ID : MRU_ 435083 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

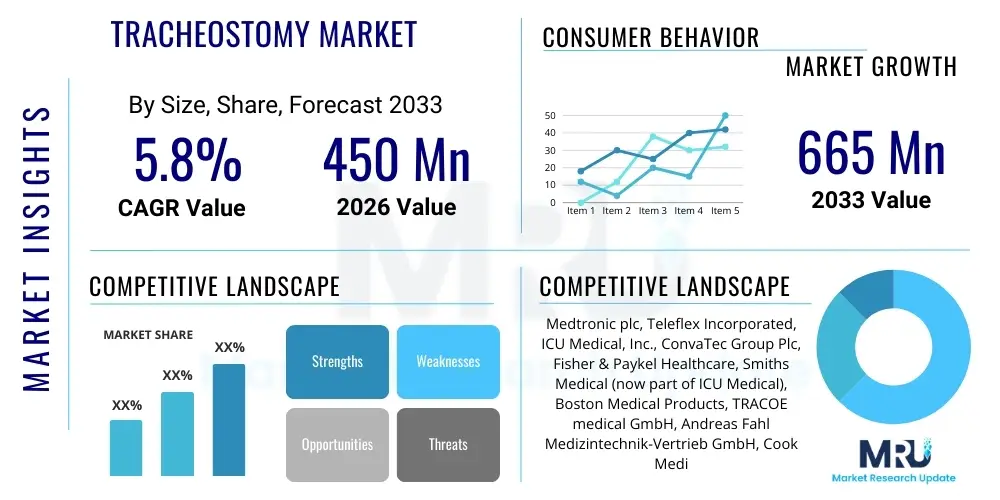

The Tracheostomy Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 665 Million by the end of the forecast period in 2033. This consistent and robust growth trajectory is fundamentally supported by the increasing global prevalence of non-communicable diseases, especially those leading to chronic respiratory failure and the necessity for prolonged mechanical support. Market valuation is steadily appreciating due to the integration of premium features into essential devices, such as anti-microbial coatings and advanced cuff technologies, which command higher price points while delivering verifiable clinical benefits in acute care settings. The market size reflects not only the volume of procedures but also the expanding revenue derived from the accessories segment, including speaking valves and specialized HMEs, critical for long-term patient rehabilitation and management.

The expansion is strategically influenced by geopolitical and economic factors, particularly the acceleration of healthcare infrastructure development across major emerging economies where the critical care sector is rapidly maturing. Furthermore, established markets maintain high revenue contribution through continuous replacement cycles and the preference for single-use, specialized kits, which reduces the complexity and risk of reprocessing. Successful penetration into the home healthcare market also contributes significantly to the overall market size projection, as providers transition care outside the hospital walls, creating reliable demand for durable and patient-friendly chronic care products. Stakeholders view this market as highly stable, given the non-elective nature of the procedure, ensuring that investment in production capacity and innovation remains attractive across the entire forecast horizon. This sustained demand profile ensures the market avoids sharp contractions, maintaining steady growth despite potential cost-containment measures in governmental procurement.

The Tracheostomy Market constitutes a critical segment of the medical device industry, dedicated to airway management and comprising all equipment necessary for the creation, maintenance, and closure of a tracheal stoma. Product offerings are highly diversified, catering to both emergency and planned settings, and include advanced cuffed tubes essential for mechanical ventilation, sophisticated uncuffed tubes suitable for ambulatory patients, and comprehensive kits designed for rapid, bedside percutaneous insertion. The inherent value of these devices lies in their capacity to bypass upper airway obstructions, facilitate the removal of pulmonary secretions, and minimize the risk of laryngeal and tracheal injury associated with prolonged endotracheal intubation, which is crucial for maximizing patient comfort and improving long-term outcomes.

The clinical spectrum of application for tracheostomy devices is vast, covering patients in Intensive Care Units battling severe conditions such as Acute Respiratory Distress Syndrome (ARDS) or major trauma, individuals with degenerative neuromuscular diseases (e.g., ALS), and post-surgical patients in otolaryngology. A significant benefit driving adoption is the ability of tracheostomy to enhance patient mobility and facilitate the initiation of oral feeding and speech therapy much sooner than traditional ventilation methods allow. This holistic approach to patient recovery underscores the shift in market focus from simply sustaining life to actively improving the patient’s quality of life during the recovery and rehabilitation phase, influencing device design toward materials and features that maximize user interaction and comfort.

