ID : MRU_ 432991 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

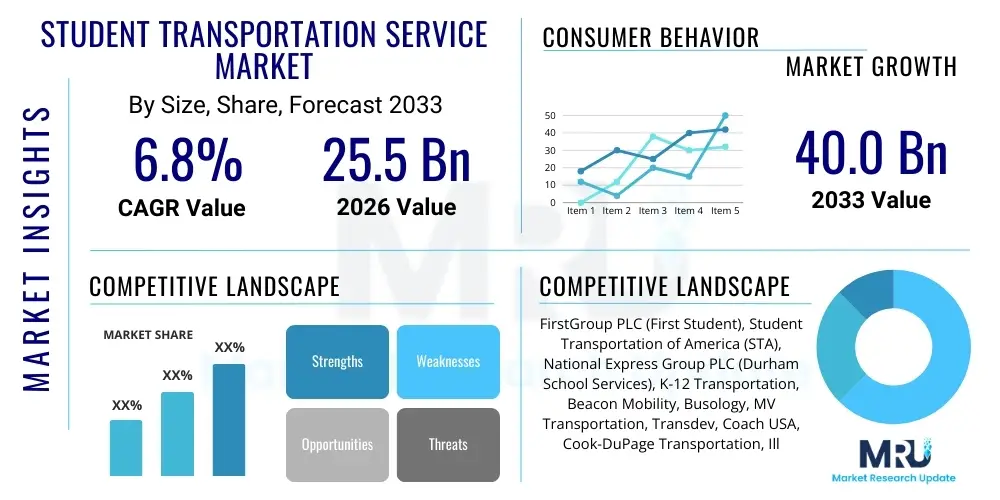

The Student Transportation Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 25.5 Billion in 2026 and is projected to reach USD 40.0 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by increasing enrollment rates globally, stringent safety regulations imposed by governmental bodies, and the rising demand for sophisticated, technology-integrated transport solutions that ensure timely and secure student transit. Urbanization and expanding residential areas necessitate longer transport routes, further fueling the demand for dedicated student transportation services provided by both public and private entities.

The market expansion is heavily influenced by the privatization of school bus operations, particularly in developed economies, which allows for greater efficiency and fleet modernization. Developing regions are witnessing rapid adoption due of infrastructure limitations and the need for organized systems to replace informal transport methods. Furthermore, the emphasis on reducing traffic congestion around educational institutions and improving overall student welfare contributes significantly to the market's size increase, prompting schools and district authorities to invest in reliable, large-scale transportation contracts.

The Student Transportation Service Market encompasses all organized mobility solutions dedicated to ferrying students between their residences and educational institutions, including primary schools, secondary schools, and universities. This service ranges from traditional yellow school buses owned by districts or outsourced to private operators, to specialized vans and carpooling services utilizing modern digital platforms. Key applications include daily commute services, transport for extracurricular activities, field trips, and special needs transportation. The primary benefits derived from these services are enhanced safety and security for minors, improved schedule reliability, reduced parental stress, and compliance with institutional logistics requirements, ensuring efficient management of large student populations across varying geographical distances.

Driving factors for this market are multifaceted, centering on demographic shifts, regulatory mandates, and technological advancements. Increasing global student enrollment, particularly in populous countries in Asia Pacific and Africa, generates fundamental demand. Simultaneously, government regulations regarding mandatory student safety features, such as GPS tracking, surveillance cameras, and stringent driver background checks, necessitate professional service provision. Moreover, the trend toward outsourcing non-core functions allows educational institutions to concentrate resources on academics while relying on specialized vendors for complex transportation logistics.

Product descriptions within this sector emphasize fleet modernization, moving towards low-emission and electric vehicles (EVs), and integrating telematics systems for real-time monitoring. Major applications extend beyond basic transit, incorporating specialized routes designed for students with disabilities (ADA compliance) and flexible routing optimization to adapt to dynamic urban environments. The integration of mobile applications for parental tracking and notifications is becoming a standard feature, enhancing service transparency and accountability, thereby defining the current competitive landscape.

