ID : MRU_ 436505 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

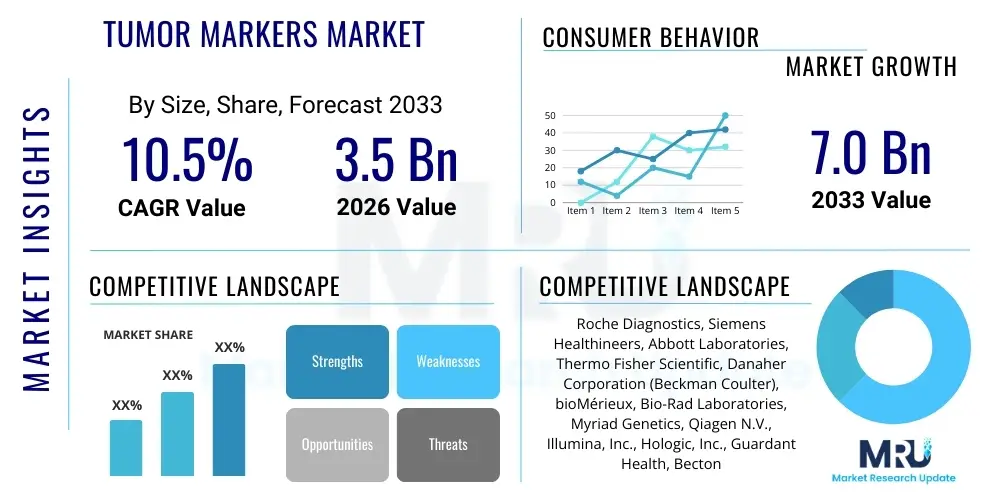

The Tumor Markers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2026 and 2033. The market is estimated at $3.5 Billion in 2026 and is projected to reach $7.0 Billion by the end of the forecast period in 2033.

The Tumor Markers Market encompasses a range of biochemical substances, typically proteins, produced either by the cancer cells themselves or by the body in response to the presence of cancer or certain benign conditions. These markers are crucial tools in oncology, primarily utilized for screening high-risk populations, confirming diagnosis, determining prognosis, staging cancer, and monitoring treatment efficacy and recurrence. Key products include established protein markers like Prostate-Specific Antigen (PSA), Carcinoembryonic Antigen (CEA), and Carbohydrate Antigen 125 (CA 125), alongside emerging technologies focused on circulating tumor cells (CTCs) and cell-free DNA (cfDNA).

Major applications of tumor markers span across various cancer types, including breast, prostate, colorectal, lung, and ovarian cancers. The increasing global prevalence of these chronic diseases, coupled with growing awareness regarding the benefits of early cancer detection, significantly drives market demand. Furthermore, advancements in diagnostic technologies, particularly the shift towards less invasive testing methods such as liquid biopsy, enhance the utility and accessibility of tumor marker analysis, moving the technology closer to personalized medicine paradigms.

The principal benefits derived from the use of tumor markers include their ability to guide personalized treatment strategies, predict patient response to specific therapies, and enable timely intervention upon disease relapse. Technological drivers include high-throughput screening methods, such as Enzyme-Linked Immunosorbent Assays (ELISA), Chemiluminescence Immunoassays (CLIA), and sophisticated mass spectrometry techniques, which offer increased sensitivity and specificity compared to traditional immunohistochemistry methods. This technological evolution is pivotal in overcoming historical limitations associated with the low predictive value of single-marker tests, pushing the market towards panel-based testing approaches.

The Tumor Markers Market is characterized by robust business trends driven primarily by the global imperative for early and accurate cancer detection and the integration of precision medicine into clinical practice. Strategic collaborations between pharmaceutical companies and diagnostic developers are accelerating the discovery and validation of novel biomarkers, particularly those related to treatment response and drug resistance. Key business trends include the strong adoption of liquid biopsy technologies, which provide non-invasive alternatives for monitoring disease progression, and the consolidation of diagnostic platforms to offer comprehensive multianalyte testing solutions. Furthermore, increasing investments in proteomics and genomics research are continuously expanding the repertoire of clinically relevant tumor markers, driving strong revenue growth across developed and developing economies.

