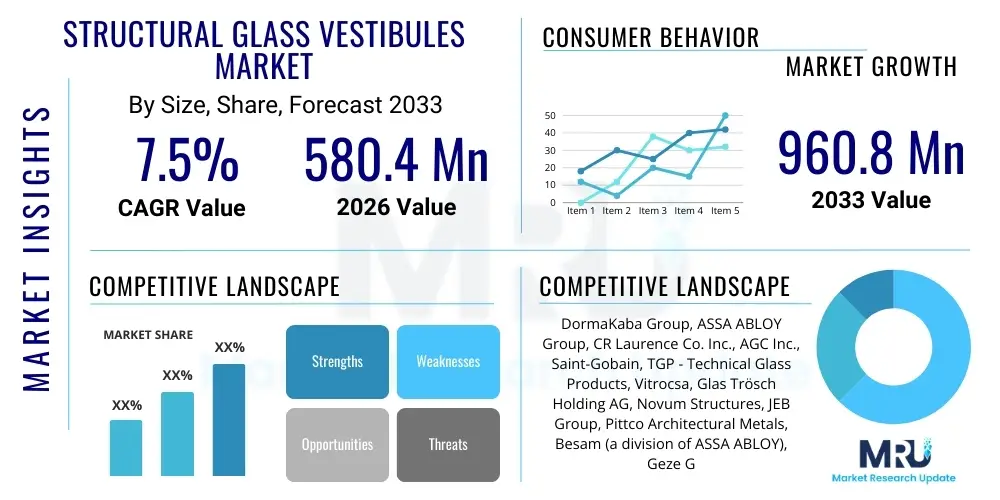

The Structural Glass Vestibules Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2026 and 2033. The market is estimated at $580.4 Million in 2026 and is projected to reach $960.8 Million by the end of the forecast period in 2033.

Structural Glass Vestibules, often referred to as glass entrance systems or airlocks, are specialized architectural enclosures designed to enhance building aesthetics, improve energy efficiency, and provide environmental buffering between the interior and exterior environments. These systems utilize advanced structural glass technology, often incorporating tempered or laminated glass panels supported by minimalist hardware, such as spider fittings or tension rods, rather than traditional frames. The primary product description centers on frameless, high-transparency assemblies that integrate seamlessly with modern building facades, offering maximum daylight penetration and an unobstructed view.

Major applications for structural glass vestibules span across high-traffic commercial and public sectors, including corporate headquarters, luxury retail establishments, high-end residential towers, hospitals, educational institutions, and airports. The core benefit derived from these installations is thermal efficiency; by creating an air lock, vestibules significantly reduce heating and cooling losses caused by pedestrian traffic, thereby lowering operational energy costs. Furthermore, they contribute significantly to architectural prestige and compliance with modern green building standards and accessibility regulations, particularly in regions promoting sustainable construction.

The market is primarily driven by the global trend toward aesthetically pleasing, energy-efficient, and biophilic architectural designs. Increased investment in commercial real estate refurbishment and new construction projects in emerging economies further fuels demand. Key driving factors include stringent building codes mandating energy conservation, technological advancements in glass processing (allowing for greater panel sizes and strength), and the growing preference for minimalist, high-visibility entrance solutions that enhance the user experience and building security profile. The integration of automated sliding or revolving doors within these vestibules also contributes significantly to market growth.

The Structural Glass Vestibules Market is characterized by robust business trends centered on sustainability and automation. Leading market participants are focusing intensely on developing smart vestibule systems that integrate IoT sensors for climate control, traffic flow management, and predictive maintenance. A major business trend involves strategic partnerships between glass manufacturers, architectural firms, and door automation specialists to deliver turnkey solutions for large-scale commercial projects. Furthermore, standardization and modularization of components are enhancing installation efficiency and reducing overall project timelines, appealing particularly to fast-paced construction markets in North America and Asia Pacific.

Regional trends indicate that North America maintains a strong leadership position, driven by significant investment in commercial infrastructure renewal and strict adherence to energy performance standards (such as LEED certification). However, the Asia Pacific region, particularly China and India, is emerging as the fastest-growing market segment, fueled by rapid urbanization, massive infrastructural development, and the increasing adoption of Western architectural styles in high-rise constructions. Europe demonstrates maturity, with a strong emphasis on preservation and renovation projects where historically sensitive designs require high-transparency, minimally invasive structural glass solutions compliant with rigorous EU environmental directives.

