ID : MRU_ 436259 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

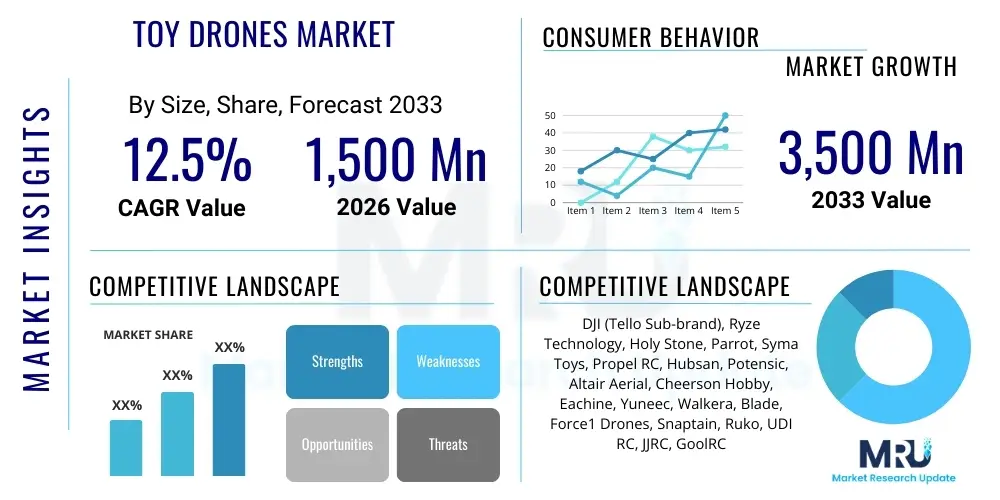

The Toy Drones Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at USD 1,500 Million in 2026 and is projected to reach USD 3,500 Million by the end of the forecast period in 2033.

The Toy Drones Market encompasses remotely operated, usually small-scale, unmanned aerial vehicles (UAVs) primarily designed for recreational use, entertainment, and educational purposes. These devices are generally characterized by user-friendly controls, affordability, and limitations in range and payload capacity compared to professional or commercial drones. The core product includes micro-drones, mini-drones, and standard recreational quadcopters, often equipped with basic cameras for first-person view (FPV) flying and stunt capabilities. Product development in this sector is heavily focused on enhancing battery longevity, improving stability through advanced gyroscopes, and integrating simpler programming features suitable for children and novice adults.

Major applications of toy drones revolve around personal entertainment, amateur aerial photography (especially for entry-level hobbyists), and STEM education initiatives, where drones are used to teach basic concepts of physics, coding, and engineering. The immediate benefit to the consumer is accessible high-tech recreation, offering an engaging introduction to aerial robotics without the high cost and complex regulatory hurdles associated with larger UAVs. Furthermore, improvements in collision avoidance systems and simplified calibration processes have made these products safer and more robust for indoor and crowded outdoor environments, significantly reducing the barrier to entry for new users.

Key driving factors propelling market growth include the decreasing cost of manufacturing sophisticated components, such as brushless motors and high-density batteries, making advanced features more accessible in the toy segment. The exponential rise in e-commerce platforms has provided global reach for specialized drone manufacturers, alongside widespread media coverage and the popularity of drone racing leagues, which continue to pique consumer interest in the technology. Rapid innovation in modular design also allows for easy repair and customization, extending the lifecycle and appeal of recreational drone models among enthusiasts.

The Toy Drones Market is characterized by intense price competition and rapid technological turnover, primarily driven by consumer demand for integrated camera features, extended flight times, and ease of use. Business trends indicate a strong move toward STEM-focused drones that incorporate basic coding interfaces (like block programming), transforming the product from a mere toy into an educational tool. Major manufacturers are consolidating supply chains in Asia Pacific regions to leverage low-cost manufacturing while focusing R&D on proprietary flight control algorithms that differentiate their products in crowded entry-level and mid-range segments. The market dynamics show that while the high-end segment of 'prosumer' drones is distinct, technological spillover continually introduces features like GPS stabilization and high-definition video capture into the affordable toy category, continually raising performance expectations.