Key market drivers are inextricably linked to demographic trends, specifically the increasing life expectancy leading to a greater number of individuals requiring long-term respiratory support due to age-related illnesses. Furthermore, the global successful clinical adoption of the Percutaneous Dilatational Tracheostomy (PDT) technique is accelerating market growth by making the procedure safer, faster, and more accessible across various healthcare settings. The market dynamics are further bolstered by rising public awareness and increased healthcare spending in emerging economies, facilitating the integration of these advanced airway management devices into local critical care protocols, thereby ensuring sustained compounded growth and continuous product development focused on infection reduction and ease of long-term patient use.

The Tracheostomy Market is characterized by intense competition and a continuous drive toward clinical safety and user-centric design. Business trends reveal a clear strategic prioritization of innovation in infection control, leading to high investment in devices utilizing silver coatings or proprietary anti-microbial plastics to combat healthcare-associated infections like VAP. Consolidation activities remain paramount, allowing key players like Medtronic and Teleflex to leverage economies of scale and offer integrated ventilation and airway management solutions, reinforcing their global market leadership. Furthermore, the demand for disposables and single-use components continues to rise, driven by heightened infection control protocols and labor efficiency requirements in acute care settings.

Regional analysis underscores the dual dominance of North America and Europe, which together account for the majority of the market value, primarily purchasing high-end devices supported by sophisticated reimbursement structures. However, the future growth epicenter lies in the Asia Pacific region, where massive population size, increasing modernization of critical care infrastructure, and rising incidence of non-communicable respiratory diseases are creating an unprecedented demand surge. Companies are adapting their product lines and pricing strategies to address the heterogeneous needs of these regions, balancing the requirement for advanced features in Western markets with the imperative for cost-effectiveness and volume supply in Asian markets.

Segmentation insights emphasize the increasing importance of patient rehabilitation segments. While tracheostomy tubes remain the core revenue driver, the accessory segment, including advanced speaking valves and cuff pressure monitors, is witnessing exponential growth as hospitals adopt best practices focused on earlier speech and swallowing rehabilitation. The ongoing shift toward the percutaneous procedure model continues to drive robust demand for all-in-one procedural kits, minimizing variation and enhancing safety during emergency insertions. This summary highlights a market successfully balancing acute life-saving functionality with the evolving requirements for enhanced patient quality of life, steering product development toward minimally invasive and chronic care optimized solutions.

User analysis consistently reveals profound interest in how Artificial Intelligence (AI) can transcend conventional limitations in managing patients requiring long-term tracheostomy. The most recurring queries surround AI’s ability to standardize and objectify the highly complex clinical decision-making involved in decannulation readiness, which currently relies heavily on clinician experience and variable protocols. Users seek verified AI models that can process continuous physiological data streams—such as respiratory mechanics, airway resistance, and secretions output—to generate a Decannulation Readiness Score (DRS), ensuring that the withdrawal of the life-support device is done at the absolute safest and most optimal moment, preventing clinical deterioration and the traumatic need for re-intubation or re-tracheostomy. This shift is crucial for maximizing patient throughput and improving institutional efficiency metrics.

Furthermore, critical care personnel frequently inquire about AI-enhanced monitoring systems designed specifically for detecting the subtle, early indicators of life-threatening complications, particularly tube occlusion and accidental decannulation, which require immediate intervention. Traditional alarms often generate high rates of false positives, leading to alarm fatigue. AI is expected to filter this noise by recognizing genuine crisis patterns with high specificity and sensitivity, reducing nursing workload and focusing immediate attention where it is critically needed. This integration of 'smart' surveillance technology is anticipated to become a non-negotiable feature in premium tracheostomy management systems, driving innovation in sensor technology embedded within the tubes or their holders, directly enhancing critical care quality and safety compliance metrics across hospitals.

