ID : MRU_ 437023 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

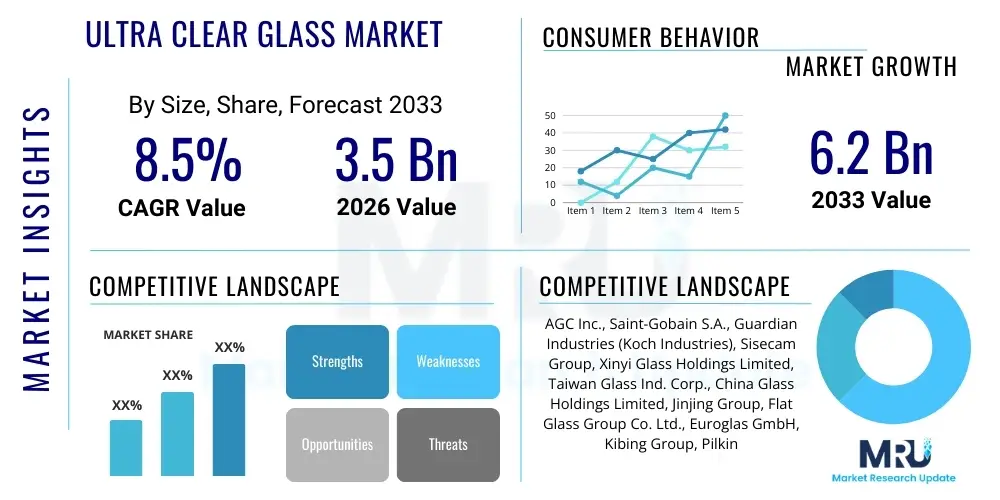

The Ultra Clear Glass Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 3.5 Billion in 2026 and is projected to reach USD 6.2 Billion by the end of the forecast period in 2033. This substantial growth is primarily driven by the increasing global demand for high-performance building materials, particularly in large-scale architectural projects, solar energy installations, and premium electronic displays where superior light transmission and color neutrality are paramount. Market expansion is further supported by technological advancements in float glass production, minimizing iron content and thus maximizing clarity, a critical factor for efficiency in photovoltaic systems and aesthetic appeal in modern structures.

The Ultra Clear Glass Market encompasses the production and distribution of specialized low-iron content glass characterized by exceptional light transparency, minimal greenish tint, and high solar energy transmittance. This product, also commonly referred to as extra-clear glass or low-iron glass, achieves superior optical clarity due to the reduced presence of ferrous oxide (iron) compared to standard clear float glass, leading to a visible light transmission (VLT) typically exceeding 91% for standard thicknesses. The manufacturing process involves selecting raw materials with extremely low iron impurities and often incorporating advanced refining techniques during the melting phase to ensure optimal optical performance. Ultra clear glass is essential in applications where both maximizing solar gain and achieving true color representation are necessary, thereby positioning it as a premium material in various high-specification industries globally.

Major applications of ultra clear glass span across several high-growth sectors. In architecture, it is extensively used for facades, skylights, interior partitions, and display cases, enhancing natural light ingress and providing an uncompromised aesthetic view. The solar energy sector represents perhaps the most critical application, where low-iron photovoltaic glass serves as the front sheet in solar modules (both crystalline silicon and thin-film technologies), minimizing reflectance and maximizing the absorption of sunlight to boost overall panel efficiency. Furthermore, it is integral in the production of high-definition electronic displays, museum exhibit enclosures, specialized laboratory equipment, and high-end automotive windows, where visual precision is non-negotiable. The inherent benefits of ultra clear glass—including UV resistance, high durability, and enhanced aesthetics—drive its increasing adoption across global markets, substituting traditional glass products in premium installations.

