ID : MRU_ 435239 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

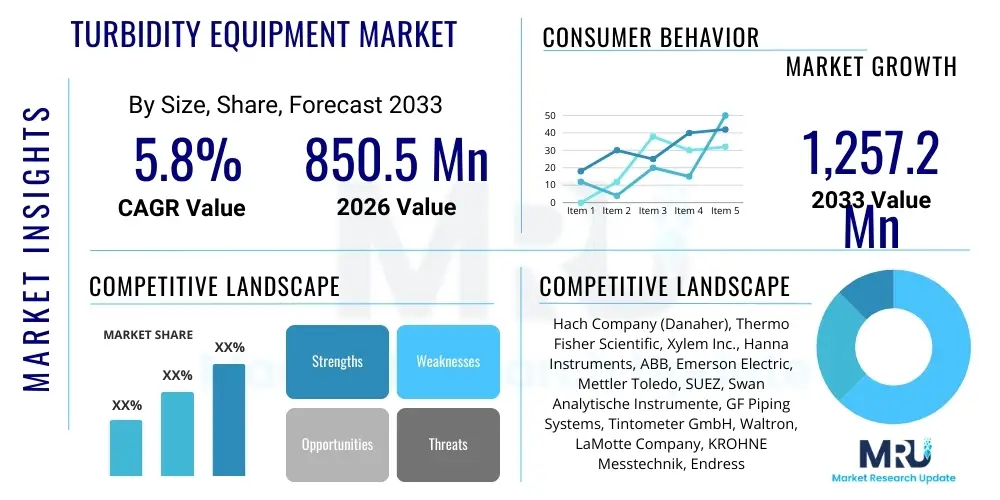

The Turbidity Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 850.5 million in 2026 and is projected to reach USD 1,257.2 million by the end of the forecast period in 2033.

The Turbidity Equipment Market encompasses instruments and systems designed to measure the cloudiness or haziness of a fluid, a critical parameter in assessing water quality. Turbidity is caused by suspended particles, ranging from clay and silt to microorganisms, which scatter light. These measurements are fundamentally important for ensuring compliance with stringent regulatory standards established by bodies like the Environmental Protection Agency (EPA) and the World Health Organization (WHO), particularly in municipal water treatment and environmental monitoring. The primary function of turbidity equipment, which includes turbidimeters and associated probes, is to quantify this characteristic, usually expressed in Nephelometric Turbidity Units (NTU) or Formazin Nephelometric Units (FNU).

The core products within this market range from compact, portable meters used for field testing to sophisticated, inline process turbidimeters integrated directly into industrial control systems. Key applications span across drinking water treatment, wastewater management, industrial process control (such as in brewing, pharmaceuticals, and chemical manufacturing), and environmental assessment of surface waters. The instruments operate based primarily on the principle of nephelometry, measuring the light scattered by particles at a 90-degree angle to the incident light beam, offering high sensitivity and reliability in monitoring particle suspension levels that could indicate contamination or filtration inefficiencies.

The market growth is substantially driven by the increasing global focus on water safety, sanitation infrastructure development in emerging economies, and the continuous tightening of effluent discharge regulations across developed nations. Furthermore, the rising adoption of continuous monitoring systems in critical sectors like power generation and food and beverage manufacturing, where product quality is directly tied to water clarity, fuels the demand for advanced and highly precise turbidity measurement solutions. The benefits delivered by these systems include proactive identification of filtration failures, optimization of chemical dosing (e.g., coagulants), and overall improvement in operational efficiency and regulatory adherence, making them indispensable tools in modern water management.

The Turbidity Equipment Market is poised for robust expansion, driven primarily by tightening global regulatory frameworks and the rapid modernization of water and wastewater infrastructure, particularly across Asia Pacific and Latin America. Business trends show a distinct pivot towards smart, connected devices capable of real-time data logging and remote diagnostics, enhancing operational efficiency for end-users. Manufacturers are increasingly focusing on developing multi-parameter probes that integrate turbidity measurement with other essential parameters like pH, conductivity, and dissolved oxygen, offering comprehensive water quality solutions. Strategic acquisitions and collaborations aimed at integrating digital platforms and IoT capabilities into traditional instrumentation remain a key competitive element among leading market players, ensuring instruments are compliant with ISO 7027 and EPA methods.