Regionally, the Asia Pacific (APAC) currently dominates the market both in terms of consumption and production, fueled by a large youth population, increasing disposable incomes, and the presence of major manufacturing hubs in China and Taiwan. North America and Europe represent mature markets with high purchasing power, where the demand is skewed towards safer, regulatory-compliant drones, often purchased through organized retail channels. Emerging markets in Latin America and MEA are experiencing rapid adoption, though growth is sometimes tempered by infrastructure limitations and complex import regulations regarding radio frequency devices. The regional landscape is complex, requiring localized marketing strategies that address varying safety standards and consumer preferences regarding battery certification and altitude limits.

Segmentation analysis reveals that the quadcopter category remains the dominant drone type due to its stability and simple architecture, although micro-drones are rapidly gaining traction due to minimal regulatory scrutiny and suitability for indoor flying. In terms of technology, the Wi-Fi/Bluetooth control segment is expected to maintain leadership due to integration with existing smart devices, but dedicated radio frequency (RF) controllers are preferred by advanced hobbyists seeking greater range and lower latency. The primary consumer segment remains children and adolescents (8–16 years), but the adult hobbyist segment (seeking affordable FPV racing or flight practice platforms) is increasingly driving demand for higher performance and modular capabilities.

User inquiries regarding AI's influence on the Toy Drones Market frequently center on concerns about autonomy, collision avoidance sophistication, and the practical implementation of machine learning (ML) within cost-sensitive recreational platforms. Consumers commonly ask: "Will AI make toy drones fly themselves?", "Can inexpensive drones use complex obstacle avoidance like professional models?", and "How does AI enhance drone photography and videography for beginners?" The analysis reveals that key user themes revolve around enhanced user experience, safety improvements, and educational integration. Users expect AI to minimize crashes, stabilize flight under difficult conditions (e.g., wind), and simplify advanced maneuvers, thereby lowering the skill threshold required for enjoyable flying.

The core expectation is that AI integration will primarily focus on optimizing flight stability and safety features rather than full autonomy, given the recreational nature and price constraints of the segment. Specifically, AI algorithms are being applied to sensor fusion (combining data from accelerometers, gyroscopes, and potentially cheap computer vision modules) to achieve highly stable hovering and precise positioning, even in GPS-denied indoor environments. This integration provides a significant competitive edge, turning what was previously a difficult-to-control device into a stable aerial platform suitable for novice flyers, ensuring user satisfaction and reducing returns related to poor control performance. Furthermore, elementary AI is utilized in battery management systems to predict flight time more accurately and initiate automatic low-power landings.

Another critical area where AI is generating interest is in the enhancement of onboard camera features. While toy drones generally use basic optics, ML models can be implemented to offer simplified "follow me" modes, basic object tracking, or optimized flight paths for pre-programmed stunts, all managed through the user's smartphone interface. This democratization of advanced flight modes, once exclusive to high-end professional drones, is transforming the recreational segment by offering compelling, smart features at low price points. The educational segment benefits significantly, as AI features like programmed path finding provide tangible examples of robotics and computational decision-making for students, reinforcing the product's value proposition beyond simple play.

The market dynamics of toy drones are shaped by a complex interplay of Drivers, Restraints, and Opportunities, which collectively constitute the Impact Forces influencing industry trajectory. Key drivers center on technological accessibility and increasing consumer appetite for engaging, high-tech recreational products. The rapid decrease in component costs—especially for microprocessors, MEMS sensors, and camera modules—allows manufacturers to pack advanced features into affordable units, sustaining demand volume. Social media proliferation further acts as a powerful driver, showcasing user-generated content and creating aspiration for aerial capabilities among a broad consumer base. Simultaneously, the growing integration of drones into STEM curricula globally positions these products as essential educational tools, diversifying the market beyond mere entertainment.

However, the market faces significant Restraints, primarily stemming from stringent and evolving aviation regulations worldwide. Governments are increasingly concerned about airspace safety, leading to restrictions on altitude, proximity to airports, and registration requirements, even for smaller recreational drones. These regulatory complexities can often confuse consumers and discourage adoption, particularly for those unfamiliar with aviation laws. Furthermore, concerns regarding battery safety, particularly lithium polymer batteries used in these devices, pose a logistical and reputational risk, necessitating costly certifications and often impacting product design and shipping logistics. High product fragmentation and the resulting intense price wars, particularly among non-branded manufacturers, erode profit margins across the industry, acting as a financial restraint on sustained R&D investment.

