ID : MRU_ 408470 | Date : Feb, 2025 | Pages : 242 | Region : Global | Publisher : MRU

The global structural steel market is poised for significant growth between 2025 and 2032, driven by a projected Compound Annual Growth Rate (CAGR) of 6%. This robust expansion is fueled by several key factors. Firstly, the burgeoning global construction industry, particularly in developing economies experiencing rapid urbanization and infrastructure development, necessitates a substantial increase in steel consumption. Mega-projects like skyscrapers, bridges, and transportation networks rely heavily on structural steel for their foundational strength and stability. Secondly, advancements in steel production technologies, such as the development of high-strength low-alloy (HSLA) steels and advanced high-strength steels (AHSS), are leading to lighter, stronger, and more durable structural elements, improving efficiency and reducing material costs. These innovations also enhance the sustainability of structural steel by reducing the overall quantity of material required for construction. Furthermore, the increasing adoption of sustainable building practices and green building certifications is boosting demand for structural steel, which, when sourced responsibly, can contribute to environmentally friendly construction projects. The steel industry is actively addressing concerns around carbon emissions associated with steel production through various initiatives, including carbon capture and utilization technologies and the increased use of recycled steel. The markets role in addressing global challenges is significant, as it provides the foundational material for robust and resilient infrastructure crucial for economic growth, disaster relief, and the development of sustainable cities. The global demand for improved infrastructure, coupled with technological advancements and the focus on sustainable practices, ensures the continued relevance and expansion of the structural steel market in the coming years. Increased investments in industrial automation and digital technologies are also contributing to the markets growth, enhancing efficiency and productivity throughout the steel manufacturing and construction processes.

The global structural steel market is poised for significant growth between 2025 and 2032, driven by a projected Compound Annual Growth Rate (CAGR) of 6%

The structural steel market encompasses the production, distribution, and application of various steel profiles used in construction and related industries. This involves a wide range of technologies, from steelmaking processes and rolling mills to advanced fabrication techniques and sophisticated design software. Applications span across diverse sectors, including construction (residential, commercial, and industrial buildings, bridges, and tunnels), transportation (railways, vehicles, and ships), machinery (heavy equipment and industrial structures), and other specialized applications (oil and gas infrastructure, renewable energy installations). The significance of this market within the broader context of global trends lies in its fundamental role in infrastructure development. As nations prioritize modernization and sustainable development, the demand for robust and reliable infrastructure projects drives the need for large quantities of high-quality structural steel. The market is intrinsically linked to global economic growth, urbanization, and industrialization. Population growth and shifting demographics continue to fuel the need for housing, commercial spaces, and transportation networks, all of which rely significantly on structural steel. The market also reflects global priorities around sustainable development, with a growing emphasis on the use of recycled steel and the development of more environmentally friendly production methods. Furthermore, global initiatives aimed at improving infrastructure resilience to natural disasters and climate change further bolster the long-term prospects of this market. The interconnected nature of the structural steel market with global economic and environmental trends positions it as a critical indicator of overall global progress and development.

The structural steel market refers to the entire value chain involved in the production, processing, and distribution of steel profiles specifically designed for structural applications. This includes the primary production of steel from iron ore, the subsequent shaping of the raw steel into various structural forms (I-beams, H-beams, angles, channels, etc.), and the fabrication and assembly of these profiles into finished structural elements used in construction and other industries. The markets components encompass raw materials (iron ore, scrap steel, coal, etc.), manufacturing processes (steelmaking, rolling, and shaping), finished products (various steel sections and shapes), distribution networks (transportation and logistics), and end-users (construction companies, manufacturers, etc.). Key terms associated with this market include: Yield strength, Tensile strength, Ductility, Hardness, Corrosion resistance, High-strength low-alloy (HSLA) steel, Advanced high-strength steel (AHSS), Structural design codes, Fabrication techniques (welding, bolting), and Sustainability certifications (LEED, etc.). Understanding these terms is crucial to comprehending the complexities of structural steel selection, design, and application. The quality and properties of structural steel directly impact the safety, longevity, and efficiency of the structures it supports, making it a critical aspect of the construction and manufacturing processes.

