ID : MRU_ 432318 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

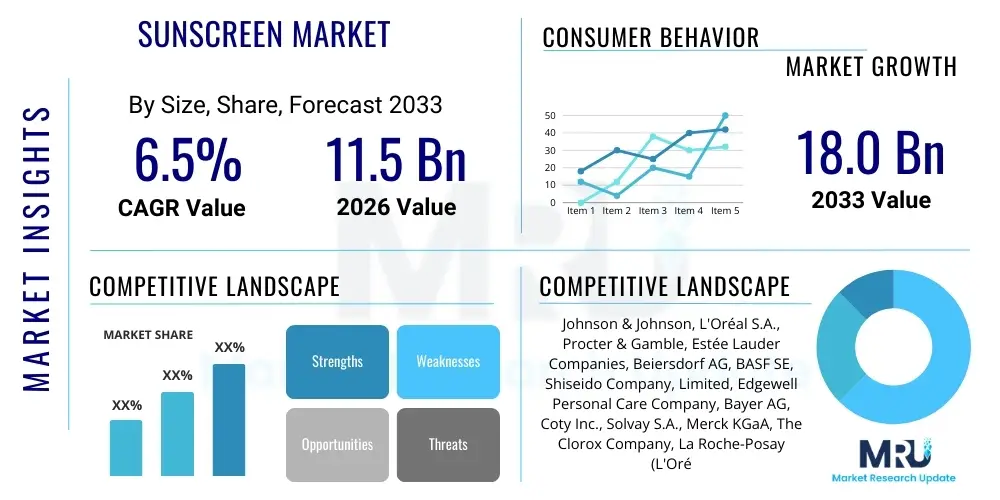

The Sunscreen Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 11.5 Billion in 2026 and is projected to reach USD 18.0 Billion by the end of the forecast period in 2033.

The Sunscreen Market encompasses the global sales of topical products designed to protect the skin from harmful ultraviolet (UV) radiation emitted by the sun. These products primarily contain organic (chemical) or inorganic (physical/mineral) filters that absorb, reflect, or scatter UV rays, thereby preventing sunburn, premature aging, and reducing the risk of skin cancer. The continuous rise in consumer awareness regarding the detrimental effects of UV exposure, coupled with increasing instances of skin conditions related to sun damage, serves as the fundamental driving force for market expansion across both developed and emerging economies. Product diversity has increased significantly, moving beyond traditional lotions to include sprays, sticks, gels, and integrated cosmetics.

The core application of sunscreen products spans daily skincare routines, recreational outdoor activities, and specific dermatological needs. Major applications include facial care, body protection, and specialized use for sensitive skin or specific activities like water sports, necessitating water-resistant formulations. The primary benefit derived from regular sunscreen usage is robust photoprotection, crucial for maintaining skin health and appearance. Furthermore, sunscreens are increasingly marketed with additional benefits such as anti-pollution, moisturizing, and anti-aging properties, blending sun protection with cosmetic enhancement, which broadens their appeal to a demographic focused on holistic skin wellness.

Market growth is substantially driven by stringent regulatory frameworks in regions like North America and Europe mandating high SPF (Sun Protection Factor) standards and encouraging consumer compliance. Key driving factors also include product innovation focusing on reef-safe formulas (addressing environmental concerns), the integration of sophisticated delivery systems for enhanced efficacy, and the massive uptake of daily-use facial sunscreens among younger, digitally-native consumers. The market dynamics are highly competitive, characterized by rapid shifts in consumer preferences towards natural ingredients and clean beauty labels, compelling manufacturers to continually refine their compositions and transparency regarding filter safety.

The global Sunscreen Market exhibits robust expansion driven by increasing health consciousness, heightened regulatory oversight regarding UV protection standards, and significant innovations in product formulations. Current business trends indicate a strong pivot towards mineral-based sunscreens containing zinc oxide and titanium dioxide, perceived by consumers as safer and more environmentally friendly alternatives to traditional chemical filters. Furthermore, the convergence of sun protection with daily cosmetic routines, particularly through the proliferation of SPF-enhanced moisturizers and foundations, is expanding the usage base beyond beach use to everyday urban settings. Strategic collaborations focused on sustainable packaging and ingredient sourcing are critical determinants of market success and brand loyalty.

