ID : MRU_ 436929 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

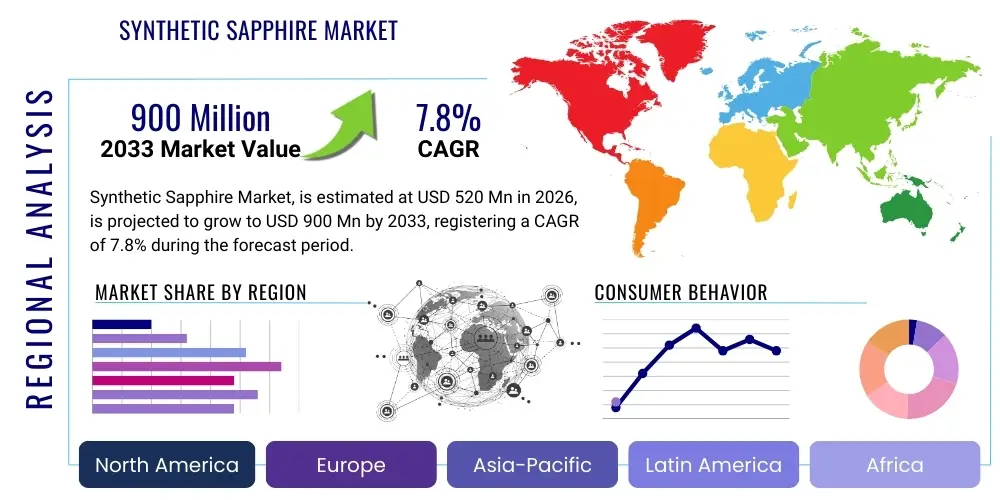

The Synthetic Sapphire Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 520 million in 2026 and is projected to reach USD 900 million by the end of the forecast period in 2033. This substantial growth trajectory is primarily driven by the escalating demand from the consumer electronics sector, particularly for scratch-resistant covers in smartphones and high-end watches, coupled with rapid advancements in LED lighting technology globally. The market size reflects significant investment in advanced manufacturing techniques, such as the Kyropoulos method and the Czochralski process, ensuring high-quality, large-diameter sapphire substrates necessary for next-generation microelectronic applications.

The market valuation underscores the indispensable role synthetic sapphire plays across various high-performance industries where material strength, thermal stability, and optical transparency are paramount. Factors such as the expansion of solid-state lighting (SSL) technologies, where sapphire substrates are critical for Gallium Nitride (GaN)-based LEDs, contribute profoundly to market expansion. Furthermore, the defense and aerospace industries rely on synthetic sapphire for robust optical windows and sensor protection, demanding materials that withstand extreme environmental conditions, thereby cementing the market's strong financial outlook over the next seven years.

The Synthetic Sapphire Market encompasses the production, distribution, and utilization of laboratory-grown aluminum oxide (Al2O3) crystals, which possess the identical chemical and physical properties of natural sapphire but are manufactured under controlled conditions. This highly versatile material is characterized by extreme hardness, exceptional thermal conductivity, high melting point, and excellent transparency across a broad spectrum of light, making it suitable for demanding technical applications. It is chemically inert and possesses high mechanical strength, surpassing traditional materials like glass or quartz in durability and performance. The production processes, including the Kyropoulos method, Czochralski method, and Edge-defined Film-fed Growth (EFG), have been optimized to create large, high-purity boules required for industrial scaling.

Major applications of synthetic sapphire span substrate material for LEDs and microelectronics, protective covers and components in consumer electronics (smartwatches, phone cameras), high-pressure viewports, precision optics, and medical devices. Its superior hardness (9 on the Mohs scale) and chemical resistance offer significant benefits over alternatives, particularly in environments requiring longevity and scratch resistance. The primary driving factors for market growth include the global transition towards energy-efficient LED lighting, the miniaturization and increased sophistication of consumer electronic devices, and growing requirements from military and aerospace sectors for durable optical windows and infrared systems.

The Synthetic Sapphire Market is poised for robust expansion, primarily steered by accelerating demand in the optoelectronics and consumer electronics domains. Business trends indicate a strong shift towards larger diameter wafers (6-inch and 8-inch) to improve economies of scale in LED and semiconductor manufacturing, prompting key players to invest heavily in advanced crystal growth furnaces and post-processing capabilities. Technological improvements in crystal growth methods, focusing on reducing internal defects and increasing yield rates, are critical competitive differentiators. Furthermore, the market exhibits intense integration across the value chain, as substrate manufacturers increasingly collaborate with LED fabricators to secure long-term supply agreements and standardize substrate specifications, ensuring seamless material integration and stability of supply.

