ID : MRU_ 436763 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

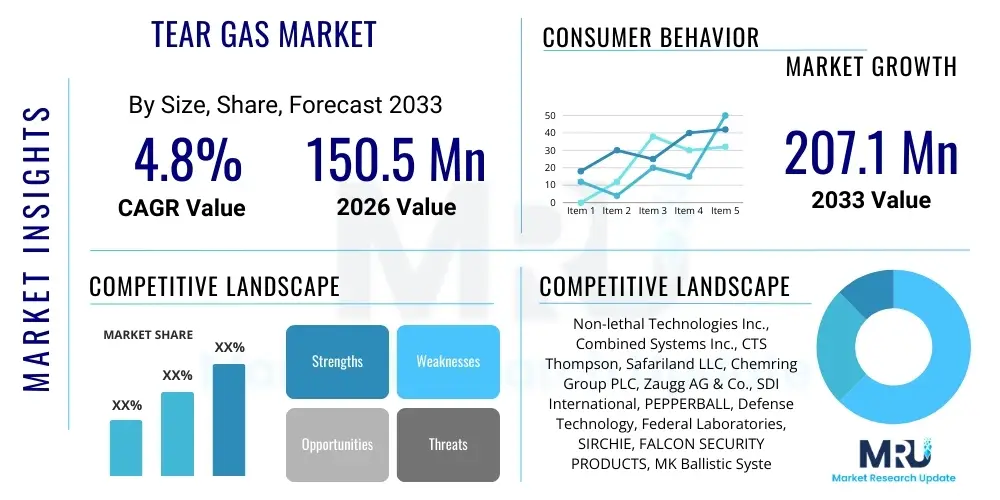

The Tear Gas Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 150.5 Million in 2026 and is projected to reach USD 207.1 Million by the end of the forecast period in 2033.

The Tear Gas Market encompasses the manufacturing, distribution, and deployment of chemical compounds specifically designed to incapacitate individuals temporarily by irritating the eyes, respiratory system, and skin. These products, classified primarily as riot control agents (RCAs), are critical components within the non-lethal weapons arsenal utilized globally by government agencies. The primary product descriptions include agents based on O-Chlorobenzylidene Malononitrile (CS gas), Chloroacetophenone (CN gas), and Oleoresin Capsicum (OC gas, commonly known as pepper spray). CS gas represents the conventional standard due to its rapid efficacy and relatively short-term effects, though ongoing research seeks less harmful alternatives.

Major applications of tear gas center around crowd dispersal and riot control operations managed by domestic law enforcement agencies and, to a lesser extent, military and internal security forces involved in peacekeeping. Additionally, smaller, portable versions are increasingly applied in the private security sector and for personal defense purposes. The primary benefit derived from their use is the ability to deter or subdue non-compliant subjects or large groups without resorting to potentially lethal force, thereby maintaining public order and minimizing fatalities during volatile situations. This non-lethal capacity drives demand, especially as global civil unrest incidents increase and police forces seek methods compliant with escalating ethical standards.

Driving factors for market expansion include the continuous global demand for effective non-lethal solutions in urban security environments, necessitated by geopolitical tensions and internal political instability. Furthermore, ongoing governmental initiatives across developing and developed nations to modernize police equipment and incorporate robust training programs regarding de-escalation tactics often include updated procurement cycles for riot control agents. Regulatory frameworks, while restrictive regarding chemical warfare, generally permit and regulate the use of these agents for domestic law enforcement, ensuring a continuous, albeit highly scrutinized, market base.

The Tear Gas Market is characterized by stable, albeit regulated, growth, primarily driven by heightened needs for internal security and non-lethal crowd control capabilities across emerging economies. Current business trends indicate a significant focus on research and development aimed at producing formulations with reduced long-term health risks, responding directly to ethical pressures and humanitarian concerns regarding conventional CS and CN agents. Market profitability is heavily influenced by government procurement cycles and defense spending, making long-term contracts with national security agencies the cornerstone of stable revenue generation. Furthermore, strategic partnerships between chemical defense contractors and localized distributors are critical for navigating complex import/export regulations inherent to riot control technology. The sector is seeing consolidation, with key players investing in vertical integration to control the supply chain of precursor chemicals, ensuring product consistency and regulatory compliance, particularly concerning the Chemical Weapons Convention (CWC), even though domestic use of RCAs is exempted.