Beyond immediate patient care, common user themes address AI's role in optimizing resource management and training efficiency. Machine learning algorithms are increasingly seen as pivotal for predicting the necessary inventory of specialized tracheostomy equipment based on historical usage and predictive modeling of local disease outbreaks or seasonal peaks in respiratory illnesses, optimizing hospital purchasing decisions and minimizing critical shortages. In the realm of education, the integration of AI into sophisticated virtual reality simulators promises to offer personalized, adaptive procedural training for percutaneous tracheostomy insertion, providing objective performance feedback to trainees and accelerating the development of highly skilled critical care teams capable of performing this delicate procedure with minimal error.

The Tracheostomy Market operates under strong positive drivers that propel its expansion, predominantly the overwhelming global increase in non-communicable respiratory diseases such as COPD, asthma, and lung cancer, which require complex airway management intervention. This driver is powerfully reinforced by global medical advances that have significantly improved survival rates for critically ill patients, necessitating long-term ventilator support often facilitated by a tracheostomy. Furthermore, the economic advantage offered by the shift from prolonged, damaging endotracheal intubation to earlier tracheostomy placement (particularly PDT), which enables earlier patient mobilization, feeding, and transfer out of the most expensive acute care beds, provides a compelling economic driver for hospitals seeking cost efficiencies.

Notwithstanding the strong market drivers, significant restraints temper the potential growth rate. These include the specialized expertise and high skill set required for the initial tracheostomy procedure and, critically, for the continuous post-operative monitoring and care, which results in a persistent shortage of adequately trained healthcare professionals globally. Furthermore, the substantial clinical risks associated with complications, such as accidental decannulation, aspiration pneumonia, and infection at the stoma site, necessitate intensive resource allocation and continuous patient surveillance, increasing the overall cost of care and posing a liability challenge to providers. These procedural risks heighten the preference for advanced, costly safety devices, creating a financial barrier in resource-limited settings.

Opportunities for profound market acceleration stem from technological breakthroughs focusing on non-invasive monitoring and enhanced patient rehabilitation. The development and widespread adoption of innovative accessories, particularly HMEs with superior filtration and moisture capabilities, and speaking valves designed for maximal clarity, are driving new market demand by improving patient quality of life metrics. The rapid expansion and professionalization of the home healthcare sector present a major opportunity for manufacturers to create durable, highly simplified, and intuitive tracheostomy management systems and accompanying telemonitoring solutions, tapping into a large, currently underserved patient population transitioning from hospital to home care settings globally.

The core Impact Forces shaping the market environment include the increasing standardization imposed by international quality organizations and government regulators, compelling manufacturers to adhere to the highest levels of device biocompatibility and sterility assurance. Secondly, the powerful force of Value-Based Healthcare models dictates purchasing decisions, forcing manufacturers to generate robust clinical data proving their devices reduce VAP rates or shorten hospital stays, thereby justifying premium pricing through demonstrable economic benefits. Lastly, the rapid global dissemination of best-practice guidelines and evidence-based medicine encourages uniform adoption of superior products like subglottic suctioning tubes, acting as a powerful global equalizer in clinical practice standards and driving market demand toward quality and innovation.

Segmentation analysis of the Tracheostomy Market provides a critical framework for understanding demand drivers, competitive dynamics, and future growth areas across distinct product categories, procedural preferences, and end-user environments. The foundational segmentation by Product Type, encompassing Tubes, Kits, and Accessories, reveals differential growth rates; while tubes are the core revenue generators, accessories like speaking valves and HMEs show rapid expansion, reflecting increased clinical emphasis on patient rehabilitation and chronic care quality. The distinction between various tube types—cuffed, uncuffed, and fenestrated—is essential for accurate forecasting, as cuffed tubes align with acute ICU usage, whereas the others dominate long-term care and home settings.

