ID : MRU_ 438995 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

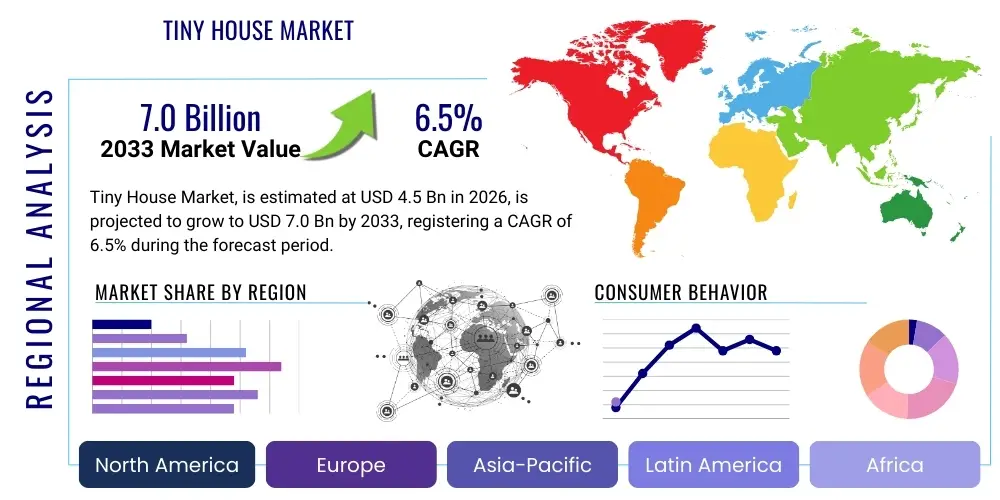

The Tiny House Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at $4.5 Billion in 2026 and is projected to reach $7.0 Billion by the end of the forecast period in 2033. This growth trajectory is fundamentally supported by shifting consumer preferences towards sustainable and affordable housing solutions, particularly among Millennials and Baby Boomers seeking simplified lifestyles. The market size expansion reflects not only increased adoption in core North American and European markets but also nascent growth in Asia Pacific regions where land scarcity drives innovation in compact dwelling design.

The valuation reflects the increasing acceptance of tiny houses not just as recreational vehicles or temporary shelters, but as viable, long-term primary residences. Factors contributing significantly to the market valuation include the rising cost of traditional construction and mortgages, coupled with regulatory adjustments in various municipalities permitting tiny homes on foundations or as auxiliary dwelling units (ADUs). Furthermore, advancements in prefabricated construction techniques and modular design are improving the efficiency and speed of construction, making tiny houses more accessible to a broader consumer base and pushing the overall market value upwards.

Geographically, North America currently holds the largest market share, driven by strong cultural movements emphasizing minimalism and financial independence. However, the future growth rate is expected to be substantially high in regions like Europe, where environmental sustainability is a primary policy focus, and in developing economies facing rapid urbanization and density challenges. The integration of smart home technologies and energy-efficient building materials further differentiates the product offerings, attracting premium segments and bolstering the average selling price, which in turn elevates the total market size projection for 2033.

The Tiny House Market encompasses the design, manufacture, and sale of residential structures typically ranging from 100 to 400 square feet, built on foundations or wheels. These dwellings offer a compelling alternative to conventional housing, addressing critical needs related to housing affordability, environmental sustainability, and lifestyle minimalism. The product description spans various structural types, including custom-built, prefabricated, and modular units, often emphasizing multi-functional furniture, optimized storage, and high energy efficiency. Major applications include primary residences, vacation rentals, guest houses (ADUs), and specialized community developments, such as planned tiny house villages aimed at offering affordable living solutions for specific demographics like retirees or low-income populations.

The inherent benefits of tiny houses are manifold, primarily revolving around significant cost savings, reduced environmental footprint due to lower material consumption and energy needs, and greater financial freedom derived from reduced mortgage burdens or property taxes. Driving factors include escalating urban housing costs, increased desire for nomadic or flexible living arrangements, and a growing societal movement advocating for downsized, simpler living. Furthermore, favorable shifts in zoning and building codes across progressive municipalities are legitimizing tiny homes as permanent housing, thereby accelerating market adoption. The psychological appeal of decluttering and focusing resources on experiences rather than extensive property maintenance also fuels consumer interest, particularly among younger generations disillusioned with traditional homeownership models.