Regionally, the market is characterized by differential growth rates. Asia Pacific (APAC) leads in terms of consumption volume, primarily fueled by massive populations, rapidly increasing disposable income, and a deep-seated cultural preference for skin whitening and anti-pigmentation products, making high-SPF, broad-spectrum sunscreens essential. North America and Europe maintain high market shares due to established consumer awareness, mature regulatory environments, and high demand for specialized, premium, and clean-label sunscreens. Emerging markets in Latin America and the Middle East and Africa (MEA) are demonstrating accelerated growth due to rising outdoor tourism and growing penetration of international beauty and wellness brands.

In terms of segmentation trends, the chemical sunscreen segment currently holds the dominant revenue share but is facing intense competitive pressure from the rapidly expanding physical/mineral segment. Within the distribution channel segment, e-commerce platforms are recording the fastest growth rate, leveraging convenience, wide product range, and detailed consumer reviews to capture market share, particularly among younger demographics. Conversely, pharmacies and specialized beauty retail stores remain crucial for premium and dermatologically recommended products. Future trends are expected to heavily favor products offering high efficacy, verifiable safety credentials (especially for active ingredients), and multi-functional benefits addressing protection and skin health simultaneously.

Common user questions regarding AI’s impact on the Sunscreen Market often revolve around personalized UV protection recommendations, the development speed of new, safer UV filters, and how AI might revolutionize consumer education and purchasing experiences. Users frequently inquire if AI can analyze individual skin profiles, geographical UV intensity, and behavioral patterns to suggest the optimal SPF and product type, moving beyond generic recommendations. There is also significant interest in how machine learning can accelerate R&D by simulating the efficacy and toxicity profiles of novel organic compounds, significantly reducing laboratory time and cost associated with regulatory approvals. Key concerns center on data privacy regarding skin health data and the potential for algorithmic bias in product recommendations.

The analysis indicates that key themes focus on optimization and personalization. Users expect AI to provide highly customized solutions, transitioning the market from mass-produced sunscreens to tailored photoprotection strategies. Expectation levels are high regarding AI-driven skin diagnostic tools integrated into mobile applications or smart mirrors that provide real-time UV index updates and application reminders specific to the user’s exposure level and planned activities. This level of personalization not only enhances protection but also boosts consumer engagement and product usage adherence, a significant challenge in the current market.

Furthermore, AI is poised to dramatically influence supply chain efficiency and consumer trend forecasting. Predictive analytics can help manufacturers anticipate shifts in demand, such as sudden spikes for reef-safe or mineral sunscreens in specific coastal regions, allowing for optimized inventory management and waste reduction. For content and marketing, AI models are essential for optimizing AEO/GEO strategies, analyzing search intent related to terms like "best non-nano zinc sunscreen" or "waterproof SPF for sensitive skin," ensuring that product information is easily accessible and directly answers specific consumer queries, thereby solidifying brand authority and driving online sales conversion.

The Sunscreen Market is profoundly shaped by a combination of strong drivers, notable restraints, and expansive opportunities, forming a complex structure of impact forces. The primary drivers include rapidly increasing consumer awareness regarding the link between UV exposure and melanoma, heightened regulatory requirements mandating clear labeling and efficacy testing (SPF, Broad Spectrum), and the integration of sun protection into daily beauty and anti-aging regimens. These factors collectively push manufacturers toward innovation, focusing on higher SPF values and better sensorial qualities. However, the market faces significant restraints, chiefly concerning the public perception of the safety of chemical UV filters (e.g., oxybenzone, octinoxate), which has led to consumer hesitancy and demands for more comprehensive safety data. Furthermore, the complexity and cost associated with obtaining FDA or equivalent regulatory approvals for new filter ingredients pose substantial barriers to entry and innovation speed.

