ID : MRU_ 432444 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

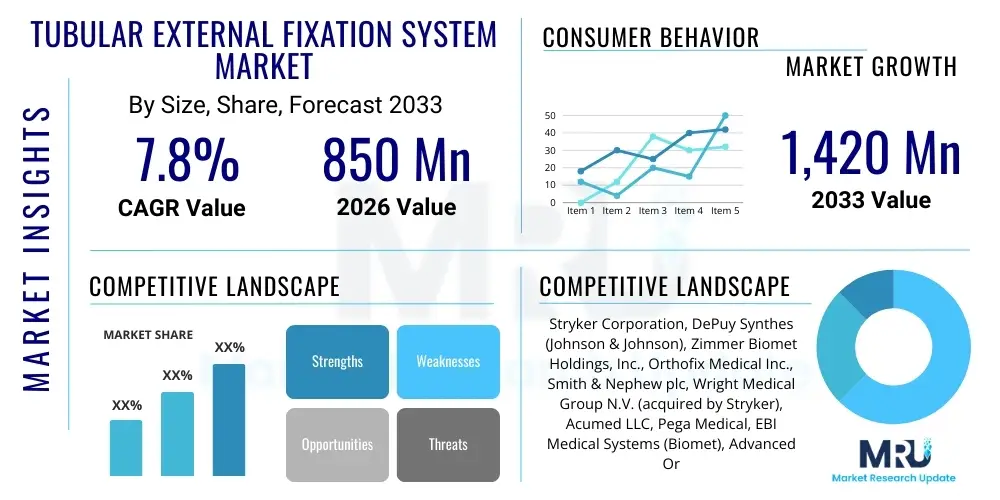

The Tubular External Fixation System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at $850 million in 2026 and is projected to reach $1,420 million by the end of the forecast period in 2033.

The Tubular External Fixation System Market encompasses devices used in orthopedic trauma management to stabilize complex fractures, correct deformities, and perform limb lengthening procedures. These systems are characterized by a rigid external frame connected to the bone fragments via pins or wires, offering stability outside the body. They are particularly vital in emergency trauma settings, where soft tissue damage or contamination prevents internal fixation. The core product includes various components such as clamps, rods (tubular segments), posts, and pins/wires, fabricated primarily from biocompatible materials like titanium alloys, stainless steel, or carbon fiber composites. The increasing incidence of high-energy trauma, road accidents, and sports injuries globally is a primary catalyst driving the demand for these immediate stabilization solutions.

Tubular external fixators are preferred for definitive fracture management in cases involving open fractures, severe comminution, or osteomyelitis, due to their ease of application, minimal soft tissue disruption, and ability to allow weight-bearing earlier than traditional casting methods in certain applications. These systems are essential tools in damage control orthopedics (DCO), providing temporary stability until the patient is physiologically optimized for definitive surgery. Furthermore, advancements in design, such as modular and hybrid systems, are expanding their utility beyond simple fracture stabilization into complex reconstructive surgeries, including pelvic ring stabilization and pediatric orthopedics for growth plate considerations.

The key driving factors fueling market expansion include a rapidly aging global population prone to falls and fragility fractures, enhanced access to advanced orthopedic care in emerging economies, and continuous technological innovation focusing on reducing system weight, improving radiolucency, and simplifying the surgical technique. The systems are highly beneficial for managing poly-trauma patients, offering a versatile and adjustable solution for limb realignment. Moreover, the increasing adoption of carbon fiber materials is enhancing imaging capabilities, reducing artifacts during subsequent CT or MRI scans, thereby improving post-operative assessment and long-term patient outcomes.

The Tubular External Fixation System Market is poised for substantial growth, driven fundamentally by the escalating worldwide burden of traumatic injuries and musculoskeletal disorders. Key business trends indicate a strategic shift among leading manufacturers toward developing modular and hybrid fixation systems that offer greater flexibility and reduced invasiveness. There is a strong emphasis on integrating smart materials, particularly carbon fiber composites, to enhance imaging compatibility and decrease system profile, addressing a major clinical concern. Competitive dynamics are characterized by intensive merger and acquisition activity focused on consolidating niche expertise, particularly in pediatric and deformity correction segments. Furthermore, manufacturers are heavily investing in surgeon training and educational programs to ensure optimal utilization of sophisticated fixation techniques, thereby accelerating adoption rates globally.