Market dynamics are characterized by intense competition among custom builders, large-scale modular manufacturers, and DIY suppliers catering to different segments of the consumer base. The market faces a constant need for innovation in maximizing space utility and integrating resilient, lightweight construction materials. Regulatory fragmentation remains a structural challenge, requiring manufacturers to tailor products to hyper-local codes. Despite these hurdles, the robust demand fueled by economic volatility and environmental consciousness positions the Tiny House Market for sustained, long-term expansion as it transitions from a niche movement to a recognized segment of the broader residential construction industry, influencing sustainable urban planning strategies globally.

The Tiny House Market demonstrates robust expansion, underpinned by converging business trends, shifting consumer demographics, and improving regulatory environments. Key business trends include the vertical integration of design, manufacturing, and distribution channels to streamline the construction process, moving from highly customized, site-built models to standardized, mass-produced prefabricated units. This shift enhances scalability and reduces turnaround times, directly impacting profitability margins for major players. Furthermore, increased investment in digital visualization tools and virtual reality (VR) technologies is improving the customization experience for buyers, despite the constraints of smaller footprints. Strategic alliances between tiny house builders and finance providers specializing in non-traditional mortgages are also crucial business accelerators, addressing a historical barrier to entry for potential homeowners.

Regional trends indicate North America retaining its leadership, yet the Asia Pacific region, particularly Australia and Japan, is showing accelerated growth driven by innovation in disaster-resilient and space-saving urban dwellings. Europe is focused heavily on the sustainability aspect, with Scandinavian countries and Germany emphasizing high-performance insulation, passive house principles, and renewable energy integration within tiny house designs, often linking them to eco-tourism initiatives. The market observes a significant segment trend where tiny houses on wheels (THOWs) dominate in regions with restrictive foundation regulations, providing flexibility, while foundation-based tiny homes are gaining ground in established tiny house communities or as formal ADUs, capitalizing on permanent land integration and easier financing structures. The premium segment is showing a preference for technologically integrated smart homes, demanding higher quality finishes and custom layouts.

Overall, the market is poised for continued fragmentation initially, followed by consolidation as standardized building practices and certifications become more widespread. The primary strategic imperative for industry stakeholders is navigating the complex patchwork of zoning regulations and leveraging technological advancements, such as advanced Computer-Aided Design (CAD) and precision robotics, to optimize construction. Consumer demand is tilting towards comprehensive, turnkey solutions that include land acquisition and utility connection assistance, suggesting that future market success depends on offering end-to-end services beyond just the physical structure, solidifying the market's transition into a mature residential alternative globally.

Common user inquiries regarding the impact of Artificial Intelligence (AI) on the Tiny House Market center primarily on how technology can solve the intrinsic challenge of maximizing small spaces efficiently, the potential for AI-driven construction cost reduction, and the role of smart systems in enhancing the living experience within constrained environments. Users frequently question whether AI tools can autonomously generate optimal floor plans based on specific lifestyle requirements (e.g., remote work, pet ownership, specific hobbies) and how AI can ensure compliance with varying hyper-local building codes during the design phase. A key theme revolves around AI's ability to automate parts of the modular construction process, thereby reducing labor costs and improving precision, addressing concerns about the overall cost of custom-built units. Furthermore, there is significant interest in predictive maintenance systems and energy management within tiny homes, utilizing AI to optimize resource consumption and reduce utility expenses, thereby reinforcing the core appeal of affordability and sustainability.

The integration of AI algorithms into the tiny house design phase represents a paradigm shift, enabling generative design processes that rapidly iterate through thousands of layout options, ensuring structural integrity, ergonomic optimization, and regulatory adherence simultaneously. These tools leverage machine learning to analyze successful compact space utilization techniques, consumer feedback, and material stress tolerance, resulting in highly optimized, bespoke designs that maximize every cubic foot. This capability is vital in a segment where customization is highly valued but traditional architectural services can be cost-prohibitive. AI thus democratizes high-quality, efficient design, moving beyond generic templates and offering personalized solutions at scale, fundamentally altering the competitive landscape among design firms and manufacturers.

