ID : MRU_ 438744 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

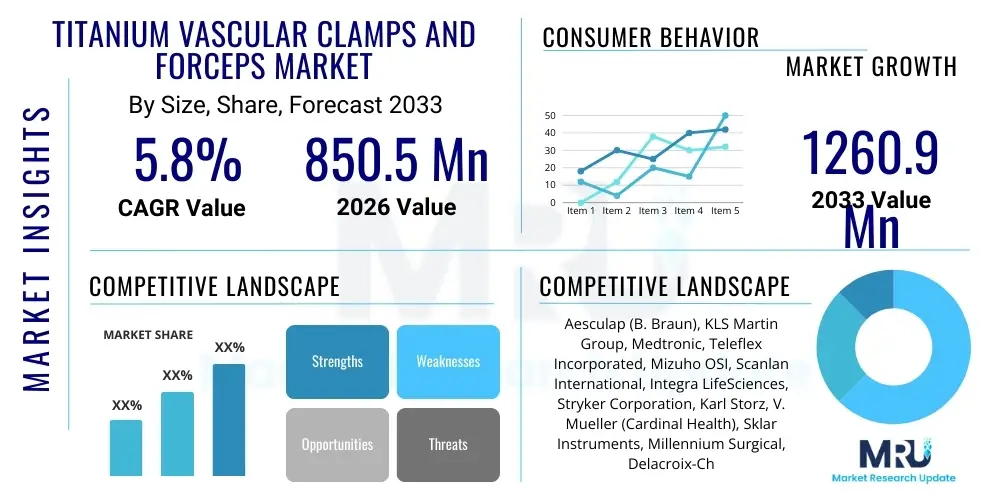

The Titanium Vascular Clamps and Forceps Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 850.5 Million in 2026 and is projected to reach USD 1260.9 Million by the end of the forecast period in 2033.

The Titanium Vascular Clamps and Forceps Market encompasses specialized surgical instruments used primarily in cardiovascular, neurosurgical, and general vascular procedures to temporarily occlude or manage blood flow in arteries and veins. These instruments, manufactured predominantly from high-grade medical titanium alloys, are critical tools utilized for achieving precise hemostasis and enabling surgeons to work in a relatively bloodless field during complex reconstructions or repairs. The inherent properties of titanium, including its high strength-to-weight ratio, excellent biocompatibility, and superior corrosion resistance compared to stainless steel, make it the preferred material, minimizing tissue reaction and ensuring longevity and repeated sterilization capability of the instruments.

Major applications for titanium vascular instruments span critical surgical domains, including Coronary Artery Bypass Grafting (CABG), aneurysm repair, carotid endarterectomy, and complex microvascular surgeries. The lightweight nature of titanium clamps and forceps significantly enhances surgical maneuverability, particularly beneficial in prolonged or intricate procedures requiring high precision, such as micro-neurosurgery. Furthermore, titanium instruments are generally non-magnetic, offering compatibility with Magnetic Resonance Imaging (MRI) technologies, which is a crucial advantage in post-operative imaging compared to certain ferrous material instruments.

Market growth is substantially driven by the global increase in age-related cardiovascular and neurological disorders, necessitating a higher volume of vascular surgeries. The continuous development of minimally invasive surgical techniques further fuels demand for highly specialized, smaller, and more ergonomic titanium instruments. Government initiatives aimed at improving healthcare infrastructure, coupled with technological advancements in surgical instrument manufacturing, including precision engineering and superior polishing techniques, are collectively acting as major catalysts propelling the expansion and adoption of titanium vascular clamps and forceps across global healthcare settings.

The Titanium Vascular Clamps and Forceps Market is characterized by robust growth, primarily anchored by increasing prevalence of chronic cardiovascular diseases and the global demographic shift toward an aging population. Business trends indicate a strong focus on innovation in instrument design, emphasizing ergonomic handling, improved clamping pressure distribution to minimize vessel trauma, and compatibility with robotic surgical systems. Leading manufacturers are intensely competing through product differentiation, strategic acquisitions, and expanding their distribution networks into high-growth emerging economies, especially in the Asia Pacific region, driven by expanding healthcare access and rising surgical volumes.

Regional trends highlight North America and Europe as dominant markets, primarily due to established healthcare infrastructure, high reimbursement rates for complex surgeries, and rapid adoption of advanced surgical technologies. However, the Asia Pacific region is poised for the fastest market growth, fueled by substantial investments in public and private hospitals, increasing disposable incomes, and the modernization of surgical facilities in countries such as China and India. Regulatory harmonization and standardization efforts across regions are streamlining market entry for new product variants, though stringent approval processes remain a critical barrier in developed economies.

