ID : MRU_ 432323 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

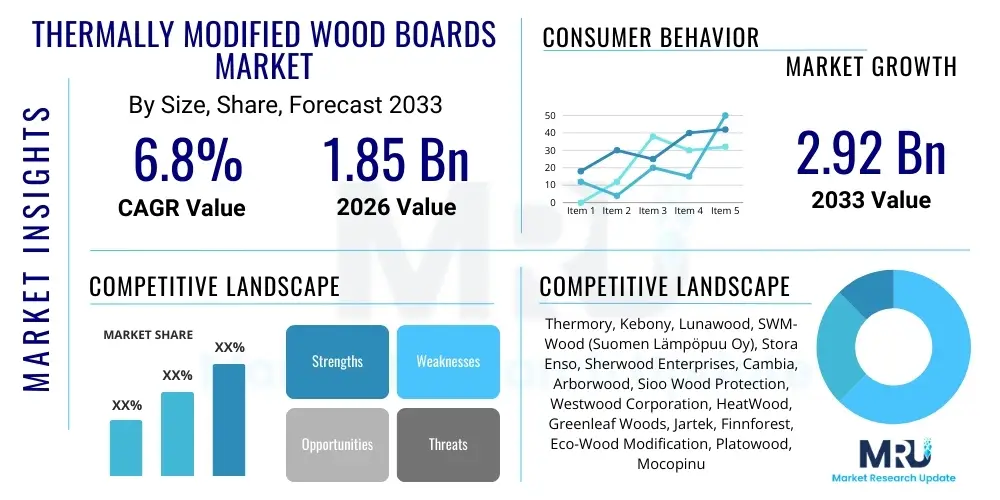

The Thermally Modified Wood Boards Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 1.85 Billion in 2026 and is projected to reach USD 2.92 Billion by the end of the forecast period in 2033. This growth trajectory is significantly influenced by increasing global emphasis on sustainable building materials, coupled with the rising demand for wood products that offer superior durability and dimensional stability without the reliance on harmful chemical preservatives. The expansion of high-end residential construction and commercial renovation projects, particularly in mature markets across North America and Europe, further accelerates market penetration. Furthermore, the aesthetic appeal and enhanced performance characteristics of thermally treated wood, such as improved resistance to decay and insects, position it favorably against traditional treated lumber or composite materials, driving steady revenue generation in specialized construction and exterior applications.

The Thermally Modified Wood Boards Market encompasses the production and distribution of wood materials that have undergone controlled, high-temperature treatment in low-oxygen environments. This process fundamentally alters the chemical and physical properties of the wood, resulting in enhanced attributes such as reduced moisture content, superior dimensional stability, and increased biological resistance (fungal and insect). These modified properties make the resulting wood suitable for demanding exterior applications, including decking, cladding, siding, and outdoor furniture, where natural wood conventionally struggles with longevity and stability. The foundational technology behind thermal modification leverages heat to break down hemicelluloses, thereby reducing the wood’s capacity to absorb moisture and making it less palatable to biological degrading agents.

Major applications of thermally modified wood boards span the construction and architectural sectors. In residential construction, they are widely used for premium decking solutions and high-performance exterior wall siding due to their unique color profile—ranging from rich brown to near black—and reduced maintenance requirements. Commercially, they are specified for public boardwalks, façade elements in commercial buildings, and landscaping features where long-term material integrity is paramount. Key benefits driving adoption include the complete absence of toxic chemicals, positioning the product as an environmentally superior alternative to chemically pressure-treated woods, and its consistent performance across varying climates, minimizing warping, swelling, and cracking over its lifespan.

Driving factors underpinning market expansion are multifaceted. A primary driver is the stringent regulatory environment in developed nations promoting sustainable forestry and non-toxic building materials, pushing manufacturers toward cleaner preservation methods. Additionally, consumer preferences are shifting toward natural, aesthetically pleasing materials that require minimal maintenance, favoring the consistent appearance and inherent durability of thermally modified wood. Technological advancements in thermal modification machinery, which improve energy efficiency and batch throughput, are also reducing production costs and making the product more price-competitive against high-performance composites and tropical hardwoods, thereby broadening its accessibility across mid-tier construction projects globally.

