ID : MRU_ 434201 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

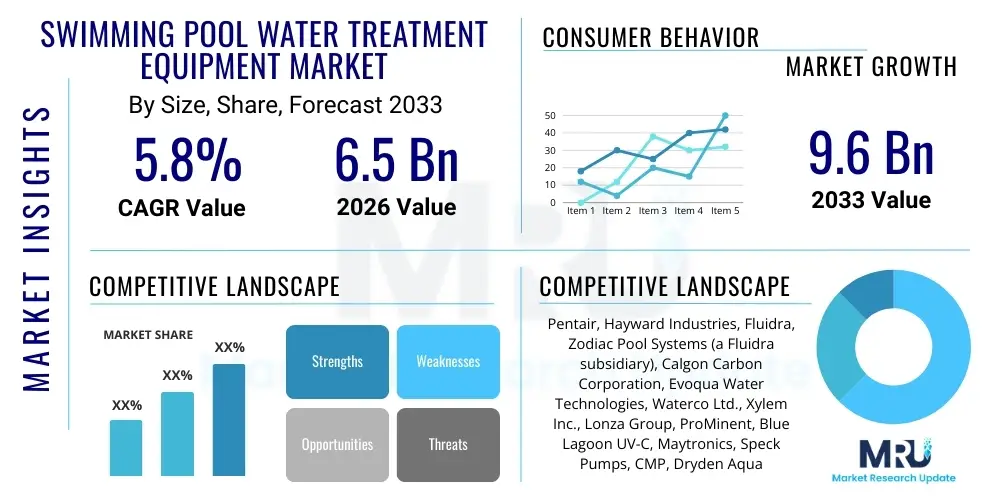

The Swimming Pool Water Treatment Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 6.5 Billion in 2026 and is projected to reach USD 9.6 Billion by the end of the forecast period in 2033.

The Swimming Pool Water Treatment Equipment Market encompasses a wide array of devices, systems, and chemicals designed to maintain the hygiene, clarity, and safety of swimming pool and spa water. These essential systems include filtration units, circulation pumps, chemical feeders, disinfection systems (such as chlorinators, ozonators, and UV systems), automated controllers, and water quality sensors. The primary objective of this equipment is to remove physical contaminants, prevent the growth of pathogens, algae, and bacteria, and ensure the chemical balance (pH and alkalinity) remains within safe and comfortable parameters for bathers. Growing awareness regarding waterborne diseases and stringent public health regulations globally are central to the sustained demand for advanced treatment solutions.

The product portfolio within this market is highly diverse, ranging from traditional sand filters and chlorine dispensing mechanisms to highly sophisticated, energy-efficient, and automated water management systems. Key products driving market growth include variable speed pumps, which reduce energy consumption significantly, and salt-chlorine generators, which offer a gentler and less irritating method of sanitation compared to traditional liquid or tablet chlorine. Furthermore, the integration of smart technologies allows for remote monitoring and automated dosing adjustments, optimizing water chemistry in real-time and minimizing the need for manual intervention, thereby appealing to both residential and commercial pool owners seeking convenience and operational efficiency.

Major applications span residential pools, commercial facilities (such as hotels, fitness centers, and water parks), and public pools. The benefits derived from utilizing high-quality water treatment equipment are substantial, including enhanced bather safety, reduced maintenance costs over the long term, protection of pool infrastructure from corrosion or scaling, and compliance with increasingly demanding environmental and health standards. Driving factors for market expansion include the global increase in disposable income leading to higher demand for residential pools, the robust growth of the tourism and hospitality sector requiring well-maintained commercial pools, and technological advancements focusing on sustainability and automation in water management.