Segmentation analysis reveals that reusable clamps and forceps currently hold a significant market share, preferred for their long-term cost-effectiveness in high-volume surgical centers, although the single-use segment is rapidly gaining traction due to growing concerns regarding cross-contamination and the efficiency benefits associated with eliminating sterilization cycles. By application, cardiovascular surgery remains the largest revenue generator, while neurosurgery is projected to exhibit the highest CAGR, reflective of increasing sophistication and frequency of cerebral vascular interventions. The market environment necessitates continuous material science optimization to ensure superior performance characteristics under clinical stress.

User queries regarding AI's influence on the Titanium Vascular Clamps and Forceps Market often center on automation potential, precision enhancement, and operational efficiency improvements in surgical settings. Key themes include whether AI can automate the clamping process, how AI-driven image guidance systems influence instrument selection and placement, and the role of machine learning in predicting optimal clamp force to prevent vessel injury. There is significant expectation that AI integration, particularly through robotic surgery platforms, will necessitate clamps and forceps with integrated sensors or highly standardized geometries suitable for robotic manipulation, thus driving a shift towards "smart" or AI-compatible instrumentation. Users are also concerned about the regulatory path for AI-assisted instruments and the necessary retraining required for surgical staff.

The market dynamics are governed by critical Drivers, Restraints, and Opportunities (DRO), which collectively form the Impact Forces shaping the industry's trajectory. Key drivers include the exponential increase in complex vascular procedures globally, supported by technological shifts toward lightweight and highly ergonomic titanium instruments, which are essential for prolonged surgeries. However, the market faces significant restraints, primarily stemming from the high initial cost associated with manufacturing and purchasing specialized titanium instruments, coupled with rigorous regulatory compliance requirements for medical devices. Opportunities reside predominantly in developing novel clamp designs that integrate features like atraumatic jaws and controlled pressure mechanisms, and expanding into rapidly developing healthcare markets where infrastructure investment is surging.

The Titanium Vascular Clamps and Forceps Market is comprehensively segmented based on product type, application, end-user, and geographic region, allowing for granular analysis of market trends and revenue streams. Segmentation by product type differentiates between permanent clamps (such as partial occlusion clamps and complete occlusion clamps) and temporary clamps, as well as classifying instruments based on reusability (single-use vs. reusable). The application segment highlights the dominance of cardiovascular and neurosurgical applications, given the critical nature and high volume of procedures requiring temporary vascular control. Analyzing these segments provides strategic insights into which areas of instrument design and distribution require focused investment to meet specific clinical demands and optimize market penetration.

The value chain for titanium vascular clamps and forceps begins with upstream analysis focusing on the sourcing of high-purity medical-grade titanium alloys (e.g., Ti-6Al-4V). Raw material procurement is crucial, as the quality and trace elements of the metal directly affect the biocompatibility, strength, and corrosion resistance of the final instrument. Key upstream suppliers are specialized metal producers who must meet stringent quality standards and regulatory certifications. Manufacturing involves complex processes such as forging, precision milling (CNC machining), surface treatment (e.g., polishing, passivation), and meticulous sterilization packaging, all requiring significant capital investment and highly skilled labor to meet the exacting tolerances demanded by micro-surgical applications.

The midstream component encompasses the core manufacturing processes where design innovation is paramount. Companies must continuously invest in research and development to refine ergonomic designs and introduce novel features, such as non-slip tips and specialized jaw geometries tailored for specific vessel sizes and types. Quality assurance and regulatory compliance (e.g., FDA, CE mark) form a substantial bottleneck and cost center within the midstream. Efficiency gains in this phase often rely on advanced manufacturing techniques like laser welding and sophisticated assembly lines to ensure repeatability and consistency across batches of delicate instruments.

Downstream distribution channels are diverse, involving both direct and indirect sales models. Direct sales are typically preferred for large hospital groups and government contracts, facilitating direct relationship management and custom training support. Indirect distribution, utilizing specialized medical device distributors and surgical supply houses, is essential for reaching smaller clinics and geographically dispersed markets. The choice of channel significantly impacts profit margins and market penetration speed. Furthermore, after-sales service, including instrument maintenance, repair, and efficient re-sterilization guidance, forms a vital component of the downstream value delivery, ensuring optimal instrument lifecycle management for healthcare providers.

The primary consumers of titanium vascular clamps and forceps are institutional healthcare providers that perform high-volume or highly specialized vascular, cardiac, and neurosurgical procedures. Hospitals, particularly those classified as tertiary or quaternary care centers, represent the largest segment of potential customers. These institutions require diverse inventories of both temporary and permanent occlusion clamps and various sizes of microvascular forceps to support their extensive surgical schedules, training programs, and specialized departments such as cardiac catheterization labs and neuro-intensive care units. Purchasing decisions are heavily influenced by clinical efficacy, instrument durability (measured by successful sterilization cycles), and total cost of ownership.

