ID : MRU_ 431750 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

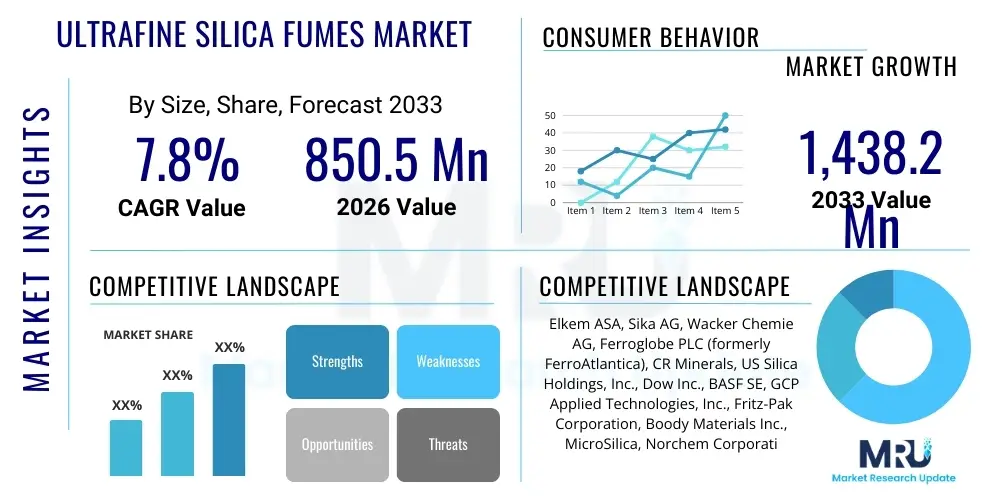

The Ultrafine Silica Fumes Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 850.5 Million in 2026 and is projected to reach USD 1,438.2 Million by the end of the forecast period in 2033. This robust expansion is primarily driven by escalating global infrastructure development, particularly in emerging economies where high-performance concrete (HPC) and ultra-high-performance concrete (UHPC) are becoming standard requirements for long-lasting public works.

The increasing utilization of ultrafine silica fumes, also known as microsilica, in structural engineering applications is critical to this growth trajectory. These materials are essential for enhancing the density, impermeability, and compressive strength of cementitious composites, addressing the demands of seismic resistance and harsh environmental exposure, such as marine structures and chemically aggressive environments. Regulatory push towards sustainable construction practices further favors the adoption of silica fumes, as they are a byproduct of ferrosilicon and silicon production, aligning with circular economy initiatives.

Market valuation reflects a sustained shift towards high-value applications, moving beyond basic concrete additives to specialized uses in refractories, polymers, and elastomers. The advanced material properties offered by ultrafine silica fumes, including their pozzolanic reactivity and filler effect, provide significant performance advantages over traditional mineral admixtures. Investment in manufacturing capacity expansion, especially in the Asia Pacific region, coupled with technological advancements in dispersion and blending, are key factors underpinning the calculated market size and projected growth rates through 2033.

The Ultrafine Silica Fumes Market centers around the production and distribution of amorphous silicon dioxide, an ultrafine, non-crystalline material harvested as a byproduct during the production of silicon and ferrosilicon alloys. This material, characterized by spherical particles averaging less than 0.1 micrometers and a high specific surface area, is predominantly utilized as a high-performance additive in the construction industry. Its primary function is to significantly enhance the mechanical and durability properties of concrete, mortar, and grout, mitigating issues like concrete permeability and alkali-silica reaction (ASR).

Major applications for ultrafine silica fumes span several critical industries. In construction, it is indispensable for developing high-strength concrete used in bridges, skyscrapers, dams, offshore drilling platforms, and road overlays, where durability and strength are paramount. Beyond cement, silica fumes are crucial components in refractory materials, providing increased density, reduced porosity, and enhanced thermal shock resistance necessary for furnace linings and kilns. They also find niche uses in advanced polymers and elastomers, serving as a functional filler to improve tensile strength and abrasion resistance, particularly in specialized coatings and sealants.

The key benefits driving market expansion include superior technical performance, such as achieving compressive strengths exceeding 100 MPa in concrete mixes, and environmental sustainability derived from utilizing an industrial waste stream. Furthermore, the material offers enhanced chemical resistance against chlorides and sulfates. Driving factors for the market involve rapid urbanization and infrastructure renewal projects globally, stringent governmental standards requiring longer life spans for public infrastructure, and continuous research into new application areas, such as specialized repair mortars and high-temperature ceramics, reinforcing its status as a critical performance enhancer.