The driving factors propelling the market include stringent regulatory requirements encouraging energy efficiency in building codes, the global push towards renewable energy targets necessitating high-efficiency solar panels, and the burgeoning construction industry focused on luxurious, transparent designs. Furthermore, the rise in consumer demand for high-quality, vibrant electronic displays, such as those used in smartphones, tablets, and large-format digital signage, significantly contributes to market buoyancy. Continuous research and development focused on optimizing thickness while maintaining structural integrity and clarity, alongside improvements in coating technologies (such as anti-reflective and self-cleaning coatings), ensure that ultra clear glass remains a vital and expanding component of modern industrial and architectural landscapes.

The Ultra Clear Glass Market is undergoing robust growth, predominantly fueled by sustainable energy initiatives and upscale architectural developments across key global regions. Business trends indicate a strong move toward integration, where major glass manufacturers are expanding their product portfolios to include specialized coatings—such as low-emissivity (Low-E) and anti-reflective (AR) treatments—applied directly to low-iron substrates, thereby offering multi-functional, high-value solutions to end-users. Strategic partnerships between glass producers and photovoltaic module assemblers are becoming more common, securing long-term supply agreements critical for the scaling of solar power projects. Furthermore, advancements in robotic handling and automated cutting systems are optimizing production efficiency and reducing waste, supporting competitive pricing despite the premium nature of the product. Innovation in thin-film technologies also creates new demands for lighter, yet equally clear, glass substrates for portable electronics and specialized glazing applications.

Regionally, Asia Pacific (APAC) stands out as the dominant market, largely driven by massive investments in solar farms, particularly in China and India, and rapid urbanization leading to extensive commercial and residential construction utilizing modern architectural glass. North America and Europe follow closely, propelled by strict energy efficiency mandates and a high adoption rate of Building Integrated Photovoltaics (BIPV). European markets emphasize high-specification architectural glass for historical preservation and aesthetic enhancements, while North America focuses heavily on large-scale solar utility projects and high-end residential construction. Emerging markets in Latin America and the Middle East and Africa (MEA) are also showing promising growth, albeit from a smaller base, primarily due to infrastructure development and nascent solar energy adoption programs, particularly in arid regions where superior light transmission is highly beneficial.

Segmentation trends highlight the Solar Glass segment's rapid acceleration, reflecting the global renewable energy transition. Within the product type segmentation, the market observes increasing demand for laminated ultra clear glass, driven by safety and security requirements in architectural applications, providing both high clarity and enhanced structural resilience. In terms of end-use, the construction sector maintains a stable, high-volume demand base, but the growth rate in the photovoltaic (PV) segment is significantly outpacing others, compelling manufacturers to dedicate substantial production capacity towards specialized PV glass. Technological refinement continues to focus on achieving higher clarity (VLT > 92%) across varying thicknesses, ensuring that product performance meets the increasingly demanding specifications of high-efficiency solar cell technologies, such as Heterojunction Technology (HJT) and PERC solar cells, which require minimum light loss.

Users frequently inquire about how Artificial Intelligence (AI) can optimize the notoriously energy-intensive and precise manufacturing processes of ultra clear glass, focusing on questions like predictive maintenance for high-temperature float lines, real-time defect detection, and optimization of raw material input ratios to consistently maintain low iron content. Key themes emerging from user concerns center on operational efficiency, quality control, and supply chain responsiveness. Users anticipate that AI-driven quality assurance systems will significantly reduce waste associated with inconsistent clarity or microscopic blemishes, which are unacceptable in photovoltaic or premium display applications. There is also strong interest in how AI algorithms can model complex thermal dynamics within the glass furnace to minimize energy consumption and stabilize the melting process, a crucial factor given the high environmental standards increasingly imposed on industrial manufacturing. The expectation is that AI integration will lead to more uniform product quality, faster reaction times to process deviations, and a more sustainable production footprint for low-iron glass.