Opportunities within the sector are abundant, particularly in the development and commercialization of mineral sunscreens that are both high-efficacy and cosmetically elegant (non-whitening, lightweight texture). A significant opportunity lies in capitalizing on the "Blue Beauty" trend, emphasizing marine and coral reef safety, driving demand for zinc oxide and titanium dioxide formulations free from harmful oxybenzone and octinoxate. Moreover, expanding product penetration in developing nations through affordable, locally relevant formats and targeted educational campaigns offers substantial revenue potential. The development of ingestible sun protection supplements (nutricosmetics) and specialized sunscreens for different population groups (e.g., children, athletes, specific ethnic skin types) also represents niche market growth areas.

The impact forces are largely driven by health and regulatory pressures. The ongoing scientific debate over the systemic absorption and endocrine disruption potential of certain chemical filters exerts a strong negative force, compelling large corporations to reformulate or phase out controversial ingredients, often at significant cost. Conversely, the positive force of dermatologist recommendations and public health campaigns strongly advocates for consistent daily use, stabilizing demand. The market equilibrium is continuously shifting as environmental concerns (reef safety) become intertwined with personal health concerns, forcing manufacturers to adopt sustainable practices not just in ingredients but also in packaging and sourcing, requiring continuous adaptation to maintain market relevance and trust among increasingly informed consumers.

The Sunscreen Market is comprehensively segmented based on product type, active ingredient, form, usage area, distribution channel, and application, enabling a granular understanding of consumer purchasing habits and technological preferences. The core segmentation by active ingredient—chemical versus mineral (physical)—defines major competitive landscapes and consumer perception strategies. Segmentation by product form (lotion, spray, stick, etc.) addresses usability and convenience preferences, while distribution channel segmentation (online, retail, pharmacy) identifies optimal market reach strategies. This multi-dimensional analysis is crucial for stakeholders developing targeted marketing campaigns and product development pipelines to capture specific demographic needs, such as high water resistance for sports or non-comedogenic formulations for facial care.

The value chain for the Sunscreen Market commences with the upstream analysis, which is highly specialized, involving the sourcing and synthesis of active ingredients—both organic filters (like Avobenzone) and inorganic filters (pharmaceutical-grade zinc oxide and titanium dioxide). Key stakeholders at this stage include specialized chemical manufacturers and pharmaceutical companies that comply with stringent cosmetic ingredient standards (e.g., EU regulations, FDA monographs). This initial phase also includes sourcing excipients, emulsifiers, antioxidants, and carrier oils, which are critical for the product’s texture, stability, and cosmetic elegance. High quality control and stability testing are mandatory upstream activities due to the functional requirements of UV protection.

The midstream phase involves manufacturing, formulation, and packaging. Large multinational beauty conglomerates and specialized contract manufacturers undertake the blending and stability testing of complex formulas. This stage demands sophisticated R&D capabilities to ensure photostability, broad-spectrum coverage, and meeting specific consumer requirements such as water resistance or non-comedogenicity. Downstream analysis focuses heavily on distribution and retailing. Products move through a complex network encompassing direct channels (brand websites), indirect channels (large-scale supermarkets and specialized drugstores like CVS or Boots), and, increasingly, highly influential e-commerce platforms (Amazon, dedicated beauty portals). The efficiency of the distribution channel is crucial for maximizing shelf presence and managing seasonal demand fluctuations inherent in the sunscreen market.

Direct distribution, primarily through brand-owned stores or direct-to-consumer (DTC) e-commerce, allows brands maximum control over pricing, branding, and customer experience, facilitating the rapid launch of niche or premium products. Conversely, indirect channels like hypermarkets and pharmacies dominate mass-market sales due to convenience and trust, especially when sunscreens are positioned as essential health and pharmacy items. Specialized beauty retailers play a vital role in showcasing innovative, high-end formulations and offering expert consultation, reinforcing premium positioning. The complexity of regulatory compliance across international borders—where sunscreens may be classified as drugs (US) or cosmetics (EU)—significantly influences logistics and marketing strategies within the downstream segment.