Segment trends highlight the dominance of the Frameless Glass Vestibule segment due to its superior aesthetic appeal and compatibility with modern facade requirements. In terms of application, the Corporate and Commercial Office Buildings segment remains the largest consumer, valuing the enhanced corporate image and energy savings provided by structural vestibules. There is also a notable upward trend in the adoption of specialized glass types, such as low-emissivity (Low-E) glass and electrochromic glass, which actively manage solar gain and glare, further driving segment growth and increasing the average unit value within the market.

Common user questions regarding AI's impact on Structural Glass Vestibules typically revolve around optimizing operational efficiency, integration with smart building management systems (BMS), and enhancing security protocols. Users are keen to understand how AI can predict peak traffic times to adjust HVAC settings automatically within the vestibule space, how AI-driven analysis of pedestrian flow can optimize door opening speeds and cycles, and whether AI can detect and flag security anomalies or overcrowding. Key themes summarizing user expectations include achieving predictive maintenance for automated door mechanisms, maximizing energy savings by learning and adapting to micro-climates, and utilizing generative AI tools for accelerated, site-specific structural design and engineering verification, thereby reducing the time and cost associated with complex custom installations.

The Structural Glass Vestibules Market is influenced by strong drivers, including the persistent global focus on energy efficiency in commercial buildings and the architectural shift towards frameless, transparent facades that necessitate high-performance glass structures. However, this growth is restrained by the high initial installation cost compared to conventional framed entry systems and the complexity associated with installing bespoke structural glass assemblies, which requires highly specialized labor. Opportunities lie predominantly in integrating advanced smart technology, such as dynamic shading systems and IoT sensors, and expanding into emerging secondary markets like educational and healthcare facilities seeking aesthetic upgrades and rigorous environmental separation. These dynamics collectively exert a powerful impact force, pushing the market towards premium, technology-enabled offerings while simultaneously creating pressure on manufacturers to rationalize installation costs and complexity to broaden market accessibility.

Drivers contributing significantly to market momentum include the rapidly increasing adoption of green building certifications (e.g., LEED, BREEAM) that specifically reward designs incorporating energy-saving vestibules. Furthermore, aesthetic preferences among leading architects and developers consistently favor the clean, modern look of structural glass, driving demand away from bulky traditional metal frames. Technological advancements in glass lamination and strengthening techniques, such as the use of SentryGlas Plus (SGP) interlayer, allow for safer, larger, and more structurally robust glass panels, alleviating previous concerns about durability and wind load resistance, thus expanding potential applications in high-wind zones and seismically active areas.

Conversely, significant market restraints include the logistical challenges of transporting and handling large, delicate structural glass panels, which contributes substantially to project risk and overall cost. Regulatory hurdles related to fire safety and impact resistance, which vary widely across different municipal jurisdictions, sometimes necessitate extensive custom engineering and certification processes, adding time and expense. The market is also vulnerable to fluctuations in raw material costs, particularly specialized iron-free glass and stainless steel components used in spider fittings, which can impact profitability and pricing stability for end-users, potentially slowing adoption among cost-sensitive clients.

The Structural Glass Vestibules Market is meticulously segmented based on Type, Material, Application, and Operating Mechanism to accurately reflect the diversity of products and end-use environments. The Type segmentation distinguishes between Frameless (dominant due to aesthetic trends) and Semi-Framed systems, based on the degree of visible structural support. Material segmentation is critical, highlighting the use of Tempered Glass (standard safety requirement) versus Laminated Glass (superior safety and structural integrity) and Insulated Glass Units (essential for thermal performance). Application segmentation maps usage across high-value sectors like Corporate Offices and high-volume sectors like Retail & Hospitality. Understanding these segments provides clarity on where capital expenditure is concentrated and guides product development toward specific functional requirements, such as high security in governmental applications or high thermal performance in educational settings.

The value chain for Structural Glass Vestibules begins with upstream activities focused on the procurement and processing of raw materials, primarily high-quality float glass, specialized interlayers (like PVB and SGP), and stainless steel for hardware fittings. Key upstream players include major global glass producers and specialized metal fabrication firms. This stage involves sophisticated processes such as tempering, heat soaking, and lamination to create structural-grade glass panels suitable for exterior architectural use. Efficiency and cost management at this stage are crucial, as raw material consistency and quality directly determine the performance characteristics (e.g., wind load resistance, thermal efficiency) of the final vestibule system, demanding stringent quality control and supply chain reliability from specialized glass fabricators who often operate under tight tolerances.

