ID : MRU_ 431622 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

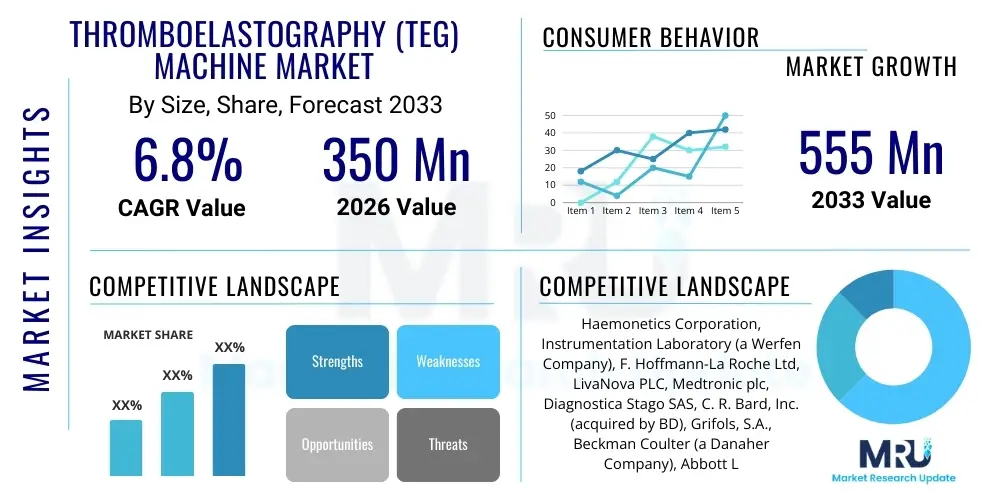

The Thromboelastography (TEG) Machine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $350 million in 2026 and is projected to reach $555 million by the end of the forecast period in 2033.

The Thromboelastography (TEG) Machine Market encompasses devices and consumables used for comprehensive viscoelastic testing of blood hemostasis. TEG provides a global assessment of coagulation, including clot formation, stabilization, and lysis, offering crucial insights beyond traditional coagulation assays like PT and aPTT. These machines are essential diagnostic tools utilized in critical care settings, operating rooms, and cardiovascular units to guide goal-directed therapy (GDT) for patients experiencing acute bleeding or hypercoagulability. The market growth is fundamentally driven by the rising prevalence of chronic diseases requiring complex surgical interventions, the increasing elderly population prone to bleeding complications, and the growing recognition of TEG's superiority in minimizing blood product usage and improving patient outcomes in trauma and cardiac surgery.

TEG machines operate by analyzing the physical properties of a blood clot as it forms under controlled conditions, producing a graphical output that details kinetic parameters such as R-time (reaction time), K-time (clot formation time), Alpha Angle (rate of clot formation), and Maximum Amplitude (clot strength). The product portfolio primarily includes benchtop and portable analyzers, along with proprietary disposable cartridges and reagents. Major applications span perioperative management, particularly in cardiothoracic surgery, liver transplantation, and obstetrics, where rapid, actionable data on patient hemostatic status is critical. Furthermore, TEG is increasingly adopted in monitoring the effects of novel anticoagulants and antiplatelet drugs, driving demand for specialized assays and software integration capabilities.

Key benefits of adopting TEG technology include faster turnaround times compared to centralized laboratory testing, which facilitates quicker clinical decision-making, particularly in emergency situations. This shift towards near-patient testing, or Point-of-Care (POC) diagnostics, is a major impetus for market expansion. Driving factors also include supportive clinical guidelines recommending viscoelastic testing for transfusion management, technological advancements leading to miniaturization and enhanced automation of devices, and intensive training programs aimed at educating critical care practitioners on the effective interpretation and application of TEG data to optimize patient safety and resource utilization.

The Thromboelastography (TEG) Machine Market is experiencing robust expansion, characterized by a fundamental shift towards decentralized and rapid testing platforms, which significantly influences business trends across key geographical regions. Manufacturers are focused on developing compact, user-friendly, and fully automated TEG systems that integrate seamlessly into high-acuity clinical environments, emphasizing ease of use to overcome the historical barrier of specialized training requirements. Mergers, acquisitions, and strategic partnerships between device manufacturers and diagnostic service providers are defining the competitive landscape, aiming to broaden global distribution networks and enhance technological interoperability. Furthermore, rigorous efforts in obtaining favorable reimbursement status for TEG testing procedures are pivotal to accelerating adoption rates in developed economies, while emerging markets present untapped potential driven by infrastructural improvements in healthcare.