In the construction and operational phases, AI significantly enhances efficiency and sustainability. Predictive analytics powered by AI monitors sensor data related to structural health, energy usage (HVAC, lighting), and internal climate control, adjusting systems autonomously to maintain optimal conditions while minimizing waste. Furthermore, in modular manufacturing facilities, AI-driven robotics can perform high-precision cutting, assembly, and quality control tasks, drastically improving construction speed and reducing material scrap rates. This optimization is critical for maintaining the affordability advantage of tiny houses. The long-term impact suggests AI will facilitate the creation of truly intelligent, resilient, and highly customized tiny homes that seamlessly adapt to occupant needs and external environmental changes, reinforcing the market's appeal to tech-savvy consumers.

The dynamics of the Tiny House Market are shaped by a complex interplay of Drivers, Restraints, and Opportunities (DRO), all subject to significant Impact Forces stemming from macroeconomic conditions, social shifts, and technological advancements. Key drivers include the overwhelming crisis of housing affordability globally, particularly in developed nations, prompting consumers to seek viable, low-cost alternatives. Concurrently, a burgeoning cultural shift toward minimalism and environmental consciousness strongly supports the market, as tiny homes inherently offer reduced consumption and lower ecological footprints. Opportunities are abundant in the form of developing specialized tiny house communities, partnering with government bodies to address homelessness and disaster relief housing needs, and integrating advanced off-grid sustainable technologies such as composting toilets and advanced water recycling systems.

Restraints primarily revolve around the fragmented and often contradictory regulatory landscape. Zoning restrictions often prohibit tiny homes as permanent dwellings, limiting their market penetration to specific, approved zones or non-regulated land. Financing remains a significant hurdle, as tiny homes, especially those on wheels, are often classified as recreational vehicles rather than real property, making traditional mortgages unavailable and relying instead on higher-interest personal loans or chattel mortgages. The negative perception of tiny homes as temporary or substandard housing in some traditional communities also acts as a social restraint. These barriers necessitate constant advocacy and adaptation from industry players, requiring substantial efforts to educate municipalities and financial institutions regarding the legitimate status and durability of modern tiny house constructions.

The principal impact forces influencing the market trajectory are socioeconomic shifts, specifically the purchasing power and preferences of Millennials and Generation Z, who prioritize flexibility and experiences over extensive material possessions. Technological innovation in modular and prefabricated construction significantly reduces the cost barrier and improves quality control, pushing adoption. Furthermore, legislative changes, particularly the proliferation of favorable ADU (Accessory Dwelling Unit) legislation in North America, are acting as powerful catalysts, instantly expanding the allowable application scope of tiny homes. The market's resilience is tied directly to its ability to leverage these opportunities while systematically overcoming regulatory and financial friction points, ensuring that the foundational appeal of affordability and sustainability translates into accessible, mainstream housing solutions.

The Tiny House Market is segmented based on structure type, foundation type, size, and application, reflecting the diverse needs and regulatory requirements across the global consumer base. Understanding these segments is crucial for manufacturers to tailor their production lines and marketing strategies. The structural segmentation primarily differentiates between standard tiny homes built using conventional materials and techniques, and modular/prefabricated units which prioritize rapid assembly and standardization. Foundation type segmentation is arguably the most critical, dictating regulatory status and financing options, dividing the market into Foundation-based (permanent) and Tiny Houses on Wheels (THOWs, portable). Application segmentation identifies whether the unit serves as a primary residence, a vacation rental, or an Auxiliary Dwelling Unit (ADU), each demanding different features regarding longevity, utility connections, and internal amenities. These segments are highly interconnected, with THOWs often favored for recreational or interim housing, while foundation-based units are essential for integration into formal housing markets.

Segmentation by size is another key differentiator, generally categorized into Small (under 150 sq ft), Medium (150-300 sq ft), and Large (300-400 sq ft). Larger units are increasingly popular as they offer a better balance between minimalism and functional family living, often appealing to established couples or small families seeking affordable primary housing without extreme sacrifices in comfort. Conversely, the smallest units are typically chosen by single occupants or for specific niche applications like mobile offices or specialized backyard studios. The material used for construction also provides a segmentation lens, classifying units based on conventional wood framing, steel framing, or innovative materials like shipping containers or structural insulated panels (SIPs). Steel framing and SIPs are gaining traction due to superior durability, quicker assembly, and enhanced energy efficiency, aligning with the market's long-term sustainability goals.

