ID : MRU_ 434124 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

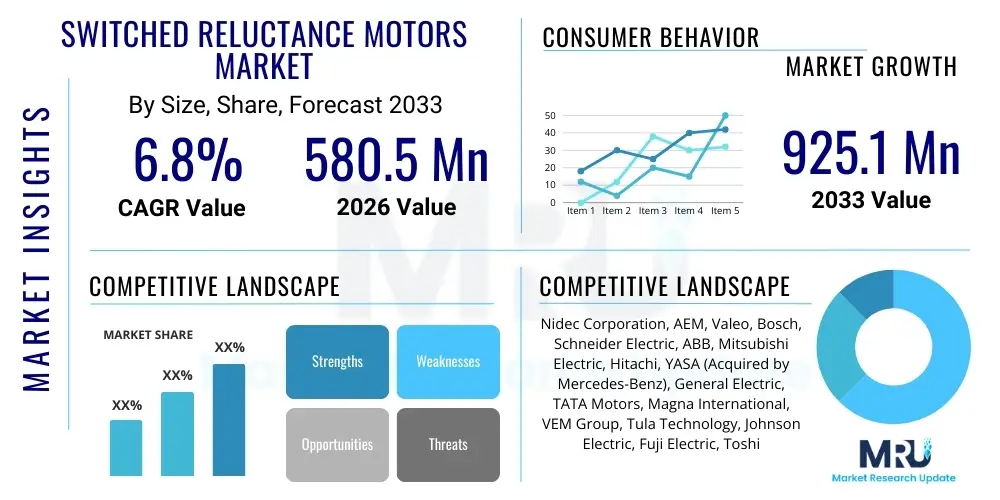

The Switched Reluctance Motors Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 580.5 Million in 2026 and is projected to reach USD 925.1 Million by the end of the forecast period in 2033.

The Switched Reluctance Motor (SRM) market is experiencing robust growth driven primarily by the escalating demand for high-efficiency and robust motor solutions across various industrial and automotive applications. SRMs are characterized by their simple, durable construction, featuring no windings or magnets on the rotor, which significantly reduces manufacturing complexity and material costs compared to traditional AC induction motors or permanent magnet synchronous motors (PMSMs). This structural advantage provides inherent reliability, particularly in harsh operating environments such as high temperatures or vibrational stress, making them increasingly attractive for heavy-duty industrial machinery and emerging electrification initiatives.

Key applications driving market penetration include the rapidly expanding electric vehicle (EV) sector, where the magnet-free design of SRMs mitigates reliance on increasingly volatile rare-earth element supply chains. Furthermore, SRMs are gaining traction in variable speed applications, such as pumps, fans, compressors, and heating, ventilation, and air conditioning (HVAC) systems, due to their wide speed range capabilities and operational resilience. Their ability to maintain high efficiency across diverse load conditions contributes directly to reduced energy consumption, aligning with global energy efficiency standards and sustainability mandates.

The principal benefits propelling the adoption of SRMs include superior fault tolerance, lower inertia, and simplified thermal management. These benefits, combined with advancements in power electronics and control algorithms—which historically posed challenges for SRM drive systems—have unlocked new performance envelopes. Driving factors for the market include stringent regulatory pressures concerning motor efficiency (e.g., IE4/IE5 standards), the ongoing global transition towards electric mobility, and the continuous need for reliable, cost-effective industrial automation solutions capable of operating under extreme conditions.

The Switched Reluctance Motors (SRM) market is poised for significant expansion, characterized by crucial business, regional, and segmental shifts. Business trends indicate a focus on refining control system complexity and integrating advanced digital signal processors (DSPs) to optimize torque ripple and acoustic noise, addressing historical drawbacks of SRM technology. Major manufacturers are investing heavily in prototyping and scaling production facilities, particularly in response to the massive demand surge from the automotive sector for reliable, magnet-free traction motors. Strategic partnerships between motor producers and EV manufacturers, along with acquisitions targeting specialized power electronics firms, define the current competitive landscape, aiming to establish comprehensive drivetrain solutions.