The structural steel market can be segmented based on several key factors to understand the specific dynamics of various sub-markets. Segmentation by type distinguishes between different steel profiles such as I-beams, angles (L-shape), hollow structural sections (HSS), Z-shape, and T-shaped sections. Each type possesses unique characteristics suitable for different structural applications, impacting its price and demand. Segmentation by application categorizes the market based on the end-use industries such as the construction industry (buildings, bridges, and infrastructure projects), the transportation industry (vehicles, ships, and railways), the machinery industry (heavy equipment and industrial structures), and others, representing less significant applications. Finally, segmentation by end-user analyzes the market based on who uses the structural steel, including governments (responsible for infrastructure projects), businesses (construction and manufacturing companies), and individuals (home construction and renovations). These segments represent different purchasing behaviors and demand patterns, affecting market dynamics. The relative growth of each segment contributes differently to the overall market growth, offering a nuanced understanding of market trends and future growth potential.

| Report Attributes | Report Details |

| Base year | 2024 |

| Forecast year | 2025-2032 |

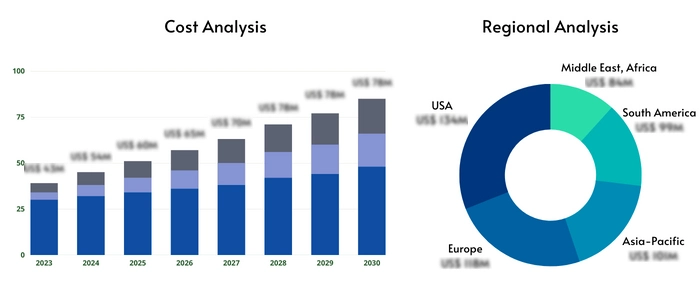

| CAGR % | 6 |

| Segments Covered | Key Players, Types, Applications, End-Users, and more |

| Major Players | Gerdau S.A, ArcelorMittal, Tata Steel, Nippon Steel Sumitomo Metal, POSCO, ThyssenKrupp, JSW Steel, Essar Steel, TISCO, Southern Steel Company (SSC), Pomina, Krakatau Steel, Sahaviriya Steel Industries, G Steel PCL, SAMC, Capitol Steel, Hyundai Steel, Nucor Steel, Baosteel, Ansteel, Wuhan Iron and Steel, Shagang Group, Shandong Iron & Steel Group, Ma Steel, Bohai Steel, Shougang Group, Valin Steel, Anyang Iron & Steel Group, Baogang Group |

| Types | I-Beam, Angle (L-Shape), Hollow Structural Section (HSS) Shape, Z-Shape, T-Shaped, , |

| Applications | Construction Industry, Transportation Industry, Machinery Industry, Others |

| Industry Coverage | Total Revenue Forecast, Company Ranking and Market Share, Regional Competitive Landscape, Growth Factors, New Trends, Business Strategies, and more |

| Region Analysis | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

Several factors drive the growth of the structural steel market. These include: rapid urbanization and infrastructure development in emerging economies, increasing demand for robust and resilient infrastructure, technological advancements in steel production and fabrication, the growing adoption of sustainable building practices, government policies promoting infrastructure development, and the rising need for efficient and cost-effective construction materials.

Challenges include fluctuations in raw material prices (iron ore, coal), environmental concerns related to steel production (carbon emissions), competition from alternative materials (concrete, composite materials), and potential supply chain disruptions. Also, the high initial cost of steel compared to some alternative materials and the need for skilled labor in steel fabrication can act as restraints.