Geographic segmentation remains essential, as regulatory environments dramatically impact product feasibility. North American segments focus heavily on customization and off-grid capabilities, driven by expansive rural areas and a strong DIY culture. European segments prioritize highly engineered, passive house standards and material sustainability. The strategic objective for market participants is often to specialize in one or two segments—such as high-end modular THOWs catering to the digital nomad demographic—and then geographically replicate that successful model, adapting only where required by local building codes, thereby achieving economies of scale and strategic market dominance.

The Value Chain for the Tiny House Market begins with Upstream Analysis, focusing on the procurement and processing of raw materials. This stage is dominated by suppliers of lumber, steel, and advanced materials like SIPs, alongside specialized components such as compact appliances, multi-functional furniture hardware, and highly efficient insulation materials. Key competitive advantages at this stage include securing sustainable and locally sourced materials, ensuring compliance with green building standards (e.g., FSC certified wood), and establishing reliable supply relationships to manage volatile raw material costs. Manufacturers often seek customized, miniaturized versions of standard home components, driving innovation in the upstream supplier ecosystem, particularly concerning lightweight, durable, and space-saving utility systems like HVAC and plumbing.

The core segment of the value chain is the Manufacturing and Assembly process. This involves design, fabrication, assembly, and quality control. Direct distribution channels are prominent, especially for custom builders who manage the entire customer relationship from initial design consultation to final delivery or site setup. For prefabricated and modular units, the distribution channel often involves dedicated dealerships or authorized distributors who handle sales, financing coordination, and local regulatory navigation, acting as crucial intermediaries between the factory and the end consumer. Indirect distribution channels, such as large online retailers specializing in kits or shell units, cater primarily to the DIY segment, offering cost savings but requiring significant customer involvement in the construction phase. The efficiency of the manufacturing process, particularly the adoption of lean assembly lines and robotic precision, determines the final unit cost and time-to-market.

Downstream analysis centers on the logistics of transporting and placing the finished unit, site preparation, utility connection, and after-sales service. Given the physical constraints of transporting large structures, logistical proficiency is paramount, especially for wider units requiring specialized permits and transport escorts. After-sales support, including warranty services and assistance with long-term maintenance and potential modifications, is critical for establishing brand reputation and customer loyalty. The end-user financing process is a bottleneck, highlighting the importance of partnerships with specialty lenders or credit unions familiar with tiny house asset valuation. Success in the downstream segment hinges on providing comprehensive, end-to-end solutions that mitigate the logistical and financial complexities faced by the consumer, thereby maximizing the total delivered value of the product.

The primary End-Users/Buyers of tiny house products represent a diverse demographic unified by a shared pursuit of affordability, financial independence, and a desire for simplified, intentional living. The largest segment includes Millennials and younger generations entering the housing market who are disillusioned by prohibitive property costs and massive student debt loads, seeing tiny homes as the most realistic path to homeownership. This group highly values technological integration, customization, and mobile flexibility, often leveraging THOWs to navigate employment mobility or urban rental market volatility. They prioritize minimalist aesthetics and sustainable features, viewing the purchase as both an economic and ethical decision, driving demand for smart, off-grid compatible systems.

Another rapidly expanding potential customer group comprises Baby Boomers and retirees seeking to downsize their primary residences, simplify maintenance, and unlock capital for retirement. This demographic often prefers foundation-based units integrated as ADUs on family property or situated within planned tiny house communities that offer amenities and a supportive social structure. Their focus is less on mobility and more on accessibility, single-level living, and high-quality, durable construction. Furthermore, the market encompasses specialized buyers such as entrepreneurs needing compact, non-traditional commercial spaces, municipalities requiring affordable or emergency housing solutions, and the hospitality sector utilizing tiny homes for unique, experiential vacation rentals (glamping, eco-resorts), demanding high-end finishes and robust rental durability.