Regional trends indicate North America maintaining the largest market share, attributed to established healthcare infrastructure, high awareness of coagulation disorders, and significant expenditure on advanced medical devices, particularly in trauma centers and large hospital systems. However, the Asia Pacific (APAC) region is projected to exhibit the fastest growth rate, fueled by expanding surgical volumes, rising incidence of cardiovascular diseases, improving access to sophisticated diagnostics, and increasing government investments in healthcare modernization in populous countries like China and India. Europe also remains a crucial market, distinguished by early clinical acceptance of viscoelastic testing and stringent regulatory frameworks ensuring high-quality diagnostic performance.

Analysis of segment trends reveals that the consumables segment, including reagents, cups, and pins, dominates the market revenue due to the recurring nature of purchases associated with the installed base of TEG machines. By application, cardiothoracic surgery holds the largest share, given the criticality of monitoring hemostasis during complex bypass procedures and valve replacements. However, the general surgery and obstetrics segments are poised for rapid growth, reflecting the broadening clinical utility of TEG beyond conventional high-risk specialties. Technological segmentation indicates a steady preference for traditional TEG platforms while newer technologies offering enhanced data analysis capabilities and integration with electronic health records (EHRs) gain momentum.

User queries regarding the impact of Artificial Intelligence (AI) on the TEG market frequently revolve around its potential to standardize complex clot interpretation, improve diagnostic efficiency, and predict patient outcomes more accurately than manual analysis. Common themes include whether AI algorithms can seamlessly integrate raw TEG data with other clinical parameters (e.g., patient demographics, drug history) to generate more personalized treatment recommendations, thus optimizing blood product transfusion protocols. Users are also keen to understand the regulatory pathway for AI-driven diagnostic software integrated into TEG machines and how these technologies will mitigate potential human error and variability in result interpretation, a recognized challenge in viscoelastic testing. The consensus expectation is that AI will move TEG analysis from descriptive graphical interpretation to prescriptive, automated therapeutic guidance.

The implementation of AI and machine learning (ML) algorithms is set to revolutionize the efficiency and accuracy of TEG machine utilization. AI can process the vast data generated by viscoelastic tests—including multiple kinetic parameters and dynamic changes over time—to identify subtle patterns indicative of specific coagulopathies that might be overlooked by human interpretation, especially in complex or mixed clinical scenarios. This capability significantly enhances the diagnostic sensitivity and specificity of TEG. Furthermore, ML models can be trained on large datasets correlating TEG parameters with actual patient outcomes (e.g., massive transfusion protocols, post-operative complications), enabling highly accurate predictive analytics regarding bleeding risk or thrombotic events before they manifest clinically.

Beyond diagnostics, AI facilitates the automation of quality control, monitoring instrument performance, and flagging potential issues with reagent integrity or calibration, ensuring the reliability of results. For clinicians, AI-powered decision support systems (DSS) integrated within the TEG software can provide real-time recommendations for transfusion volumes and type (e.g., platelet vs. cryoprecipitate vs. fresh frozen plasma) based on the comprehensive data analysis. This shift towards automated, personalized transfusion management is crucial for minimizing unnecessary transfusions, reducing associated risks, and substantially lowering healthcare costs, thereby driving significant clinical value and increasing the market attractiveness of next-generation TEG platforms.

The Thromboelastography (TEG) Machine Market is influenced by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO), collectively constituting the market's impact forces. A primary driver is the global paradigm shift towards personalized medicine and goal-directed therapy (GDT) in hemorrhage management, where TEG offers essential real-time diagnostic capabilities crucial for tailoring treatment protocols, minimizing complications, and conserving expensive blood products. Coupled with this, the expanding scope of high-risk surgical procedures, particularly in cardiovascular and trauma surgery, mandates sophisticated hemostasis monitoring, sustaining demand for reliable viscoelastic testing equipment. These drivers exert a positive push force on the market, encouraging continuous innovation in device portability and automation.

However, significant restraints temper the market’s growth trajectory. The relatively high initial capital expenditure required for acquiring TEG machines, coupled with the recurring costs of proprietary consumables, presents a formidable financial barrier, particularly for smaller healthcare facilities or those in budget-constrained emerging markets. Furthermore, the specialized nature of TEG results necessitates expert interpretation, and despite advancements, a perceived lack of standardized training and reluctance among some practitioners to transition from traditional coagulation assays impede broader clinical adoption. These restraints introduce friction, requiring market participants to focus on cost-effectiveness studies and educational outreach to demonstrate clear ROI.

Opportunities for expansion lie predominantly in two areas: geographical penetration into underserved regions, particularly Latin America and APAC, and clinical utility expansion into non-traditional settings such as outpatient clinics and primary care screening for inherited coagulopathies. Technological advancements, specifically the development of miniaturized, fully disposable cartridge systems and enhanced connectivity features (IoT integration), promise to overcome the complexity barrier and broaden Point-of-Care applications. The impact forces indicate a market poised for accelerated adoption, provided manufacturers successfully navigate pricing sensitivity and standardize educational resources to foster greater clinical confidence in TEG diagnostics.