Regionally, North America maintains market dominance due to high healthcare expenditure, sophisticated technological infrastructure, and favorable reimbursement policies for advanced diagnostic tests. However, the Asia Pacific (APAC) region is projected to exhibit the highest growth rate, fueled by rapid expansion of healthcare facilities, increasing prevalence of cancer, and rising patient awareness. Governmental initiatives in countries like China and India focused on improving cancer screening programs are significant regional drivers. Segment trends indicate that the utilization of protein biomarkers remains high for routine monitoring, but the molecular markers segment (based on genetic and epigenetic analysis) is expanding rapidly due to its superior predictive capabilities for targeted therapies. The application segment focused on therapy monitoring and recurrence detection demonstrates the fastest growth, reflecting the need for continuous, non-invasive patient surveillance post-treatment.

The market faces operational challenges, including the inherent lack of specificity and sensitivity of certain traditional markers, leading to false positives or negatives, which necessitates continuous R&D investment to validate new generation biomarkers. Successful implementation relies heavily on regulatory harmonization and ensuring clinical utility is robustly proven across diverse patient populations. Strategic success factors involve differentiating product offerings through enhanced multiplexing capabilities and integrating AI-driven analytical tools to manage the complexity of large biomarker datasets, thereby providing clearer clinical actionable insights for oncologists.

User queries regarding the impact of Artificial Intelligence (AI) on the Tumor Markers Market frequently center on its ability to enhance diagnostic accuracy, predict therapeutic outcomes, and streamline high-throughput screening processes. Common questions involve how AI algorithms can integrate complex data from multiple sources (imaging, genomics, proteomics, clinical history) to provide a more holistic understanding of a patient’s cancer status, thereby improving upon the limitations of single-marker assays. Users also express interest in AI's role in the rapid discovery and validation of new, highly specific biomarkers, reducing the time and cost associated with traditional research methods. Concerns often revolve around data privacy, algorithm bias, and the necessity for regulatory frameworks capable of validating AI-driven diagnostic tools, emphasizing the need for robust, explainable AI (XAI) models in clinical settings.

AI is fundamentally transforming biomarker analysis by moving beyond simple threshold interpretation to complex pattern recognition. Machine learning models, particularly deep learning, are adept at identifying subtle correlations between biomarker concentrations, patient characteristics, and clinical outcomes that are invisible to the human eye or standard statistical methods. This capability is paramount in liquid biopsy, where the concentration of molecular markers (like cfDNA mutations) is often extremely low and requires sophisticated signal processing to differentiate true positives from noise. AI applications are significantly improving the sensitivity of these non-invasive tests, making them more reliable for minimal residual disease (MRD) monitoring and early recurrence detection, which is crucial for managing patient anxiety and ensuring timely therapeutic adjustments.

Furthermore, AI accelerates biomarker research pipelines by processing vast genomic and proteomic datasets generated by Next-Generation Sequencing (NGS) and mass spectrometry platforms. It can swiftly identify optimal biomarker panels, predict their clinical relevance, and guide validation studies, dramatically reducing the drug and diagnostic development cycle. The integration of AI into laboratory information management systems (LIMS) is also optimizing workflow efficiency, reducing human error, and ensuring quality control in high-volume testing environments. The overarching expectation is that AI will standardize and personalize tumor marker utilization, transforming it from a supplementary tool into a central, predictive component of precision oncology.

The Tumor Markers Market is significantly influenced by a confluence of accelerating drivers and persistent restraints, creating a dynamic operational environment. Drivers include the rising global incidence and prevalence of various cancers, which necessitate frequent screening and monitoring, coupled with continuous technological innovation leading to the development of highly sensitive detection assays like digital PCR and multiplex immunoassays. Restraints primarily involve the critical challenges associated with the specificity and sensitivity of many established protein markers, which can lead to high rates of false positives in certain conditions, potentially causing unnecessary patient anxiety and costly follow-up procedures. Opportunities are robustly present in the expansion of non-invasive testing methods, particularly liquid biopsy, and the successful integration of tumor markers into population-wide screening programs for high-mortality cancers, such as lung cancer.

Impact forces currently shaping the market trajectory include technological advancements, which act as a powerful positive force, continually lowering the cost and increasing the throughput of complex genetic and proteomic analyses. Regulatory policies, such as those governing the approval of companion diagnostics and novel IVD devices, exert a moderate impact, demanding rigorous clinical validation before market entry but ensuring the quality and reliability of new assays. Economic forces, driven by increasing healthcare expenditure in emerging economies and favorable reimbursement policies in developed markets, provide sustained financial impetus for market growth. However, ethical considerations regarding the use of genetic markers and patient data privacy also constitute a significant, though indirect, force that mandates responsible market development and stringent data security protocols.