From a regional perspective, North America and Europe currently dominate the market due to established healthcare infrastructure, high reimbursement rates for orthopedic procedures, and a high prevalence of sports-related injuries and vehicular trauma. However, the Asia Pacific region is projected to register the fastest growth rate. This accelerated expansion is attributed to rapid improvements in healthcare access, modernization of trauma care facilities in countries like China and India, increasing disposable incomes enabling sophisticated treatments, and the demographic pressures of a large population base susceptible to trauma. Latin America and MEA are also showing promising growth, primarily driven by investments in public health infrastructure and rising awareness regarding specialized orthopedic treatments.

Segmentation trends highlight the increasing demand for advanced materials, with titanium and carbon fiber systems gaining significant traction over traditional stainless steel due to superior strength-to-weight ratios and bio-compatibility. The application segment sees robust growth in lower extremity and pelvic fixation, often associated with high-impact trauma. End-user analysis reveals that specialized Trauma Centers and large Hospitals remain the primary consumers, although Ambulatory Surgical Centers (ASCs) are increasingly adopting these systems, particularly for less complex, elective deformity correction procedures, influencing product design towards portability and streamlined sterilization processes.

User queries regarding the impact of Artificial Intelligence (AI) on the Tubular External Fixation System Market frequently center on how AI can enhance surgical precision, improve patient selection for fixation types, and optimize post-operative monitoring to prevent complications like pin tract infections or non-union. Users are keenly interested in the potential for AI-driven surgical planning systems that can model complex fractures in 3D, simulating the optimal placement of pins and rod configurations to maximize stability and minimize stress shielding. Furthermore, there is high expectation for AI algorithms to analyze radiographic images and clinical data, predicting outcomes, identifying high-risk patients for revision surgery, and automating the assessment of bone healing progression, thereby transforming the current reliance on manual interpretation and subjective clinical judgment in follow-up care.

The Tubular External Fixation System Market is significantly shaped by robust Drivers, clinical Restraints, and transformative Opportunities, collectively known as DRO, which interact to create the defining Impact Forces. Key drivers include the global epidemic of orthopedic trauma resulting from escalating road traffic accidents, industrial mishaps, and military conflicts, demanding immediate and reliable stabilization solutions. The increasing prevalence of complex skeletal deformities, particularly in pediatric populations requiring limb reconstruction and lengthening, further bolsters demand. Furthermore, the clinical advantage of external fixation in managing severe open fractures (Gustilo Type III) with massive soft tissue injury or contamination, where internal fixation is contraindicated, cements its indispensable role in trauma protocols. These drivers exert a strong positive impact, accelerating product development and clinical adoption, particularly in emerging trauma care sectors worldwide.

Conversely, the market faces significant restraints. A primary concern is the high incidence of pin tract infections, which remains a leading complication associated with external fixators, requiring meticulous patient care and potentially leading to premature device removal or prolonged hospitalization. Another restraint involves the bulkiness and relatively reduced patient comfort and mobility compared to internal fixation, which can affect long-term adherence and quality of life. The steep learning curve associated with complex frame construction, particularly for circular and hybrid systems used in deformity correction, restricts broader adoption to highly specialized orthopedic surgeons. These restraints necessitate continuous research into bio-active coatings for pins and simplification of frame assembly techniques to mitigate adverse effects and widen the user base.

Opportunities for growth are abundant, primarily centered on technological convergence. The integration of bio-absorbable materials for temporary components, development of lightweight, radiolucent carbon fiber frames, and the incorporation of remote monitoring technologies (telemedicine) for post-operative management offer significant avenues for market expansion. Furthermore, specializing in niche applications such as bone transport techniques for large bone defects and enhanced systems for ankle and foot fixation represents a high-potential segment. The strongest impact force on the market is the continuous technological innovation aimed at reducing complications and improving patient ergonomics, ensuring that external fixators remain the gold standard for specific, high-acuity trauma and reconstructive cases, thereby maintaining a steady market trajectory despite the competition from internal fixation methods.