Midstream activities encompass the actual design, engineering, and manufacturing of the vestibule components, including custom metal brackets, spider fittings, and integration kits for automated door systems. Architectural firms and specialist facade engineering consultants play a vital role here, translating client aesthetic and functional requirements into feasible structural designs. Direct distribution channels often involve the manufacturer selling custom-engineered solutions directly to general contractors or construction management firms, particularly for large, complex commercial projects where tailored installation oversight is mandatory. Indirect channels utilize specialized glazing subcontractors and authorized dealers who handle smaller projects and maintenance services, providing regional accessibility and local expertise in installation and compliance.

Downstream activities center on installation, post-sales service, and maintenance. Installation is highly specialized, typically requiring certified glaziers and structural engineers to ensure proper load transfer and sealing against weather elements. Maintenance contracts, crucial for automated and revolving door components, represent a significant aftermarket revenue stream. Potential customers, or end-users, ultimately influence the demand signal, valuing reliability, energy performance, and aesthetic integration above all else. The successful execution of the value chain relies heavily on seamless coordination between the system supplier (vestibule manufacturer), the installer, and the architectural designer to deliver a fully functional and compliant entrance system that meets the high standards expected in contemporary commercial architecture.

The primary potential customers for Structural Glass Vestibules are developers and owners of high-value commercial properties seeking to enhance operational efficiency, architectural distinctiveness, and tenant appeal. End-users fall broadly into two categories: those undertaking new construction projects, where vestibules are integrated into the initial design specifications, and those involved in retrofitting existing buildings to meet modern energy efficiency standards or aesthetic revitalization goals. Corporate clients, particularly multinational corporations and financial institutions, are significant buyers, viewing these entrances as critical components of their brand image and sustainability commitments. Their procurement decisions prioritize durability, state-of-the-art automation features, and compliance with stringent internal environmental policies, driving demand for premium, custom-engineered solutions.

Another rapidly expanding segment of buyers includes entities managing large-scale public and semi-public infrastructure, such as major international airports, large urban hospitals, university campuses, and significant governmental buildings. For these institutions, the key purchasing drivers are high-volume traffic management, security integration, and extreme resilience against continuous heavy use. Airports, for instance, require vestibules designed for heavy baggage traffic and immediate integration with sophisticated security screening and climate control systems. This segment demands robust, low-maintenance designs, often favoring revolving door vestibules for optimized thermal separation and constant traffic flow management, highlighting the diversity in specific functional requirements among major end-user groups.

Furthermore, the high-end retail and luxury hospitality sectors represent lucrative, albeit often niche, potential customer groups. Luxury hotel chains and flagship retail stores leverage structural glass vestibules not just for energy saving, but as crucial elements of their experiential design philosophy, utilizing them to create a dramatic, transparent, and welcoming entrance that aligns with their brand identity. In these contexts, aesthetic quality, seamless integration with surrounding facade materials, and flawless operation of automatic mechanisms are paramount. Architects acting on behalf of these clients are instrumental in specifying the systems, making the cultivation of relationships with influential design firms a critical strategic priority for vestibule manufacturers seeking access to these premium market opportunities.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $580.4 Million |

| Market Forecast in 2033 | $960.8 Million |

| Growth Rate | 7.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | DormaKaba Group, ASSA ABLOY Group, CR Laurence Co. Inc., AGC Inc., Saint-Gobain, TGP - Technical Glass Products, Vitrocsa, Glas Trösch Holding AG, Novum Structures, JEB Group, Pittco Architectural Metals, Besam (a division of ASSA ABLOY), Geze GmbH, Horton Automatics, Record-USA, Boon Edam, Tormax, Stanek Windows, Oldcastle BuildingEnvelope, Scheldebouw (Permasteelisa Group) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Structural Glass Vestibules Market is defined by innovations primarily focused on enhancing safety, thermal performance, and user interaction. A critical advancement involves the use of structural interlayers, notably SentryGlas Plus (SGP), which provides five times the tear strength and 100 times the rigidity of conventional PVB interlayers. This technological shift allows architects to design significantly larger, heavier, and more robust frameless panels while maintaining extremely high levels of transparency and meeting stringent structural requirements against high wind loads and potential impact events. Furthermore, the increasing sophistication of insulated glass units (IGUs) incorporating low-emissivity (Low-E) coatings and argon or krypton gas fills is foundational to meeting modern energy efficiency targets, ensuring that the transparent vestibule structure does not become a thermal liability for the building.