A critical, high-potential segment involves individuals seeking solutions for Accessory Dwelling Units (ADUs). As regulatory environments soften, homeowners are increasingly purchasing tiny houses—both portable and foundation-based—to serve as guest quarters, home offices, or rental units to generate passive income. These customers prioritize ease of installation, compliance with stringent local codes, and aesthetic integration with the main property. The strategic importance of this segment lies in its large, untapped size and the increasing political momentum favoring ADU expansion as a solution to urban density and housing shortages, suggesting significant long-term growth driven less by lifestyle choice and more by practical, financial utility.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $4.5 Billion |

| Market Forecast in 2033 | $7.0 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Tumbleweed Tiny House Company, Getaway House, Skyline Champion Corporation, Koto Design, Minimaliste, American Tiny House, New Frontier Tiny Homes, Tru Form Tiny, Suma Design, Escape Traveler, Custom Container Living, Tiny Heirloom, Handcrafted Movement, Modern Tiny Living, VIVA Collectiv, Wheelhaus, Oregon Cottage Company, Movable Roots, Rocky Mountain Tiny Houses, B&B Tiny Houses |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Tiny House Market relies heavily on specialized and innovative technologies to maximize utility within a minimal footprint, focusing particularly on advanced manufacturing techniques and smart home integration. A critical technological foundation involves modular and prefabricated construction methodologies, utilizing precision cutting technologies such as CNC (Computer Numerical Control) machines and laser-guided assembly systems. These technologies ensure extremely accurate material fabrication, minimizing waste, accelerating the construction timeline (often reducing build time from months to weeks), and guaranteeing structural uniformity necessary for transport. The use of advanced materials, including Structural Insulated Panels (SIPs) and lightweight steel framing, significantly improves thermal performance and structural rigidity compared to traditional stick-built housing, directly enhancing the tiny home's long-term value proposition and energy efficiency.

Space-saving innovations represent another vital technological domain. This includes the development and integration of multi-functional and transforming furniture—such as Murphy beds, convertible dining tables, and built-in vertical storage systems—often operating with hydraulic or electromechanical assistance. These specialized components require precise engineering to ensure reliability and seamless operation. Furthermore, the market is increasingly adopting compact, energy-efficient appliances, including combination washer/dryers and highly efficient tankless water heaters, which are essential for maintaining comfort without consuming excessive space or electricity. The focus on hyper-efficient utilities supports the crucial off-grid capabilities demanded by many tiny house owners, relying on composting toilets and advanced water filtration systems.

The modern tiny house is rapidly transforming into a smart home, integrating technologies that enhance security, energy management, and remote monitoring. Key elements of this technological landscape include centralized smart hubs managing lighting, climate control, and security features via voice command or mobile applications. Energy optimization is often achieved through sophisticated solar panel arrays and battery storage systems, managed by AI algorithms that predict energy needs based on weather patterns and usage habits. Connectivity solutions, including specialized mobile broadband setups and satellite internet, are critical for owners who utilize tiny homes for remote work or nomadic living. This technological sophistication is essential for the market's mainstream acceptance, assuring consumers that downsizing does not necessitate sacrificing modern comforts or professional connectivity.

The market growth is primarily driven by the escalating global housing affordability crisis, consumer shifts toward minimalist and sustainable lifestyles, and regulatory changes in many regions that are increasingly accepting tiny homes as legal Accessory Dwelling Units (ADUs) or permanent residences. Economic volatility and the desire for financial freedom among younger generations also accelerate adoption.

The main challenge is that Tiny Houses on Wheels (THOWs) are often classified as recreational vehicles or chattel property rather than real estate, making them ineligible for conventional mortgages. Buyers typically rely on higher-interest personal loans, RV loans, or specialized lending products, which increases the total cost of ownership compared to traditional housing finance.

THOWs offer mobility and often bypass restrictive traditional building codes, making them popular for nomadic lifestyles or placement in areas where permanent structures are prohibited. Foundation-based tiny homes, however, generally qualify for traditional property status, are easier to insure, and are necessary for long-term community integration and formalized ADU usage.

Multi-functional, transforming furniture systems are critically important for spatial efficiency, allowing limited square footage to serve multiple purposes. Equally important are integrated smart home systems and high-efficiency building materials (like SIPs) that maximize energy savings and reduce the ongoing operational costs, reinforcing the economic benefit.