The primary Opportunities lie in the expansion of FPV (First Person View) racing and freestyle flying, transforming toy drones into a viable e-sport and hobbyist platform that demands higher-performance, modular devices. The development of 'swarming' and collaborative drone play offers a novel, sophisticated gameplay experience that taps into the multi-user gaming market. Additionally, leveraging augmented reality (AR) integration allows users to overlay digital elements onto real-world drone flights viewed through a smartphone or headset, creating immersive new forms of interaction. The market can also capitalize on the demand for specialized educational drones that integrate advanced coding languages and robotics curriculum, creating a premium, recession-resistant segment focused on educational outcomes rather than pure recreational value. Navigating regulatory environments effectively by developing drones that inherently comply with regional weight and performance limits presents a crucial strategic opportunity for market leaders.

The Impact Forces are heavily weighted towards technological momentum and consumer acceptance. While regulation presents a persistent drag, innovation in battery technology (increasing flight time) and miniaturization (reducing weight below regulatory thresholds) are mitigating restraints. The competitive landscape is forcing innovation in user interface and durability, with manufacturers prioritizing modular components that are easily replaced, thereby improving the overall lifetime value proposition. The convergence of entertainment, education, and accessible technology ensures that the Toy Drones Market will continue its strong upward trajectory, provided key players successfully manage regulatory volatility and maintain aggressive pricing strategies necessary to attract the mass consumer market.

The Toy Drones Market is segmented across various dimensions, including Drone Type, Technology, Application, and End-User, each reflecting distinct consumer preferences and operational capabilities. This segmentation is crucial for manufacturers to target specific demographic niches effectively, moving beyond generic offerings to specialized products such as micro-drones designed for indoor use or larger recreational drones equipped for beginner aerial photography. Understanding these segments helps in optimizing distribution strategies, focusing on channels like hobby stores for performance models and mass retail for entry-level devices, ensuring maximal market penetration and competitive positioning.

The Type segmentation (quadcopter, hexacopter, multi-rotor) highlights the dominance of the four-rotor design due to its stability, manufacturing simplicity, and ease of control, which is paramount in the toy category. However, the rapidly growing micro-drone sub-segment (under 100 grams) is crucial because these devices often fall outside the stricter regulatory scope, making them highly appealing for unrestricted indoor and small-space recreational flying. Technology segmentation, primarily between Wi-Fi/Bluetooth control and dedicated RF controllers, reflects the trade-off between convenience (using a smartphone) and performance (using an RF remote), where serious hobbyists invariably opt for the lower latency of RF systems, while casual users prefer seamless smart device integration.

From an End-User perspective, the market divides into the dominant Children/Adolescent segment, driven by novelty and gift purchases, and the expanding Adult Hobbyist segment, characterized by higher disposable income and a demand for more sophisticated features like advanced FPV cameras, modular frames, and compatibility with aftermarket components. This latter segment is key for sustaining higher average selling prices (ASPs). The Application segmentation (Entertainment vs. Education) underscores the dual utility of toy drones, guiding marketing efforts to either emphasize pure fun and stunts or highlight the product’s capability as a teaching aid in STEM fields, particularly appealing to parents and educational institutions.

The Value Chain for the Toy Drones Market begins with Upstream activities centered on the procurement and design of highly specialized electronic components, flight control systems, and structural materials. Key upstream suppliers include manufacturers of high-efficiency brushless DC motors, MEMS sensors (gyroscopes and accelerometers), lightweight plastics and composites (like ABS or polycarbonate), and rechargeable lithium polymer batteries. Crucially, the firmware and flight control software, often proprietary, represent significant intellectual property in the upstream phase. Manufacturers must maintain robust relationships with ASIC and microcontroller suppliers to ensure cost control and consistency in performance, as slight variations in sensor quality directly impact the stability and usability of the final product, a critical factor for customer retention in the toy segment.