The Thermally Modified Wood Boards Market is experiencing robust expansion, primarily fueled by the accelerating global trend towards sustainable and durable construction materials. Business trends indicate a strong move toward vertical integration among key players, focusing on securing raw material supply chains—predominantly sustainable softwoods like spruce and pine—and optimizing modification processes to maximize yield and minimize energy expenditure. Innovation is concentrated on developing hybrid modification techniques, such as combining thermal treatment with oil or wax impregnation, to further enhance water repellency and UV resistance, thus creating specialized, high-margin product lines tailored for harsh climates. Furthermore, strategic partnerships between thermal wood producers and architectural firms are crucial for increasing specification rates in large-scale commercial and infrastructure projects, solidifying the product's premium positioning within the building materials market.

Regional trends highlight Europe as the historical nucleus and current market leader, particularly driven by Nordic countries and Germany, which possess both advanced technology and a strong commitment to eco-friendly building codes like those pertaining to BREEAM and LEED certifications. North America is poised for the highest growth rate, stimulated by a surge in outdoor living space renovation (decking and patio additions) post-pandemic and the increasing acceptance of thermal modification as a viable, long-lasting alternative to endangered tropical hardwoods. Asia Pacific, while nascent, shows significant promise, particularly in Australia, New Zealand, and Japan, where high seismic activity and varying humidity levels necessitate materials with exceptional dimensional stability. These regions are prioritizing investment in local production facilities to reduce reliance on expensive European imports and establish domestic supply chains for thermally treated materials.

Segment trends reveal that the Softwood category (primarily Pine and Spruce) dominates the volume share due to its wide availability, lower cost base, and high suitability for modification, catering predominantly to high-volume decking and structural applications. However, the Hardwood segment, utilizing ash, maple, and oak, commands a higher average selling price and is favored for premium interior flooring, decorative paneling, and high-end furniture due to superior aesthetic grain patterns and density. Application-wise, Decking remains the largest revenue segment globally, followed closely by Siding/Cladding, which is benefiting from architectural innovation favoring maintenance-free exterior façades. This segmentation showcases a duality in the market: volume-driven standardization utilizing softwoods for exterior structures and value-driven customization utilizing hardwoods for aesthetic and specialty components.

Analysis of user inquiries regarding the intersection of Artificial Intelligence (AI) and the Thermally Modified Wood Boards Market reveals key themes centered on process optimization, quality control, and predictive maintenance. Users frequently ask how AI can standardize the highly variable thermal modification process, which relies heavily on raw material properties (species, moisture content, density). Concerns revolve around leveraging machine learning to predict the optimal temperature and duration cycles required for different wood batches to achieve desired performance metrics (e.g., equilibrium moisture content, decay resistance class) consistently, thereby reducing expensive waste and improving energy efficiency. There is also significant interest in using computer vision systems integrated with AI to automate defect detection, both pre-treatment and post-treatment, ensuring quality conformity that is difficult to maintain manually across large production runs, addressing labor shortage issues and enhancing overall product reliability for high-specification projects.

The deployment of AI, specifically through advanced data analytics and prescriptive modeling, offers significant opportunities for manufacturers to move beyond traditional empirical methods. For example, machine learning algorithms can analyze vast datasets concerning kiln performance, ambient weather conditions, wood density variations, and resultant material performance in the field. This capability allows producers to dynamically adjust processing parameters in real time, moving from static, pre-set thermal cycles to adaptive, predictive manufacturing. This not only minimizes operational variances but also maximizes the yield of high-grade material from each batch, directly impacting profitability. Furthermore, AI-driven simulations can model long-term durability under specific climatic loads, enabling manufacturers to provide highly precise performance warranties, thereby enhancing trust among architects and end-users.

Beyond the manufacturing floor, AI is beginning to influence supply chain management and inventory planning. Predictive analytics can forecast demand for specific wood types (hardwood vs. softwood) and applications (decking vs. siding) based on macroeconomic indicators, regional construction permits, and seasonal trends. This leads to optimized raw material procurement, reducing holding costs and ensuring timely delivery of specialized products. In customer-facing roles, AI-powered tools are enhancing design and visualization platforms, allowing architects and consumers to simulate how thermally modified wood façades will age and weather over time, aiding in the specification and selection process, which is crucial given the product’s distinctive, aging characteristics.