The Thromboelastography (TEG) Machine Market is systematically segmented based on Product Type, Application, End-User, and Technology. This segmentation allows for precise market analysis, identifying high-growth pockets and niche areas within the broader diagnostic landscape. By Product Type, the market is categorized into Instruments/Analyzers and Reagents & Consumables. The consumables segment typically generates higher recurring revenue due to the nature of diagnostic testing, sustaining profitability for vendors. The Application segmentation is crucial as it reflects the primary clinical environments where TEG is indispensable, with cardiac surgery historically dominating, but expanding adoption in general trauma and liver transplantation providing future growth vectors. Understanding these segments helps manufacturers tailor marketing strategies and product development to specific clinical needs and utilization patterns.

Segmentation by End-User distinguishes between primary consumers of TEG technology, namely Hospitals and Clinics, Diagnostic Laboratories, and Point-of-Care Settings. Hospitals, particularly those with high-volume surgical units and intensive care facilities, represent the largest end-user segment due to the immediate need for rapid hemostasis monitoring. The Point-of-Care (POC) segment, encompassing operating rooms, emergency departments, and mobile medical units, is projected to witness the fastest growth rate, directly driven by the increasing availability of portable TEG systems and the clinical imperative for rapid results in acute care management. Furthermore, analyzing the market by Technology, differentiating between standard TEG and newer resonant frequency viscoelastometry (like ROTEM), provides insight into competitive dynamics and the diffusion rate of competing viscoelastic testing modalities, noting the functional equivalence but differing technological approaches.

Effective segmentation analysis reveals that future market growth will be heavily dependent on penetration into the POC and Diagnostic Laboratory segments, requiring cost optimization and greater throughput capabilities. The instruments segment is witnessing innovation focused on automation, reduced sample volume requirements, and enhanced data management features to minimize operational complexity. Strategic investment will be channeled towards developing specialized reagent panels that enable accurate assessment of patients on different types of novel oral anticoagulants (NOACs), thereby capitalizing on the growing need for personalized anticoagulation management and ensuring TEG relevance in evolving pharmacotherapy landscapes.

The value chain for the Thromboelastography (TEG) Machine Market starts with upstream activities involving the sourcing and refinement of specialized components and raw materials crucial for manufacturing sophisticated diagnostic devices and high-precision proprietary consumables. This includes electronics manufacturing for the analyzer units, precision engineering for mechanical components (e.g., torsion wires, measuring systems), and the chemical synthesis of lyophilized reagents and activators required for sample testing. Key success factors in the upstream phase involve maintaining stringent quality control, securing specialized components at competitive costs, and continuous R&D to enhance sensor technology and improve reagent stability, all of which directly influence the final product quality and manufacturing efficiency.

Midstream activities encompass the core manufacturing, assembly, and testing of the TEG instruments and related consumables. This stage involves complex assembly processes, rigorous calibration, and software development for data analysis and user interface design. Distribution channel strategies form a critical part of the downstream value chain. Manufacturers utilize both direct sales forces, particularly in major developed markets like the US and Western Europe, to handle high-value capital equipment sales and provide technical support, and indirect channels through specialized medical device distributors or regional agents to penetrate smaller markets and manage consumable distribution efficiently. The choice of channel strategy heavily depends on regional regulatory requirements, existing clinical relationships, and the necessary level of after-sales technical support.

The ultimate downstream activities focus on market penetration, clinical adoption, and post-sale service. Successful market access requires robust clinical validation studies, favorable reimbursement codes, and extensive training programs for end-users. Direct channels offer better control over training and service quality, which is vital for complex diagnostic tools like TEG. Indirect channels often rely on the distributor's existing network in hospitals and labs. Continuous after-sales service, including maintenance, software updates, and reliable supply of consumables, is crucial for maintaining customer loyalty and maximizing the long-term profitability generated by the installed base of TEG machines.

The primary purchasers and end-users of Thromboelastography (TEG) machines are highly specialized clinical facilities requiring rapid and comprehensive assessment of hemostatic function. Hospitals constitute the largest customer segment, driven particularly by surgical departments such as cardiothoracic, orthopedic, and neurosurgery, where large blood losses and complex coagulation issues are common. Within the hospital setting, the Intensive Care Units (ICUs) and Emergency Departments (EDs) are increasingly adopting TEG for managing sepsis, major trauma, and severe coagulopathy, reflecting the device's utility in time-critical diagnosis and patient stabilization.

Beyond the hospital environment, independent specialized diagnostic laboratories and blood banks represent significant potential customers. Diagnostic labs utilize TEG machines for specialized testing services, monitoring patients on anticoagulation therapy, and performing research studies on novel clotting disorders. Blood banks may employ TEG to assess the quality and functional integrity of stored blood products, although this remains a niche application compared to critical care settings. These customers prioritize high throughput, automation, and reliable calibration capabilities to meet demanding quality standards.

