ID : MRU_ 435098 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

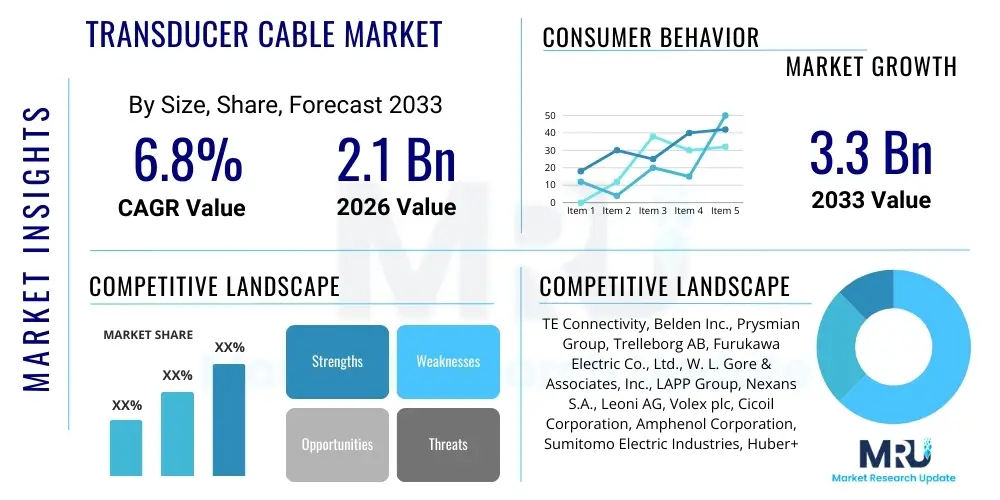

The Transducer Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $2.1 Billion in 2026 and is projected to reach $3.3 Billion by the end of the forecast period in 2033.

The Transducer Cable Market encompasses highly specialized electrical cables designed to reliably transmit low-level analog or digital signals generated by a transducer—a device converting one form of energy into another (e.g., pressure, temperature, or flow into electrical signals). These cables are crucial components in measurement, control, and monitoring systems across complex industrial and medical environments. Their core functionality depends on maintaining signal integrity despite electromagnetic interference (EMI), mechanical stress, and harsh operational conditions. The construction often involves sophisticated shielding, specialized jacketing materials, and low-capacitance designs to ensure accurate data transmission, which is non-negotiable in critical applications like medical imaging, aerospace telemetry, and deep-sea exploration.

Major applications of transducer cables span across several high-growth sectors. In the healthcare industry, they are indispensable for connecting ultrasound probes, patient monitoring sensors, and diagnostic equipment, where clarity and absence of noise are vital for clinical accuracy. Industrially, they are integrated into smart factories and infrastructure projects for connecting pressure sensors in pipelines, strain gauges in civil engineering, and flow meters in processing plants, facilitating predictive maintenance and operational optimization. The consistent demand for real-time, high-fidelity data transmission driven by the Industry 4.0 paradigm and the accelerating adoption of sophisticated diagnostic imaging technologies are primary market drivers.

The core benefits derived from utilizing high-quality transducer cables include enhanced system reliability, extended equipment lifespan due to superior durability, and, most importantly, the assurance of data accuracy required for automated decision-making. Driving factors include the increasing complexity and sensitivity of transducer technology, demanding cables with higher bandwidth and superior noise immunity. Furthermore, stringent regulatory requirements, particularly in the medical and aerospace sectors, mandate the use of certified, robust cables, thereby elevating the value proposition of specialized transducer cable manufacturers globally.

The Transducer Cable Market is characterized by stable growth, fueled primarily by the rapid expansion of the healthcare sector, specifically in diagnostic imaging and remote patient monitoring, and intensified investment in industrial automation and condition monitoring systems. Business trends indicate a strong move toward customization, where manufacturers are focusing on developing hybrid cables that integrate power, signal, and sometimes fiber optics within a single jacket to reduce installation complexity and footprint. Strategic mergers and acquisitions among cable manufacturers and sensor producers are common, aiming to provide integrated, plug-and-play solutions to large industrial end-users. Furthermore, sustainability is becoming a key trend, with increasing focus on halogen-free and recyclable jacket materials to meet environmental mandates.

Regionally, Asia Pacific (APAC) stands out as the fastest-growing market, largely due to explosive growth in manufacturing capabilities, urbanization driving infrastructure development, and substantial governmental investments in medical device manufacturing in countries like China, India, and South Korea. North America and Europe maintain dominance in terms of technology adoption and high-value applications, particularly in aerospace, defense, and high-end medical device manufacturing, demanding premium, highly specialized cable types with military-grade specifications. The adoption curve for smart factory technology is particularly steep in Western economies, driving demand for industrial Ethernet and specialized sensor cables.