The market dynamics of Thermally Modified Wood Boards are shaped by a complex interplay of Drivers, Restraints, and Opportunities (DRO), which collectively form the Impact Forces dictating market trajectory. The primary Driver is the burgeoning global demand for green building certifications and sustainable materials, coupled with regulatory shifts restricting the use of chemically treated lumber. This is synergized by consumer willingness to invest in higher-cost, zero-maintenance exterior solutions. Restraints chiefly involve the relatively high initial capital expenditure required for sophisticated thermal modification equipment and the inherent susceptibility of the modified wood to UV degradation, necessitating additional finishes to maintain color consistency. Opportunities lie in penetrating emerging markets (APAC, MEA) where high-performance wood imports are favored, and in developing next-generation modification techniques that further enhance hardness and fire resistance, opening avenues in structural applications currently dominated by concrete or steel.

Drivers are exerting significant upward pressure. The superior environmental profile—being non-toxic and often sourced from certified sustainable forests—makes thermally modified wood a preferred choice in environmentally conscious projects. Furthermore, the inherent stability and durability translate into a lower total cost of ownership over the product lifespan compared to non-modified alternatives that require frequent replacement or intensive chemical upkeep. This shift from initial price focus to lifetime value assessment is a powerful driver, particularly within commercial and high-end residential segments. Regulatory tailwinds in the EU, restricting biocides commonly used in traditional wood preservation, further reinforce the mandatory adoption of cleaner processes like thermal modification.

The core Restraint remains the perception of high upfront cost and the complexity of the treatment process itself, which limits adoption in price-sensitive markets. The high operating temperatures (180°C to 230°C) cause a darkening of the wood, which, while aesthetically desirable to many, is not suitable for all applications, and the loss of natural color requires additional pigment application if a lighter shade is required. Impact Forces demonstrate that while technological improvement continues to drive down unit costs, the availability of specialized, high-grade raw timber feedstock remains a bottleneck. However, the Opportunity to utilize fast-growing, low-value wood species (e.g., certain softwoods) and upgrade them to premium materials via thermal modification provides a compelling economic incentive for market growth, creating new supply chains and value streams.

The Thermally Modified Wood Boards Market is comprehensively segmented based on wood type, application, treatment method, and end-user, providing a granular view of market dynamics and revenue generation potential. Segmentation by wood type is crucial as it dictates the end-use aesthetic, material performance, and price point; softwoods, being abundant and cost-effective, dominate volume, while hardwoods capture the value segment. Application segmentation clearly delineates the primary uses, with exterior applications like decking and siding consistently driving the largest market share due to the superior weather resistance imparted by thermal modification. The increasing sophistication in treatment methods, from standard thermo-vacuum to advanced steam injection and oil modification, allows manufacturers to tailor performance characteristics precisely to demanding structural and decorative requirements across different geographies.

Further analysis of segmentation reveals strategic priorities for market participants. Companies specializing in large-scale decking often focus on optimizing the treatment process for softwoods (e.g., Southern Yellow Pine, Spruce) to achieve Grade 1 or Grade 2 decay resistance, targeting the mass residential and commercial infrastructure markets with standardized products. Conversely, firms focusing on niche architectural paneling or custom furniture rely heavily on premium hardwoods (e.g., Ash, Maple) to leverage the rich, deep coloration achieved through modification, commanding premium prices through specialized distribution channels focusing on architects and interior designers. This dual market approach necessitates different operational strategies, from raw material sourcing to marketing and sales, indicating a fragmented yet highly specialized competitive landscape.

The End-User segmentation reinforces these dynamics, with the Residential sector being the largest consumer, driven by repair, renovation, and construction of high-quality homes and outdoor spaces. The Commercial sector, encompassing hotels, offices, and public infrastructure, prioritizes materials with proven longevity and low maintenance, favoring thermally modified wood specifications for their reduced lifecycle costs and high compliance with green building standards. Understanding these segments is vital for targeted marketing efforts; for instance, emphasizing sustainability benefits for the European commercial market, while highlighting durability and aesthetic appeal for the North American residential decking consumer.