Regionally, Asia Pacific (APAC) stands out as the fastest-growing market, largely attributed to massive government investments in municipal water treatment projects, necessitated by rapid urbanization and industrial expansion, particularly in China and India. North America and Europe, while mature, maintain dominance in terms of adopting advanced, high-precision equipment due to stringent regulatory enforcement and high adoption rates in industrial applications such as pharmaceutical production and power generation. Segment trends indicate that the inline/process turbidimeters segment is gaining significant momentum over benchtop and portable devices, reflecting the shift towards continuous, automated monitoring processes in large-scale industrial and utility operations. Technology wise, nephelometric sensors remain the standard, but there is growing interest in non-contact and optical density measurement technologies for specific high-turbidity applications.

The market's structural evolution is characterized by strong demand from the public utilities sector, which remains the largest application segment, followed closely by the food and beverage industry where clear water is paramount for product integrity. Restraints, such as the high initial cost of advanced inline systems and the frequent need for calibration and maintenance, pose moderate challenges. However, opportunities in developing affordable, low-maintenance sensors based on solid-state technology, coupled with the increasing integration of cloud-based data management, are expected to mitigate these drawbacks and accelerate market penetration globally. Overall, the market outlook is overwhelmingly positive, reflecting the foundational role of turbidity monitoring in safeguarding public health and ensuring industrial quality control.

Users frequently inquire about how Artificial Intelligence (AI) and Machine Learning (ML) can move turbidity monitoring beyond simple measurement into predictive analytics, asking questions such as, "Can AI predict filter failure based on turbidity fluctuations?" and "How can ML automate the calibration process to reduce downtime?" The primary themes revolve around enhancing reliability, reducing maintenance costs, and enabling proactive decision-making. Users seek sophisticated algorithms that can differentiate between routine turbidity shifts and those signaling acute operational failures, thereby optimizing chemical dosing (coagulation and flocculation) based on real-time raw water characteristics rather than fixed schedules. This interest underscores a shift from reactive monitoring to integrated, intelligent water quality management systems, aiming for optimal resource utilization and improved compliance assurance.

The Turbidity Equipment Market is primarily propelled by stringent global regulations concerning drinking water quality and effluent discharge standards, alongside the burgeoning demand for reliable industrial process control in sectors like pharmaceuticals and F&B. Key drivers include government mandates requiring continuous water quality assessment and significant infrastructure spending in emerging nations focused on expanding access to treated water. These drivers create a compelling and non-negotiable demand base for highly accurate and certified equipment. However, the market faces restraints such as the relatively high initial capital investment required for installing advanced, multi-parameter inline monitoring systems, particularly for smaller utility providers or remote installations. Furthermore, the inherent need for frequent calibration using standardized formamide polymers and the maintenance demands associated with fouling and drift in sensor performance act as limiting factors, affecting the total cost of ownership over the equipment lifespan.

Opportunities for market growth lie predominantly in the development and adoption of smart, self-cleaning, and low-maintenance sensor technology, which addresses the calibration and fouling restraints. Integrating Turbidity Equipment with the Internet of Things (IoT) platforms allows for remote diagnostics, real-time data integration into Supervisory Control and Data Acquisition (SCADA) systems, and enhanced operational efficiency through cloud-based analytics. The expansion of continuous emission monitoring systems (CEMS) in heavy industries and the increasing global emphasis on monitoring microplastics in water bodies also represent significant future market avenues, requiring specialized, high-sensitivity turbidimeters capable of detecting ultra-low levels of particulate matter.

The impact forces shaping this market are substantial. Regulatory stringency acts as a high-impact driver, compelling rapid compliance and technology upgrades, especially following major water quality incidents. Conversely, technological innovation in sensor design (e.g., solid-state sensors eliminating moving parts) is a high-impact opportunity, disrupting older equipment models by offering lower operational costs and greater reliability. The competitive pressure focuses intensely on accuracy, ease of use, and compliance certifications (e.g., meeting both ISO and EPA methods simultaneously). Overall, the demand is inelastic due to the critical nature of the application in public health and industrial safety, meaning regulatory mandates tend to override minor cost restraints, keeping market growth consistent and steady.

The Turbidity Equipment Market is systematically segmented based on Product Type, Technology, Application, and End-User. This granular categorization allows for tailored analysis of demand patterns and technological maturity across various market subsets. The segmentation by Product Type, differentiating between inline, benchtop, and portable devices, reflects the operational needs—from continuous process monitoring to laboratory verification and mobile field testing. Technology segmentation highlights the primary measurement methodologies employed, predominantly focusing on nephelometry (90° light scattering) which dominates the high-accuracy measurement segment, and other techniques like turbidimetry (attenuation measurement) used in high-turbidity environments.

