ID : MRU_ 432782 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

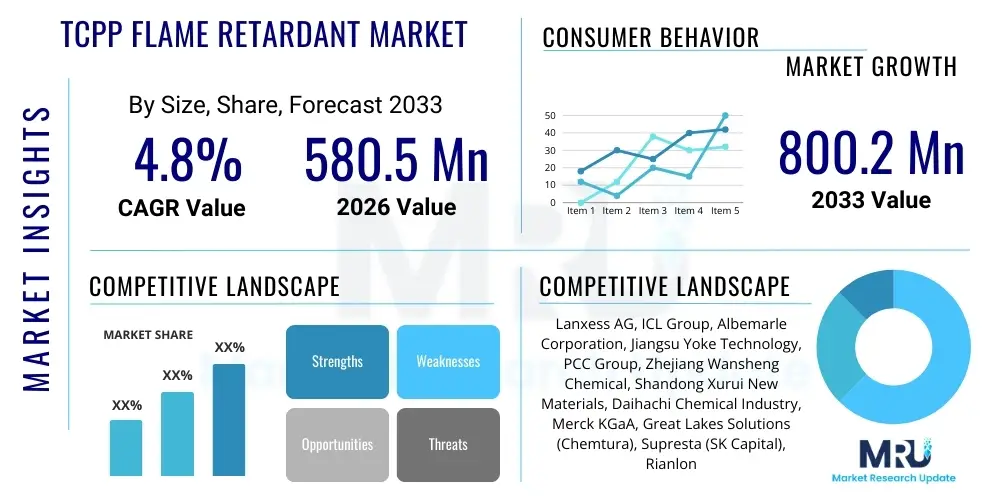

The TCPP Flame Retardant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 580.5 Million in 2026 and is projected to reach USD 800.2 Million by the end of the forecast period in 2033.

The TCPP (Tris(2-chloro-1-methylethyl) phosphate) Flame Retardant Market encompasses the production, distribution, and consumption of this organophosphorus compound primarily utilized to enhance the fire safety characteristics of various polymeric materials. TCPP is classified as a halogenated organophosphate, known for its effectiveness in the condensed phase mechanism of flame retardation, which allows it to interrupt the combustion process by forming a protective char layer and reducing the release of flammable gases. Its exceptional cost-performance ratio and compatibility with diverse polymer matrices, especially polyurethane (PU) foams, render it a staple chemical in the construction, automotive, and electronics sectors. The intrinsic chemical structure of TCPP provides high thermal stability and low volatility, crucial attributes for long-term incorporation into rigid and flexible foams used extensively for insulation purposes.

The primary applications driving the demand for TCPP include rigid polyurethane foams used in building insulation, flexible PU foams employed in furniture and bedding, and various coatings and adhesives. In the construction industry, stringent fire safety codes, particularly in developed economies, necessitate the incorporation of reliable flame retardants into insulating materials, making TCPP a preferred choice due to its effectiveness in achieving standards like ASTM E84 and EN 13501. Moreover, the global shift towards energy-efficient building standards directly correlates with increased demand for highly effective thermal insulation, thereby underpinning the continuous market growth for TCPP. Despite regulatory scrutiny regarding certain halogenated compounds, TCPP maintains market dominance owing to the difficulty in finding cost-effective, high-performance alternatives for specific applications.

Key driving factors for the TCPP market involve rapid urbanization and infrastructure development in the Asia Pacific region, leading to exponential growth in the construction and insulation markets. The robust demand for automobiles globally also contributes significantly, as TCPP is used in seating, dashboard components, and interior textiles to meet mandatory safety standards. Furthermore, continuous technological advancements in manufacturing processes aim to minimize residual volatile organic compounds (VOCs) and enhance the purity of commercial-grade TCPP, improving its environmental profile and ensuring compliance with evolving global health and safety regulations. The versatility and established efficacy of TCPP ensure its sustained relevance across multiple high-growth end-use sectors.

The TCPP Flame Retardant Market is experiencing dynamic shifts, characterized by strong demand from the global construction sector, balanced against increasing regulatory pressures concerning halogenated chemicals and a growing preference for sustainable alternatives. Business trends indicate consolidation among major global chemical manufacturers seeking to optimize supply chains and increase production efficiency, particularly in response to volatile raw material costs, specifically propylene oxide and phosphorusoxychloride. Regional trends show robust market expansion in the Asia Pacific (APAC), fueled by massive infrastructure investments in China, India, and Southeast Asian nations where thermal insulation standards are rapidly being implemented or strengthened. Conversely, mature markets in North America and Europe are focusing more on regulatory compliance and the development of low-emission, high-purity grades of TCPP.