Regionally, the market exhibits uneven demand dynamics. Asia Pacific (APAC) and the Middle East & Africa (MEA) are emerging as high-growth markets, fueled by rapid urbanization, substantial internal security challenges, and increasing government investments in paramilitary forces. North America and Europe, while mature markets, maintain high demand due to extensive use by specialized tactical units and prison systems, alongside stringent regulatory oversight ensuring high product quality and standardization. Political instability in regions like Latin America also contributes significantly to sporadic, high-volume procurement contracts. The key regional trend involves local manufacturing development in major consuming nations to bypass complex international arms trade restrictions and ensure self-sufficiency in riot control supplies, leading to competitive pricing in these localized markets.

Segmentation trends highlight the dominance of CS gas (O-Chlorobenzylidene Malononitrile) as the preferred product type globally due to its established effectiveness and supply chain, although OC gas (pepper spray) is gaining traction, especially in personal defense and less severe law enforcement scenarios, owing to its organic base and slightly better public perception. In terms of application, law enforcement agencies remain the undisputed largest segment, dictating specifications regarding deployment mechanisms (grenades, canisters, launchers). There is a nascent but expanding sub-segment dedicated to private security and personal use, driven by rising crime rates and the desire for non-lethal self-protection tools. Innovations focus on aerosol and liquid deployment systems offering better targeting accuracy and reduced contamination risks compared to traditional solid dispersion methods.

Common user questions regarding AI's impact on the Tear Gas Market often revolve around how technology can minimize collateral damage, enhance targeting precision, and potentially replace chemical agents entirely with smarter, non-harmful tools. Users are keen to understand if AI-driven analysis of crowd behavior can lead to de-escalation protocols that reduce the need for riot control agents, or if AI systems will optimize chemical delivery methods. Key themes include the ethical implications of using autonomous systems to deploy force, even non-lethal, and the role of machine learning in developing novel, less toxic chemical formulations by simulating molecular interactions. There is also significant concern about whether AI could exacerbate civil liberties issues by enabling highly efficient, targeted dispersal operations, raising questions about surveillance integration and predictive policing.

The most immediate influence of AI and associated technologies, such as advanced data analytics and predictive modeling, is seen in the operational deployment strategies used by law enforcement. AI algorithms can analyze real-time video feeds and social media activity to predict the movement, size, and potential trajectory of crowds, allowing agencies to preemptively deploy forces and resources, minimizing the need for large-scale, indiscriminate use of tear gas. This shift from reactive crowd control to proactive tactical management reduces overall consumption of riot control agents in certain scenarios, pushing manufacturers to focus on highly specific, high-precision delivery systems rather than bulk agents.

Furthermore, AI is instrumental in the quality control and supply chain logistics of tear gas manufacturing. Machine learning models optimize the chemical synthesis process, ensuring purity and consistency of the active ingredients, which is paramount given the stringent international regulations on chemical weapons precursors. In the longer term, advanced computational chemistry powered by AI could accelerate the discovery and testing of truly non-toxic incapacitating agents that achieve the desired temporary effect without the severe respiratory and ocular risks associated with current compounds, potentially rendering traditional tear gas obsolete. However, integrating these complex systems requires substantial investment in infrastructure and specialized training for security personnel.

The dynamics of the Tear Gas Market are governed by a complex interplay of Drivers, Restraints, and Opportunities (DRO), significantly shaped by geopolitical stability and ethical considerations, constituting the Impact Forces. Key drivers propelling the market include escalating global political unrest, requiring state security apparatuses to maintain high readiness for crowd dispersal. Restraints are predominantly centered on regulatory hurdles, particularly the dual-use nature of the chemicals which necessitates strict adherence to international treaties and constant ethical pressure from human rights organizations regarding the harmful effects of these agents. Opportunities lie in technological advancements that enable the creation of safer, more effective deployment mechanisms and less harmful chemical formulations, alongside market expansion into rapidly militarizing emerging economies. This dynamic balance ensures that while demand remains persistent, the methods and formulations must continuously evolve under intense public and governmental scrutiny.

A major driver is the accelerating trend of urban conflict and large-scale public demonstrations globally, compelling governments to invest heavily in non-lethal crowd control technology to manage dissent while upholding an appearance of minimal force. This modernization imperative includes purchasing advanced delivery systems, such as specialized projectile launchers and drone-based dispersal systems, increasing the value proposition of the market. Furthermore, the standardization and professionalization of law enforcement and prison systems globally mandate the continuous stocking of riot control inventory for routine training and emergency use. The need for less-than-lethal options remains crucial as an intermediate step between verbal warnings and the deployment of lethal force, cementing its role in the security toolkit.