The Tubular External Fixation System Market is comprehensively segmented based on product type, material composition, clinical application, and end-user facilities. This segmentation provides a granular view of demand dynamics, highlighting the varying requirements across surgical disciplines and geopolitical regions. The product segment is crucial, differentiating between standard monolateral fixators, which are workhorses for temporary trauma stabilization, and more complex circular and spatial frames used predominantly for specialized reconstructive procedures like gradual limb correction. Material segmentation reflects the ongoing transition from heavier, less radiolucent stainless steel to advanced, lightweight, and superior imaging-compatible titanium and carbon fiber composites, driven by clinical preferences for reduced scanning artifacts and improved patient comfort. Understanding these segment trends is vital for manufacturers planning R&D investments and targeted marketing strategies.

Application-based segmentation reveals the anatomical focus of the devices, with lower extremity fixators (tibia, femur) historically dominating the market due to the high incidence of severe lower limb trauma (e.g., tibial plateau fractures, pilon fractures). However, the demand for upper extremity and pelvic fixators is growing steadily, reflecting improved diagnostic capabilities and standardized protocols for poly-trauma management. The end-user analysis confirms the critical role of dedicated trauma centers and large hospitals, which handle the majority of acute, high-volume trauma cases requiring immediate external stabilization. This structure dictates distribution channel strategies, emphasizing direct sales and strong clinical relationships with orthopedic trauma specialists.

Overall, the market exhibits a clear trend toward high-value, specialized segments. While basic, cost-effective stainless steel monolateral systems maintain a stable share, particularly in price-sensitive markets, the future growth is overwhelmingly concentrated in modular carbon fiber systems capable of complex deformity correction. The interplay between sophisticated technology and clinical necessity ensures that the market remains resilient and responsive to advancements in orthopedic surgery, promoting a continuous cycle of innovation focused on minimizing invasiveness and optimizing long-term functional outcomes for patients suffering from severe skeletal injuries.

The value chain for the Tubular External Fixation System Market begins with the highly specialized upstream analysis involving the sourcing and processing of raw materials, primarily medical-grade titanium, stainless steel, and aerospace-quality carbon fiber. This stage requires rigorous quality control and certification due to the critical biological environment in which the devices function. Key activities include metallurgy, polymer synthesis, and precision machining to produce highly tolerance-specific components such as clamps, connecting rods, and Schanz screws. Suppliers capable of providing consistent, high-purity materials at competitive costs gain a strategic advantage, often leading to long-term supply contracts with major device manufacturers. The cost of materials, especially titanium and carbon fiber, constitutes a significant portion of the final product cost, making efficient procurement essential for maintaining profitability.

Midstream activities encompass the manufacturing, assembly, sterilization, and quality assurance processes. Leading manufacturers utilize advanced CNC machining, additive manufacturing (3D printing) for customized components, and stringent sterile packaging protocols. Research and development (R&D) plays a crucial role here, focusing on improving biomechanical stability, developing anti-bacterial coatings for pins, and simplifying the modular design for ease of surgical use. Intellectual property (IP) surrounding pin-to-bone interface technology and modular frame construction is highly valued. The distribution channel is bifurcated into direct sales teams and specialized medical distributors. Direct distribution is often preferred by major companies in developed markets to maintain tighter control over product demonstration, clinical support, and inventory management, particularly for complex, high-value systems like spatial frames.

Downstream analysis focuses on the end-users: hospitals, trauma centers, and orthopedic surgeons. The final sale involves intensive surgeon education and technical support, as the successful deployment of external fixators heavily relies on surgical skill and adherence to established protocols. Indirect distribution channels, utilizing independent local distributors, are more common in emerging markets where manufacturers seek to leverage local market knowledge and existing clinical networks. Post-market surveillance, regulatory compliance (FDA, CE Mark), and managing product recalls are continuous processes that ensure patient safety and maintain market trust. The effectiveness of the supply chain in reacting quickly to emergency trauma needs is paramount, requiring highly efficient logistics and robust inventory management at the regional level.