Regionally, the Asia Pacific (APAC) dominates the market, largely due to the massive concentration of LED production facilities, particularly in China, South Korea, and Taiwan, coupled with the world’s largest consumer electronics manufacturing base. North America and Europe also contribute significantly, driven by specialized demand from high-reliability applications, including military optics, medical instruments, and advanced semiconductor packaging. Segment trends highlight that LED substrates remain the largest revenue generator, while the demand for sapphire components in consumer electronics, especially camera lens covers and watch faces, is demonstrating the fastest CAGR, driven by consumers' willingness to pay a premium for enhanced device durability and aesthetic appeal, necessitating high-volume production of near-net-shape components.

Common user questions regarding AI's impact on the Synthetic Sapphire Market frequently revolve around optimizing complex manufacturing processes, predicting crystal quality, and reducing material waste during slicing and polishing. Users seek clarity on how AI-driven predictive maintenance can minimize furnace downtime and whether machine learning algorithms can enhance the yield of large-diameter boules. Key themes emerging from this analysis include the expectation of using AI to refine temperature gradient control and growth rate management within Kyropoulos furnaces, which are highly sensitive to variations, ultimately aiming for superior crystalline uniformity and reduced defect density. The primary concerns relate to the significant initial investment required for integrating sophisticated sensors and AI infrastructure into existing, often traditional, crystal growth environments, alongside the need for specialized data scientists capable of analyzing complex crystallography datasets.

AI's influence is anticipated to revolutionize the synthetic sapphire fabrication workflow by moving from reactive quality control to predictive process adjustments. Machine learning models, trained on real-time data collected from thousands of growth cycles, can identify subtle correlations between process parameters (like melt level, rotation speed, and thermal gradients) and resultant crystalline imperfections. This proactive approach ensures optimal growth conditions throughout the multi-week crystallization period, dramatically improving yield and consistency, particularly for high-purity, optical-grade sapphire. Furthermore, AI is crucial in optimizing the computationally intensive simulation of thermal fields used in designing new furnace architectures, leading to faster prototyping and deployment of more efficient crystal growth systems globally.

The Synthetic Sapphire Market is profoundly influenced by a complex interplay of drivers (D), restraints (R), and opportunities (O), which collectively shape the impact forces (I). Key drivers include the overwhelming global adoption of LED lighting technology, which necessitates massive quantities of sapphire substrates, coupled with the increasing integration of sapphire components into premium consumer electronic devices for enhanced durability. Conversely, significant restraints involve the extremely high energy consumption and capital expenditure required for growing large sapphire crystals, leading to high manufacturing costs, along with the intense market competition from alternative substrate materials like Silicon Carbide (SiC) and Silicon-on-Sapphire (SOS) for specific semiconductor applications. These forces define the competitive landscape and strategic investment decisions within the market.

Opportunities for market expansion are centered on the burgeoning market for advanced semiconductor devices, specifically in power electronics and RF components utilizing GaN-on-Sapphire technology, driven by 5G network expansion and electric vehicle adoption. The development of advanced, low-cost crystal growth techniques that reduce operational expenses, such as improved heat exchange methods, presents a crucial opportunity for manufacturers to increase margin and market penetration. The overall impact forces are high, primarily driven by the inelastic demand from the indispensable LED sector and the ongoing technological push in consumer electronics toward durable, high-specification materials, which consistently outweigh the restrictive factors related to manufacturing complexity and cost.

The Synthetic Sapphire Market is structurally segmented based on crucial attributes including material production method, product type, end-use application, and geographic region. This multi-dimensional segmentation facilitates precise market analysis, enabling stakeholders to identify high-growth areas and tailor their operational strategies accordingly. The differentiation based on manufacturing method—primarily Kyropoulos, Czochralski, and EFG—highlights the technological preferences of producers for specific quality characteristics and wafer sizes, directly impacting the cost structure and final application suitability. Product types, such as windows, tubes, lenses, and various substrates, cater to specialized needs across optics and electronics. The segmentation underscores the diverse utility of synthetic sapphire, moving beyond traditional applications into next-generation high-performance electronic devices and sophisticated optical systems, which increasingly demand materials with specific structural integrity and purity levels.

The value chain of the Synthetic Sapphire Market begins with upstream activities focused on securing and purifying raw materials, primarily high-purity alumina powder (Al2O3). This initial phase is crucial, as the quality of the source material directly dictates the crystalline perfection of the final sapphire boule. Key upstream suppliers include specialized chemical and material processing companies that guarantee the required 99.999% purity level. Following material preparation, the manufacturing process involves significant capital investment in energy-intensive crystal growth furnaces (Kyropoulos or HEM), where the crystalline structure is formed under precise thermal and pressure controls. This core manufacturing stage determines the yield, size, and defect concentration of the sapphire boules, representing the highest value addition point in the chain.