Conversely, the market faces substantial restraints, primarily regulatory limitations imposed by international agreements like the Chemical Weapons Convention (CWC), which, although allowing domestic riot control use, subjects manufacturers to rigorous oversight regarding precursor chemical acquisition and export controls. Public backlash and negative media coverage regarding the misuse or excessive application of tear gas often lead to moratoriums or restrictive local legislation, temporarily crippling sales in specific regions. The impact forces are further defined by the ethical debate surrounding the long-term health consequences and indiscriminate nature of wide-area deployment. Opportunities for market players, therefore, hinge on developing novel agents—like advanced OC variants or psycho-physical irritants—that offer superior control with reduced toxicity profiles, catering to a world increasingly demanding ethical security solutions.

The Tear Gas Market is primarily segmented based on the type of active chemical agent used, the final application or end-user, and the physical state of the product formulation. Analyzing these segments provides critical insights into market penetration and preferred procurement strategies across different regions and user groups. The dominance of CS gas reflects historical deployment reliability and established manufacturing processes, while the growing market share of OC gas highlights a shift towards natural, perception-friendly alternatives, especially in consumer-grade and personal defense applications. Application segmentation underscores that government agencies—law enforcement and military—are the pivotal consumers, setting the high standards for reliability and compliance. Understanding the interplay between agent type and deployment state (aerosol versus solid grenade) is crucial for manufacturers tailoring products to specific operational requirements, such as indoor clearing versus open-area crowd dispersal, defining the competitive landscape.

The value chain for the Tear Gas Market begins with the highly regulated upstream supply of specialized precursor chemicals, such as malononitrile and ortho-chlorobenzaldehyde for CS gas, or capsaicinoids extraction for OC gas. This upstream segment is characterized by rigorous quality control and stringent monitoring due to international non-proliferation laws and chemical control acts. Manufacturers must secure reliable, certified chemical suppliers who comply with necessary permits and tracking requirements, introducing a high barrier to entry and fostering reliance on a few specialized chemical producers. The manufacturing phase involves complex chemical synthesis and formulation, followed by packaging into specialized delivery systems (canisters, grenades, shells), necessitating advanced engineering capabilities for safety and effectiveness.

The midstream involves the integration of these chemical agents into usable products, encompassing tasks like loading, sealing, and testing the final delivery systems, which are often subject to military or police specification standards. Distribution channels constitute the critical downstream element, primarily relying on highly controlled, government-approved direct sales and certified defense distributors. Direct channels are prevalent for large military and law enforcement contracts, ensuring confidentiality and security, while indirect channels leverage specialized defense procurement agents or security equipment retailers for smaller government clients or the private security/personal defense segment. Due to the sensitive nature of the product, standard commercial logistics networks are rarely used, favoring high-security transport protocols.

The downstream analysis reveals that procurement is highly centralized, with government tenders and large-scale, multi-year contracts being the primary sales drivers. Marketing and sales efforts are concentrated on demonstrating compliance, safety certifications, and effectiveness under varied operational conditions, often involving specialized demonstrations for official procurement committees. The after-sales service is minimal for the chemical agents themselves, given their single-use nature, but is crucial for the reusable delivery platforms (e.g., launchers), requiring maintenance, training, and spares. The integrity of the distribution channel, including preventing diversion to unauthorized entities, is a paramount concern throughout the entire value chain.

The potential customers for tear gas products are overwhelmingly institutional, falling primarily under the umbrella of governmental and quasi-governmental security entities. The largest end-users are domestic Law Enforcement Agencies (LEAs), including metropolitan police forces, highway patrols, and particularly, specialized tactical units (SWAT, riot police) who rely on these agents for high-risk arrests, maintaining order, and controlling large civil disturbances. Correctional facilities and prison systems also constitute a major end-user group, utilizing smaller canisters and restricted agents for controlling inmate unrest within contained environments where lethal force must be avoided at all costs. These institutional customers prioritize reliability, shelf-life, and compliance with national usage protocols when making procurement decisions.