The Swimming Pool Water Treatment Equipment Market is exhibiting robust growth, propelled by strong consumer preference for automated and environmentally friendly sanitation methods. Business trends highlight a significant shift towards digitization, with manufacturers focusing on integrating IoT capabilities into pumps, filters, and chemical monitoring systems. This integration supports predictive maintenance and remote management, providing a competitive edge. Furthermore, sustainability is a core business driver, leading to increased adoption of energy-efficient variable speed pumps (VSPs) and non-chlorine or low-chlorine disinfection methods like UV and ozone. Mergers, acquisitions, and strategic partnerships centered on consolidating technology expertise are prevalent, aiming to create holistic water management solutions for both the new construction and aftermarket segments.

Regional trends indicate that North America and Europe remain mature markets characterized by high replacement rates and early adoption of premium, automated equipment, driven by strict regulatory standards concerning water quality and energy efficiency. The Asia Pacific region, particularly countries like China and India, presents the highest growth potential, fueled by rapid urbanization, expanding middle-class disposable income, and massive infrastructure development in tourism and real estate, leading to a surge in new pool constructions. Latin America and the Middle East also show promising growth, largely due to investments in luxury residential projects and resort developments that mandate high-quality, reliable water treatment solutions tailored for warm climates.

Segmentation trends reveal that the Equipment segment (pumps, filters, heaters) dominates the market share due to its foundational necessity in any pool system, with the VSP category experiencing exceptional growth. Within the Disinfection Type segment, salt-chlorine generators are gaining widespread acceptance among residential users for their ease of use, while commercial facilities increasingly adopt advanced sanitation methods like UV and ozone to minimize chemical handling risks and meet stringent regulatory disinfection residuals. The Service segment, encompassing maintenance and repair, is expanding rapidly as the installed base of complex, automated equipment grows, requiring specialized technical expertise for upkeep and calibration, solidifying recurring revenue streams for service providers.

Common user questions regarding AI's impact typically revolve around how artificial intelligence can achieve hyper-precision in chemical dosing, whether AI can truly predict equipment failures before they occur, and the cost-benefit analysis of implementing AI-driven pool management systems in residential settings versus commercial applications. Users are concerned about data privacy and the complexity of integrating sophisticated AI software with existing legacy pool infrastructure. The overarching themes are operational efficiency, enhanced safety through real-time predictive monitoring, and the potential for AI to dramatically reduce chemical consumption and energy costs by optimizing pump cycles and filtration schedules based on actual usage patterns, weather forecasts, and historical water quality data.

The market dynamics are defined by a complex interplay of drivers, restraints, and opportunities that collectively shape investment decisions and technological innovation. Key drivers include the stringent regulations enforced by health organizations globally concerning recreational water quality, the increasing consumer demand for convenient, low-maintenance pool sanitation methods, and the growing urbanization trend leading to greater adoption of communal and residential swimming facilities. These forces necessitate the continuous upgrading of existing equipment and investment in new, highly effective disinfection and filtration systems, ensuring that water is not only visibly clear but microbiologically safe. The focus on energy efficiency, particularly in mature markets like Europe and North America, mandates the replacement of standard pumps and heaters with inverter and variable speed technologies, acting as a strong market accelerator.

However, the market faces significant restraints that temper its potential. The high initial capital investment required for advanced, automated pool treatment systems, particularly UV, ozone, and smart control interfaces, can be prohibitive for budget-conscious consumers in developing regions. Additionally, the necessity for skilled professionals for the installation, maintenance, and complex troubleshooting of integrated systems presents a logistical challenge, particularly in geographically dispersed areas. Seasonal factors also introduce market volatility, as demand for new pool construction and high-end equipment is highly concentrated in specific warmer months, leading to production and supply chain planning complexities for manufacturers and distributors.

Opportunities within the market are abundant, primarily focused on the retrofit and refurbishment segment, where millions of existing pools require modernization to meet current energy and safety standards. The expansion into niche markets, such as specialized water features, therapeutic pools, and sustainable, zero-chemical water treatment, offers avenues for high-margin product differentiation. Furthermore, the proliferation of IoT and connectivity enables manufacturers to develop subscription-based monitoring and maintenance services, moving the business model from one-time equipment sales to continuous value delivery. Impact forces, driven by technological parity, standardization requirements, and competitive pricing pressures, compel manufacturers to innovate rapidly while maintaining high standards of quality and regulatory compliance, particularly regarding safe chemical handling and discharge.