The potential customer base for the Sunscreen Market is extremely broad, encompassing virtually all demographics globally due to the universal need for protection against UV radiation, irrespective of skin tone or geographical location. End-users are segmented into General Consumers (seeking daily or recreational protection), Dermatological Patients (requiring medical-grade, highly sensitive formulas), and specific Lifestyle Users (athletes, outdoor workers, and infants/children). The largest and fastest-growing customer segment is the daily user, particularly those aged 20-45, who integrate facial sunscreens into their routine for anti-aging and preventive care, often prioritizing lightweight, non-greasy textures and formulations that layer well under makeup. These buyers are heavily influenced by social media trends and clean beauty certifications.

Another crucial customer segment involves parents purchasing pediatric sunscreens. These buyers prioritize safety, often demanding mineral-based formulations (zinc and titanium) that are hypoallergenic and free from harsh chemicals. Purchase decisions in this segment are significantly influenced by pediatric recommendations and regulatory standards emphasizing safety for sensitive, young skin. The elderly population represents a growing segment, driven by increased awareness of long-term skin health risks, leading to higher demand for specialized products addressing dryness and fragility associated with aging skin, often recommended through healthcare channels. The diversification of product offerings, such as SPF-infused clothing or sunscreens specifically designed for darker skin tones (avoiding white cast), is continually expanding the market's reach into previously underserved populations.

Finally, the rising trend of outdoor tourism and destination weddings across tropical regions creates a significant demand spike for high-SPF, water-resistant, and reef-safe products, positioning travelers as key seasonal buyers. Geographically, potential customers in high-UV index regions (like Australia, Southeast Asia, and Equatorial Africa) exhibit a high frequency of purchase and high-volume usage, viewing sunscreen as a daily necessity rather than a recreational luxury. Understanding the specific needs of these varied buyers—from efficacy (athletes) to cosmetic elegance (urban daily users) and safety (parents)—is paramount for market success.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 11.5 Billion |

| Market Forecast in 2033 | USD 18.0 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Johnson & Johnson, L'Oréal S.A., Procter & Gamble, Estée Lauder Companies, Beiersdorf AG, BASF SE, Shiseido Company, Limited, Edgewell Personal Care Company, Bayer AG, Coty Inc., Solvay S.A., Merck KGaA, The Clorox Company, La Roche-Posay (L'Oréal), Unilever PLC, Revlon, Inc., Kao Corporation, COOLA, Supergoop!, EltaMD. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Sunscreen Market is rapidly evolving, driven by the need to enhance efficacy, improve cosmetic appeal, and address growing safety concerns regarding UV filters. A significant technological focus is on encapsulation and delivery systems, which aim to stabilize chemical filters, prevent their systemic absorption into the bloodstream, and ensure their uniform dispersion across the skin. Nanotechnology plays a crucial role here, particularly in refining inorganic filters like zinc oxide and titanium dioxide to reduce the particle size (often below 100nm). This modification eliminates the visible white cast often associated with mineral sunscreens, enhancing product acceptance among consumers, especially those with darker skin tones, while maintaining high UV blocking capability. However, regulatory scrutiny over potential health impacts of nanoparticles necessitates meticulous safety testing and transparent labeling.

Another critical area of technological innovation involves the development of broad-spectrum photostabilizers. Many effective chemical filters, such as Avobenzone, degrade rapidly upon exposure to sunlight, losing their protective efficacy. Manufacturers are investing heavily in photostabilization technology—using specialized ingredients or proprietary combinations—to ensure that the SPF rating holds up throughout the period of sun exposure. Furthermore, the convergence of cosmetics and healthcare is driving the integration of biotechnological ingredients, such as specialized antioxidants, DNA repair enzymes, and anti-pollution complexes, which work synergistically with the UV filters to offer comprehensive skin defense against environmental stressors beyond just sunlight, including blue light and infrared radiation.

Digital technology is increasingly influencing product application and monitoring. The emergence of wearable devices and patches that measure individual UV exposure in real-time and communicate optimal reapplication times is a key disruptive technology. Similarly, advanced spectrophotometry and in-vitro testing methods are being refined to more accurately measure SPF and broad-spectrum protection, moving beyond traditional, slower in-vivo human testing. The continuous technological push towards developing new, novel UV filters—often bio-engineered or naturally derived—that meet stringent safety profiles while offering superior protection (high critical wavelength) is the cornerstone of future market innovation, aiming to create the perfect balance between robust protection and clean-label standards.