The Ultrafine Silica Fumes Market is undergoing dynamic transformation driven by macroeconomic business trends, stringent environmental mandates, and technological innovations in material science. The dominant business trend involves significant vertical integration among key players seeking to control the supply chain, from metallurgical processing (source) to specialized additive manufacturing (downstream application). This integration aims to secure consistent supply quality, stabilize highly volatile pricing dependent on silicon production cycles, and accelerate the development of application-specific products, such as slurried or densified silica fumes, which offer easier handling and better dispersion in concrete batching plants.

Regionally, the Asia Pacific (APAC) stands as the primary engine of market growth, fueled by massive government investments in smart cities, high-speed rail networks, and extensive hydropower projects, particularly in China and India. North America and Europe, while mature, exhibit high adoption rates in repair and rehabilitation projects, focusing on highly specialized applications like bridge deck overlays and nuclear power containment structures, adhering to sophisticated engineering specifications. Restraints in developing regions often revolve around logistical challenges associated with transporting bulk, lightweight powder, and the need for greater local awareness regarding proper dosage and mixing techniques to maximize performance benefits.

In terms of segments, the construction industry retains the largest market share due to the indispensable role of silica fumes in high-performance and ultra-high-performance concrete production. However, the refractories segment is demonstrating substantial growth, propelled by increasing global steel and aluminum production requiring high-purity, durable linings. Form-wise, densified silica fume is rapidly gaining preference over undensified powder owing to its substantial reduction in volume, simplifying transportation, storage, and handling, thereby reducing operational costs for end-users and positively influencing procurement trends across all major construction contractors and material suppliers.

User queries regarding AI's influence on the Ultrafine Silica Fumes Market generally revolve around how predictive modeling can optimize concrete mix design, how machine learning can enhance quality control during production, and whether AI can improve supply chain transparency given the material’s status as a byproduct. Key concerns focus on the integration cost of AI systems into traditional batching and material processing plants, and the potential for AI-driven demand forecasting to mitigate the inherent market volatility associated with silicon smelting schedules. Users expect AI to reduce material wastage, achieve more consistent mechanical properties in high-performance concrete, and aid in developing new composite materials faster.

Artificial intelligence is positioned to revolutionize the application and production methodologies within the ultrafine silica fumes sector by enabling highly sophisticated compositional analysis and real-time process control. AI algorithms can ingest vast datasets related to raw material variability, temperature gradients, and particle size distribution during the tapping process in silicon production, allowing producers to proactively adjust parameters to optimize the physical characteristics and purity of the resulting silica fume. This optimization is crucial for ensuring the consistency required by demanding high-specification applications, reducing batch-to-batch variation which is a perennial challenge for performance additives.

Furthermore, in the construction downstream, AI and machine learning are being deployed to optimize concrete mixture proportioning, ensuring the optimal dosage of silica fume based on local climate conditions, specific structural requirements, and the characteristics of locally sourced aggregates and cement. By analyzing historic performance data, AI models can predict long-term concrete durability and strength development more accurately than conventional methods, leading to material savings and improved project reliability. This predictive capacity not only enhances the technical value proposition of silica fumes but also streamlines inventory management for contractors who require just-in-time delivery of specialized additive packages.

The dynamics of the Ultrafine Silica Fumes Market are profoundly shaped by interconnected drivers (D), restraints (R), and opportunities (O), which together constitute the primary impact forces. The core driver is the escalating global need for sustainable, durable, and structurally resilient infrastructure, particularly in high-traffic and aggressive environments where standard concrete fails to meet longevity requirements. This technical imperative pushes demand for performance-enhancing additives. Key restraints include the inconsistent supply, which is inherently tied to the cyclical nature of the silicon and ferrosilicon industries, and the persistent challenge of high transportation and handling costs associated with the material, particularly in its undensified form, creating logistical hurdles for distant end-users.

Opportunities in the market are significant and often tied to technological progression. The development of high-concentration silica fume slurries and specialized pelletized products provides novel avenues to overcome handling and dispersion limitations, broadening adoption in ready-mix concrete sectors. Furthermore, the increasing regulatory emphasis on reducing carbon emissions in construction favors silica fume, as its usage in cementitious materials allows for a substantial reduction in the overall Portland cement content, acting as a viable partial cement replacement and improving the environmental profile of construction projects. These opportunities incentivize continuous product innovation and market penetration into niche applications like specialized geopolymers and high-strength grout materials.

The impact forces exerted on the market emphasize the critical trade-off between technical superiority and supply chain reliability. High technical demand pulls the market forward, while supply constraints and cost volatility push against aggressive growth. The synergistic effect of these forces drives players towards vertical integration and strategic partnerships to secure raw material access and develop localized processing capabilities near major consumption centers. Success in this market increasingly depends on robust logistics networks capable of consistently delivering high-quality, application-specific formulations (e.g., low carbon content for refractories, high purity for specialized polymers), effectively managing the inherent risks associated with a co-product dependent supply model.