The midstream process involves highly specialized cutting, slicing, grinding, and polishing (CGP) activities to transform the raw sapphire boule into usable components, such as thin wafers (substrates) or optical windows. This stage is technically demanding due to sapphire's extreme hardness, requiring diamond-coated tools and advanced lapping techniques, often resulting in significant kerf loss (material wastage) which affects final production costs. Downstream activities involve the integration of these components into end products. For instance, sapphire substrates are sold to LED manufacturers (Epiwafer fabricators) who deposit Gallium Nitride layers, while optical components are supplied to laser or defense contractors. The distribution channel is predominantly direct for large-volume industrial buyers, ensuring technical specification compliance, while smaller, specialized components might utilize indirect channels through distributors or specialized component integrators.

Potential customers for synthetic sapphire are highly concentrated in technological and high-durability dependent industries that require materials offering superior mechanical, thermal, and optical properties unattainable with standard glass or plastics. The largest volume consumers are manufacturers of Light Emitting Diodes (LEDs), where sapphire substrates serve as the fundamental platform for epitaxially growing Gallium Nitride films essential for solid-state lighting. These customers are driven by the need for consistency, large wafer sizes, and competitive pricing in a highly commoditized lighting market. The second significant customer group comprises major global consumer electronics original equipment manufacturers (OEMs) and their suppliers, utilizing sapphire for scratch-resistant camera lens covers, watch faces, and specialized touch sensors, prioritizing material resilience and aesthetic quality.

Beyond high-volume electronics, the defense and aerospace sectors constitute a niche but high-value customer base, purchasing sapphire for applications requiring extreme environmental tolerance, such as rugged optical windows for infrared (IR) guidance systems, sensor covers in satellites, and high-pressure viewports in underwater vehicles. These customers demand the highest purity and specific optical transmission characteristics. Additionally, the medical device industry uses synthetic sapphire for specialized components in surgical instruments, endoscopes, and laser delivery systems where biocompatibility, inertness, and high wear resistance are critical performance criteria. These diverse end-user requirements underscore the need for customizable product formats and stringent quality control protocols throughout the supply chain.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 520 Million |

| Market Forecast in 2033 | USD 900 Million |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Rubicon Technology, Monocrystal, Saint-Gobain, Kyocera, Precision Sapphire Technologies, Rofin-Sinar Technologies, Lihua Group, GT Advanced Technologies, Crystalwise Technology, Silian Crystal Tech, Zhejiang Crystal-Optech, Rayotek Scientific, DK AZUR, Harris Corporation, CoorsTek, II-VI Incorporated (now Coherent), Schott AG, CERAMTEC, Meller Optics, SCHOTT North America. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Synthetic Sapphire market is defined by several advanced crystal growth technologies, each yielding slightly different crystalline properties and cost structures. The Kyropoulos (KY) method is currently the predominant technique for mass-producing large-diameter sapphire boules, particularly for LED substrates. It involves cooling a melt of high-purity alumina from the bottom up, facilitating the growth of large, high-quality, and low-stress crystals. This method offers excellent cost-effectiveness for large volumes, but requires precise thermal control over multi-week growth cycles. The Heat Exchanger Method (HEM) is another widely adopted process, known for producing high-quality optical-grade sapphire with minimal defects and high homogeneity, often preferred for critical defense and aerospace applications where optical clarity is paramount, though it typically involves higher energy usage per unit of output compared to KY.

The Edge-defined Film-fed Growth (EFG) method, along with the Stepanov technique, is specialized for growing sapphire components in specific shapes, such as rods, tubes, or predetermined profiles, minimizing the need for extensive post-growth machining. EFG is less ideal for large-diameter wafers but excels in creating near-net-shape components used extensively in medical equipment and certain consumer electronics elements, maximizing material yield. Technological innovation is focused heavily on improving the size of the boules, moving from 2-inch to 6-inch and 8-inch substrates to meet semiconductor industry demands, thereby reducing the cost per unit area. Furthermore, advancements in specialized post-growth processing, including laser slicing techniques that drastically reduce kerf loss compared to traditional wire sawing, are transforming the economic viability of high-volume production.

The predominant driver is the massive global adoption and ongoing technological evolution of Light Emitting Diode (LED) lighting, where synthetic sapphire substrates are indispensable for the efficient growth of Gallium Nitride (GaN) epitaxial layers.

Synthetic sapphire offers superior hardness (9 Mohs) and scratch resistance compared to chemically strengthened glasses (typically 6-7 Mohs). While sapphire is significantly more expensive and heavier, it provides unmatched durability crucial for premium device components and critical optical windows.

The Kyropoulos (KY) method currently dominates the market for LED substrate production due to its ability to cost-effectively grow large-diameter, high-quality sapphire boules necessary for scaling up epitaxial wafer fabrication processes.

The principal restraint is the high cost associated with manufacturing, primarily driven by the extremely high capital expenditure required for crystal growth furnaces and the intensive energy consumption inherent in the prolonged, high-temperature crystallization process.

The Consumer Electronics segment, specifically for components like smartphone camera lens covers, smart watch crystals, and specialized sensors, is exhibiting the fastest growth due to the consumer preference for premium, scratch-resistant device protection.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.