The global Sunscreen Market exhibits varied dynamics across major regions, influenced by cultural norms, regulatory environments, and climate patterns. North America, driven by the US and Canada, is a dominant market characterized by high consumer spending on premium, dermatologically approved, and mineral-based sunscreens. The region shows robust growth in the daily-wear segment, supported by continuous public health messaging promoting year-round use, regardless of climate. European demand is equally strong but heavily regulated by the European Union, which has approved a wider array of chemical filters compared to the US FDA, leading to greater product diversity. Consumers here increasingly focus on sustainability and eco-friendly packaging, driving the adoption of reef-safe and organic formulations across markets like Germany and France.

Asia Pacific (APAC) stands out as the highest growth region. This surge is driven by high population density, rising disposable incomes, and the ingrained cultural practice of avoiding tanning (whitening trend). Countries like South Korea, Japan, and China are hubs for innovation, where sun protection is seamlessly integrated into multi-step skincare routines (using high SPF foundations, cushion compacts, and highly fluid essences). This market segment prioritizes extremely light textures, non-tacky finishes, and formulations with integrated brightening agents, pushing the boundaries of cosmetic elegance in sun protection. The demand here dictates global trends in texture and sensorial experience.

Latin America (LATAM) and the Middle East and Africa (MEA) are emerging as high-potential markets. LATAM, particularly Brazil and Mexico, benefits from high solar intensity and increasing urbanization, leading to higher adoption rates for both recreational and daily-use sunscreens. The MEA region is witnessing growth spurred by rising tourism, increased expatriate populations, and a gradual increase in awareness regarding skin cancer risk, particularly in wealthy Gulf nations. However, market growth in these emerging economies often faces challenges related to price sensitivity and the need for education regarding the necessity of broad-spectrum protection tailored for diverse skin types and extreme climates.

Chemical sunscreens (organic filters like oxybenzone) absorb UV rays and convert them into heat released from the skin, while mineral sunscreens (inorganic filters like zinc oxide and titanium dioxide) create a physical barrier that sits on the skin surface to deflect and scatter UV radiation. Mineral sunscreens are often preferred for sensitive skin and are considered reef-safe.

Reef-safe sunscreens exclude ingredients such as oxybenzone and octinoxate, which have been scientifically linked to coral bleaching and DNA damage in marine life. Growing environmental consciousness and protective legislation in areas like Hawaii and Palau mandate the use of mineral-based alternatives to protect fragile marine ecosystems.

Major growth drivers include intensified consumer education on the long-term risks of UV exposure, the integration of sun protection into daily cosmetic and anti-aging routines, and technological advancements creating aesthetically pleasing mineral formulations that minimize the undesirable white cast.

Online retail and e-commerce platforms are recording the fastest growth rate, driven by consumer preference for convenience, detailed product information, easy access to specialized and international brands, and the ability to compare pricing and read extensive user reviews before purchase.

AI is projected to significantly accelerate the research and development of safer, novel UV filters through predictive modeling, reducing testing timelines. Furthermore, AI will enable hyper-personalization, using individual skin profiles and real-time geographical UV data to recommend optimal SPF levels, reapplication times, and product types.

The detailed analysis within this report underscores the transition of the Sunscreen Market from a seasonal cosmetic item to a year-round, essential component of global health and wellness strategies. Ongoing innovation in clean-label ingredients, alongside the strategic utilization of digital technologies for consumer personalization, will define competitive success throughout the forecast period.

Further analysis of the global market reveals a significant trend toward multi-functional sunscreens that offer benefits beyond simple UV filtration. Consumers are increasingly seeking products fortified with antioxidants like Vitamin C and E, as well as hyaluronic acid, to provide hydration and protection against secondary environmental aggressors such as pollution and blue light emitted from digital screens. This convergence of skincare and sun care is driving premiumization, allowing brands to justify higher price points for advanced, holistic protection solutions.