The Ultrafine Silica Fumes Market segmentation provides a granular view of market structure, facilitating targeted strategy development based on material form, application, and geographical consumption patterns. The most critical segmentation relies on the physical form of the material, differentiating between undensified (or raw), densified, and slurried forms. This distinction is crucial as it directly affects logistics, storage requirements, and ease of use for the end-user. Densified silica fume, which has undergone compaction to reduce bulk volume, currently dominates the market due to significant savings in transportation and reduced dust generation, appealing strongly to large construction sites and regional distributors.

Application-based segmentation highlights the market dominance of the construction sector, encompassing high-performance and ultra-high-performance concrete used in major infrastructure projects. However, the refractories segment, driven by the global demand for high-temperature lining materials in metallurgy, remains vital, requiring specific low-carbon grades. The third significant segment, polymers and elastomers, focuses on highly specialized industrial applications where silica fume acts as a reinforcing filler, demanding extremely high purity and consistency. Analyzing these segments helps stakeholders understand where future capacity expansion and R&D investment should be focused to capitalize on sectoral growth drivers, such as green refractory technologies or advanced composite materials.

Geographical segmentation reveals stark differences in market maturity and growth potential. Asia Pacific dictates volume growth, driven by extensive foundational construction. Conversely, North America and Europe emphasize value, focusing on rehabilitation, maintenance, and nuclear containment applications requiring certifications and stringent quality assurance protocols. Understanding this multi-dimensional segmentation is paramount for manufacturers to optimize their product portfolio, aligning product form availability (e.g., slurries popular in high-volume European ready-mix plants) with regional logistical capabilities and prevailing regulatory standards.

The value chain for the Ultrafine Silica Fumes Market is distinctive because the material originates as a co-product of the metallurgical silicon and ferrosilicon industries (upstream analysis). The initial, most crucial stage involves the high-temperature electric arc furnace process where silicon metal is produced, capturing the resulting SiO2 vapor in specialized dust collectors. The quality, specifically the carbon content and particle fineness, is inherently determined at this upstream production phase. Companies involved in this stage often exercise significant control over the subsequent availability and base pricing of the silica fume, influencing global market supply dynamics and dictating whether the material meets high-specification refractory or standard concrete grades.

The midstream processing stage focuses on transforming the raw, undensified material into marketable forms suitable for industrial use. This involves crucial steps like separation, blending, densification, and slurrification. Densification is critical for logistical efficiency, converting the extremely low-density powder into a transportable material, thereby adding significant value. Slurrification involves mixing the fume with water and chemical dispersants to create stable, pumpable suspensions, favored by ready-mix concrete operators for precision dosing. Direct distribution channels often involve integrated producers supplying large, strategically located concrete or refractory manufacturers, ensuring rapid, bulk delivery tailored to high-volume projects.

Downstream analysis highlights the end-user application segments (construction, refractories). Indirect distribution channels utilize specialized distributors and regional agents who manage inventory, repackaging, and technical support for smaller or geographically remote customers who require smaller volumes or specialized technical guidance on mix design. The value chain is characterized by a high degree of technical consulting required at the end-user phase, given that optimal performance is highly dependent on correct dosage and application methodology. Therefore, successful market participants offer comprehensive technical support alongside their physical product, enhancing perceived value and securing long-term customer relationships in performance-driven sectors.

Potential customers for ultrafine silica fumes are primarily clustered within the heavy construction, materials manufacturing, and specialized industrial sectors, all of whom seek enhanced material performance and durability that cannot be achieved with conventional additives. The largest consumer base comprises major infrastructure contractors and precast concrete manufacturers who specialize in projects requiring high-strength, low-permeability concrete, such as major bridge decks, high-rise foundations, tunnel linings, and wastewater treatment plants. These buyers prioritize product consistency and reliable, bulk supply, often preferring densified or slurried forms for ease of handling and incorporation into automated batching systems.

Another significant customer segment includes refractory manufacturers, particularly those supplying the steel, aluminum, and glass industries. These end-users require high-purity, low-carbon silica fume grades to produce high-density refractory castables, which offer superior thermal shock resistance and mechanical stability in extremely high-temperature environments. Their procurement decisions are heavily influenced by stringent quality certifications and the material's ability to maintain structural integrity under extreme thermal cycling, making performance reliability a paramount concern over marginal price variations. These relationships are often long-term contracts based on highly specific quality parameters.