Ambulatory Surgical Centers (ASCs) constitute another rapidly growing segment of potential customers. As healthcare systems increasingly shift procedures from inpatient hospital settings to outpatient facilities to reduce costs, ASCs are expanding their capacity to handle moderately complex vascular procedures. ASCs often prioritize single-use (disposable) instruments for efficiency, lower infection risk, and avoidance of complex in-house sterilization processes, although reusable titanium instruments remain essential for specialized, high-cost procedures. Marketing strategies targeting ASCs often focus on supply chain simplicity and bundled pricing structures.

In addition to large institutions, specialized cardiovascular clinics, dedicated neurosurgical centers, and academic medical centers also serve as critical end-users. Academic centers are crucial for market adoption as they often lead in the evaluation and use of cutting-edge or prototype instruments, setting the standard for training future surgeons. Procurement staff and influential Key Opinion Leaders (KOLs) within these highly specialized facilities are key decision-makers, emphasizing instrument quality, material certification, and manufacturer reputation for reliability and innovation when selecting their portfolio of surgical instruments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 850.5 Million |

| Market Forecast in 2033 | USD 1260.9 Million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Aesculap (B. Braun), KLS Martin Group, Medtronic, Teleflex Incorporated, Mizuho OSI, Scanlan International, Integra LifeSciences, Stryker Corporation, Karl Storz, V. Mueller (Cardinal Health), Sklar Instruments, Millennium Surgical, Delacroix-Chevalier, ADM Surgical, Reda Instrumente, Wexler Surgical, GerMedUSA, Surtex Instruments, Microtek Medical, Lawton GmbH. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The manufacturing technology underpinning the titanium vascular instruments market is highly sophisticated, relying heavily on advanced computer numerical control (CNC) machining and micro-milling processes to achieve the exceptional precision required for handling delicate vascular tissue. Modern instrument production utilizes multi-axis CNC machines capable of shaping complex jaw patterns and articulation points with micron-level accuracy, ensuring atraumatic clamping action. Surface finishing technology is also paramount; techniques like electropolishing and chemical passivation are employed to enhance the instrument's corrosion resistance, reduce friction, and provide a perfectly smooth, non-reflective surface, which is crucial for minimizing glare in operating room lighting.

Additive Manufacturing (3D Printing) is emerging as a disruptive technology within the key technology landscape. While mass production of standard clamps still relies on traditional methods, 3D printing offers unparalleled benefits for creating customized or complex prototypes and instruments with internal geometries that are difficult to achieve via conventional milling. This allows for the development of patient-specific instruments or specialized tools tailored for unique anatomical challenges, improving surgical outcomes and efficiency. Furthermore, coating technologies, such as plasma vapor deposition (PVD) coatings, are being utilized to enhance the hardness and lubricity of critical contact surfaces without compromising the biocompatibility of the base titanium alloy.

A significant technological focus is placed on enhancing the ergonomic design and tactile feedback mechanisms of these instruments. Manufacturers are incorporating modular design principles and optimizing handle weight and balance to reduce surgeon fatigue during long procedures. The push toward minimally invasive and robotic surgery also mandates the development of elongated, slender titanium instrument shafts with robust joint mechanisms capable of transmitting precise force and movement over longer distances. This technological evolution requires advanced material testing and simulation tools to validate the instrument's performance and longevity under repeated stress and high-temperature sterilization cycles, securing the instrument's critical role in modern operating theaters.

Titanium is preferred due to its superior biocompatibility, lighter weight (reducing surgeon fatigue), non-ferromagnetic properties (MRI compatibility), and exceptional corrosion resistance, ensuring greater longevity and sterility compared to traditional stainless steel instruments.

Cardiovascular surgery, particularly procedures related to coronary artery bypass grafting (CABG) and complex aortic repairs, currently dominates the market share due to the necessity for precise, temporary blood flow control during these critical, high-volume operations.

The rising adoption of single-use instruments is primarily driven by heightened concerns over Hospital-Acquired Infections (HAIs), the elimination of complex in-house sterilization processes, and the increasing trend toward efficient, standardized procedural setups in Ambulatory Surgical Centers (ASCs).

Robotic surgery necessitates the development of specialized, elongated, and highly precise titanium instruments designed to interface seamlessly with robotic arms. This drives demand for high-end, technologically advanced titanium forceps and clamps optimized for remote manipulation and improved tactile feedback.

The Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR), fueled by significant investments in modernizing healthcare infrastructure, increasing surgical procedure volumes, and the expanding patient population base requiring vascular interventions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.