Application analysis provides insight into the major uses of the equipment, with drinking water and wastewater treatment consistently being the largest segments due to mandatory regulatory oversight. Industrial applications such as food and beverage, pharmaceuticals, and power generation represent high-value niches demanding specialized, high-purity measurement capabilities. Furthermore, the End-User segmentation breaks down the market demand source, dominated by municipal water treatment plants and government environmental agencies, followed by private industrial entities requiring quality control instruments.

The value chain for the Turbidity Equipment Market begins with the sourcing of essential raw materials, primarily focusing on optical components such as high-precision lenses, photodetectors, light sources (LEDs or lasers), and housing materials like rugged polymers and stainless steel suitable for harsh aquatic environments. The upstream activities involve the manufacturing and precision calibration of these specialized optical and electronic components. Key suppliers are often high-tech optics firms and specialized electronics manufacturers, ensuring the core functionality of measuring light scatter accurately. Ensuring the quality and stability of the light source and detector sensitivity is paramount in this stage, directly impacting the final instrument's accuracy (measured in NTU).

The midstream process is centered on the assembly, software integration, and stringent calibration of the final turbidimeter unit. Manufacturers integrate sensors with microprocessors for data logging, self-diagnostics, and connectivity features (e.g., 4-20 mA output, Modbus, Wi-Fi). Quality assurance and mandatory certification processes (EPA or ISO compliance) form a critical bottleneck in the manufacturing stage, requiring rigorous testing. Distribution channels are typically bifurcated: direct sales channels handle large municipal or industrial contracts requiring installation support and technical training, while indirect channels utilize specialized water quality distributors and scientific equipment retailers for smaller orders, portable devices, and laboratory instruments.

Downstream activities focus heavily on installation, regular maintenance, and the supply of consumable accessories, notably calibration standards (Formazin) and cleaning solutions. Service providers play a crucial role in ensuring the continuous reliability and regulatory compliance of inline process turbidimeters, often offering service contracts that include periodic verification and recalibration. Direct engagement with end-users allows manufacturers to gather crucial feedback for product innovation, particularly concerning fouling resistance and sensor durability, closing the loop on the value chain. This ensures that the equipment remains reliable under diverse operational conditions, from clear drinking water to highly contaminated wastewater streams.

Potential customers, or end-users/buyers, of turbidity equipment are diverse yet fundamentally linked by the need to monitor and control water or fluid clarity for health, regulatory compliance, or product quality assurance. The largest volume buyers are Municipal Water Treatment Plants (WTPs) and Wastewater Treatment Facilities (WWTPs), which rely on these instruments continuously to monitor raw water intake, optimize coagulation/filtration processes, and verify final effluent quality before discharge. These entities typically invest in high-volume, automated inline turbidimeters capable of 24/7 operation and integration with SCADA systems to meet strict public health and environmental protection mandates.

The second major category involves industrial manufacturers, particularly those in the Food and Beverage (F&B) and Pharmaceutical sectors. In F&B, turbidity monitoring is vital for maintaining the clarity, texture, and stability of beverages like beer, wine, and juices, and for ensuring water quality used in processing. Pharmaceutical companies utilize high-sensitivity turbidimeters to verify the purity of process water (WFI) and measure particle suspension in formulations, adhering to extremely rigorous pharmacopeia standards. These industrial customers prioritize accuracy, high resolution (especially at low NTU values), and compliance with validation protocols.

Finally, environmental agencies, geological surveys, research institutions, and private environmental consultants constitute the third major customer group. These users primarily utilize portable and benchtop turbidimeters for field sampling, hydrological studies, monitoring sediment transport in rivers and lakes, and conducting regulatory checks. Their requirements emphasize portability, battery life, robust construction for outdoor use, and data logging capabilities to document findings accurately. Continuous demand is also observed from power generation plants (monitoring boiler feedwater quality) and chemical processing facilities (product clarity and quality control).

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 850.5 Million |

| Market Forecast in 2033 | USD 1,257.2 Million |

| Growth Rate | CAGR 5.8% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Hach Company (Danaher), Thermo Fisher Scientific, Xylem Inc., Hanna Instruments, ABB, Emerson Electric, Mettler Toledo, SUEZ, Swan Analytische Instrumente, GF Piping Systems, Tintometer GmbH, Waltron, LaMotte Company, KROHNE Messtechnik, Endress+Hauser, WTW (Xylem Brand), HORIBA, Ltd., YSI (Xylem Brand), Analytical Technology Inc. (ATI), Hach Lange. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Turbidity Equipment Market is defined by continuous advancements focused on improving accuracy, reducing maintenance, and facilitating data connectivity. Nephelometry, based on ISO 7027 standards (using an infrared light source at 860 nm) and EPA Method 180.1 (white light), remains the foundational technology, providing the highest sensitivity for low-turbidity measurements crucial in drinking water monitoring. Recent innovations emphasize solid-state technology, transitioning from traditional tungsten filament lamps to highly stable LEDs and lasers. This shift drastically improves light source longevity, reduces power consumption, and minimizes heat-induced drift, leading to longer intervals between calibrations and greater overall instrument reliability in continuous monitoring environments.