Another significant customer segment is the Military and Defense sector, especially those units involved in internal security, border control, and international peacekeeping missions. While military use is heavily restricted by international law in combat zones, its application in rear areas, base security, and crowd control during non-war operations remains vital. Military procurement typically involves larger volume products and more robust, ruggedized delivery systems compared to those used by civil police. Emerging markets often see military forces taking on expanded internal security roles, boosting demand for military-grade riot control agents in these regions.

Finally, the growing segment of Private Security and Personal Use customers, though significantly smaller in volume, offers higher profit margins for manufacturers of OC-based sprays. Private security firms protecting critical infrastructure, large corporate campuses, and commercial venues utilize these agents. On the personal side, individual consumers purchase compact pepper sprays and defense devices for self-protection, driven by increasing public awareness of non-lethal defense options. This segment is highly responsive to consumer marketing, product design (e.g., keychain sprays), and localized availability through retail channels.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 150.5 Million |

| Market Forecast in 2033 | USD 207.1 Million |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Non-lethal Technologies Inc., Combined Systems Inc., CTS Thompson, Safariland LLC, Chemring Group PLC, Zaugg AG & Co., SDI International, PEPPERBALL, Defense Technology, Federal Laboratories, SIRCHIE, FALCON SECURITY PRODUCTS, MK Ballistic Systems, ALS Technologies, Sage Control International, RAE Systems, Lamperd Less Lethal, General Dynamics, Rheinmetall AG, Arsenal AD |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape in the Tear Gas Market primarily focuses on innovations in deployment mechanisms rather than radical changes in the chemical agents themselves, which are largely standardized. Traditional deployment relies heavily on pyrotechnic grenades and single-use canisters, which disseminate the agent through either burning or explosion, leading to wide and often indiscriminate dispersion. Modern technological advancements aim to overcome these limitations by developing precision-guided delivery systems. One key area of innovation is the development of kinetic energy impact projectiles containing chemical payloads, such as those fired from specialized launchers, allowing law enforcement to target specific individuals or small groups from a safe distance, thereby significantly reducing collateral exposure to bystanders and limiting the overall volume of chemical required for an operation. These systems often incorporate trajectory guidance features to improve accuracy.

Another crucial technological shift involves the transition from traditional solid-state dispersion to highly concentrated liquid or aerosol delivery methods, often integrated into sophisticated fogging devices or drone payloads. Liquid formulations offer greater control over droplet size and dispersal duration, leading to reduced atmospheric persistence compared to pyrotechnic smoke agents. The integration of advanced sensor technology, including thermal and optical guidance systems, into deployment launchers is becoming standard practice. These smart launchers can calculate wind speed, target distance, and atmospheric conditions in real-time to adjust firing parameters, ensuring effective delivery while adhering to safety thresholds. This technological sophistication addresses operational demands for precision and minimizes environmental impact.

Furthermore, technology is playing a vital role in addressing ethical concerns through advanced chemical detection and decontamination solutions. Manufacturers are integrating inert marker dyes into riot control agents to aid in identifying exposed individuals, assisting in accountability. On the chemical formulation front, R&D is leveraging chemical engineering to encapsulate active agents, allowing for timed or sustained release, and focusing on biologically degradable carrier systems. Although conventional tear gas remains dominant, future growth will be heavily contingent on the successful commercialization of these precision deployment platforms and the adoption of low-toxicity, smart-delivery liquid agents, pushing the market towards sophisticated, controlled non-lethal deterrence systems that generate minimal public resistance compared to historical methods.

The key driver is the increasing incidence of global civil unrest, political demonstrations, and social conflicts, which necessitates law enforcement and military agencies to maintain readily available, effective, non-lethal options for large-scale crowd control and dispersal operations.

CS Gas (O-Chlorobenzylidene Malononitrile) currently dominates the market due to its established efficacy, standardized formulations, and historical role as the primary agent utilized by global law enforcement and riot control forces in various deployment systems.

Although the Chemical Weapons Convention (CWC) allows the domestic use of riot control agents, it imposes strict monitoring on the production and trade of precursor chemicals, requiring manufacturers to adhere to complex export controls and transparency standards to prevent diversion.

The primary technological innovation is the shift towards precision-guided and targeted delivery systems, such as kinetic energy projectiles and smart launchers, aimed at reducing the indiscriminate spread of chemical agents and minimizing unintended collateral exposure.

The Asia Pacific (APAC) region demonstrates the highest growth potential, driven by significant government investments in internal security modernization, high population density, and frequent security challenges requiring large-scale, non-lethal crowd management solutions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.