AI's influence extends beyond the factory floor into market forecasting and material management. Specifically, AI-driven demand prediction models are crucial for ultra clear glass manufacturers, allowing them to accurately gauge future needs from the volatile solar energy sector and the cyclical construction industry. By analyzing macroeconomic indicators, government policy changes regarding solar subsidies, and real-time project schedules, AI systems can optimize inventory levels of specialty raw materials, ensuring continuous operation without overstocking expensive low-iron sands. Furthermore, AI is beginning to be deployed in sophisticated design software used by architects and engineers, assisting in material selection and performance simulation for complex glazed structures, enabling optimal placement and usage of high-clarity glass to maximize daylighting and energy performance in buildings, thus indirectly accelerating market adoption.

The implementation of machine learning in product development is also a nascent yet powerful area. Researchers are utilizing AI to simulate and rapidly test new chemical compositions and coating formulations aimed at enhancing light transmission further, improving anti-reflection properties, or adding self-cleaning capabilities without compromising the base glass clarity. This AI-guided materials science accelerates the innovation cycle, allowing companies to quickly bring next-generation ultra clear products to market that address evolving customer needs, such as improved durability against environmental stresses or specialized optical filtering characteristics required for augmented reality (AR) displays. The cumulative effect of AI is a shift towards a smarter, more efficient, and hyper-responsive manufacturing ecosystem for ultra clear glass.

The dynamics of the Ultra Clear Glass Market are shaped by a complex interplay of driving forces, inherent restraints, and compelling opportunities, all subject to significant impact forces stemming from global economic trends, environmental policies, and technological progression. The principal driver is the surging global commitment to renewable energy, making high-efficiency solar glass indispensable for photovoltaic modules. This demand is reinforced by governmental subsidies and regulatory frameworks promoting green construction and low-carbon infrastructure. Simultaneously, restraints such as the high initial cost of production—stemming from the need for high-purity raw materials and specialized manufacturing processes—and the volatility of raw material prices (e.g., soda ash, silica sand) can slow market adoption, especially in price-sensitive developing economies. Opportunities largely revolve around developing multi-functional glass (combining ultra-clarity with features like self-cleaning or dynamic dimming) and expanding into emerging applications such as advanced glazing for electric vehicle sunroofs and specialized screens. These market forces determine the strategic direction for manufacturers and influence investment decisions in capacity expansion and technological upgrading.

Drivers: The most significant driver remains the exponential growth of the solar energy industry, where even a slight improvement in light transmission translates directly into higher energy yield and better Return on Investment (ROI) for solar farms. Government incentives globally, such as feed-in tariffs and tax credits for solar installations, create a sustained high-volume demand base for high-quality, low-iron PV glass. Furthermore, the modern architectural trend favoring floor-to-ceiling glass facades, large structural glass elements, and minimalist interior designs, requires the superior optical performance of ultra clear glass to maximize aesthetic appeal and natural light penetration in commercial and high-end residential buildings, improving occupant well-being and reducing reliance on artificial lighting during the day. This architectural preference, coupled with the need for enhanced safety in public spaces, boosts demand for ultra clear tempered and laminated glass products, often meeting strict safety glazing codes in urban environments.

Restraints: The primary constraint is the technical complexity and capital expenditure required to establish and operate dedicated low-iron float glass production lines. Achieving extremely low iron content requires meticulous sourcing and stringent quality control of raw materials, increasing input costs significantly compared to standard glass. Moreover, the ultra clear glass market is susceptible to supply chain bottlenecks, particularly concerning high-ppurity silica sand, leading to fluctuating production costs and impacting profit margins. A further restraint involves the competitive substitution threat from standard clear glass in less demanding or cost-conscious applications, alongside the nascent challenge posed by lighter, flexible materials that could potentially replace glass in certain portable electronic or specialized thin-film solar applications, although glass still maintains superior durability and scratch resistance. Finally, the energy intensity of glass melting processes contributes to high operating costs, putting pressure on manufacturers to integrate energy-efficient technologies to remain competitive and meet sustainability targets.