Furthermore, the growing trend toward Point-of-Care (POC) testing is expanding the customer base to include military field hospitals, mobile medical units, and potentially specialized private surgical clinics. These POC buyers place high value on device portability, robustness, minimal maintenance requirements, and the ability to operate effectively with limited technical expertise. The expansion into these diverse settings is crucial for the sustained growth of the market, necessitating continuous product innovation focused on miniaturization and user-friendliness to cater to these varied end-user requirements effectively.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $350 million |

| Market Forecast in 2033 | $555 million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Haemonetics Corporation, Instrumentation Laboratory (a Werfen Company), F. Hoffmann-La Roche Ltd, LivaNova PLC, Medtronic plc, Diagnostica Stago SAS, C. R. Bard, Inc. (acquired by BD), Grifols, S.A., Beckman Coulter (a Danaher Company), Abbott Laboratories, Nihon Kohden Corporation, HemoSonics, LLC, Scott Laboratory, Entegris, Inc., Life Science Production, Inc., Stago International, Thermo Fisher Scientific Inc., Sienco, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Thromboelastography (TEG) Machine Market is characterized by continuous evolution aimed at enhancing accuracy, improving workflow efficiency, and expanding accessibility through Point-of-Care (POC) delivery. The core technology remains viscoelastometry, which measures the mechanical properties of clot formation, but modern systems incorporate advanced computational analysis and automated features. Key technological shifts involve the integration of microfluidics and biosensors to reduce the required blood sample volume and decrease test turnaround time, critical requirements in acute care settings where every minute counts. Furthermore, connectivity standards, including HL7 interface protocols, are becoming essential for seamless integration of TEG data into Hospital Information Systems (HIS) and Electronic Health Records (EHRs), streamlining patient management and reducing manual data entry errors.

A significant area of innovation is the development of fully disposable, pre-calibrated cartridge systems. These systems simplify the testing procedure by eliminating the need for manual pipetting and reagent handling, thereby minimizing operator error and the dependency on highly specialized lab technicians. Competitively, companies are investing in differentiation based on the proprietary assays offered, particularly those designed to specifically evaluate platelet function or the effects of various antiplatelet agents and direct oral anticoagulants (DOACs). This specificity allows clinicians to make highly targeted treatment decisions, moving beyond general coagulation assessment. The push for portable devices is also driving miniaturization, leveraging robust components that can withstand the demanding environments of trauma centers and remote clinical settings without compromising analytical precision.

The future technology roadmap for TEG machines involves deeper integration of machine learning for pattern recognition in coagulation disorders and the adoption of advanced graphical visualization tools to help clinicians better interpret complex, multi-parameter outputs. Furthermore, the market is seeing convergence with other diagnostic technologies, potentially offering combined platforms that measure both viscoelastic properties and molecular markers (e.g., D-dimer, fibrinogen levels) simultaneously on a single, integrated instrument. This comprehensive approach promises to provide a more complete picture of the patient's hemostatic status, solidifying TEG's role as the gold standard for dynamic coagulation monitoring in critical care and high-risk surgical environments. Regulatory compliance for these highly integrated devices, particularly regarding software validation, represents a major technological and operational challenge that manufacturers must successfully address.

Regional dynamics play a crucial role in shaping the demand and adoption patterns of the Thromboelastography (TEG) Machine Market, influenced by varying healthcare expenditure, clinical guidelines, and population demographics across the globe.

TEG provides a comprehensive, real-time viscoelastic assessment of the entire coagulation process—from initiation through clot formation, stabilization, and lysis—unlike traditional tests (PT/aPTT) which only measure specific time endpoints. This holistic view is crucial for guiding Goal-Directed Therapy (GDT) and optimizing blood product transfusion in critical settings.

The highest demand is driven by applications requiring rapid assessment of complex hemostasis, primarily cardiothoracic surgery (especially bypass procedures), liver transplantation, and major trauma management. These settings rely on TEG for immediate diagnosis of acquired coagulopathies and minimizing catastrophic hemorrhage.

Yes, the market is undergoing a strong shift towards POC testing. Technological advancements leading to the development of portable, user-friendly, and highly automated TEG systems are enabling rapid deployment in operating rooms, ICUs, and emergency departments, reducing critical turnaround times significantly.

Reagents and proprietary consumables (cups, pins, and cartridges) are crucial, generating the dominant share of recurring revenue for manufacturers. This continuous demand stems directly from the installed base of TEG instruments, ensuring long-term profitability and sustainable market growth.

AI integration is expected to enhance TEG utility by automating the complex interpretation of viscoelastic graphs, reducing operator variability, and enabling predictive analytics for patient outcomes (e.g., hemorrhage or thrombosis risk). AI also supports clinical decision-making with prescriptive therapeutic guidance in real time.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.