The Swimming Pool Water Treatment Equipment Market is meticulously segmented based on Equipment Type, Chemical Type, Application, and End-User, providing a granular view of market dynamics and consumer preferences across different operational environments. This detailed analysis allows stakeholders to target specific niches, such as high-efficiency filtration solutions for commercial aquatic centers or easy-to-manage chemical dispensers for the residential aftermarket. The segmentation confirms the dominance of the residential sector in volume, while the commercial sector drives demand for complex, high-capacity, and heavily regulated sanitation technologies. Understanding these segments is crucial for strategic pricing and distribution channel optimization.

The Equipment Type segmentation, covering filters, pumps, heaters, and automatic cleaners, remains the bedrock of the market, with ongoing innovation focusing heavily on sustainability and remote management capabilities. The Chemical Type segment illustrates the transition from traditional chlorine dependence towards supplementary or alternative sanitation methods, reflecting health consciousness and environmental accountability. Regional variation in preferred sanitation methods (e.g., higher UV adoption in regulatory-heavy European markets) highlights the necessity for localized product portfolios. End-User differentiation underscores the different operational demands, with public pools requiring fail-safe redundancy and highly accurate monitoring systems, while residential users prioritize simplicity and aesthetic integration.

The value chain for the Swimming Pool Water Treatment Equipment Market begins with raw material suppliers, including manufacturers of specialized plastics (for pump casings and filter bodies), metals (for heat exchangers and motor components), and electronic components (for controllers and sensors). Upstream analysis reveals significant dependence on efficient procurement strategies, as volatility in energy costs and commodity prices directly impacts the manufacturing cost of power-intensive equipment like pumps and heaters. Research and Development activities at this stage focus on material science to improve corrosion resistance, reduce equipment weight, and enhance energy conversion efficiency, establishing the foundational quality of the final product and securing sustainable competitive advantages through proprietary designs.

The midstream involves the core manufacturing, assembly, and integration of components. Equipment manufacturers often specialize in specific categories—such as filtration, circulation, or disinfection—before offering fully integrated systems. Distribution channels are highly critical in this industry. Direct channels are typically utilized for large commercial contracts or high-volume distributors, allowing for greater control over pricing and technical support. Indirect channels, encompassing a wide network of specialized pool builders, contractors, retail dealers, and aftermarket service providers, are crucial for reaching the fragmented residential market and providing localized installation and maintenance services. The efficiency of this distribution network, including logistics for heavy equipment, significantly influences market penetration and customer satisfaction.

Downstream analysis focuses on installation, maintenance, and the relationship with the end-user. Installation is often complex, requiring certified professionals, especially for integrating smart control systems and handling potent disinfection chemicals. The aftermarket service sector is a vital revenue generator, providing necessary replacements (filters, pump parts, chemicals) and specialized technical support. The industry is highly reliant on expert pool technicians and certified dealers who act as crucial intermediaries, influencing purchasing decisions and ensuring the long-term operational integrity of the installed equipment. Value creation is increasingly moving towards service contracts and digital monitoring subscriptions, providing continuous revenue streams long after the initial equipment sale.

The primary customer base for Swimming Pool Water Treatment Equipment is broadly categorized into residential pool owners and commercial aquatic facility operators, each with distinct requirements concerning scale, operational redundancy, and regulatory compliance. Residential users, often prioritizing convenience, energy savings, and ease of maintenance, are key buyers for automated chemical feeders, salt-chlorinators, robotic cleaners, and variable speed pumps. They typically purchase through specialized retail dealers or pool construction companies and are highly responsive to product features that simplify pool care, such as smart controllers integrated with home automation systems, reducing the reliance on constant manual monitoring and chemical testing.