Automation technology forms another cornerstone of the market's innovation trajectory. Key technologies include advanced sensor systems, such as LiDAR and infrared detectors, integrated into automated sliding and revolving doors, ensuring rapid, safe, and efficient pedestrian throughput while minimizing air infiltration. These sensors are increasingly linked to proprietary control units that learn traffic patterns and optimize door speed and opening duration, a precursor to full AI integration. Additionally, the adoption of electrochromic and thermochromic glass technologies is gaining traction. Electrochromic glass allows the tint level of the glass panels to be electronically adjusted, dynamically controlling solar heat gain and glare without the need for physical blinds, providing superior comfort and energy management within the vestibule space, though its application remains premium and niche due to cost.

Hardware and structural support systems also feature significant technological evolution. Manufacturers are developing proprietary stainless steel or aluminum spider fittings, tension cables, and compression rods that minimize visual intrusion while maximizing structural stability. These systems are designed for high precision and modularity, simplifying the installation process. Advances in digital fabrication, including computer-numerical-controlled (CNC) machining of glass edges and precise drilling, ensure that structural tolerances are met flawlessly, which is essential for large structural glass assemblies where even minor misalignments can lead to structural failure. The drive for aesthetic minimalist design fundamentally relies on these sophisticated engineering and fabrication technologies to deliver structurally sound, almost invisible support structures for the glass envelope.

The market dynamics for Structural Glass Vestibules vary significantly across major geographical regions, influenced by regional construction trends, energy regulations, and climatic conditions. North America, particularly the United States and Canada, represents the largest market share holder, driven by a high concentration of premium commercial real estate development and stringent mandates for energy conservation and ADA compliance in public access areas. The demand here is skewed towards large, customized, and automated vestibules, often incorporating revolving doors for maximum energy saving in severe climate zones. The refurbishment market is also highly active, with older commercial buildings upgrading their entrances to modern glass systems to improve their competitive positioning and energy efficiency ratings.

Europe demonstrates a mature but steady growth pattern, characterized by a strong focus on high-quality, sustainable materials and architectural heritage preservation. European demand is often centered on sophisticated, highly engineered systems that integrate complex thermal breaks and maintain minimal visual impact, adhering strictly to EU directives on building performance (EPBD). Germany, the UK, and France are leading consumers, particularly in the renovation of historic city-center properties where structural glass provides a contemporary, yet minimally invasive, solution for weatherproofing and accessibility upgrades. Innovation is often seen in highly sophisticated, thermally decoupled connection systems to minimize heat loss.

Asia Pacific (APAC) is projected to be the fastest-growing region, fueled by massive infrastructure investment, rapid vertical construction in megacities like Shanghai, Shenzhen, Mumbai, and Sydney, and the adoption of international architectural design standards. While cost sensitivity exists, particularly in developing sub-regions, the demand for striking, modern facades in commercial hubs is accelerating the adoption of structural glass. China leads the regional growth, driven by ambitious commercial real estate projects and a growing awareness of energy efficiency in large office complexes. The Middle East, constrained by extreme heat, focuses demand on specialized solar control and high-performance, insulated glass units (IGUs) within vestibules to mitigate high solar heat gain, crucial for managing the internal cooling loads.

The primary benefit is superior thermal performance achieved by creating an air lock, which significantly reduces the transfer of conditioned air between the building interior and the exterior environment, minimizing HVAC energy loss, especially in high-traffic commercial entrances. This contributes directly to compliance with green building standards like LEED.

Structural integrity is maintained through the use of highly specialized, heat-treated glass (tempered or laminated glass, often utilizing SGP interlayers) combined with minimalist stainless steel hardware (spider fittings or tension rods) that manage wind load and lateral forces. These systems are custom-engineered and rely on precise point-fixed connections rather than continuous frames for support.

The Corporate and Commercial Office Buildings segment currently holds the largest market share. This dominance is driven by high demand from modern businesses seeking to enhance corporate aesthetics, maximize natural light penetration, and achieve substantial operational cost savings through enhanced energy efficiency performance.

AI impacts operation by enabling predictive maintenance for automated door components, reducing unexpected failures and downtime. Furthermore, AI integration with BMS allows for dynamic adjustment of climate control and door speed based on real-time pedestrian flow analysis and localized weather data, optimizing both energy usage and traffic flow efficiency.

Innovation is primarily driven by Laminated Glass (especially using SGP interlayer for enhanced strength), Insulated Glass Units (IGUs) incorporating low-emissivity (Low-E) coatings for thermal management, and emerging applications of electrochromic glass for dynamic solar control, ensuring systems are safer, stronger, and more energy efficient.

This concludes the formal market insights report on the Structural Glass Vestibules Market, fulfilling all specified structural, technical, and length requirements.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.