Opportunities: Significant market opportunities lie in the continuous innovation of value-added functionalities integrated with ultra clear substrates. The development of self-cleaning (photocatalytic) and anti-reflective coatings applied to low-iron glass broadens its appeal for outdoor applications like solar panels and challenging architectural installations. The expanding Electric Vehicle (EV) market presents a new frontier, particularly for specialized low-iron glazing used in panoramic roofs, enhancing interior lighting while maintaining thermal performance. Furthermore, the rising demand for sophisticated optical components, high-resolution augmented reality (AR) displays, and specialized laboratory enclosures creates niche, high-margin opportunities. Geographically, untapped potential exists in rapidly industrializing regions of Southeast Asia and Africa where large-scale infrastructure projects and emerging commitments to solar energy are poised to accelerate adoption, provided local supply chains can be established efficiently to mitigate logistics costs.

The Ultra Clear Glass market is highly segmented based on critical parameters including Product Type, End-Use Application, Thickness, and Manufacturing Process, reflecting the diverse technical requirements across different industries. Product Type segmentation primarily distinguishes between Tempered, Laminated, and Standard Float ultra clear glass, each offering varying degrees of safety, structural integrity, and application suitability. The End-Use Application segment is the most crucial driver of volume, encompassing the highly active Photovoltaic sector, the expansive Construction (Architectural) sector, and niche markets like Furniture & Decor and Electronics. Understanding these segments allows manufacturers to tailor production capabilities and specialized coatings to meet precise industry standards, such as the high solar transmittance required for PV panels versus the high safety required for laminated architectural facades. Market dynamics within these segments are defined by regulatory environment, material costs, and technological maturity of the respective end-use industries.

Thickness segmentation is critical, ranging from thin glass (under 3.2 mm, often used in electronics and specialized PV panels) to thick glass (over 10 mm, used in structural glazing and large aquariums), as clarity requirements often become more challenging with increasing thickness due to greater material mass. Manufacturing Process segmentation, though less frequently tracked by end-users, is vital for producers, differentiating between the specialized Low-Iron Float Process and specialized rolling or drawing techniques, which impact the final size, flatness, and optical homogeneity of the ultra clear substrate. The growth trajectory for each segment is often asymmetric; while Construction provides stability, the PV segment exhibits significantly higher volatility and rapid growth tied directly to global renewable energy policies and cost reductions in solar technology, necessitating flexible production planning by leading glass manufacturers to capitalize on cyclical peaks in demand.

The value chain for the Ultra Clear Glass market is structured around specialized processes designed to maintain extremely high purity, starting from raw material extraction through to installation and final usage. Upstream analysis focuses heavily on the procurement of low-iron silica sand and other critical components such as soda ash, dolomite, and limestone, which must meet stringent purity standards significantly higher than those required for standard float glass. The necessity for high-grade, often imported, raw materials introduces a complexity in logistics and cost that is foundational to the premium pricing of the final product. Key activities at this stage include mineral processing, beneficiation, and quality verification to ensure iron content is minimized before entering the manufacturing phase. Strategic long-term contracts with specialized mineral suppliers are crucial for manufacturers to maintain supply consistency and quality control.

Downstream analysis centers on transformation processes such as specialized float line production, which utilizes advanced melting and annealing stages to produce the flawless low-iron glass substrate, followed by secondary processing (tempering, laminating, cutting, edging, and coating). Distribution channels are highly specialized; the primary path involves direct sales to large-scale photovoltaic module manufacturers, ensuring just-in-time delivery for high-volume solar projects. Indirect channels include sales through specialized glass processors, distributors, and architectural glazing contractors, who handle customization, installation, and integration into building projects. The distribution network must be capable of handling large, fragile, high-value sheets, often requiring specialized logistics and handling equipment to prevent damage during transit to remote construction or solar farm sites globally. The efficiency of this downstream network directly impacts project timelines and overall cost to the end-user.