Commercial pool operators constitute the high-value segment, demanding industrial-grade, robust, and highly reliable equipment that can handle extremely high bather loads and meet rigorous public health standards. This group includes hotels, resorts, municipal public pools, water parks, fitness centers, and educational institutions. Their purchasing decisions are driven by total cost of ownership (TCO), operational uptime, redundancy features (e.g., dual pump systems), and the ability to log and report water quality data to regulatory bodies. Commercial buyers often prefer advanced disinfection methods like centralized ozone generation or UV sterilization, complementing chlorine use to minimize combined chlorine issues and enhance public safety.

Additionally, a significant and rapidly expanding customer segment is the refurbishment and retrofit market. Existing pool owners, both residential and commercial, constitute a large pool of potential customers looking to upgrade outdated, energy-intensive equipment to meet modern sustainability mandates or replace aging components. This aftermarket demand is less cyclical than new construction and provides consistent sales opportunities for energy-efficient pumps, modernized filtration media, and smart controllers. Furthermore, specialized end-users, such as hospitals with hydrotherapy pools or specialized aquaculture facilities, require customized, high-precision water treatment systems, representing a niche but high-margin customer group prioritizing sterile and highly stable water quality.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 6.5 Billion |

| Market Forecast in 2033 | USD 9.6 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Pentair, Hayward Industries, Fluidra, Zodiac Pool Systems (a Fluidra subsidiary), Calgon Carbon Corporation, Evoqua Water Technologies, Waterco Ltd., Xylem Inc., Lonza Group, ProMinent, Blue Lagoon UV-C, Maytronics, Speck Pumps, CMP, Dryden Aqua, BioLab, S.R. Smith, AstralPool (a Fluidra subsidiary), DAB Pumps, ChlorKing. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Swimming Pool Water Treatment Equipment Market is undergoing a rapid evolution, primarily driven by three core pillars: automation, energy efficiency, and enhanced non-chemical sanitation. The shift from single-speed to variable speed pumps (VSPs) represents the most significant technological adoption in circulation, with VSPs using advanced motor technology and integrated controls to adjust flow rates dynamically, reducing energy consumption by up to 90% compared to traditional models. Concurrently, filtration technology is advancing with the introduction of glass media and specialized polymer cartridge filters that offer superior particle removal efficiency and reduced backwash frequency, minimizing water waste and enhancing operational sustainability, making them highly desirable in water-scarce regions.

In the disinfection sector, the market is moving beyond heavy reliance on traditional chemical methods. Key innovations include advanced oxidation processes (AOPs), which combine UV light, ozone, and often hydrogen peroxide to destroy pathogens and organic matter, yielding superior water quality with minimal chemical byproducts like chloramines. Salt-chlorine generation technology continues to mature, offering residential users a convenient, automated, and continuous supply of chlorine produced on-site. Furthermore, the development of sophisticated sensors and controllers utilizing photometers and specialized electrodes allows for continuous, high-precision measurement of pH, ORP (Oxidation-Reduction Potential), and free chlorine levels, enabling automated dosing systems to maintain optimal water chemistry more effectively than ever before, thereby minimizing human error.

The convergence of the pool industry with the broader smart home technology ecosystem is the most transformative trend. Modern controllers are equipped with Wi-Fi and Bluetooth connectivity, allowing owners to manage all pool functions—from heating and lighting to pump schedules and chemical balance—via mobile applications. This Internet of Things (IoT) integration enables remote diagnostics and predictive maintenance by service providers, creating new service revenue models. Future technological developments are anticipated to focus heavily on integrating AI and machine learning into these smart controllers to optimize performance based on real-time environmental factors and usage patterns, guaranteeing maximum energy savings and minimal chemical usage while ensuring compliance with stringent health standards.