The Student Transportation Service Market is characterized by steady growth driven by demographic factors and technological integration focused on safety and efficiency. Current business trends highlight a significant shift towards fleet electrification and digitalization, with major providers investing heavily in smart routing software and IoT devices to optimize operational costs and enhance security standards. Regional trends indicate North America maintaining a dominant market share due to established school bus systems and high regulatory compliance, while Asia Pacific exhibits the fastest growth due to rapid urbanization and the formalization of transport systems, moving away from informal modes of transport towards regulated, contract-based services. Consolidation among private operators is a notable trend, aiming for economies of scale and broader geographic coverage, alongside increasing collaboration between EdTech platforms and transport providers.

Segment trends reveal that the Services segment, particularly outsourcing contracts, dominates the market value, driven by the operational complexity and capital investment required for fleet management. By ownership type, the private segment is gaining traction globally, favored for its flexibility and ability to rapidly adopt new technologies compared to often bureaucratic public entities. The elementary school application segment remains the largest consumer of services, requiring the highest frequency and safety supervision, though specialized transportation for secondary and higher education is growing, focusing on efficiency for longer commuter distances and varied schedules. Sustainability goals are now a core element of RFPs (Request for Proposals), favoring vendors capable of providing alternative fuel or electric vehicle options.

Common user questions regarding AI's impact on student transportation center around how AI can enhance safety protocols, optimize complex routing schedules to reduce transit times, and predict maintenance needs for fleet vehicles. Users are particularly concerned with AI's role in real-time risk assessment, addressing challenges like traffic variability and unexpected road closures, and ensuring personalized route efficiency for individual students, especially those with special requirements. Key expectations revolve around achieving cost reduction through smart utilization and dynamic scheduling, while maintaining or exceeding current safety benchmarks. The primary themes summarized are safety optimization, predictive logistics management, and operational cost efficiency through automation.

The integration of Artificial Intelligence and Machine Learning (ML) is rapidly transforming the student transportation landscape from a static logistics challenge to a dynamic, real-time service system. AI enables operational efficiencies previously unattainable through manual or simple algorithmic scheduling. By processing massive datasets encompassing traffic patterns, weather forecasts, route history, and driver performance, AI engines can continuously refine routes, leading to significant reductions in miles driven and associated operational costs. This transformation is crucial for meeting the rising consumer expectation for transparency and real-time updates regarding student location and transit status.

Furthermore, the safety benefits derived from AI are paramount and serve as a major market differentiator. AI-driven surveillance systems and driver assistance technologies move beyond simple recording, actively analyzing behavior and environment to proactively mitigate risks. Predictive maintenance driven by ML ensures that vehicles are kept in optimal condition, minimizing the potential for road failures. As regulatory bodies increasingly demand higher safety standards, AI integration becomes essential for providers seeking to secure long-term contracts and demonstrate commitment to modern safety management practices, thereby positioning AI as a critical enabler for future market growth.

The Student Transportation Service Market is propelled by stringent safety regulations (Drivers) and the growing urbanization leading to dispersed student populations (Opportunity). However, high operating costs, including fuel price volatility and labor shortages, act as significant Restraints. The key Impact Forces include government mandates for fleet modernization, the increasing adoption of electric school buses spurred by environmental concerns, and parental demand for technology-enabled tracking and security features. These forces collectively shape investment decisions, pushing the market towards sophisticated, capital-intensive service models that offer superior safety and transparency while requiring efficient logistical management to maintain profitability amidst rising operational expenses.

Drivers: The fundamental drivers include mandatory educational attendance laws globally, increasing student enrollment figures, and the legal obligations of school districts to provide secure transport. Specific government mandates regarding child safety, requiring features like seat belts, surveillance, and specialized training for drivers and attendants, compel institutions to utilize professional, regulated services. Additionally, the increasing complexity of urban traffic necessitates professional route planning to ensure punctuality, a non-negotiable requirement for school schedules.

Restraints: Major restraints involve the significant capital expenditure required for fleet acquisition and maintenance, coupled with rising fuel costs and the persistent shortage of qualified commercial drivers. Regulatory hurdles regarding inter-state or inter-district transport logistics also create barriers to entry or expansion for smaller providers. Furthermore, the reliance on contract bidding often leads to narrow profit margins, limiting providers' ability to invest quickly in advanced technologies unless subsidized or mandated.