Segment trends highlight the dominance of multiconductor cables due to their versatility in handling multiple signals, although coaxial and fiber optic cables are experiencing accelerated growth driven by high-frequency and high-speed data requirements, respectively. By application, the medical segment commands the largest market share, consistently requiring innovation in miniaturization and flexibility for portable devices. The oil & gas sector also presents substantial opportunity, requiring highly robust and temperature-resistant cables for downhole and subsea monitoring applications, driving revenue growth for specialized high-durability product lines. Overall, market evolution is characterized by continuous material science advancements focused on resilience and signal integrity.

Common user inquiries concerning AI's impact on the Transducer Cable Market frequently revolve around two primary themes: the role of AI in predictive maintenance and its influence on data volume and transmission requirements. Users are concerned about whether AI-driven sensor networks will necessitate significantly higher bandwidth or drastically alter the design requirements for existing cables. Key expectations center on AI models improving the accuracy of diagnostics, necessitating higher quality, low-noise signal transmission from transducers. This emphasis on high-fidelity input data means AI indirectly drives demand for premium, highly shielded cables, making robust signal integrity an even greater competitive factor. The summary conclusion is that AI deployment does not replace the cable infrastructure but rather elevates the technical demands placed upon it, driving innovation toward ultra-low latency and fault-tolerant cabling solutions.

The dynamics of the Transducer Cable Market are influenced by a robust combination of drivers and opportunities linked to global industrialization and technological advancement, tempered by significant restraints regarding material costs and stringent regulatory hurdles. The primary drivers include the global push towards Industry 4.0, which mandates comprehensive sensor deployment across manufacturing and logistics, exponentially increasing the need for connectivity solutions. Opportunities are particularly visible in the development of specialized, highly durable cables for extreme environments, such as deep-sea exploration (subsea) and high-temperature environments (aerospace/oil & gas), offering higher profit margins for innovators.

Restraints largely center on the volatility of raw material prices, particularly copper and specialized polymer jackets, which directly influence manufacturing costs and profitability. Additionally, the need to comply with diverse and evolving international standards (e.g., medical device certifications, hazardous environment ratings) creates significant barriers to entry and operational complexity. The impact forces show that technological innovation, particularly in miniaturization and enhanced shielding materials, exerts a high positive influence, allowing cables to be used in increasingly confined and electromagnetically noisy spaces, thus expanding the addressable market considerably.

Key impact forces indicate that the substitution threat from wireless technologies, while present, remains relatively low for critical, high-speed, or high-power transducer applications where reliability and latency are paramount. The bargaining power of buyers is moderate, concentrated among large OEM manufacturers who procure high volumes and demand customization. Conversely, the bargaining power of suppliers, particularly those providing specialized components like high-purity copper or custom fluoropolymers, is often high due to supply chain complexities and proprietary material science knowledge.

The Transducer Cable Market is meticulously segmented based on Type, Application, and End-Use Industry, reflecting the diverse technical requirements imposed by different operational environments and data transmission needs. The segmentation framework is critical for market participants to identify niche opportunities, allocate R&D resources effectively, and tailor product offerings to specific compliance standards. The technical distinctions among segments, such as the difference in shielding robustness between medical imaging cables and industrial pressure sensor cables, significantly influence pricing structures and competitive strategy. Market analysis reveals a persistent trend towards high-performance segments, particularly those serving sensitive or mission-critical applications where failure tolerance is near zero, demanding premium pricing and specialized material engineering.

The value chain for the Transducer Cable Market begins with upstream activities involving the sourcing and processing of raw materials, primarily high-purity copper conductors, insulation polymers (like PTFE, FEP, or specialized PUR for durability), and shielding materials (aluminum foil, braided copper). This stage is capital intensive, relying heavily on specialized chemical and metal processing suppliers. Key differentiation here lies in material science, with leading cable manufacturers often collaborating closely with chemical companies to develop proprietary jacket compounds offering superior chemical resistance, flexibility, and temperature performance, essential for compliance in harsh operational environments.

Midstream activities involve core manufacturing processes: drawing and stranding conductors, insulation extrusion, twisting/cabling, sophisticated shielding application, and jacketing. Advanced manufacturers utilize automated processes and rigorous quality control (QC) to minimize defects, particularly focusing on maintaining tight tolerances for impedance and capacitance, which are crucial for signal integrity. Vertical integration is observed where large market players control conductor drawing to ensure consistency. Following manufacturing, cable assemblies are often customized into finished products through cutting, stripping, and connectorization, adding significant value specific to the end-user's equipment interface requirements.

Downstream distribution channels are characterized by a mix of direct sales to large Original Equipment Manufacturers (OEMs)—especially in the medical and aerospace sectors—and indirect channels involving specialized industrial distributors, component resellers, and system integrators for general industrial monitoring applications. Direct sales channels are preferred for high-complexity, low-volume orders requiring custom specifications and technical support, ensuring precise compatibility with the transducer system. Indirect channels provide broad market reach and logistical efficiency for standardized, high-volume products used in routine industrial setups. Effective supply chain management and strong distributor relationships are vital for penetrating geographically dispersed end-use markets efficiently.