Midstream activities involve the highly integrated assembly and manufacturing process, predominantly located in Asia Pacific (China). These activities include circuit board assembly, precision molding of drone frames, component integration, calibration, and rigorous quality control testing (especially for flight stability and battery performance). Direct sales channels are characterized by manufacturers selling directly through their own e-commerce portals, offering customization and direct customer support, which allows for higher margins and quicker feedback loops. Indirect distribution is dominated by partnerships with large global retailers (e.g., Walmart, Amazon, Target) and specialized distributors who manage logistics, inventory, and localized retail placement. The sheer volume required by the mass market necessitates a heavy reliance on indirect channels for reach.

Downstream analysis focuses on reaching the end consumer. The distribution channels are highly diversified, ranging from brick-and-mortar specialty toy and hobby stores (important for FPV and high-end models where advice is needed) to vast online marketplaces which account for the majority of entry-level and mid-range sales volumes. Marketing focuses heavily on video demonstrations and user-generated content to showcase flight capabilities and stunts. After-sales service, including easily accessible replacement parts (propellers, batteries, guards) and comprehensive repair guides, is a crucial downstream activity that enhances brand loyalty and mitigates consumer frustration associated with common crashes and wear-and-tear in this product category.

Potential customers for the Toy Drones Market are highly diverse, spanning various age groups and motivations, but are generally unified by a desire for accessible, engaging, and technologically advanced recreation. The largest and most volatile segment includes parents purchasing drones as gifts for Children and Adolescents (typically 8 to 16 years old). This segment demands robust, easy-to-fly, and low-cost devices that emphasize simple control interfaces and brightly colored designs. Purchasing decisions here are heavily influenced by safety certifications, battery life, and durability to withstand frequent minor crashes, with price point being a primary constraint given the perception of drones as disposable toys.

A rapidly expanding customer base consists of Adult Hobbyists and Tech Enthusiasts. These buyers seek drones for purposes beyond simple play, including learning the basics of FPV racing, practicing aerial maneuvers, or utilizing the drone as a low-cost platform for entry-level programming and customization. This segment values modularity, low-latency control, advanced firmware features, and compatibility with standard hobby components (e.g., specific FPV goggles or radios). Although they are less price-sensitive than the children's segment, they demand a higher performance-to-cost ratio and superior build quality, driving the growth of the $150-$300 segment of 'prosumer lite' drones.

Furthermore, Educational Institutions, including K-12 schools, universities running engineering outreach programs, and private STEM academies, represent a stable and growing B2B customer base. These buyers purchase drones in bulk as tools for teaching robotics, coding, and basic aerospace principles. They require supporting curriculum materials, robust fleet management features, and often favor proprietary programming interfaces. These customers prioritize long-term durability and the availability of educational support resources over pure recreational features, making them a premium segment focused on functionality and pedagogical value.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1,500 Million |

| Market Forecast in 2033 | USD 3,500 Million |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | DJI (Tello Sub-brand), Ryze Technology, Holy Stone, Parrot, Syma Toys, Propel RC, Hubsan, Potensic, Altair Aerial, Cheerson Hobby, Eachine, Yuneec, Walkera, Blade, Force1 Drones, Snaptain, Ruko, UDI RC, JJRC, GoolRC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Toy Drones Market is defined by the rapid migration of sophisticated flight control and sensor technologies from high-end commercial UAVs into affordable recreational models, often at a significantly reduced cost and size. A core technological area is miniaturization of Micro-Electro-Mechanical Systems (MEMS), including six-axis gyroscopes and accelerometers, which are crucial for maintaining the stable flight performance that novice users require. These small, low-power sensors, coupled with powerful yet inexpensive microcontrollers (MCUs), execute complex PID (Proportional-Integral-Derivative) control loops thousands of times per second to ensure stable hovering and predictable maneuverability. The performance of these systems is the primary differentiator in the highly competitive mid-range toy drone market, affecting user perception of quality and ease of use.