Regionally, the Asia Pacific (APAC) stands out as the primary growth engine, fueled by extensive manufacturing capabilities, rapid industrialization, and aggressive governmental policies promoting EV adoption, notably in China and India. North America and Europe are focusing on high-performance industrial applications and aerospace, where the reliability and fault tolerance of SRMs offer distinct advantages. The European market, in particular, benefits from rigorous energy efficiency directives, making SRMs a preferred alternative in high-efficiency industrial pump and fan systems. Infrastructure investment in smart factories and renewable energy installations further solidifies regional market growth.

Segmentally, the market is predominantly segmented by power rating, application, and type. The High-Power segment (> 75 kW) is expected to exhibit the highest CAGR, primarily due to its pivotal role in commercial vehicles, heavy machinery, and high-performance industrial drives. Within applications, the Automotive segment, particularly Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs), dominates market share, promising sustained double-digit growth. The trend within product type leans towards High-Performance SRMs, which incorporate advanced winding configurations and optimized stator geometries to maximize power density and minimize operational noise, thereby bridging the performance gap with PMSMs in critical applications.

User queries regarding the influence of Artificial Intelligence (AI) on the Switched Reluctance Motors (SRM) market frequently revolve around how AI can resolve the long-standing challenges associated with SRM operation, specifically torque ripple mitigation, acoustic noise reduction, and enhancing overall system efficiency under transient conditions. Users are keen to understand the practical applications of machine learning in optimizing SRM control algorithms, predicting motor faults before failure occurs, and facilitating design optimization during the R&D phase. The consensus theme is the expectation that AI and machine learning (ML) will elevate SRMs from niche technology into mainstream adoption by solving the complex control challenges that traditional techniques struggle with, thereby unlocking the full potential of these robust motors in high-demand sectors like electric mobility and industrial automation.

AI's role is transformative, moving beyond simple parameter calibration to predictive modeling and real-time operational optimization. ML algorithms are being deployed to learn the non-linear characteristics of SRM magnetic circuits and mechanical dynamics. This deep learning approach allows the drive system to anticipate and counteract inherent torque ripple by precisely adjusting switching angles and current waveforms in microseconds, leading to smoother operation and reduced vibrations. Furthermore, predictive maintenance models, trained on large datasets of operational telemetry, allow industrial users to schedule maintenance proactively, minimizing downtime and extending the lifespan of critical machinery powered by SRMs. This capability enhances the overall value proposition of SRMs in factory automation settings.

The integration of AI also fundamentally shifts the design process. Generative design tools, powered by AI, can rapidly iterate through thousands of potential stator and rotor geometries, magnetizing curve parameters, and winding configurations. This significantly reduces the time and cost associated with optimizing SRMs for specific application requirements, such as maximizing power density for EVs or ensuring efficiency at partial loads for HVAC systems. By enabling higher precision control and fault prediction, AI addresses the complexity barrier that previously limited widespread SRM adoption, positioning the technology as a strong competitor to conventional motor technologies in the era of smart, connected industrial systems and autonomous vehicles.

The Switched Reluctance Motors (SRM) market dynamics are shaped by a complex interplay of Drivers, Restraints, and Opportunities (DRO), collectively forming significant impact forces. A primary driver is the accelerating global shift towards electric mobility, where the inherent durability and magnet-free design of SRMs offer a compelling, cost-stable alternative to Permanent Magnet Synchronous Motors (PMSMs), which are vulnerable to rare-earth supply chain volatility. Coupled with this is the rigorous enforcement of industrial energy efficiency standards (IE4 and IE5), compelling manufacturers across various sectors to adopt motor technologies capable of higher efficiencies, especially in variable speed operations common in HVAC and fluid handling systems. These drivers collectively push for technological adoption and scale-up.