Potential customers for transducer cables are typically large-scale technology integrators and manufacturers operating in compliance-heavy and data-critical industries where equipment reliability directly impacts safety, quality, or operational uptime. The primary customer base comprises OEMs in the medical device sector, such as manufacturers of MRI machines, CT scanners, and ultrasound systems, who require robust, biocompatible, and high-flex-life cables for probes and sensors. Another significant customer group includes industrial automation firms and system integrators specializing in implementing smart factory solutions, requiring cables to connect PLCs, condition monitoring sensors (vibration, strain), and machine vision systems in demanding factory environments.

Furthermore, aerospace and defense contractors represent high-value, albeit volume-constrained, customers demanding cables that meet stringent military specifications regarding temperature tolerance, radiation resistance, and fire safety. The subsea and marine industry, serving offshore oil platforms, research vessels, and defense sonar systems, also constitutes a crucial customer segment, necessitating extreme water-blocking and pressure-resistant cable designs. These end-users prioritize product longevity and certification over cost, driving demand for specialized and expensive cable materials, ensuring manufacturers focus their sales strategies on technical capability and regulatory compliance guarantees.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $2.1 Billion |

| Market Forecast in 2033 | $3.3 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | TE Connectivity, Belden Inc., Prysmian Group, Trelleborg AB, Furukawa Electric Co., Ltd., W. L. Gore & Associates, Inc., LAPP Group, Nexans S.A., Leoni AG, Volex plc, Cicoil Corporation, Amphenol Corporation, Sumitomo Electric Industries, Huber+Suhner, HELUKABEL GmbH, General Cable Technologies (Prysmian Group), Marmon Group, Precision Interconnect (Amphenol), Alpha Wire, Northwire (The Lemax Group) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Transducer Cable Market technology landscape is characterized by continuous innovation focused on maximizing signal integrity, durability, and miniaturization. A core technological advancement involves specialized shielding techniques, moving beyond simple braiding to utilize complex foil-braid combinations, coupled with conductive polymer layers, specifically designed to mitigate the increasing threat of electromagnetic interference (EMI) in densely packed electronic environments, particularly crucial for medical ultrasound probes and high-speed industrial sensors. Furthermore, low-capacitance dielectric materials, such as foamed polyethylenes or specialized fluoropolymers, are increasingly employed to ensure minimal signal degradation and fast response times required by modern digital transducers transmitting high-frequency data streams.

Another pivotal technological trend is the development and adoption of high-flex and robotic-grade cables, particularly vital in the manufacturing and automation sectors where cables are subjected to millions of repetitive bending cycles. Manufacturers are leveraging thermoplastic elastomers (TPE) and highly durable polyurethane (PUR) jacketing compounds formulated for superior resistance to oils, chemicals, and abrasion while maintaining excellent mechanical flex life. The move towards hybrid cable designs—combining power conductors, twisted pair data lines, and often fiber optics—streamlines installations, reduces overall system weight, and enhances data transmission capability over long distances, addressing the integrated needs of modern diagnostic and monitoring equipment.

Fiber optic technology integration is becoming essential for applications demanding extreme bandwidth and absolute immunity to electrical noise, especially in large-scale data acquisition systems and high-resolution medical imaging. Specialized fiber optic transducer cables are engineered to handle harsh physical conditions, including high pressure and temperature variances, broadening the market scope into challenging domains like downhole oil and gas monitoring. The overall technology trajectory emphasizes smart cable solutions, incorporating RFID or specialized marking systems for asset tracking and predictive maintenance insights, thus merging physical cable technology with digital management capabilities, aligning with the broader smart infrastructure paradigm.

Shielding, typically provided by foil or braid layers, is critical for protecting the low-voltage, sensitive signals transmitted by transducers from external electromagnetic interference (EMI) and radio frequency interference (RFI), ensuring accurate and reliable data transmission necessary for monitoring and control systems.

The medical sector demands extreme miniaturization, high flexibility (flex-life), and biocompatible, non-shedding jacketing materials (often USP Class VI certified) for repeated sterilization and use in patient contact applications like ultrasound probes and diagnostic catheters, pushing manufacturers towards advanced polymer science.

Coaxial cables are designed for high-frequency signals, offering superior electrical performance and controlled impedance for single channels. Multiconductor cables are used for transmitting multiple lower-frequency or mixed signals (data, power, ground) simultaneously within a single jacket, prioritizing system integration and complexity reduction.

Industry 4.0 significantly increases demand by requiring extensive sensor deployment across manufacturing facilities for continuous condition monitoring and data acquisition. This necessitates robust, industrial-grade transducer cables capable of supporting high-speed industrial communication protocols and resisting harsh factory environments (e.g., oil, abrasion, heat).

The Asia Pacific (APAC) region is projected to demonstrate the fastest growth rate, primarily driven by large-scale investments in industrial automation, expanding healthcare infrastructure, and rapid technological adoption within key emerging economies such as China and India.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.