The value chain for the Thermally Modified Wood Boards Market begins with upstream activities centered on sustainable forestry and raw timber procurement. Upstream analysis involves sourcing high-quality, sustainably certified (FSC/PEFC) softwood and hardwood logs, primarily from North American and European forests. Due to the energy-intensive nature of the modification process, proximity to well-managed forest resources and efficient primary processing (sawmilling) is crucial for cost optimization. The intermediate stage involves the core manufacturing process: the thermal modification itself, where raw lumber is kiln-dried and then subjected to high temperatures (180°C–230°C) in specialized reactors to impart the enhanced properties. This stage adds the highest value, transforming commodity timber into a specialty, high-performance building material. Technological expertise and energy efficiency are the key competitive differentiators at this processing level.

Downstream analysis focuses on secondary processing, distribution, and end-market installation. Secondary processing includes planing, profiling (e.g., tongue and groove, deck board profiles), and application of protective finishes (e.g., UV inhibitors, oil treatment) tailored to specific end-user requirements. Distribution channels are highly critical for market access. Direct channels are often utilized for large commercial or architectural projects where manufacturers deal directly with contractors or specifiers, offering customized solutions and technical support. Indirect channels involve utilizing a network of specialized building material distributors, lumber yards, and retailers who handle bulk stock and cater to smaller contractors and the residential DIY market. These distributors often require specialized training to effectively communicate the unique benefits and installation requirements of thermally modified wood versus traditional alternatives.

The effectiveness of the value chain is highly dependent on logistics and quality assurance throughout the process. Since thermal modification significantly increases the wood’s stability, minimizing post-treatment movement, maintaining quality from the factory gate to the installation site is easier than with conventional lumber. However, the specialized nature of the product requires focused marketing and technical education across the distribution network. Potential customers (End-Users/Buyers) include high-end home builders, landscape architects, commercial developers, and specialized furniture manufacturers, all seeking materials that offer exceptional durability, low maintenance, and high environmental performance. Efficient upstream supply of certified timber and effective downstream market education are essential drivers of long-term market growth and profitability.

The primary consumers and end-users of thermally modified wood boards are concentrated in sectors prioritizing material longevity, environmental stewardship, and aesthetic quality. End-user segments include residential property owners engaged in high-end renovation and new construction projects, particularly those focused on extensive outdoor living spaces like custom decks, pergolas, and pool surrounds. These buyers are willing to pay a premium for chemical-free durability and reduced lifecycle costs associated with minimal maintenance. Professional buyers in the commercial sector include hospitality groups developing resorts and hotels, and property management firms specializing in high-traffic public spaces, requiring cladding and flooring that can withstand heavy use and harsh weather conditions without rapid degradation.

Furthermore, architects, landscape designers, and large construction contractors act as crucial intermediaries and specifiers. They are the key decision-makers who determine which materials are incorporated into project plans. Their preference for thermally modified wood is driven by its compliance with green building standards (e.g., LEED, BREEAM), its consistent quality, and the ability to achieve specific, high-end design aesthetics using domestic wood species instead of relying on endangered tropical hardwoods. Specialized industrial buyers, such as manufacturers of high-quality outdoor furniture and pre-fabricated modular homes, also represent significant volume purchasers, utilizing the material's stability and resistance to provide value-added features in their final products.

The buying process for these customers is often influenced by long-term warranty provisions and performance data rather than just initial price. High-volume purchases are typically made directly from manufacturers or specialized national distributors, whereas smaller contractors and DIY homeowners purchase through regional lumberyards and retail chains. Educating these diverse distribution channels on the specific installation techniques required for thermally modified wood (e.g., specialized fasteners, ventilation needs) is critical to ensure customer satisfaction and repeat business, solidifying the product's position as a premium building solution.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 2.92 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Thermory, Kebony, Lunawood, SWM-Wood (Suomen Lämpöpuu Oy), Stora Enso, Sherwood Enterprises, Cambia, Arborwood, Sioo Wood Protection, Westwood Corporation, HeatWood, Greenleaf Woods, Jartek, Finnforest, Eco-Wood Modification, Platowood, Mocopinus, NFP, WTT Wood Treatment Technologies, Sayerlack (part of Sherwin-Williams) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technology landscape of the Thermally Modified Wood Boards Market revolves around the precise control of heat, moisture, and atmospheric conditions to alter wood structure without combustion. The dominant process remains the Thermo-vacuum or Thermo-hydro process, pioneered primarily in Europe. This involves subjecting lumber to temperatures typically ranging from 180°C to 230°C within sealed kilns. The atmosphere is controlled either by steam (Thermo-hydro) or nitrogen/vacuum (Thermo-vacuum) to prevent oxidation and charring of the wood, which would occur rapidly in a standard air kiln. Key technological innovations in this space focus on optimizing the energy consumption of these large kilns, utilizing heat recovery systems, and integrating sensors for precise real-time monitoring of core wood temperature and moisture release, ensuring batch consistency and maximizing material yield across different species.