Segmentation trends highlight the dominance of the polyurethane foams segment, which accounts for the vast majority of TCPP consumption, driven primarily by the need for rigid foams in energy-efficient construction. Within the application types, the construction and building segment remains the cornerstone of market demand, followed by automotive interiors and electrical casings. A critical trend impacting future segmentation involves the increasing investment in flexible foam applications, specifically for bedding and upholstered furniture, where flame retardancy standards are becoming stricter in response to fire safety legislation. The competitive landscape is intensely focused on product differentiation through purity levels and customized formulations designed to meet highly specific fire testing requirements across different polymer systems.

Strategic initiatives across the industry include vertical integration to secure precursor chemical supply and aggressive capacity expansions, particularly in regions with lower operating costs. While TCPP faces long-term challenges from non-halogenated alternatives, its established performance profile and cost-effectiveness ensure short-to-medium-term market stability. Companies are strategically balancing the need to maintain existing TCPP market share while simultaneously investing in next-generation phosphorus and silicon-based flame retardants to prepare for potential future regulatory shifts. The overall market trajectory remains positive, underpinned by non-negotiable global fire safety standards and sustained growth in infrastructure and manufacturing activities worldwide.

User queries regarding AI's influence on the TCPP market frequently revolve around how artificial intelligence can optimize the synthesis and formulation of flame retardants, mitigate supply chain risks associated with precursor chemicals, and accelerate the discovery of safer, more sustainable alternatives. Common concerns include the cost implication of adopting AI-driven manufacturing processes and the predictability of future regulatory environments. Users are primarily seeking reassurance that AI can enhance the efficiency of existing TCPP production while simultaneously aiding R&D efforts to future-proof the industry against bans on halogenated compounds. The consensus theme is that AI will transform TCPP production from a batch-based, empirical process to a data-driven, continuous operation, thereby reducing waste and improving product consistency, which is crucial for achieving high-specification certifications required in end-use applications like aerospace or high-performance insulation panels.

AI’s influence is segmented into operational efficiency and predictive intelligence. Operationally, machine learning algorithms are being applied to optimize reactor conditions (temperature, pressure, catalyst concentration) during the synthesis of TCPP, leading to higher yields and reduced energy consumption. Predictive intelligence, on the other hand, utilizes complex data modeling to forecast fluctuations in the pricing and availability of key raw materials such as phosphorus oxychloride and epichlorohydrin, allowing manufacturers to implement dynamic inventory strategies and hedge against market volatility. Furthermore, AI-powered predictive maintenance minimizes unscheduled downtime in capital-intensive chemical plants, thereby guaranteeing stable production schedules necessary to meet the high-volume demand from the rapidly expanding construction sector, particularly during peak building seasons in Asia Pacific and North America.

In the area of product innovation, AI is playing an increasingly vital role in molecular design. Generative models are being used to simulate the flame retardancy mechanism of novel organophosphates, allowing researchers to screen thousands of potential TCPP derivatives or synergistic blends without extensive physical laboratory testing. This high-throughput computational screening drastically reduces the time-to-market for specialized or regulatory-compliant formulations. This capability is especially important given the increasing regulatory scrutiny worldwide, compelling producers to rapidly develop TCPP grades with lower migration potential or enhanced thermal stability, thus ensuring that the industry can maintain its competitive edge while adhering to evolving environmental and health mandates.

The market for TCPP Flame Retardants is shaped by a confluence of strong market drivers, significant regulatory restraints, and compelling technological opportunities, all interacting as impact forces. Key drivers include increasingly stringent global fire safety standards, especially within the construction sector, where materials like rigid polyurethane insulation foam must meet demanding fire codes to minimize property damage and loss of life. The massive global urbanization trend, particularly in emerging economies, mandates increased use of standardized building materials, further amplifying the demand for effective and economical flame retardants like TCPP. Simultaneously, the restraints are dominated by regulatory actions, particularly in Europe and parts of North America, focused on reducing the use of halogenated flame retardants due to environmental and potential human health concerns, leading to sustained pressure on manufacturers to seek alternatives or provide low-VOC formulations. The market dynamic is characterized by the constant tension between performance requirements and environmental compliance.