The distribution methodology frequently employs both direct sales and specialized intermediary channels. Direct sales are preferred for large Original Equipment Manufacturers (OEMs) in the solar and electronics sectors, facilitating tighter quality control and specifications alignment. Indirect distribution via certified processors and glazers is essential for the construction and architectural segments, as these intermediaries provide value-added services such as specialized custom cutting, heat treating, and complex installation, translating the primary sheet glass into a final integrated product. The selection of distribution channel is often dictated by order volume, geographic location, and the complexity of the required secondary fabrication, with advanced coating services often being performed either by the primary manufacturer or by highly specialized third-party processors before final installation.

The primary end-users and buyers of Ultra Clear Glass are concentrated in industries where optical performance and energy efficiency are critical determinants of product success and regulatory compliance. The largest and fastest-growing segment of potential customers comprises Photovoltaic (PV) Module Manufacturers, including leading solar panel assemblers who utilize low-iron glass as the encapsulation front cover to maximize light capture and efficiency for both monocrystalline and polycrystalline cells, as well as those integrating Building Integrated Photovoltaics (BIPV) into architectural elements. These customers are highly sensitive to solar transmittance percentage and durability testing standards (e.g., IEC standards). The second major group involves large-scale Commercial Construction Developers and Architectural Firms that specify premium materials for modern skyscrapers, museums, airports, and high-end residential complexes, prioritizing aesthetic clarity, natural light, and structural safety through the use of laminated and tempered ultra clear products for facades, railings, and interior features.

A significant, though smaller, customer base resides in the Electronics and Display sector, encompassing manufacturers of high-definition digital signage, specialized touchscreens, and advanced industrial displays where color fidelity and scratch resistance are paramount. Furthermore, specialized optical equipment manufacturers, including those producing high-performance lenses, laboratory glassware, and measuring instruments, rely on the superior optical uniformity of low-iron glass. Finally, the Furniture and Interior Design industry serves as a consistent customer base for applications such as high-clarity tabletops, showcases, and glass doors, where the lack of a greenish tint is highly valued for showcasing products or interiors accurately. Each customer segment demands specific product characteristics, driving the need for customized product specifications regarding thickness, surface treatment, and size availability.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 6.2 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | AGC Inc., Saint-Gobain S.A., Guardian Industries (Koch Industries), Sisecam Group, Xinyi Glass Holdings Limited, Taiwan Glass Ind. Corp., China Glass Holdings Limited, Jinjing Group, Flat Glass Group Co. Ltd., Euroglas GmbH, Kibing Group, Pilkington (NSG Group), Schott AG, Qingdao Jinhui Glass Co. Ltd., Vitro Architectural Glass, Vatti Glass, Ipasol Glass, Fuso Glass India Pvt Ltd., Cardinal Glass Industries, and Hunan Sanxing Glass Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Ultra Clear Glass Market is primarily defined by continuous advancements in the float glass manufacturing process aimed at reducing ferrous oxide content to minuscule levels, typically below 0.01%, which is significantly lower than the standard 0.1% to 0.3% found in conventional glass. Key technological efforts focus on optimizing the raw material selection, employing high-purity silica sand (often requiring magnetic separation or acid washing), and utilizing advanced chemical refining agents, such as cerium oxide, during the melting phase to convert any remaining ferrous ions (Fe2+) into the less color-absorbing ferric ions (Fe3+). This precise chemical engineering within the high-temperature melting furnace is critical for achieving the target Visible Light Transmittance (VLT) exceeding 91% and maintaining color neutrality, preventing the characteristic greenish tint associated with high-iron glass. Investment in large-scale, dedicated low-iron float lines that ensure homogeneous distribution of materials and precise temperature control is a fundamental technological requirement for volume production.