Conversely, the market faces significant restraints, primarily centered around the historical challenges associated with high torque ripple and substantial acoustic noise generated during operation. Although modern control techniques mitigate these issues, the perception of SRMs as noisy and complex to control persists in some end-user segments, slowing broader acceptance. Furthermore, the reliance on sophisticated, high-performance power electronics and digital controllers significantly increases the cost and complexity of the drive system compared to simpler induction motor drives, presenting a barrier to entry, particularly for smaller-scale industrial applications where cost sensitivity is high. Overcoming this complexity hurdle requires continuous advancements in integrated power modules and standardized control platforms.

Opportunities for market expansion are vast and primarily reside in exploiting the unique characteristics of SRMs in underserved or high-demand sectors. The robust nature of SRMs makes them ideal for specialized military, aerospace, and high-temperature industrial environments where permanent magnets might demagnetize or windings might fail. Moreover, the decentralization of renewable energy systems, necessitating reliable, variable-speed generators and pump motors, opens significant avenues. The most critical opportunity lies in leveraging advancements in AI-driven control to entirely neutralize the traditional drawbacks (noise and ripple), thereby establishing SRMs as a high-performance, cost-effective standard for next-generation electric powertrains and industrial drives. These forces dictate investment cycles and product development priorities across the global market.

The Switched Reluctance Motors (SRM) market is structurally segmented to reflect variations in power demand, intended application environment, and technological sophistication. Key segmentation variables include Power Rating, which dictates the end-use scope from small consumer electronics to heavy industrial machinery; Application, focusing heavily on the automotive and industrial sectors; and Type, distinguishing between standard designs and high-performance variants optimized for specific characteristics. Understanding these segments is crucial for market participants to tailor product development, pricing strategies, and distribution channels, ensuring alignment with diverse global industrial and mobility requirements. The inherent versatility of SRMs allows them to be customized effectively across these distinct categories, catering to varying needs for efficiency, ruggedness, and cost effectiveness.

The segmentation by power rating serves as a critical differentiator in market strategy. Low Power SRMs (typically under 15 kW) are essential in small appliances, power tools, and certain light industrial equipment where energy efficiency at variable speeds is paramount but cost pressures are relatively high. Medium Power SRMs (15 kW to 75 kW) form the backbone of general industrial automation, powering critical components such as pumps, fans, and compressors in commercial HVAC and manufacturing environments. High Power SRMs (over 75 kW) target heavy-duty applications, including electric buses, commercial vehicles, large marine propulsion systems, and heavy-duty industrial process machinery, where high torque density and extreme reliability are non-negotiable requirements.

Application-wise, the Automotive sector represents the most lucrative segment due to the transition to electromobility. SRMs are utilized in traction drives for electric vehicles (EVs), hybrid electric vehicles (HEVs), and ancillary systems like electric power steering and vacuum pumps. The Industrial segment remains vital, demanding SRMs for critical process control, robotics, and machinery drives. Furthermore, specialized segments like Aerospace and Defense, leveraging the high fault tolerance and ruggedness of SRMs, present significant opportunities for premium-priced solutions. The continued evolution of these segments necessitates ongoing innovation in motor design and control technologies to maximize performance across this broad spectrum of applications.

The value chain for the Switched Reluctance Motors (SRM) market commences with the upstream analysis, focusing heavily on raw material procurement, particularly specialized electrical steel (silicon steel laminations) necessary for the stator and rotor core, and copper for the stator windings. Unlike PMSMs, the upstream stage benefits from avoiding rare-earth magnet sourcing, mitigating significant geopolitical and commodity price risks. However, the quality and specification of the electrical steel are critical as they directly influence the motor's magnetic performance and efficiency. Key upstream suppliers include steel manufacturers and specialized winding component providers. Efficiency gains in this stage are tied to advanced material science and automated coil winding techniques.