The market is expected to consolidate gradually. While custom builders will maintain a significant presence in the high-end, niche segment, the increasing demand for affordability and scalability will favor larger modular and prefabricated manufacturers who can standardize designs, leverage AI-driven construction, and navigate complex regulations more efficiently across multiple jurisdictions.

The sustained expansion of the Tiny House Market is inextricably linked to macroeconomic trends, particularly those impacting consumer debt and housing supply. High inflation rates in raw materials, such as lumber and steel, have presented a significant challenge to maintaining the cost-effectiveness of tiny homes, forcing manufacturers to innovate in supply chain management and material substitution. Despite these cost pressures, the relative affordability gap between traditional residential homes and even premium tiny homes continues to widen, reinforcing the value proposition of downsized living. Furthermore, the demographic shift involving older generations seeking equity release through downsizing and younger generations avoiding large mortgage burdens creates a dual market demand, ensuring persistent vitality across varied socioeconomic strata. The market's resilience during economic downturns suggests it acts as a counter-cyclical hedge against high interest rates and tight credit availability in the conventional housing sector, providing a robust foundation for forecast period growth.

A crucial market dynamic involves the normalization of non-traditional living arrangements. What was once viewed as an extreme lifestyle choice is now transitioning into a credible segment of the residential market, driven by powerful social influencers and increasing media acceptance. This shift is manifesting in formalized development projects, such as purpose-built tiny house villages and specialized vacation resort concepts that capitalize on the trend. These planned communities often address the primary restraint of land acquisition and zoning by providing shared infrastructure, community amenities, and streamlined regulatory compliance, making the tiny house lifestyle more accessible and appealing to mainstream consumers. The successful development of these community models is instrumental in proving the long-term viability and stability of tiny homes as permanent housing, encouraging further municipal acceptance and easing the regulatory friction that currently inhibits widespread adoption.

In terms of competitive dynamics, the market is characterized by a high degree of specialization. Companies are differentiating themselves not only through design aesthetics—ranging from rustic farmhouse styles to ultra-modern Scandinavian minimalism—but also through specialized services. Full-service providers who handle everything from design and financing consultation to site preparation and utility hookups are gaining a competitive edge over simple kit suppliers. The ability to offer robust warranties and ensure compliance with stringent regional requirements (e.g., hurricane resistance in coastal zones or seismic standards) is becoming a non-negotiable factor. As the market matures, consolidation is anticipated, driven by larger modular builders acquiring smaller, design-focused custom firms to integrate their specialized expertise into scalable, standardized production models, thereby streamlining the fragmented supply landscape.

The regulatory environment remains the single most impactful external factor governing the market's trajectory. Zoning ordinances, which often categorize tiny homes based on their dimensions, foundations, and connections to utilities, vary dramatically between jurisdictions, creating a compliance labyrinth for manufacturers and consumers. Historically, many localities enforced minimum square footage requirements for primary residences, effectively banning tiny homes. However, a significant trend towards progressive regulatory reform is observed, particularly the widespread adoption of specific allowances for ADUs, often capped at 400-500 square feet, which legitimizes foundation-based tiny houses as backyard rentals or guest homes. The acceptance of the International Residential Code (IRC) Appendix Q in various states provides a pathway for code-compliant tiny houses, standardizing requirements related to emergency egress, ceiling height, and loft access, which is crucial for reducing legal ambiguity and enhancing consumer confidence.

For Tiny Houses on Wheels (THOWs), the primary regulatory constraint involves their classification. If titled as RVs, they face limitations on long-term residency and placement, often being restricted to official RV parks. Efforts are underway by industry associations to lobby for a distinct legal category that recognizes THOWs as habitable dwellings rather than purely recreational vehicles, a change that would unlock significant market potential. The lack of uniformity in inspection and certification processes also poses a strategic hurdle. Manufacturers must often obtain multiple state or provincial certifications, adding to production costs and complexity. Future growth heavily depends on the industry's collective effort to push for federal or national standardization bodies to streamline approvals, similar to what exists for manufactured housing, allowing builders to achieve national scale without the current localized compliance burden.