Opportunities: Opportunities lie in the transition towards sustainable transportation, specifically the proliferation of Electric School Buses (ESBs), which attracts government incentives and subsidies. There is also a substantial opportunity in integrating advanced IoT and telematics solutions to offer 'smart transport' services, enhancing security and operational efficiency. The outsourcing trend in regions where school districts traditionally managed their own fleets presents lucrative contractual opportunities for large private operators focused on specialized logistics management.

The Student Transportation Service Market is comprehensively segmented based on service type, ownership model, and the type of educational institution served. This segmentation provides a granular view of market dynamics, revealing differences in service requirements, regulatory pressures, and spending patterns across different user groups. The Services segment (e.g., contracting, routing, maintenance) significantly outweighs the Product segment (bus manufacturing/sales) in terms of market value, reflecting the recurring nature and complexity of transport operations. Analysis shows that segmentation by ownership (Public vs. Private) is critical, as private operators demonstrate higher flexibility and technological adoption, while the application segment (Elementary, Secondary, Higher Education) determines specific logistical needs, with younger students requiring maximum supervision and higher education routes focusing on mass transit efficiency.

The value chain for student transportation services begins with Upstream activities centered on vehicle manufacturing (OEMs), component suppliers (engines, safety technology, telematics), and fuel/energy providers. Vehicle procurement is a crucial step, often involving significant capital investment or long-term leasing agreements. Midstream operations involve the core service delivery, including route planning (logistics software providers), driver hiring and training, fleet maintenance, and daily operations management, which are typically executed by school districts or contracted private operators. Downstream activities focus on the interaction with the end-users—students, parents, and schools—involving communication platforms (apps for tracking), billing, and customer service. Distribution channels are predominantly Direct, utilizing B2B contracts between the educational institution and the service provider, though indirect channels include third-party management firms or brokerages that coordinate services for multiple small districts.

Upstream efficiency, particularly the supply chain reliability for new electric vehicle fleets and advanced safety systems, directly impacts midstream operational capability. The complexity of regulatory compliance significantly influences operational costs midstream. Driver training and technology integration, especially sophisticated telematics, are major value additions at this stage. The shift towards sustainable fleets places pressure on manufacturers and energy suppliers to provide viable, cost-effective solutions. Successful service providers differentiate themselves downstream by offering high levels of safety, reliability, and real-time communication transparency to parents, establishing trust and securing contract renewals.

Potential customers and primary buyers in the Student Transportation Service Market are highly concentrated among governmental and private educational organizations requiring regulated and reliable transit solutions for minors. The largest segment comprises Public School Districts and Local Educational Authorities (LEAs) which are often legally mandated to provide transportation services and procure large-scale, multi-year contracts through competitive bidding processes. Private and Charter Schools represent the second significant customer base, valuing customized, high-quality service and often seeking integrated safety features and personalized routing capabilities, prioritizing reliability over the lowest cost.

Other substantial customer groups include universities and colleges that require internal campus shuttles and off-campus housing routes, often focusing on efficiency and high passenger volume throughput. Furthermore, specialized government agencies or non-profit organizations dealing with students with disabilities (requiring ADA-compliant transport) form a niche, high-value customer segment due to the requirement for highly trained staff and specialized vehicles. The procurement cycle for these customers is typically long, involving detailed safety and financial audits, making customer acquisition a strategic, relationship-driven process focused on demonstrating long-term operational excellence.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 25.5 Billion |

| Market Forecast in 2033 | USD 40.0 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | FirstGroup PLC (First Student), Student Transportation of America (STA), National Express Group PLC (Durham School Services), K-12 Transportation, Beacon Mobility, Busology, MV Transportation, Transdev, Coach USA, Cook-DuPage Transportation, Illinois Central School Bus, Zum Services, Inc., Nuvve Corporation, Blue Bird Corporation, IC Bus, Thomas Built Buses, Synovia Solutions, Propark Mobility, Enterprise Fleet Management, Laidlaw Transit Services. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Student Transportation Service Market is dominated by advanced telematics, IoT sensors, and software platforms focused on safety, routing, and fleet efficiency. Key technologies include real-time GPS tracking systems, integrated video surveillance (both internal and external), and specialized student ridership tracking systems (RFID/NFC cards or mobile apps) that confirm boarding and exiting. Route optimization software leveraging complex algorithms and GIS mapping is fundamental for reducing operational mileage and time. Furthermore, the increasing penetration of diagnostic telematics provides critical data on vehicle health and driver behavior, facilitating predictive maintenance and adherence to compliance standards. These technologies collectively transform the traditional bus service into a 'Smart Transport System,' improving accountability and security.