Beyond the primary melt technology, secondary processing technologies, particularly advanced coating applications, are rapidly evolving to create high-value ultra clear products. Anti-Reflective (AR) coatings, often applied through sophisticated vacuum deposition techniques like magnetron sputtering, are essential for photovoltaic glass to maximize light capture by reducing surface reflection, sometimes boosting VLT up to 96%. Furthermore, Low-E coatings are integrated onto architectural ultra clear glass to enhance thermal insulation without compromising light ingress, crucial for energy-efficient building envelope design. Another growing area is the adoption of self-cleaning technologies (hydrophilic or hydrophobic surfaces, often titanium dioxide-based), which utilize UV light to break down organic dirt, making ultra clear glass maintenance easier, particularly for inaccessible facades or ground-mounted solar arrays. These coating technologies transform the base material from a simple substrate into a highly engineered, multi-functional component, thereby commanding higher market prices and enabling new applications.

The industry is also leveraging digitalization and automation to enhance quality control and minimize production defects. The use of high-resolution scanning systems and machine learning algorithms (as mentioned in the AI analysis) is now standard practice for detecting microscopic flaws, bubbles, or inclusions that would degrade optical performance in high-specification uses. Furthermore, manufacturing technology is focusing on optimizing the production of thinner, lighter ultra clear glass (down to 2.0 mm or less) while maintaining high structural integrity, achieved through precise annealing and tempering processes. This thinner glass is particularly vital for BIPV applications and lightweight solar modules intended for installation on low-load-bearing roofs. Overall, the technological focus remains dual-pronged: refining the core chemistry for purity and advancing surface engineering for added functionality and performance customization.

The regional market analysis reveals distinct consumption patterns and growth drivers influenced by local regulatory frameworks and energy policies. Asia Pacific (APAC) currently dominates the global Ultra Clear Glass Market, primarily due to the colossal scale of solar photovoltaic installations, particularly in China, which leads both manufacturing capacity and deployment. Countries like India, Japan, and South Korea are also significantly contributing through large-scale infrastructure projects and supportive government policies aimed at increasing renewable energy adoption. The rapid urbanization and high-density architectural developments in major metropolitan areas throughout the region demand premium, high-clarity glazing for aesthetic and energy performance reasons. This robust demand across both PV and construction sectors establishes APAC as the pivotal market for current volume and future growth potential, necessitating massive, localized manufacturing capacity.

North America, particularly the United States and Canada, represents a mature market characterized by stringent energy efficiency building codes and high investment in utility-scale solar farms. The demand here is driven by high-specification requirements, including the use of highly durable, tempered, and laminated ultra clear glass for hurricane-prone coastal regions and for meeting LEED certification standards in commercial buildings. The market exhibits a strong preference for domestically manufactured or high-quality imported products that comply with specific regional safety standards. The substantial solar pipeline, particularly in states like California and Texas, ensures consistent, high-volume demand for low-iron PV glass, even as local manufacturers face competitive pressure from large-scale Asian suppliers.

Europe maintains a strong, technology-driven market position, heavily influenced by ambitious EU energy efficiency directives (e.g., nearly zero-energy buildings targets) and strong environmental consciousness. While less focused on utility-scale PV than APAC, the European market excels in high-value, niche applications, including BIPV, specialized heritage building glazing, and sophisticated interior design, which demand ultra clear glass integrated with advanced Low-E and dynamic coatings. Germany, France, and the UK are key consumers, where architectural quality and sustainability certifications are paramount. The Middle East and Africa (MEA) and Latin America represent emerging high-potential markets. MEA growth is spurred by large-scale giga-projects (like those in Saudi Arabia and UAE) focusing on modern, reflective architecture and substantial solar energy investments, requiring glass capable of performing optimally in high-temperature, dusty environments. Latin America’s market growth is slower but steady, supported by infrastructure development and increasing adoption of solar power in countries like Brazil and Chile.