The segmentation by Procedure Type—Open Surgical versus Percutaneous Dilatational Tracheostomy (PDT)—highlights a pivotal trend: the significant global migration toward PDT. PDT kits, being comprehensive and designed for bedside insertion, are replacing open surgery in many critical care scenarios, driving demand for specialized guidewires, dilators, and introducers. This procedural preference change has direct implications for manufacturing and distribution, favoring companies that offer highly integrated and standardized PDT systems. Simultaneously, End-User segmentation provides insight into consumption patterns; hospitals and ICUs remain the primary high-volume purchasers, dictated by acute need, while the accelerating growth in the Home Care sector necessitates products designed for ease of maintenance, durability, and simplified operation by non-professional caregivers.

Further segmentation by Material, mainly PVC and Silicone, helps explain cost variations and durability profiles. While PVC tubes offer cost-effectiveness and good rigidity for insertion, the increasing use of medical-grade silicone reflects a premium segment dedicated to maximizing patient comfort and reducing the risk of mucosal injury during prolonged placement. A meticulous review of these segments allows market participants to refine their competitive strategies, focusing on underserved niches such as pediatric devices or developing integrated smart accessories that utilize advanced materials, thereby capitalizing on both volume-driven and value-driven market opportunities across different global health economies and regulatory compliance requirements.

The value chain in the Tracheostomy Market is characterized by highly specialized production processes and stringent regulatory compliance, beginning with the Upstream analysis which centers on sourcing biocompatible, high-quality raw materials. Manufacturers must secure reliable supplies of materials such as phthalate-free PVC, medical-grade silicone elastomers, and high-tensile plastics for tube construction, ensuring they meet ISO standards and often proprietary specifications for flexibility and non-toxicity. This phase also includes the design and engineering of complex components, such as low-pressure cuffs and integrated subglottic suction lumens, necessitating continuous collaboration with material science experts. Efficiency in this stage dictates the final product quality and manufacturing cost, with supply resilience being paramount given the life-critical nature of the final product.

Midstream activities encompass the precise manufacturing, assembly, sterilization, and packaging of the devices. Investment in automated molding and assembly lines is crucial for high-volume production, especially for commodity items like standard cuffed tubes. However, specialized products, such as customized fenestrated tubes or speaking valves, require more intricate manual assembly and rigorous quality control checks. Distribution channels are bifurcated into Direct and Indirect models. Major global players often utilize direct sales forces and established relationships for large volume tenders with governmental health systems and major integrated delivery networks (IDNs). Indirect channels rely on specialized third-party medical distributors, leveraging their regional warehousing capabilities and strong existing contacts with smaller regional hospitals, ambulatory centers, and the expanding network of home healthcare suppliers, thereby optimizing last-mile delivery and inventory levels.

Downstream analysis focuses on the interaction between the devices and the end-users. Key downstream activities include comprehensive clinical education and technical training provided by manufacturers to physicians and nurses, ensuring the safe and appropriate use of PDT kits and specialty accessories. The purchasing decisions at this level are influenced heavily by Clinical Value Assessment (CVA) committees, which weigh factors like complication reduction (VAP rates), ease of use, and overall cost savings from reduced length of stay. The final critical element is the post-market surveillance and continuous feedback loop, which allows manufacturers to rapidly iterate on design flaws or adverse event reports, maintaining regulatory compliance and enhancing the product’s clinical utility and safety profile in real-world settings, which is essential for sustained market acceptance and positive reimbursement outcomes.

The primary customer base for the Tracheostomy Market comprises institutions dedicated to acute and critical care, most notably Hospital Intensive Care Units (ICUs), including surgical, medical, cardiac, and trauma ICUs. These settings are the largest purchasers of immediate insertion systems, primarily specialized Percutaneous Tracheostomy Kits and high-volume Cuffed Tubes, used for stabilizing patients with acute respiratory failure, post-trauma injuries, and prolonged ventilator dependence. Procurement decisions in hospitals are highly centralized and influenced by clinical effectiveness data, evidence of reduced infection rates (like VAP), and bulk purchasing efficiencies. The focus of these buyers is on reliability, sterility assurance, and compatibility with existing ventilation equipment, ensuring smooth integration into complex critical care workflows that operate under immense time pressure.