The primary customers and end-users of Tubular External Fixation Systems are specialized medical institutions that manage acute orthopedic trauma and complex skeletal deformities. High-volume, Level I and Level II Trauma Centers are the most significant buyers, as they handle severe poly-trauma cases, including high-energy vehicular accidents and ballistic injuries, necessitating immediate damage control orthopedics (DCO). These centers require a broad inventory of standard monolateral, circular, and pelvic fixation systems available 24/7. Their purchasing decisions are heavily influenced by product reliability, ease of application, long-term clinical data, and integration capabilities with established trauma care protocols.

General hospitals with dedicated orthopedic departments also represent a substantial customer base, particularly for managing less severe closed fractures, temporary stabilization prior to definitive internal fixation, and elective deformity correction cases. Within these settings, the economic viability and versatility of the fixators play a crucial role. Furthermore, specialized pediatric hospitals and clinics are increasingly important customers due to the growing need for limb reconstruction and lengthening procedures using spatial frames, often requiring highly precise, customizable components tailored for growing bone structures. These institutions prioritize systems that offer minimal impact on growth plates and allow for complex adjustments over an extended treatment period.

Ambulatory Surgical Centers (ASCs) are emerging potential customers, primarily adopting these systems for outpatient or short-stay elective procedures, such as minor extremity deformity corrections, reflecting the trend toward cost-effective, decentralized healthcare. Rehabilitation centers, while not direct end-users of the surgical system, often play a role in post-operative care, influencing demand for systems that facilitate early weight-bearing and physiotherapy. Ultimately, the purchasing entity (hospital procurement) makes the final decision, but the demand is critically driven by orthopedic trauma surgeons, pediatric orthopedic specialists, and reconstructive surgeons who specify the required brand and type based on their surgical preferences and clinical experience.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $850 million |

| Market Forecast in 2033 | $1,420 million |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Stryker Corporation, DePuy Synthes (Johnson & Johnson), Zimmer Biomet Holdings, Inc., Orthofix Medical Inc., Smith & Nephew plc, Wright Medical Group N.V. (acquired by Stryker), Acumed LLC, Pega Medical, EBI Medical Systems (Biomet), Advanced Orthopaedic Solutions, Bioretec Ltd., Response Ortho, Meril Life Sciences Pvt. Ltd., Elite Surgical, Fixus Medical, Globus Medical, Integra LifeSciences, Limacorporate S.p.A., B. Braun Melsungen AG, Medtronic plc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Tubular External Fixation System Market is undergoing a rapid technological evolution, moving beyond simple static stabilization toward dynamic, customizable, and patient-friendly solutions. A critical advancement involves the widespread adoption of carbon fiber composites, which offer superior strength-to-weight ratios and are completely radiolucent. This radiolucency is vital as it allows surgeons to obtain high-quality X-rays, CT scans, and MRI images post-operatively without significant metallic artifact obscuring the fracture site or adjacent soft tissues, greatly enhancing the monitoring of bone consolidation and reducing the need for frame removal for imaging purposes. Furthermore, the modular nature of modern tubular systems allows for intra-operative adjustments and the conversion from temporary fixation (damage control) to definitive fixation using the same frame components, streamlining procedures and reducing inventory complexity.

Another major technological thrust is in the development of sophisticated spatial frames, such as the Taylor Spatial Frame (TSF) and similar hexapod systems, which utilize computer software and six degrees of freedom to achieve highly accurate, gradual correction of complex multiplanar deformities. These systems transform the clinical management of challenging limb malalignments, non-unions, and bone defects through programmed strut adjustments. The use of sterile, pre-assembled modules and quick-connect clamps is becoming standard, significantly reducing operative time and the risk of contamination. Additionally, manufacturers are focusing heavily on enhancing the pin-bone interface through specialized thread designs (e.g., hydroxyapatite coating, self-drilling/self-tapping pins) aimed at maximizing stability, reducing the risk of pin loosening, and minimizing the potential for pin tract infection, which remains a primary complication associated with these devices.