The primary difference lies in the iron oxide content. Standard clear glass typically contains 0.1% to 0.3% iron oxide, which imparts a noticeable greenish tint, particularly when viewed on the edge, and absorbs a portion of the incoming solar radiation (light transmission approximately 83-90%). Ultra clear glass, or low-iron glass, reduces this content drastically, often below 0.01%, eliminating the greenish hue and dramatically increasing the Visible Light Transmittance (VLT) to over 91% for standard thicknesses. This superior clarity is critical for the solar energy sector because maximizing light capture directly translates to higher Photovoltaic (PV) module efficiency and increased energy output (kilowatt-hours generated), improving the overall economic viability and performance of solar farms. The absence of the greenish tint ensures that maximum solar spectrum light reaches the silicon cells, a fundamental requirement for high-efficiency solar cells like PERC and Heterojunction Technology (HJT).

The Photovoltaic (PV) sector currently drives the highest global volume demand for Ultra Clear Glass. This segment uses the low-iron substrate extensively as the front cover of solar panels to maximize light transmission and protect the sensitive solar cells. The massive scale of utility-scale solar projects and governmental commitments to renewable energy, particularly across the Asia Pacific region, necessitate vast quantities of high-quality PV glass, accounting for the majority of the market's output. Major future growth areas are expected in Building Integrated Photovoltaics (BIPV), where ultra clear glass is integrated directly into building facades, windows, and roofs for power generation. Furthermore, the specialized glazing segment for Electric Vehicles (EVs), particularly panoramic sunroofs requiring high clarity and thermal control, represents a significant, high-value expansion opportunity. The continued refinement of anti-reflective (AR) and self-cleaning coatings tailored for low-iron glass will further enhance market penetration in both solar and architectural applications.

The main technological challenge is maintaining extremely low iron content throughout the entire float glass production process, which demands precise control over raw material sourcing and rigorous furnace chemistry. Low-iron silica sand is expensive and less readily available than standard silica, increasing upstream procurement costs. Furthermore, the specialized melting and refining techniques required to manage remaining iron impurities are energy-intensive, contributing to higher operational expenditure compared to standard glass production. Manufacturers are addressing these high costs through several strategies: leveraging Artificial Intelligence (AI) and machine learning for enhanced process optimization, minimizing energy consumption in the furnace, and implementing advanced automated inspection systems to reduce defects and waste, thereby improving overall production yield. Additionally, vertical integration and securing long-term supply contracts for specialized raw materials help stabilize input costs and ensure quality consistency, making the premium product more economically competitive against traditional alternatives.

Regional regulatory policies significantly influence market adoption by mandating higher performance standards. In Europe, directives focusing on nearly zero-energy buildings (nZEB) and stringent environmental performance require glazing solutions that offer exceptional thermal insulation (Low-E coatings) combined with maximum daylighting, driving the specification of high-clarity, low-iron glass for architectural projects. North America, driven by building codes and certifications like LEED, similarly prioritizes energy efficiency, but also emphasizes structural integrity and safety standards (e.g., impact resistance). Regulations related to renewable energy portfolio standards and solar tax credits in both regions directly stimulate demand for highly efficient PV modules, inherently requiring low-iron glass to maximize energy yield. These regulatory pressures compel architects and developers to choose premium ultra clear products over standard glass, often integrating advanced coatings to meet dual requirements of clarity and thermal performance.

Several emerging niche markets are proving vital for innovation and future revenue growth beyond the traditional solar and construction sectors. The high-end Electronics and Display market is increasingly crucial, requiring ultra clear substrates for large format digital signage, high-definition displays, and specialized medical/laboratory equipment where optical fidelity and absence of color shift are paramount. The Automotive sector presents a rapidly expanding niche, particularly with the proliferation of Electric Vehicles (EVs), which often feature expansive, high-clarity panoramic sunroofs and specialized heads-up display (HUD) systems, demanding thin, light, and durable low-iron glass. Additionally, the increasing complexity of optical systems, including lenses and components for Augmented Reality (AR) and Virtual Reality (VR) devices, requires ultra clear glass with unparalleled homogeneity and purity. These niche applications, while lower in volume than solar, often command significantly higher margins and push the technological boundaries regarding glass thickness, surface treatment, and customized functionality.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.