Specific market drivers include the growing adoption of personalized medicine, where specific markers are mandatory for selecting targeted therapies, such as PD-L1 testing for immunotherapy. The increasing elderly population, which is more susceptible to cancer, also contributes significantly to market volume. Conversely, the high cost associated with advanced molecular diagnostics, particularly in resource-constrained settings, acts as a restraint, limiting access and adoption. The opportunity to shift from diagnostic usage towards preventative and surveillance applications, leveraging markers to identify pre-cancerous conditions or detect recurrence earlier than traditional imaging methods, provides compelling avenues for future market expansion and substantial growth.

The Tumor Markers Market is structurally segmented based on product type, cancer type, application, technology, and end-user. This layered segmentation provides a granular view of market dynamics, revealing varying growth rates and adoption patterns across different clinical and technological categories. The segmentation by product type is critical, distinguishing between traditional protein biomarkers and the rapidly evolving molecular biomarkers, which are becoming central to personalized oncology. Cancer type segmentation focuses resources on the largest volume areas, such as breast, prostate, and lung cancer, which benefit most from widespread marker use. Application segmentation is equally important, highlighting the differences in testing requirements for diagnosis versus continuous monitoring of therapeutic response, with the latter showing accelerated expansion due to improved non-invasive methods.

The product segmentation currently favors protein biomarkers due to their long-established use and lower cost, but molecular markers, encompassing genetic and epigenetic markers, are gaining significant traction due to their high predictive and prognostic value. Within technology, the market is shifting from older, manual immunoassays towards automated, high-throughput platforms like CLIA and ELISA, and increasingly towards sophisticated platforms such as PCR and NGS for molecular analysis. The dominant application remains monitoring treatment efficacy and disease recurrence, driven by the shift towards treating cancer as a chronic disease requiring continuous surveillance. Geographically, while North America leads in value, the burgeoning patient population and infrastructural improvements in Asia Pacific are paving the way for substantial volumetric growth and regional diversification in market demand.

The value chain for the Tumor Markers Market is intricate, beginning with extensive upstream research and development (R&D) focused on biomarker discovery, validation, and assay development. Upstream activities involve academic institutions, biotech startups, and large diagnostic firms investing heavily in genomics, proteomics, and bioinformatics to identify clinically relevant markers. This stage is highly capital-intensive and requires specialized expertise in molecular biology and assay design to transition a newly discovered molecule into a clinically reliable test kit. The quality and intellectual property surrounding the initial marker discovery significantly dictate the subsequent success and profitability downstream.

The midstream phase focuses on manufacturing and production, where validated assays are scaled up for commercial use. This involves the production of reagents, antibodies, and the integration of these components into automated diagnostic platforms (instruments). Key players in this phase focus on achieving high standardization, quality control, and obtaining necessary regulatory approvals (e.g., FDA, CE Mark). The integration of complex technologies, such as NGS platforms or automated immunoassay analyzers, necessitates strong partnerships between reagent suppliers and instrument manufacturers to ensure seamless clinical utility. Efficiency in this phase directly impacts the final cost and accessibility of the diagnostic test.

The downstream component involves distribution and utilization channels. Distribution channels are typically segmented into direct sales forces targeting large hospital networks and reference laboratories, and indirect channels relying on third-party distributors for broader market reach, especially in emerging economies. The end-users—hospitals, diagnostic centers, and research laboratories—are crucial for test utilization, and their adoption is heavily influenced by clinical guidelines, favorable reimbursement rates, and physician education. Effective clinical support and data interpretation services are increasingly important downstream elements, ensuring that complex molecular results are translated into actionable clinical decisions, thus completing the value cycle.

The primary end-users and buyers of tumor marker products are hospitals and large clinical laboratories, forming the backbone of demand due to their high volume of oncology testing and patient management responsibilities. Hospitals rely on these markers for initial screening, differential diagnosis, staging, and particularly for post-treatment surveillance to detect early recurrence. Comprehensive clinical laboratories, often acting as reference centers, purchase high-throughput automated systems and specialized molecular testing kits (NGS and PCR) to serve multiple healthcare providers, valuing efficiency, scalability, and multiplexing capabilities in their procurement decisions.

A rapidly growing segment of potential customers includes specialized cancer research institutes and academic medical centers. These entities utilize tumor markers not only for routine patient care but also extensively in clinical trials to monitor therapeutic efficacy, identify patient subpopulations likely to respond to novel drugs, and contribute to the discovery and validation of next-generation biomarkers. Their purchasing decisions are often guided by the need for cutting-edge technology and high analytical sensitivity suitable for research applications, prioritizing flexibility and customization over sheer throughput often favored by routine clinical labs.