A significant trend in technological development is the move towards hybrid modification techniques designed to address the specific performance trade-offs inherent in standard thermal treatment, such as increased brittleness and UV susceptibility. Technologies like Thermo-Hydro-Oil (THO) modification integrate an oil bath or pressurized oil injection step immediately following or during the thermal cycle. This infusion of natural oils (e.g., linseed or sunflower oil) helps restore some elasticity to the wood cells, significantly improving water repellency and providing enhanced protection against environmental factors. These hybrid processes, while more complex and marginally more expensive, deliver superior performance characteristics that open up applications in marine environments or areas with extreme humidity fluctuations, thus capturing higher-value market niches and differentiating premium product lines.

Furthermore, the digital transformation of the production process, incorporating Industrial IoT (IIoT) and advanced control software, is central to the modern technology landscape. Sophisticated SCADA systems and proprietary software modules are being developed to manage complex variables like heating gradients, pressure ramps, and hold times across multiple, simultaneously operating kilns. This level of automation ensures repeatable quality outcomes, reduces reliance on operator expertise, and allows for rapid adjustments based on material input characteristics. Future technology focuses on microwave or radio-frequency assisted heating for faster and more uniform heat penetration, potentially reducing overall cycle times and further enhancing energy efficiency in the production of high-volume thermally modified wood boards.

Regional dynamics play a critical role in defining the structure and growth potential of the Thermally Modified Wood Boards Market, driven by local building codes, access to raw materials, and consumer environmental awareness. Europe stands as the dominant market, historically pioneering the technology (especially in Finland and Germany). The region benefits from stringent environmental legislation and a strong cultural preference for natural, durable building materials, which favor chemical-free thermal modification. North America is experiencing the fastest growth, propelled by the massive residential renovation market and the increasing use of thermally modified materials as a premium, low-maintenance alternative to chemically treated lumber and exotic hardwoods in decking and cladding. APAC is emerging rapidly, primarily focused on imports from Europe, with domestic manufacturing ramping up in countries like Japan and Australia, where performance against high humidity and insect infestation is a crucial purchasing criterion.

Thermally modified wood (TMW) offers superior dimensional stability, drastically reducing warping and twisting. Crucially, TMW achieves resistance to decay and insects using only heat and steam, making it an entirely chemical-free and non-toxic alternative, unlike traditional pressure-treated wood which relies on chemical preservatives.

Thermal modification does not typically confer significant fire resistance; it primarily enhances decay resistance and stability. In fact, standard thermal treatment can slightly increase the wood’s flammability due to reduced moisture content. Specialized fire-retardant treatments must be applied separately if fire rating compliance is required for the application.

High-quality thermally modified wood, when properly installed and maintained (via re-oiling), is certified to last 25 to 30 years or more in exterior applications, depending on the wood species and climate exposure. Its exceptional resistance to moisture absorption and biological decay ensures long-term integrity.

Both achieve high-temperature modification, but Thermo-hydro uses high-pressure steam as the protective medium during heating, which helps control moisture release. Thermo-vacuum uses a vacuum or inert gas (like nitrogen) to remove oxygen and prevent combustion. Thermo-vacuum often achieves deeper, more uniform color and slightly lower moisture content, but both enhance durability effectively.

Yes, TMW is highly sustainable as it uses abundant, often locally sourced softwoods and avoids harmful chemicals. Customers often seek certification confirming the raw wood's origin, such as the Forest Stewardship Council (FSC) or the Programme for the Endorsement of Forest Certification (PEFC), alongside specific performance classifications (e.g., Durability Class 1 or 2).

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.