The midstream of the value chain involves core manufacturing activities: motor design, core lamination stamping, coil winding, assembly, and integration of the power electronics drive unit. This stage is highly technologically intensive, requiring specialized expertise in magnetic circuit design and the production of high-precision components. The complexity of the drive electronics—which involves IGBTs or MOSFETs, sensors, and the critical control unit (often based on DSPs or microcontrollers)—demands a strong focus on semiconductor sourcing and firmware development. Direct manufacturing generally handles high-volume standard units, while specialized engineering firms often cater to customized, high-performance, or low-volume requirements for aerospace or defense applications.

The downstream analysis involves distribution, sales, integration, and aftermarket services. Distribution channels are typically bifurcated into direct sales to large Original Equipment Manufacturers (OEMs), particularly in the automotive and heavy industrial sectors, and indirect channels utilizing distributors and system integrators for general industrial clients and smaller businesses. System integrators play a vital role, especially when SRMs are replacing existing motor technologies, requiring specialized installation and commissioning support. Aftermarket services, including maintenance, spare parts supply, and software updates for the control system, contribute significantly to the overall revenue pool and customer loyalty, given the technological sophistication of SRM drives.

Potential customers for Switched Reluctance Motors span a wide spectrum of industries characterized by a high need for energy efficiency, durability, and robust operation in demanding environments. The primary end-users are Original Equipment Manufacturers (OEMs) in the automotive industry, specifically manufacturers of Electric Vehicles (EVs), Plug-in Hybrid Electric Vehicles (PHEVs), and ancillary EV component suppliers who seek alternatives to permanent magnet motors for traction applications, driven by cost stability and safety considerations. These buyers prioritize high torque density and fault tolerance crucial for powertrain reliability and performance across diverse driving conditions. The shift towards greater electrification ensures sustained demand from this cohort.

Another major group of potential customers comprises heavy industrial machinery manufacturers and process control operators. This includes OEMs producing large pumps, high-speed compressors, industrial fans, textile machinery, and machine tools. For these customers, the key purchasing criteria revolve around the SRM's ability to operate efficiently at variable speeds, its inherent ruggedness, and its long operational life, which minimizes maintenance downtime. Companies involved in chemical processing, mining, and oil and gas extraction, where motors often face high heat and corrosive environments, are particularly strong buyers due to the SRM's minimal reliance on rotor windings and magnets, which are prone to failure under extreme stress.

Furthermore, specialized sectors such as the Aerospace and Defense industry, along with specialized HVAC system manufacturers, represent crucial niche buyers. Aerospace users leverage the SRM's fault-tolerant nature for critical applications like actuators and environmental control systems, where failure is unacceptable. HVAC buyers, particularly those focusing on commercial and large-scale industrial heating and cooling, are increasingly adopting SRMs to comply with stringent energy efficiency regulations, making them attractive end-users focused on long-term operational cost savings and sustainability metrics.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 580.5 Million |

| Market Forecast in 2033 | USD 925.1 Million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Nidec Corporation, AEM, Valeo, Bosch, Schneider Electric, ABB, Mitsubishi Electric, Hitachi, YASA (Acquired by Mercedes-Benz), General Electric, TATA Motors, Magna International, VEM Group, Tula Technology, Johnson Electric, Fuji Electric, Toshiba, Parker Hannifin, Brook Crompton, Regal Rexnord |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Switched Reluctance Motors (SRM) market is currently dominated by advancements focused on mitigating their inherent control drawbacks and maximizing power density for competitive applications, particularly electric vehicles. Core innovations revolve around sophisticated power electronics and high-speed digital control systems. The development of advanced asymmetrical bridge converters, often utilizing Silicon Carbide (SiC) and Gallium Nitride (GaN) power modules, is critical. These wide-bandgap semiconductors enable faster switching speeds, higher operational temperatures, and significantly reduced losses compared to traditional Silicon-based IGBTs, allowing the drive system to respond rapidly to control inputs, which is essential for minimizing torque ripple and acoustic noise generation.