Opportunities for market players primarily lie in developing high-purity TCPP grades with lower volatile organic content (VOC) profiles to appease regulatory bodies and market demand for safer products. Furthermore, strategic alliances and focused R&D on synergistic blends combining TCPP with non-halogenated compounds (like melamine or red phosphorus derivatives) present a viable pathway to maintaining performance while improving environmental acceptability. The rising global focus on energy efficiency in buildings provides a robust long-term opportunity, as insulation remains the largest application area, consistently driving TCPP consumption. Impact forces include economic cycles affecting the construction industry, geopolitical instability impacting phosphorus supply chains, and continuous innovation in polymer science which can either introduce high-performing non-TCPP alternatives or further integrate TCPP into complex, multi-layered material systems.

Ultimately, the impact forces suggest a market segment undergoing transformation. While the high efficacy and cost advantages of TCPP provide inertial resistance to immediate replacement, sustained regulatory pressure ensures that innovation towards less hazardous alternatives remains a critical business imperative. Companies that successfully navigate this environment by demonstrating rigorous risk management, investing in product stewardship, and achieving compliance with the most stringent global standards are positioned for market leadership. The immediate impact is a focus on formulation adjustments and advanced testing protocols, whereas the long-term impact involves diversification into sustainable flame retardant chemistries while leveraging TCPP’s established application base in regions where regulatory scrutiny is less intense or where cost-performance remains the paramount decision factor.

The TCPP Flame Retardant market is comprehensively segmented based on its Purity Grade, Application Method, and primary End-Use Industry, reflecting the diverse requirements of the end-user landscape. Purity grade segmentation differentiates between technical grade TCPP, often used in less sensitive applications like construction materials, and high-purity grades, which are required for stringent applications such as electrical casings, automotive components, and certain flexible foams where low fogging and low residual VOCs are paramount. Application Method segmentation primarily includes reactive flame retardants, which chemically bond with the polymer, and additive flame retardants like TCPP, which are physically mixed into the material, with TCPP overwhelmingly falling into the additive category, demonstrating its ease of incorporation into polyurethane systems.

The end-use industry segmentation forms the core of market revenue analysis, dominated by the construction and building segment due to the vast volumes of rigid polyurethane (PU) insulation foam consumed globally. This segment's growth is inherently tied to global construction activity and evolving energy efficiency mandates. The second critical segment is the automotive sector, where TCPP is used in seating, headliners, and under-the-hood components to meet strict vehicular fire safety standards (FMVSS 302). Furthermore, the electrical and electronics sector utilizes TCPP in casings and circuit board coatings to prevent short-circuit fires. Geographic segmentation also plays a crucial role, highlighting the differential regulatory environments and consumption patterns between regions like APAC (high volume, rapidly growing) and Europe (stable volume, high regulatory constraint).

The value chain for the TCPP Flame Retardant Market is highly integrated, starting from the extraction and processing of core raw materials upstream and culminating in the delivery of fire-safe final products downstream. Upstream analysis reveals reliance on key chemical precursors: phosphorus oxychloride, propylene oxide, and epichlorohydrin. The stability and pricing of these commodities are critical factors determining the profit margins for TCPP manufacturers. Manufacturers must manage complex chemical synthesis processes, often requiring stringent safety and environmental controls. Given the chemical nature of TCPP, vertical integration by large chemical conglomerates is common, allowing better control over raw material sourcing and quality assurance, which directly impacts the purity and effectiveness of the final flame retardant product supplied to the market.

Midstream activities involve the actual chemical synthesis, purification, and granulation or liquid formulation of TCPP. This stage requires significant technological expertise to ensure compliance with product specifications, such as thermal stability, viscosity, and low residual volatility. Distribution channels for TCPP are bifurcated into direct sales and indirect sales. Direct distribution is favored for large-volume customers, such as major multinational polyurethane system houses or large construction material manufacturers, ensuring technical support and tailored logistics. Indirect distribution relies on specialized chemical distributors and regional agents who manage smaller orders and provide localized stockholding and delivery services to smaller, regional foam manufacturers or compounders, thereby widening market access.

Downstream analysis focuses on the integration of TCPP into end-use products. The largest customers are the rigid and flexible polyurethane foam producers who incorporate the additive during the foaming process. These foam products are then sold to the construction sector (insulation panels), automotive manufacturers (seating components), and furniture producers. The final consumer purchasing decisions, though indirect, are heavily influenced by regulatory mandates and safety certifications achieved by the end-products. The efficiency of the entire chain is dependent on minimizing logistical costs for a relatively high-volume chemical and ensuring the rapid adoption of newly compliant or purified formulations across all manufacturing touchpoints.