A significant trend involves the development of self-cleaning sensors and non-contact measurement techniques. Fouling—the accumulation of biological or particulate matter on the sensor windows—is the primary cause of measurement drift and maintenance requirements. Manufacturers are addressing this through integrated wiper systems, ultrasonic cleaning mechanisms, and advanced materials designed to resist biofouling. Non-contact technologies, often utilizing laser scattering or sophisticated fluidics to measure samples without direct sensor immersion, are emerging in specialized high-purity applications, though inline contact probes remain the industry standard for robust environmental monitoring.

Furthermore, the incorporation of advanced digital communication protocols and smart sensor technology is transforming data handling. Modern turbidimeters are increasingly equipped with digital outputs (e.g., Modbus, HART) that enable seamless integration into industrial automation systems and facilitate remote monitoring via IoT platforms. Multi-sensor probes, capable of simultaneously measuring turbidity, temperature, pH, and dissolved oxygen, are also becoming standard, offering comprehensive water quality data from a single device. This technological integration is crucial for maximizing operational efficiency and supporting the complex data requirements of modern smart water utilities.

The regional dynamics of the Turbidity Equipment Market exhibit significant variations based on regulatory strictness, infrastructural maturity, and industrial concentration. North America, particularly the United States, commands a substantial market share, primarily driven by the extremely stringent enforcement of the Safe Drinking Water Act (SDWA) by the EPA, necessitating highly accurate and regularly certified monitoring equipment across all municipal water sources. High industrialization, particularly in the food and beverage and chemical sectors, also contributes to sustained demand for high-end, dedicated process control turbidimeters. The market here is characterized by early adoption of sophisticated digital and IoT-enabled solutions, and high expenditure on replacement and modernization of existing monitoring infrastructure.

Europe represents another mature, high-value market segment. Growth in this region is primarily fueled by the European Union's directives on environmental protection and wastewater discharge, which impose rigorous quality standards on industrial effluents. Western European nations demonstrate high demand for integrated monitoring solutions, often utilizing multi-parameter probes in alignment with the Water Framework Directive (WFD). While market penetration is high, the focus is shifting towards innovation in low-maintenance, sustainable sensor technologies and instruments designed for ultra-low turbidity measurement in bottled water and pharmaceutical production, maintaining premium pricing.

Asia Pacific (APAC) is projected to be the fastest-growing region during the forecast period. This rapid expansion is a direct result of massive urbanization, rapid industrial development, and subsequent governmental investments in building and expanding municipal water and wastewater treatment capabilities in countries like China, India, and Southeast Asian nations. While the initial focus was on basic, cost-effective equipment, the increasing pressure to address high pollution levels is driving demand for more advanced inline monitoring systems. This region presents substantial opportunity for both established global players and local manufacturers, focusing on balancing affordability with regulatory compliance requirements, especially regarding industrial effluent monitoring.

The primary driver is the increase in global regulatory mandates, particularly those set by organizations like the EPA and WHO, which require continuous and accurate monitoring of water quality in municipal and industrial settings to protect public health and manage effluent discharge.

EPA Method 180.1 requires the use of white light (tungsten lamp) and measurement at 90 degrees, primarily used in the US. ISO 7027 requires the use of infrared light (860 nm) at 90 degrees, offering better compensation for color and preferred globally, particularly in Europe, for measuring non-colored water samples.

The Inline/Process Turbidimeters segment holds the largest market share. This is due to the rising industry demand for continuous, real-time monitoring of fluid clarity within industrial control systems and large-scale municipal water treatment plants.

AI significantly reduces maintenance needs by using predictive analytics to forecast sensor fouling or drift, optimizing calibration schedules, and automatically correcting minor data variances, thus improving the overall uptime and accuracy of the monitoring systems.

Major non-utility applications include quality control in the Food and Beverage industry (especially brewing and juice clarification), monitoring process water purity in Pharmaceutical manufacturing, and measuring suspended solids and sediment in environmental surveys and hydrological research.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.