The regulatory environment remains a pivotal force, particularly the divergent approaches taken by the U.S. FDA, which has been slow to approve new organic filters, and the EU, which maintains a more dynamic list of approved filters. This regulatory fragmentation poses logistical challenges for multinational corporations, forcing them to develop regionally specific formulations. The ongoing dialogue surrounding the safety data for current chemical filters, such as oxybenzone, necessitates preemptive reformulation strategies by market leaders to maintain consumer trust and market compliance, potentially increasing the immediate cost of goods but ensuring long-term market sustainability.

In the Asia Pacific market, the demand for highly advanced cosmetic textures is not merely a preference but a prerequisite for market entry. Technologies focusing on water-gel textures, quick absorption, and non-pilling formulas are dominating R&D efforts. This region also showcases the highest adoption of integrated SPF products, often found in traditional cosmetics like cushion foundations and brightening creams, reflecting a consumer base that values efficiency and seamless integration into daily beauty routines. The success of brands in this region often hinges on their ability to deliver high-SPF protection (SPF 50+) without compromising on the weight or feel of the product.

The sustainable packaging movement also impacts the value chain, compelling manufacturers to invest in post-consumer recycled (PCR) plastic, refillable options, and biodegradable containers. While this increases short-term production complexity and cost, it aligns with AEO and GEO optimization by satisfying consumer search intent related to "eco-friendly" and "sustainable beauty" sunscreens, boosting brand visibility and preference among environmentally conscious segments. These strategic investments ensure the market continues its upward trajectory, balanced by regulatory and environmental accountability.

The competitive landscape is characterized by established pharmaceutical giants leveraging their dermatological research pedigree, alongside agile, Direct-to-Consumer (DTC) brands that specialize in niche, clean-label, or specific demographic sunscreens (e.g., mineral-only brands). The success of new market entrants often relies on transparent ingredient lists, strong digital marketing campaigns that educate consumers, and cultivating loyal followings through social media endorsements, particularly from dermatologists and skin health influencers. Intellectual property related to photostability and non-whitening zinc oxide dispersion technologies is increasingly becoming a critical competitive asset.

Furthermore, specialized sunscreens for different light spectrums are gaining traction. Research into protection against High Energy Visible Light (HEVL), commonly known as blue light, is driving the inclusion of ingredients like iron oxides or specific plant extracts. As consumers spend more time indoors and interacting with screens, the demand for HEVL-protective products is growing, distinguishing high-end formulations from standard UV blockers. This expansion reflects the market's continuous adaptation to modern lifestyle factors and a growing scientific understanding of light-induced skin damage beyond traditional UV exposure.

Technological advancement is also focusing on improving the sensory profile of mineral sunscreens. Older formulations often left a thick, white residue, which deterred consistent application. Current innovation uses advanced micronization and specific carrier oils and silicones to create sheer, rapidly absorbing mineral products that rival the texture of chemical sunscreens. This continuous refinement directly addresses one of the primary historical restraints of the mineral segment, further supporting its rapid market takeover, especially in high-volume, sensitive facial application categories.

In terms of distribution, the shift towards Omnichannel retail is paramount. While e-commerce provides scalability, physical channels such as specialized pharmacies remain essential for products requiring high trust, such as medical-grade sunscreens recommended post-procedure or for sensitive conditions. Brands that successfully integrate online engagement (personalized advice, virtual try-ons) with physical accessibility (pharmacy stockists) are best positioned for future market leadership, ensuring that the AEO focus translates into actual point-of-sale conversions across all touchpoints.

The penetration rate of sunscreens in emerging markets is strongly correlated with consumer education initiatives. Partnerships between major brands and local health organizations to communicate the risks of sun exposure are crucial catalysts for market growth in regions like Sub-Saharan Africa and certain parts of South Asia. Overcoming cultural hesitations and misconceptions regarding sunscreens' necessity for all skin types requires targeted, localized marketing efforts that address specific climate conditions and skin characteristics, moving beyond generic global marketing campaigns. This localized strategy is essential for unlocking substantial long-term market value in these high-potential geographical segments.