Regional analysis confirms that market maturity and growth potential vary significantly across geographies, influenced primarily by climate, regulatory stringency, disposable income, and tourism dependency. North America, encompassing the United States and Canada, represents the largest and most technologically advanced market. This dominance is driven by high per capita pool ownership, a large existing installed base demanding frequent replacement and upgrades (especially to VSPs and smart automation), and strong regulatory enforcement concerning both water quality and energy efficiency standards. Consumers in this region readily adopt premium products like robotic cleaners and integrated smart systems, resulting in a high average equipment value.

Europe holds a substantial market share, characterized by diverse regional preferences and stringent environmental regulations. Countries in Southern Europe (Spain, France, Italy) benefit from favorable climates leading to high pool usage and construction rates, favoring traditional equipment but rapidly adopting energy-saving heat pumps. Conversely, Northern and Central European countries focus heavily on indoor pools and specialized water treatment solutions, prioritizing UV and ozone systems to minimize chemical usage. European policy initiatives, such as the push for energy reduction, heavily influence procurement decisions, accelerating the adoption of high-efficiency components across the commercial sector.

The Asia Pacific (APAC) region is projected to register the fastest growth rate during the forecast period. This growth is underpinned by booming real estate development, rising urbanization, and the proliferation of luxury resorts and residential complexes in coastal areas of China, Australia, and Southeast Asia. While cost sensitivity remains a factor in certain developing APAC nations, the commercial segment (hotels, public facilities) is quickly adopting advanced filtration and disinfection systems to meet international tourism standards. This region represents a massive opportunity for manufacturers providing scaled solutions and integrating localized, reliable service networks to handle the influx of new installations, particularly in high-density urban environments demanding reliable and compact treatment systems.

The primary driver for VSP adoption is the significant reduction in operational electricity costs and the push for greater energy efficiency, mandated by regulations in key markets like North America and Europe. VSPs automatically adjust flow rates based on demand, leading to energy savings of up to 90% compared to traditional single-speed pumps, alongside offering quieter operation and prolonged equipment lifespan, appealing directly to environmentally conscious consumers and operators focused on long-term operational savings.

AI and IoT technologies are integrating smart sensors and controllers that provide continuous, real-time monitoring of water parameters (pH, ORP, chlorine levels). AI algorithms use this data, combined with usage patterns and weather information, to calculate and automatically dispense the precise chemical dose required. This transformation ensures consistently balanced water chemistry, minimizes chemical waste and human handling errors, and enhances bather safety through immediate anomaly detection, moving chemical management from reactive testing to proactive automation.

Advanced non-traditional disinfection systems, particularly UV (Ultraviolet) and Ozone systems, are projected to experience the fastest growth, especially in the commercial sector. These technologies effectively neutralize chlorine-resistant pathogens and reduce the formation of irritating chloramines, offering superior water quality with reduced dependency on high levels of residual chlorine. Salt-chlorine generators also show robust growth in the residential segment due to their convenience and softer water feel, but UV and Ozone systems dominate the high-end commercial market growth.

Residential pools prioritize user convenience, aesthetic integration, and energy efficiency (e.g., VSPs, robotic cleaners). Commercial pools, conversely, require equipment built for high bather loads, 24/7 reliability, and strict regulatory compliance. Commercial systems are characterized by greater redundancy (backup pumps/filters), large-capacity filtration systems, highly accurate automated chemical controllers, and often utilize secondary disinfection methods like UV or ozone for fail-safe microbial control, leading to higher initial investment costs and more complex maintenance protocols.

The primary restraint is the significant upfront capital investment required for advanced equipment such as fully automated controllers, high-capacity UV systems, and premium VSPs, particularly for residential buyers and small-to-medium commercial facilities. Additionally, the complexity of installation and maintenance necessitates specialized technical labor, which can be scarce or expensive in certain regions. Market growth is also restrained by consumer hesitation regarding the integration complexity of new smart technologies with existing legacy pool infrastructure.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.