Furthermore, pharmaceutical and biotechnology companies are significant, albeit indirect, consumers of tumor marker diagnostics, particularly in the form of companion diagnostics (CDx). These companies integrate marker testing directly into their drug development pipelines to ensure the right drug is given to the right patient. They often partner with diagnostic developers to co-develop or co-market assays essential for drug selection (e.g., PD-L1, HER2 status). Their demand is highly specific, driven by regulatory requirements for drug approval, making them critical high-value customers focused on regulatory compliance and clinical validity.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $3.5 Billion |

| Market Forecast in 2033 | $7.0 Billion |

| Growth Rate | 10.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Roche Diagnostics, Siemens Healthineers, Abbott Laboratories, Thermo Fisher Scientific, Danaher Corporation (Beckman Coulter), bioMérieux, Bio-Rad Laboratories, Myriad Genetics, Qiagen N.V., Illumina, Inc., Hologic, Inc., Guardant Health, Becton, Dickinson and Company, Agilent Technologies, GE Healthcare, NanoString Technologies, F. Hoffmann-La Roche Ltd. (Ventana Medical Systems), NeoGenomics Laboratories, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Tumor Markers Market is undergoing rapid evolution, moving away from single-analyte testing towards highly sensitive, multiplexed platforms capable of analyzing numerous markers simultaneously. Immunoassays, including Chemiluminescence Immunoassays (CLIA) and Enzyme-Linked Immunosorbent Assays (ELISA), remain foundational for quantifying established protein markers due to their high throughput and automation capabilities, making them standard practice in clinical labs globally. However, the future is increasingly dominated by technologies offering superior precision and molecular-level detail, necessitated by the shift towards precision oncology and the need to detect extremely low concentrations of molecular targets.

Crucially, Next-Generation Sequencing (NGS) and Polymerase Chain Reaction (PCR), especially digital PCR (dPCR), are defining the molecular segment. NGS allows for the comprehensive analysis of genomic alterations, including mutations, gene fusions, and copy number variations, particularly in circulating tumor DNA (ctDNA) derived from liquid biopsies. dPCR offers unparalleled sensitivity for monitoring minimal residual disease (MRD) by accurately quantifying ultra-low concentrations of specific genetic markers in blood, proving vital for patient surveillance post-treatment. These molecular methods provide the high specificity required to differentiate malignant lesions from benign conditions, addressing a key limitation of traditional markers.

Furthermore, Mass Spectrometry (MS) is emerging as a powerful tool in proteomics for discovering and validating novel protein biomarkers with improved accuracy over antibody-based methods, especially in complex biological matrices. The integration of bioinformatics and artificial intelligence with these high-output technologies is the next major leap. AI algorithms process the complex datasets generated by NGS and MS, identifying clinically relevant patterns and assisting in the assembly of robust multianalyte panels, thus transforming raw data into actionable clinical insights. This technological convergence is central to the viability of future tumor marker applications, particularly in preventative and early diagnosis settings.

Protein tumor markers (e.g., PSA, CEA) are typically used for routine monitoring and recurrence detection, measuring protein levels in blood. Molecular tumor markers (e.g., ctDNA, gene mutations) analyze genetic material, offering higher specificity for targeted therapy selection and predicting patient response, forming the core of precision oncology.

Liquid biopsy allows for non-invasive sampling of circulating tumor cells (CTCs) and cell-free DNA (cfDNA) from a simple blood draw. This reduces the need for costly and invasive tissue biopsies, enabling frequent and continuous monitoring of disease progression, treatment response, and early detection of cancer recurrence with high sensitivity.

The main challenges are the lack of perfect sensitivity and specificity of many traditional markers, which can lead to high rates of false positives or negatives. This complexity necessitates careful interpretation and restricts the use of many markers to monitoring disease rather than definitive, standalone diagnosis in asymptomatic populations.

The application segment focused on Monitoring and Recurrence Detection is experiencing the fastest growth. This is driven by the rise of chronic cancer management models, advancements in sensitive liquid biopsy techniques, and the recognized need for continuous, non-invasive surveillance post-surgery or chemotherapy.

AI, specifically machine learning, integrates complex multimodal data (genomics, proteomics, clinical) generated by multianalyte panels. It identifies subtle patterns and correlations that predict patient outcomes more accurately than single markers, transforming large datasets into precise, actionable insights for personalized treatment planning and prognosis.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.