Regulatory bodies globally are also pushing for clearer labeling regarding 'broad spectrum' protection, ensuring consumers understand the difference between UVA and UVB protection. This push towards greater transparency empowers consumers to make more informed choices, favoring brands that offer robust, verifiable protection levels. The future success of sunscreens will therefore rely heavily on validated efficacy data, transparent ingredient communication, and a clear commitment to environmental safety, solidifying the product's role as a necessary health and wellness product rather than a mere cosmetic item.

The utilization of blockchain technology is a nascent but important trend, particularly in assuring the authenticity and traceability of ingredients, especially for clean-label or mineral sunscreens where sourcing transparency is a major consumer demand. Implementing blockchain can verify the supply chain origin of zinc oxide or specific botanical extracts, enhancing brand trust and providing a definitive answer to consumer queries about ethical sourcing and ingredient purity. This technological step moves beyond basic labeling to provide immutable data on product composition, setting a new standard for premium positioning and regulatory compliance.

Furthermore, the sports and outdoor activity segment continues to drive demand for specialized, high-performance sunscreens. These products require exceptional water and sweat resistance, durability under physical stress, and often need to be non-migratory to prevent stinging the eyes. Innovation in film-forming polymers and application mechanisms (such as continuous spray technology) are key technical advancements supporting this segment, allowing athletes and outdoor enthusiasts to maintain consistent protection throughout prolonged exposure periods, contributing significantly to the overall market resilience and value growth across multiple geographies.

The pediatric sunscreen category is experiencing innovation driven primarily by heightened parental concern about ingredient absorption. Manufacturers are focusing on formulations that minimize the number of components, prioritize non-nano mineral filters, and offer hypoallergenic certifications. Packaging innovation here also plays a role, with brightly colored, easy-to-apply sticks and pump dispensers favored for ease of use on children. The emphasis on ultra-gentle, high-SPF protection reflects the high willingness of consumers in developed markets to invest in premium safety products for their children, guaranteeing stable demand and driving category specialization.

The rise of specialized retail environments, focusing solely on clean beauty or dermatology, has created platforms where premium sunscreen brands can thrive. These stores provide consultative sales experiences, educating consumers on filter types, application techniques, and the science behind UV protection—elements often lacking in mass-market supermarkets. This channel reinforces the perception of sunscreens as an essential health item, not just a seasonal commodity, thereby aiding market expansion and value growth by promoting complex, higher-priced formulations effectively to a discerning consumer base.

Another area of technological focus is improving the photostability of Vitamin A derivatives (retinoids) often found in anti-aging routines, which can increase sun sensitivity. Future sunscreens are increasingly formulated to be compatible with, or even enhance the stability of, these companion skincare ingredients, catering directly to the sophisticated user who layers multiple active products. This focus on compatibility and synergistic benefits strengthens the daily-use facial segment and encourages consistent morning application of high-efficacy SPF, supporting year-round revenue generation for the market.

The market faces the constant challenge of regulatory divergence on SPF testing methods, particularly between Asian countries (which often use the PPD method for UVA protection) and Western standards. Harmonizing these testing procedures remains a long-term goal for the industry, as complexity in testing and labeling procedures directly increases operational costs and hampers global product rollout efficiency. The investment in robust, internationally accepted testing standards is thus a vital component of future market infrastructure and regulatory technology compliance.

The continued strong performance of the Sunscreen Market is inextricably linked to global climate change and the resulting increase in average UV Index levels in many regions. As environmental factors exacerbate the need for protection, the market demand becomes non-cyclical, moving towards mandatory daily usage across wider geographical spreads and for extended periods of the year. This macro-environmental force acts as a permanent driver, underpinning the projected compound annual growth rate and ensuring sustained long-term investment in protective product innovation.

Finally, the growing popularity of medical tourism, particularly for cosmetic procedures such as lasers and peels, drives significant demand for post-procedure sunscreens. These products must be non-irritating, possess extremely high SPF, and aid in wound healing and pigmentation prevention. This niche medical segment emphasizes the essential health role of sun protection, creating a dedicated high-value category where efficacy and dermatologist endorsement are the paramount purchasing criteria, demonstrating the market's successful diversification beyond general recreational use.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.