The primary potential customers and end-users of TCPP flame retardants are manufacturers of polymeric materials who are legally mandated or voluntarily choose to comply with fire safety standards. The most significant customer base comprises the global polyurethane system houses and foam producers, both rigid and flexible, as TCPP is exceptionally effective and cost-efficient in these matrices. These include large-scale manufacturers of thermal insulation boards utilized in commercial and residential buildings, cold storage facilities, and pipe insulation. Furthermore, the construction chemicals industry, which produces specialized coatings, sealants, and adhesive systems requiring flame resistance, represents a substantial customer segment constantly seeking proven, reliable fire-retarding additives for enhancing product performance.

A secondary, yet crucial, group of buyers includes companies in the transportation sector, specifically automotive OEMs and Tier 1 suppliers. These entities purchase TCPP either directly or as an additive within compounded plastics and textiles used for car interiors, engine compartments, and vehicle sound-dampening materials to adhere to stringent transportation safety regulations. The electronics and electrical appliance manufacturing sector also forms a key customer base, utilizing TCPP in injection-molded plastic casings and potting compounds where heat generation is a constant concern. These customers prioritize high thermal stability and electrical performance, alongside flame retardancy, demanding high-purity, low-fogging grades of TCPP to prevent component corrosion or interference.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 580.5 Million |

| Market Forecast in 2033 | USD 800.2 Million |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Lanxess AG, ICL Group, Albemarle Corporation, Jiangsu Yoke Technology, PCC Group, Zhejiang Wansheng Chemical, Shandong Xurui New Materials, Daihachi Chemical Industry, Merck KGaA, Great Lakes Solutions (Chemtura), Supresta (SK Capital), Rianlon Corporation, Chitec Technology, Tianjin Bohai Chemical Industry, Italmatch Chemicals. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape surrounding the TCPP Flame Retardant market primarily focuses on refining synthesis processes to enhance purity and minimize environmental impact, rather than developing fundamentally new applications for the molecule itself. Core manufacturing technology involves the phosphorylation of chlorinated alcohols, typically requiring batch or semi-continuous reaction systems. Recent technological advancements aim to optimize these reaction conditions, utilizing advanced catalysis techniques and sophisticated filtration systems to yield High Purity Grade TCPP with extremely low levels of volatile organic compounds (VOCs). This low-VOC focus is a direct response to health and safety regulations, particularly in the European Union and North America, necessitating investment in specialized purification trains and handling systems to ensure product compliance for sensitive applications like bedding and aerospace materials.

Furthermore, technology is rapidly evolving in the application side, specifically concerning the formulation of polymer systems containing TCPP. Significant R&D is directed towards creating synergistic flame retardant packages. This involves combining TCPP, an effective vapor-phase and condensed-phase inhibitor, with intumescent agents or mineral fillers. These blended formulations aim to meet new, more rigorous fire tests (e.g., California Technical Bulletin 117-2013) while potentially reducing the overall TCPP loading, thereby mitigating health concerns associated with high concentrations. Advances in continuous mixing and dispensing technologies for polyurethane foams ensure homogeneous dispersion of TCPP throughout the matrix, maximizing its efficiency at lower usage levels and improving the structural integrity of the final insulating product.

In response to long-term sustainability pressures, technology development also includes sophisticated analytical tools and modeling software that predict the environmental fate and toxicity of various TCPP formulations. Chromatography and mass spectrometry techniques are being employed to monitor residual reactants and byproducts rigorously, ensuring the final product meets the highest possible standards for worker safety and consumer exposure. The future technological trajectory is characterized by digital manufacturing integration (Industry 4.0 principles) to achieve real-time process control, further optimizing energy consumption during synthesis and ensuring unprecedented batch-to-batch consistency, which is vital for multinational customers operating under global quality standards.

The primary driver is the global implementation of stricter fire safety regulations across the construction industry, particularly the mandatory requirement for effective flame retardancy in rigid polyurethane foam used for building insulation.

TCPP (Tris(2-chloro-1-methylethyl) phosphate) is classified as a halogenated organophosphate flame retardant, meaning it contains chlorine atoms within its chemical structure, which contributes to its high efficacy.

The Construction and Building industry holds the largest market share, driven overwhelmingly by the high-volume consumption of TCPP as an additive in rigid polyurethane (PU) foam insulation panels and spray foam systems.

The main challenges stem from increasing regulatory scrutiny in developed markets, notably in Europe and North America, concerning the long-term environmental and health impact of certain halogenated compounds, pressuring manufacturers to develop low-VOC or alternative formulations.

The market is leveraging AI to optimize TCPP synthesis processes for higher purity and lower energy consumption, predict volatility in raw material supply chains, and accelerate the computational screening and design of next-generation flame retardant formulations.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.