Another pivotal technology is the advancement in battery technology, particularly the shift toward higher-energy density Lithium Polymer (LiPo) cells, which directly addresses the major user complaint of short flight times. Manufacturers are continually innovating battery form factors and management systems to maximize flight duration while adhering to strict safety standards (reducing the risk of thermal runaway). Furthermore, the implementation of 5.8 GHz radio frequency (RF) transmission is becoming standard for FPV (First Person View) models, offering significantly lower latency compared to Wi-Fi, which is essential for drone racing and highly responsive control. This distinction in transmission technology effectively bifurcates the market into casual Wi-Fi-controlled devices and performance-oriented RF-controlled systems, catering to different user demands.

Finally, the growing adoption of simplified computer vision and AI-assisted flight features, even if rudimentary, is transforming the entry-level segment. Basic downward-facing optical flow sensors (OFS) allow drones to maintain altitude and position accurately indoors or when GPS signals are unavailable, providing essential stability. As component prices drop, basic obstacle avoidance using infrared or ultrasonic sensors is increasingly integrated, enhancing safety and durability. For the educational segment, open-source flight controllers and simplified coding platforms like Scratch or Python interfaces are becoming commonplace, enabling students to modify flight behavior and learn programming fundamentals directly through the drone platform, underscoring the technology’s dual role in recreation and learning.

The global distribution and consumption of toy drones show distinct regional patterns influenced by local economic conditions, regulatory frameworks, and cultural adoption of technology. Asia Pacific (APAC) dominates the global market, both in terms of manufacturing output and consumer demand. China serves as the undisputed global hub for drone production, leveraging its sophisticated supply chain and massive industrial scale to offer the lowest cost-per-unit, attracting major global brands. Consumer demand within countries like China, India, and South Korea is soaring, driven by a youthful population base, rising middle-class disposable incomes, and early adoption of consumer electronics, resulting in APAC holding the largest market share by volume and value.

North America (NA), primarily the United States and Canada, represents a high-value market characterized by consumers demanding high quality, enhanced safety features, and specific compliance with stringent FAA regulations, particularly regarding the sub-250g classification. The North American market has a robust segment of adult hobbyists focused on FPV racing and advanced recreational flying. Purchases are heavily influenced by strong brand reputation and readily available customer support. Although overall volume might be lower than APAC, the average selling price (ASP) is typically higher due to preference for features like GPS return-to-home functionality and integrated HD cameras, sustaining significant revenue streams for market players.

Europe mirrors North America in its focus on safety and regulatory compliance, mandated by EASA rules, which heavily influences product design, especially regarding flight zones and licensing requirements. Western European countries exhibit high demand for STEM education-focused drones, driven by governmental emphasis on digital literacy and technical skills acquisition. The market is competitive, with a mix of global brands and strong localized distributors. Latin America and the Middle East & Africa (MEA) are emerging as high-growth regions. Although hampered by infrastructure challenges and economic volatility, increasing internet penetration and rising urbanization are steadily boosting demand for consumer electronics, presenting long-term opportunities for manufacturers willing to navigate complex local customs and import taxes. South Africa, Brazil, and the UAE are key entry points within these emerging markets.

The primary driver is the rapid decrease in component costs (sensors, motors, processors), which allows manufacturers to integrate advanced features like cameras, GPS, and superior flight stabilization into highly affordable recreational models, making high-tech flying accessible to mass consumers globally.

In many regions (e.g., US, EU), toy drones weighing under a specific threshold (often 250 grams) are exempt from complex registration requirements, making them more attractive to casual users. However, all drones, regardless of weight, must adhere to rules regarding restricted airspace and visual line of sight.

Battery life is critical; consumers prioritize flight time, with anything less than 8–10 minutes often being a deterrent. Advancements in higher energy density Lithium Polymer (LiPo) batteries and intelligent power management systems are key technological differentiators that influence purchasing choices and perceived value.

The Asia Pacific (APAC) region currently holds the largest market share, driven by its dominance in manufacturing (China) and immense consumer demand stemming from increasing disposable incomes and a large youth population highly engaged with consumer electronics.

The educational segment (STEM learning) is a critical growth opportunity, transforming drones into educational tools for teaching coding, engineering, and physics. This segment drives demand for specialized, programmable, and durable drone kits, offering a stable revenue stream beyond seasonal recreational sales.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.