The adoption of Electric Vehicle (EV) technology represents a major technological shift, requiring complementary infrastructure such as specialized charging management systems and depot optimization software to manage battery life and charging schedules efficiently. Connectivity is paramount; thus, high-speed onboard Wi-Fi and mobile applications for parent communication are increasingly standard offerings, enhancing the perceived value of the service. Future advancements are heavily focused on autonomous or semi-autonomous vehicle features, though widespread commercial deployment for student transport remains regulatory and safety-dependent, but pilots and advanced driver assistance systems (ADAS) are already prevalent to enhance collision avoidance.

The convergence of fleet management software with educational administration platforms (like Student Information Systems or SIS) allows for seamless data flow regarding student enrollment and address changes, optimizing route planning dynamically and automatically. This integration minimizes manual administrative errors and ensures the accuracy of ridership data, which is essential for billing and resource allocation. The investment focus remains on robust cybersecurity measures to protect sensitive student and location data, adhering to strict privacy regulations such as COPPA and GDPR, reinforcing technology as a foundation for compliance and competitive advantage.

The global Student Transportation Service Market exhibits diverse characteristics across major geographical regions, influenced by regulatory environments, infrastructure development, and varying levels of market maturity. North America, encompassing the United States and Canada, represents the largest and most mature market, characterized by extensive, well-established public school bus systems and high integration of private contractors. Stringent federal and state safety regulations drive continuous investment in advanced technology (GPS, surveillance, safety features). The region is currently leading the transition towards electric school buses, supported by substantial government funding and incentive programs aimed at decarbonization.

The Asia Pacific (APAC) region is projected to be the fastest-growing market due to rapid urbanization, increasing per capita income, and a booming population base leading to higher school enrollment. While the market here is more fragmented, with informal services still prevalent in many developing countries, formalization and consolidation are accelerating, particularly in China and India, where structured private service providers are emerging to meet the logistical demands of large metro areas. Safety concerns raised by parents are a primary catalyst for adopting professional, technology-enabled transportation services across the region.

Europe presents a mature but varied landscape. Service provision is often decentralized and managed at the municipal level, with significant reliance on public transit systems integrated with school routes, especially in Western Europe. However, specialized and long-distance student transport remains a substantial contract opportunity. Regulation often focuses heavily on environmental standards, driving the adoption of low-emission zones and fostering innovation in fuel-efficient and electric buses. The Latin America and Middle East & Africa (MEA) regions show significant potential, driven by improving educational access and the demand for formal, secure transport solutions to address safety challenges inherent in less structured urban environments.

The primary factor driving market growth is the increasing stringency of government safety regulations worldwide, mandating advanced security features, standardized vehicles, and professional operational protocols for student transit, thereby accelerating the outsourcing of these complex services to specialized private operators.

AI is primarily utilized for dynamic route optimization based on real-time traffic and student data, predictive maintenance to minimize vehicle downtime, and enhancing safety through driver behavior monitoring and automated student ridership verification systems.

The Elementary School Transportation segment (K-5) holds the largest market share by application due to the critical need for constant supervision, higher frequency of service, and mandatory transport provision for younger, safety-vulnerable age groups across most educational systems.

Key constraints include the volatility of fuel prices, high initial capital expenditure required for fleet modernization (especially EV transition), and a persistent shortage of qualified, licensed commercial drivers necessary to meet operational demand across high-growth regions.

The shift towards ESBs is significant as it aligns the sector with global sustainability goals, reduces long-term operational costs (fuel and maintenance), and is strongly supported by government incentives and funding, positioning electrification as a critical market opportunity and competitive differentiator.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.