Looking ahead, the landscape is being shaped by digitalization and material science. Smart fixation systems equipped with embedded sensors are in development, designed to monitor biomechanical parameters such as load distribution, strain, and micromotion at the fracture site. This data, transmitted wirelessly, allows surgeons to remotely assess the progression of healing and modify weight-bearing instructions via telemedicine platforms, thereby personalizing rehabilitation protocols. Additive manufacturing (3D printing) is also beginning to play a role, allowing for the rapid creation of patient-specific, customized jigs and guides to assist in complex frame assembly and pin placement, promising unprecedented levels of accuracy and customization in orthopedic trauma and reconstructive surgery. These technological leaps are fundamental to the market's trajectory, focusing on improving clinical outcomes and patient quality of life.

Tubular external fixation systems are primarily used in orthopedic trauma surgery for the temporary stabilization of complex, high-energy fractures (especially open fractures), damage control orthopedics (DCO), joint stabilization, and definitively for specialized procedures like limb lengthening, bone transport, and correction of skeletal deformities.

Carbon fiber fixators are significantly lighter and provide superior radiolucency compared to stainless steel or titanium systems. This radiolucency is critical as it minimizes imaging artifacts on X-rays and CT scans, allowing for clearer visualization of the fracture healing process and surrounding soft tissues without needing to remove the device for imaging.

The major challenges include the high risk of pin tract infection, which requires rigorous site care; potential pin loosening leading to reduced stability; and reduced patient comfort and mobility due to the external bulkiness of the frame, which can sometimes interfere with daily activities and sleep.

Key technological drivers include the development of modular and hybrid systems for versatile application, the integration of specialized anti-microbial coatings on fixation pins to prevent infection, and the advancement of computer-assisted spatial frames for precision deformity correction and bone reconstruction procedures.

The Material segment, specifically carbon fiber composites, holds the highest growth potential due to increasing clinical preference for lightweight, highly rigid, and radiolucent systems that improve post-operative imaging quality and enhance patient compliance and mobility.

In DCO, external fixation provides rapid, minimally invasive provisional stability for severely injured poly-trauma patients who are physiologically unstable. This temporary stabilization minimizes secondary soft tissue damage and blood loss, allowing the surgical team to delay definitive internal fixation until the patient is medically optimized, significantly reducing morbidity and mortality risk.

Yes, external fixators, particularly specialized circular and spatial frames, are extensively used in pediatric orthopedics for managing complex fractures, correcting congenital or acquired limb length discrepancies, and treating angular deformities while minimizing disturbance to the delicate growth plates, which is a major advantage over most internal fixation methods in children.

AI is beginning to contribute by enhancing pre-operative surgical planning through 3D modeling and stress analysis, optimizing pin placement to avoid vital structures, and using machine learning to analyze sequential radiographic images to accurately assess bone healing rates, helping surgeons decide the optimal timing for frame removal.

Hospital procurement decisions are primarily influenced by the system's clinical efficacy and reliability, total cost of ownership (including inventory and disposables), vendor reputation and technical support, ease of sterilization, and comprehensive training programs offered by the manufacturer to the orthopedic surgical staff.

Yes, there is a growing trend, particularly for certain pins, wires, and single-use clamps used in emergency trauma settings. This shift aims to reduce the logistical burden of cleaning and sterilization, decrease the risk of surgical site infections associated with reusable components, and improve overall operational efficiency in busy trauma units.

Monolateral (or unilateral) fixators are simpler, single-bar systems primarily used for temporary stabilization or simple diaphyseal fractures, offering stability in one plane. Circular fixators, such as the Ilizarov frame, are complex, multi-ring systems used for highly specialized procedures like bone segment transport and gradual, multiplanar deformity correction, providing superior rigidity and dynamic adjustment capabilities.