A secondary, yet rapidly ascending, customer segment includes Long-Term Acute Care Hospitals (LTACHs), specialized rehabilitation facilities, and integrated Home Healthcare agencies. As patients stabilize and transition from acute care, the demand shifts towards products optimized for chronic management and rehabilitation, such as uncuffed tubes, speaking valves, and high-performance HMEs. LTACHs and rehab centers purchase devices intended to promote patient mobility, speech capability, and facilitate the ultimate goal of decannulation. Home care agencies, often acting as intermediaries, purchase devices directly related to patient comfort, ease of cleaning, and durability, catering to the non-professional caregiver environment. This segment’s growth is driven by healthcare economics focused on reducing expensive acute care days.

Additionally, Ambulatory Surgical Centers (ASCs) and specialty clinics, particularly those specializing in otolaryngology and pulmonology, represent niche but growing customers, often performing elective or planned tracheostomies under controlled conditions. These customers value efficiency and specialized, smaller-gauge tubes for specific non-emergency cases. Finally, academic medical centers and specialized training institutes constitute a vital segment, purchasing advanced simulation equipment and demonstration devices necessary for training the next generation of critical care specialists and respiratory therapists, thereby influencing future adoption patterns and procedural standardization across the broader clinical community.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 665 Million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic plc, Teleflex Incorporated, ICU Medical, Inc., ConvaTec Group Plc, Fisher & Paykel Healthcare, Smiths Medical (now part of ICU Medical), Boston Medical Products, TRACOE medical GmbH, Andreas Fahl Medizintechnik-Vertrieb GmbH, Cook Medical, Well Lead Medical Co., Ltd., Troge Medical GmbH, Fuji Systems Corporation, Marpac Inc., Pulmodyne, Inc., PFM Medical AG, Stening S.A., DLG Medical Ltd., Jotech Biomedical Inc., Shiley, Kapitex Healthcare, Inc., Biesse S.r.l., Rusch, Vygon S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Tracheostomy Market's technological advancements are critically focused on iterative improvements in material science and procedural innovation to minimize morbidity and optimize patient quality of life. The shift from traditional open surgical methods to the widespread acceptance of Percutaneous Dilatational Tracheostomy (PDT) represents the most significant procedural shift. Modern PDT kits utilize advanced dilator systems, often featuring hydrophilic coatings and integrated safety mechanisms, coupled with high-resolution fiberoptic bronchoscopes for precise, real-time visualization. This technology minimizes tracheal trauma, shortens procedural time, and crucially, allows the procedure to be performed safely at the patient's bedside in the ICU, dramatically reducing the risks and costs associated with transporting critically ill patients to the operating theater.

In terms of device technology, innovation centers on developing tubes that actively mitigate the two most common complications: Ventilator-Associated Pneumonia (VAP) and tracheal wall damage. This has resulted in the prevalence of specialized tubes incorporating dedicated subglottic suction lumens, which ensure continuous removal of secretions pooling above the cuff. Additionally, manufacturers are leveraging advanced polymer chemistry to create low-pressure, high-volume cuffs that distribute pressure more evenly across the tracheal mucosa, alongside using softer, flexible silicone and polyurethane materials for the tube shaft. These material science improvements are essential for reducing the risk of tissue necrosis and granulation tissue formation, particularly for patients requiring long-term placement, directly improving clinical safety metrics.

Furthermore, the digital integration of care is rapidly gaining prominence. The development of smart tracheostomy accessories, such as electronic cuff pressure monitors and wireless sensor-enabled holders, provides continuous, objective data on critical parameters. These digital tools are essential for maintaining the ideal cuff pressure—a narrow window between preventing leaks and causing mucosal injury—and for immediate alerting in case of accidental displacement, which is a life-threatening event. Future technological research is also focusing on bioabsorbable materials for temporary stoma reinforcement and advanced manufacturing techniques like 3D printing, enabling the production of highly customized, patient-specific tracheostomy solutions for complex airway anatomies, pushing the boundaries of personalized respiratory care management.