Looking forward, regulatory modernization is anticipated to accelerate, driven by political pressure to address housing shortages and climate change mitigation goals. Municipalities are increasingly recognizing tiny homes as a practical tool for increasing housing density without extensive infrastructure overhaul. We project a future where dedicated tiny house zoning overlays become commonplace in urban fringes and suburban areas. Furthermore, environmental regulations demanding zero-net-energy homes will align favorably with the inherent design characteristics of tiny houses. The successful integration of tiny houses into mainstream society will thus rely on collaborative efforts between industry stakeholders, advocacy groups, and local governments to finalize and standardize the regulatory framework, transforming tiny homes from a regulatory outlier into a recognized and integral component of modern affordable housing policy.

Sustainability is not merely a feature but a fundamental pillar of the Tiny House Market’s appeal, driving significant material innovation and construction trends. Tiny houses inherently reduce resource consumption, requiring fewer materials for construction and consuming significantly less energy for heating and cooling compared to conventional homes. The trend toward utilizing reclaimed, recycled, and locally sourced materials minimizes the carbon footprint of the building process. Advanced material adoption, particularly Structural Insulated Panels (SIPs), is rising due to their superior insulation properties, which far exceed those of standard wood framing, drastically reducing energy needs. Furthermore, the shift towards durable, low-maintenance exterior cladding, such as metal siding and composite materials, is designed to increase the longevity of the structure and reduce the long-term environmental impact associated with ongoing maintenance.

The push for off-grid capabilities is intrinsically linked to material and technology trends. High-efficiency systems, including advanced lithium-ion battery banks coupled with monocrystalline solar arrays, are becoming standard features, enabling owners to achieve complete energy independence. Water conservation technologies, such as rainwater harvesting systems, greywater recycling, and composting or incinerating toilets, eliminate the need for traditional septic or municipal sewer connections in remote settings. This technological adoption enhances the marketability of tiny homes to environmental conscious buyers and those seeking to reduce monthly utility expenses, reinforcing the core economic and ecological appeal of the dwelling.

Green building certifications and standards, such as LEED or Passive House principles, are increasingly being applied to tiny house design, establishing benchmarks for performance and quality. Manufacturers are leveraging these certifications in their marketing to demonstrate commitment to environmental stewardship and verifiable energy efficiency. The future of tiny house material innovation lies in bio-based composites, lightweight smart materials, and construction waste minimization technologies. The commitment to superior sustainability performance differentiates the tiny house segment from other forms of minimalist or temporary housing, positioning it as a leader in environmentally responsible residential construction and driving demand from government bodies and non-profit organizations focused on green housing initiatives.

Consumer behavior within the Tiny House Market is heavily influenced by a fundamental desire for simplification and prioritization of experiences over possessions. This segment is characterized by intentional consumption, focusing on quality, durability, and functionality in their purchases. The motivation extends beyond mere cost savings; it represents a philosophical opposition to consumerism and a preference for reduced psychological burden associated with maintaining a large property. This demographic often seeks customizable solutions that reflect their unique lifestyle, such as integrated home offices for remote work, specialized storage for hobbies (e.g., outdoor gear), or pet-friendly features, placing high value on intelligent, space-saving design over sheer volume.

The digital nomad culture and the rise of remote work have created a significant sub-segment of consumers who require mobile, fully connected living solutions. These buyers demand robust internet connectivity, ergonomic workspaces, and the ability to relocate frequently without disrupting their professional lives. This fuels the demand for high-end THOWs equipped with sophisticated electrical systems, dedicated battery backups, and state-of-the-art telecommunications infrastructure. Manufacturers must strategically address this need by providing integrated technology packages and warranty support for systems that are often complex and sensitive to movement, ensuring the tiny home functions effectively as a mobile professional office.

Furthermore, the communal aspect of tiny house living is a growing behavioral driver. Many consumers are actively seeking specialized tiny house communities, valuing the social interaction, shared resources (e.g., communal laundry, gardens, workshops), and built-in support network these developments offer. For retirees and older demographics, these communities mitigate the isolation often associated with downsizing. For developers, understanding this preference for community and social infrastructure is key to successful project planning, as the appeal often transcends the physical dwelling unit itself, centering on the holistic lifestyle and social environment offered. This convergence of financial prudence, environmental ethics, and community seeking behavior solidifies the long-term viability and growth potential of the tiny house lifestyle movement.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.