Further technological progress is evident in the area of sensing and control algorithms. High-resolution position sensors and advanced sensorless control techniques are fundamental to the accurate commutation of current in SRMs, which directly impacts efficiency and noise levels. Modern control schemes increasingly incorporate Artificial Intelligence (AI) and Machine Learning (ML) to implement predictive and adaptive control strategies. These AI-driven algorithms move beyond lookup tables, optimizing current excitation profiles in real-time based on fluctuating load conditions and magnetic saturation effects. This technological refinement is crucial for elevating SRM performance to levels competitive with PMSMs in demanding applications like automotive traction.

Material and structural innovations also play a significant role. Manufacturers are utilizing advanced lamination stamping techniques and specialized electrical steel with enhanced magnetic properties to reduce core losses and maximize torque per unit volume. Furthermore, the integration of specialized thermal management systems, including sophisticated cooling jackets and optimization of winding insulation materials, allows High-Performance SRMs to operate reliably at higher temperatures and current densities. The combination of high-speed electronics, AI control, and optimized material usage defines the cutting edge of SRM technology, facilitating adoption in high-reliability, high-power-density sectors.

Regional dynamics are instrumental in shaping the adoption and growth trajectory of the Switched Reluctance Motors (SRM) market, reflecting varying levels of industrialization, regulatory pressures, and investment in electric mobility infrastructure. Asia Pacific (APAC) holds the dominant market position, largely due to the sheer volume of manufacturing activity, especially in China, which serves as a global hub for industrial machinery and is rapidly accelerating its Electric Vehicle (EV) production targets. Government subsidies and stringent mandates for industrial energy efficiency further bolster the demand for efficient SRM technology in large-scale manufacturing and commercial applications across the region, including India, Japan, and South Korea.

Europe represents a mature market characterized by a strong emphasis on high performance and energy conservation. Strict regulatory frameworks, such as the Ecodesign Directive, mandate high efficiency (IE4 and above) for industrial motors, creating a favorable environment for the adoption of SRMs in HVAC systems, pumps, and fans. European automotive manufacturers and Tier 1 suppliers are heavily invested in researching SRMs as a rare-earth-free alternative for future EV platforms, with innovation often centered in Germany and France. The focus here is balanced between achieving ultra-high efficiency and mastering noise reduction for passenger vehicles.

North America is steadily increasing its adoption of SRMs, driven by significant investment in industrial automation, specialized high-reliability applications (aerospace and defense), and the burgeoning domestic EV market. While traditional AC induction motors still dominate general industry, the robust nature of SRMs appeals to heavy industrial users (mining, oil and gas) and specialized military applications where maintenance costs are high and operational reliability is critical. Government initiatives supporting manufacturing revitalization and electrification across commercial fleets provide sustained momentum, positioning North America for accelerated growth over the forecast period, particularly in the high-power segment.

SRMs offer several key advantages including a magnet-free design, eliminating reliance on expensive and volatile rare-earth elements. They possess superior mechanical ruggedness, inherent fault tolerance, and simpler, cheaper rotor construction, making them highly reliable in harsh operating conditions compared to PMSMs.

SRMs are attractive for EVs because their robust, magnet-free structure ensures supply chain stability and reduces costs. Furthermore, their high efficiency over a wide speed range and excellent fault tolerance are crucial for reliable and cost-effective automotive traction drive systems, addressing long-term sustainability goals.

The main technical challenges historically include high torque ripple, significant acoustic noise during operation, and the necessity for complex, high-performance power electronics and sophisticated digital control algorithms to manage commutation and maintain optimal efficiency.

AI integration fundamentally improves SRM performance by enabling advanced, real-time control algorithms that dynamically adjust switching patterns. This optimization drastically reduces torque ripple and acoustic noise, overcoming the motor's traditional drawbacks and enhancing overall efficiency and operational smoothness.

The High Power segment (Greater than 75 kW) is projected to experience the fastest growth. This is driven by their application in heavy-duty commercial vehicles, large industrial processes, and high-performance electric machinery requiring maximum torque density and superior reliability under extreme load conditions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.