The Tracheostomy Market exhibits distinctive regional dynamics influenced by variations in healthcare policy, disease prevalence, critical care infrastructure, and economic development. North America, anchored by the United States, holds the dominant revenue share, primarily due to exceptionally high per capita healthcare spending, widespread clinical adoption of advanced, high-cost devices (such as VAP-reducing tubes and specialized kits), and a high burden of chronic, complex conditions like advanced COPD and cardiovascular diseases, necessitating prolonged mechanical ventilation. The region benefits from established reimbursement frameworks that support expensive critical care procedures and a competitive landscape that encourages continuous high-level innovation and early adoption of new technologies, particularly in the private hospital sector and major academic medical centers.

Europe represents a mature market with high demand, governed by stringent European Medical Device Regulation (MDR) standards, ensuring high product quality and safety profiles. Key contributions to market size come from Western European nations (Germany, UK, France), driven by sophisticated public healthcare systems, a high prevalence of aging-related respiratory illnesses, and a strong emphasis on post-acute care and rehabilitation. The European market distinguishes itself through substantial investments in home healthcare infrastructure, creating specific demand for durable, easy-to-use tracheostomy equipment and accessories designed for long-term patient management outside the intensive care environment, contrasting slightly with the acute focus often seen in the US market.

The Asia Pacific (APAC) region is forecasted to achieve the highest Compound Annual Growth Rate (CAGR) globally. This explosive growth is attributed to rapid economic development leading to increased per capita healthcare expenditure, governmental initiatives to improve public health infrastructure (especially in countries like China, India, and South Korea), and a vast, increasingly aware population base. While price sensitivity historically favored basic products, there is a clear and accelerating trend toward adopting internationally standardized, advanced tracheostomy devices and kits, driven by the modernization of large hospital networks and the increasing clinical training in minimally invasive PDT techniques across major urban centers, making it the most pivotal region for future market expansion.

The Tracheostomy Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. This consistent growth is primarily driven by the rising global incidence of chronic respiratory diseases, the demographic shift towards an older population, and continuous improvements in critical care survival rates globally.

The Percutaneous Dilatational Tracheostomy (PDT) procedure is experiencing the fastest adoption rate. PDT is widely preferred over traditional surgical methods due to its minimally invasive nature, the ability to be performed efficiently at the patient's bedside in the ICU, and its association with reduced recovery times and overall lower complication risks.

The rapidly aging global population is a core market driver. Older individuals are statistically more prone to chronic obstructive pulmonary disease (COPD), severe neurological deficits, and trauma requiring long-term airway management, thereby generating sustained, high-volume demand for specialized tracheostomy tubes and necessary accessories.

Technological advancements are focused on critical patient safety improvements, notably the development of tubes with integrated subglottic suction lumens to actively mitigate Ventilator-Associated Pneumonia (VAP) and the implementation of smart monitoring systems to prevent accidental decannulation and maintain optimal cuff pressure.

The Asia Pacific (APAC) region is anticipated to exhibit the highest CAGR. This accelerated growth is primarily attributed to rapidly expanding critical care capacity, significant government investment in modern healthcare infrastructure, and rising adoption of advanced respiratory care protocols across densely populated countries like China and India.

Fenestrated tubes contain small openings that allow air to pass up through the vocal cords when the cuff is deflated. Their primary benefit is enabling the patient to speak and cough more effectively, assisting in the crucial psychological and physical rehabilitation process toward ultimate decannulation.

Manufacturers are addressing the shift to home care by developing durable, user-friendly, and lightweight tracheostomy accessories, such as simplified tube holders and easy-to-clean inner cannulas, alongside comprehensive educational resources specifically designed for effective use by non-professional, lay caregivers.

PVC tubes are generally cost-effective and rigid, often used for short-term and acute care. Silicone tubes, conversely, are premium products offering superior flexibility and softness, minimizing mucosal irritation and making them the preferred choice for long-term placement and chronic management due to enhanced patient comfort.

Clinical education is critical because the specialized nature of tracheostomy insertion and care requires high precision. Manufacturers providing thorough training to clinicians and nurses ensure safe usage, minimize procedural complications, and maximize the efficacy of advanced devices, directly influencing clinical adoption and patient outcomes.

Stringent regulatory scrutiny, particularly under standards like the MDR in Europe, compels manufacturers to allocate significant R&D investment towards generating robust clinical evidence and high-quality data to substantiate safety and performance claims, increasing the cost and duration of product development cycles.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.