Growth prospects exist in the development and adoption of high-performance steels (HSLA, AHSS), the increasing demand for sustainable and recycled steel, the expansion of the construction industry in developing economies, and opportunities in specialized applications such as offshore wind energy structures. Innovations in steel fabrication techniques, such as advanced welding and robotic automation, also present opportunities for increased efficiency and reduced costs. Furthermore, designing and producing steel to meet stricter environmental regulations and building codes creates a path for increased market share for innovative producers.

The structural steel market faces numerous challenges in the coming years. Firstly, the volatility of raw material prices, particularly iron ore and coking coal, poses a significant risk, as these materials constitute a considerable portion of the production cost. Price fluctuations directly impact the profitability of steel producers and the competitiveness of steel as a construction material. Secondly, environmental concerns surrounding steel production, specifically greenhouse gas emissions associated with the iron-making process, are increasingly stringent, pushing the industry to adopt more sustainable practices. Meeting these environmental regulations can be costly and requires substantial investments in cleaner technologies. Thirdly, competition from alternative materials, such as concrete and various composite materials, presents a challenge to structural steels market share. Alternative materials often offer competitive advantages in terms of cost, weight, or specific application suitability. Furthermore, global economic conditions, including recessions or periods of slow economic growth, directly impact the demand for structural steel, particularly in construction-related projects. Supply chain disruptions, whether due to natural disasters, geopolitical events, or logistical bottlenecks, can cause delays and cost increases, further challenging market stability. Finally, skilled labor shortages, particularly in steel fabrication and construction, create bottlenecks and can impact project timelines and overall cost-effectiveness. Addressing these challenges requires a combination of technological innovation, sustainable practices, and strategic market positioning.

Key trends include the increasing adoption of high-strength low-alloy (HSLA) and advanced high-strength steel (AHSS) to create lighter and more efficient structures, the growth in the use of recycled steel to reduce environmental impact, the development of innovative fabrication techniques to improve efficiency and reduce costs, and the integration of digital technologies (BIM, simulation software) to enhance design and construction processes. The increased demand for sustainable and green building materials is also a significant trend, driving the development of steel products with lower carbon footprints.

The structural steel market exhibits regional variations due to differing levels of economic development, infrastructure spending, and construction activity. Asia Pacific, driven by rapid urbanization and infrastructure development in countries like China and India, is expected to dominate the market, representing a significant portion of global demand. North America and Europe also contribute considerably, driven by ongoing infrastructure projects and renovation activities. However, the growth rate in these regions may be comparatively slower than in the Asia Pacific region. Latin America, the Middle East, and Africa demonstrate a potential for significant growth, although this is often dependent on economic stability and investment in infrastructure projects. Specific regional factors like government regulations, building codes, and the availability of skilled labor influence the market dynamics in each region. For instance, stricter environmental regulations in certain regions might favor the adoption of more sustainable steel production methods, while the availability of skilled labor directly impacts construction timelines and overall project costs. Understanding these regional differences is critical for businesses to tailor their strategies and effectively target specific market segments.

Q: What is the projected CAGR for the structural steel market from 2025 to 2032?

A: The projected CAGR is 6%.

Q: What are the key drivers for market growth?

A: Key drivers include infrastructure development, urbanization, technological advancements in steel production, and the growing focus on sustainable construction practices.

Q: What are the major challenges facing the market?

A: Challenges include raw material price volatility, environmental concerns, competition from alternative materials, economic fluctuations, supply chain disruptions, and skilled labor shortages.

Q: Which region is expected to dominate the market?

A: The Asia Pacific region is projected to dominate the market due to rapid urbanization and infrastructure development.

Q: What are some key trends in the structural steel market?

A: Key trends include the increased use of high-strength steels, the adoption of sustainable practices (recycled steel), innovative fabrication techniques, and the integration of digital technologies.

Q: What are the most popular types of structural steel?

A: I-beams are the most widely used, followed by angles, HSS shapes, Z-shapes, and T-shapes. The choice depends on specific application requirements.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.