The market is addressing this through R&D focused on pins with advanced surface technologies, including antimicrobial coatings (such as silver or antibiotic-loaded polymers) and improved thread designs that minimize micromotion at the bone-pin interface. Additionally, standardized care protocols and specialized dressings are being promoted globally.

The Asia Pacific (APAC) region exhibits the highest market growth potential, fueled by rapidly improving healthcare infrastructure, massive population bases facing increasing incidence of road traffic accidents, rising healthcare expenditure, and accelerating adoption of advanced Western surgical technologies in major developing economies like India and China.

Hybrid fixation systems combine the principles of circular and monolateral fixation. Typically, a circular frame is used near a joint (e.g., knee or ankle) to stabilize the peri-articular segment using tensioned wires, while the diaphyseal (shaft) portion of the bone is stabilized with a monolateral or tubular rod system connected to half-pins, offering high rigidity where needed and flexibility elsewhere.

New entrants face stringent regulatory requirements from bodies like the FDA in the US and the EMA in Europe, requiring extensive biomechanical testing, biocompatibility documentation for novel materials, and often complex clinical trial data to demonstrate safety and efficacy, particularly for specialized deformity correction devices.

While advances in internal fixation (e.g., locking plates, intramedullary nails) have reduced the use of external fixation for simple closed fractures, external fixation remains indispensable and irreplaceable for specific indications, such as definitive treatment of severe open fractures, pelvic ring injuries, and complex limb lengthening or bone transport procedures where soft tissue integrity is compromised or gradual correction is required.

Telemonitoring, potentially integrated with smart fixators, allows surgeons to remotely track patient progress, monitor for early signs of pin site complications, and adjust the frame or weight-bearing advice based on wirelessly transmitted biomechanical data. This improves follow-up efficiency and patient safety, especially in rural or geographically isolated settings.

Manufacturers are optimizing comfort by utilizing lighter materials like carbon fiber, creating lower-profile designs to reduce bulkiness, and developing ergonomic clamp systems that minimize skin and soft tissue irritation, thereby improving the patient's overall experience during the prolonged treatment period.

The overwhelming trend in new product development is the shift away from stainless steel toward titanium alloys and, most notably, carbon fiber composites. This shift prioritizes reduced weight, enhanced compatibility with advanced imaging technologies (MRI/CT), and improved long-term patient ergonomics and mobility.

The highest value-add activity is concentrated in the research and development (R&D) and specialized manufacturing stages. This includes developing proprietary software for spatial frame planning, designing anti-infection pin technology, and precision machining of high-tolerance modular components, which command premium pricing in the final market.

The increasing complexity of high-velocity trauma requires more sophisticated and versatile stabilization techniques. External fixators are perfectly suited for this, offering immediate, adjustable stability for complex, comminuted fractures with severe soft tissue compromise, reinforcing their critical role in modern, standardized trauma protocols.

Constraints in emerging economies primarily include lower affordability limiting the widespread adoption of premium carbon fiber and specialized systems, less developed trauma center infrastructure, variable surgeon training levels in complex frame construction, and inconsistent reimbursement policies for advanced orthopedic procedures.

Bio-absorbable materials are anticipated to be used primarily for specific fixation pins or temporary components. The goal is to design components that maintain stability during the critical healing phase and then gradually dissolve, eliminating the need for a second surgery required for the removal of metallic components, thereby reducing cost and surgical risk.

The pelvic and acetabular fixation segment is witnessing rapid innovation. Given the high morbidity associated with pelvic ring instability, there is continuous development of specialized, low-profile external fixation frames and percutaneous pin placement techniques to achieve strong, anatomical stabilization with minimal invasiveness, improving outcomes in severe pelvic trauma.

Competitive strategies often involve dual pricing models: premium pricing for specialized, R&D-intensive systems (like TSF or specialized carbon fiber fixators) offered in developed markets, and more competitive, cost-effective pricing for standard monolateral systems marketed in price-sensitive emerging economies to capture broader market share and volume.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.