In the specialty chemical and oil & gas sectors, potential customers include manufacturers of polymer composites, high-temperature coatings, and specialized oil well cements. Oil and gas companies utilize silica fume in cementing operations to seal boreholes, requiring the material to withstand high pressures and temperatures while ensuring zonal isolation integrity, where its fine particle size and pozzolanic activity are highly beneficial. These diverse potential customers share a common need for a material that transcends the capabilities of ordinary Portland cement or filler materials, thereby commanding a premium for its performance-enhancing attributes across demanding, high-stakes operational environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 850.5 Million |

| Market Forecast in 2033 | USD 1,438.2 Million |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Elkem ASA, Sika AG, Wacker Chemie AG, Ferroglobe PLC (formerly FerroAtlantica), CR Minerals, US Silica Holdings, Inc., Dow Inc., BASF SE, GCP Applied Technologies, Inc., Fritz-Pak Corporation, Boody Materials Inc., MicroSilica, Norchem Corporation, Osthoff Omega Group, RW Silicium GmbH, Saint-Gobain, Momentive Performance Materials, Refratechnik Cement GmbH, Sibelco, Fesil AS. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Ultrafine Silica Fumes Market is primarily defined by advancements in collection, processing, and application methodologies designed to enhance material usability and maintain high-performance standards. Upstream, the core technology remains the high-efficiency filtration and collection systems associated with electric arc furnaces, such as baghouses and electrostatic precipitators, which capture the amorphous silica vapor generated during metallurgical processes. Recent technological focus here has been on optimizing the furnace operation and flue gas cooling rates to influence the resulting particle size distribution and minimize undesirable impurities like residual carbon, directly impacting the final grade and market value of the captured fume.

The most transformative technologies are found in the processing stage, notably densification and slurrification. Densification technology utilizes specialized equipment, often high-pressure roller presses or pelletizers, to reduce the bulk density of the fume from as low as 150-300 kg/m³ to 500-700 kg/m³. This technological improvement dramatically lowers logistical costs and improves material flow, making large-scale handling practical. Slurrification technology involves advanced mixing and chemical dispersion techniques, utilizing high-shear mixers and specialized polymer-based dispersants to create stable, homogeneous aqueous suspensions, ensuring the micro-silica particles do not agglomerate, which is critical for achieving optimal performance in high-dosage concrete applications.

Furthermore, application technologies, particularly in the ready-mix sector, are evolving to incorporate automated dosing systems specifically designed for slurried silica fume, providing accurate, consistent introduction into the concrete mixer, a critical factor for quality control in high-specification mixes. Research also centers on surface modification technologies, where silica fume particles are chemically treated to improve compatibility with specific polymer matrices or cement types, opening up new, high-value applications in nanotechnology and advanced composite materials, positioning the market at the intersection of traditional construction additives and specialized material engineering.

The global distribution and consumption patterns of ultrafine silica fumes exhibit distinct regional characteristics, reflecting differential rates of urbanization, construction spending, and adherence to performance standards. Asia Pacific (APAC) stands out as the largest and fastest-growing market, primarily due to unprecedented infrastructure development in countries like China, India, and Southeast Asian nations. The demand here is fundamentally driven by high-volume requirements for massive projects—ranging from high-speed rail lines and mega-bridges to large-scale hydroelectric dams—where the ability of silica fume to enhance durability and prolong service life is essential for long-term governmental investment stability. Regional players are focusing on expanding local production and densification facilities to meet this explosive domestic demand.

North America and Europe represent mature markets characterized by stable, high-value consumption. In these regions, the primary demand driver is the repair, rehabilitation, and maintenance of aging infrastructure, necessitating highly durable, specialized concrete mixes for structures such as nuclear facilities, marine jetties, and major highway systems. European consumption is strongly influenced by strict environmental regulations (e.g., Eurocodes) promoting longevity and sustainability, making silica fume a favored cement replacement material. Furthermore, the European market exhibits a high preference for silica fume slurries due to the widespread adoption of advanced, automated ready-mix batching plants that prioritize efficiency and precise dosing over the complexities of handling powder forms.

The Middle East and Africa (MEA), particularly the Gulf Cooperation Council (GCC) countries, show significant growth potential, driven by ambitious diversification and construction projects like NEOM and other large-scale city developments, which demand materials capable of withstanding extreme heat and high salinity environments. Latin America’s market growth, while uneven, is sustained by oil well cementing activities, particularly in Brazil and Mexico, where silica fume is crucial for deep-well applications requiring high-density, low-permeability cement slurries. These regional differences mandate that global suppliers customize their product forms, logistics chains, and technical support documentation to align precisely with local construction norms and climatic challenges.

The primary driver is the necessity for high-performance concrete (HPC) that offers superior durability, extremely low permeability, and high compressive strength, especially for critical infrastructure projects like marine structures, bridges, and high-rise towers. Silica fume enhances the concrete microstructure, significantly improving resistance to chloride ingress, sulfates, and abrasion, thereby extending the service life of structures far beyond standard concrete mixes.

Densified silica fume, which has reduced bulk volume, is preferred by purchasers focused on minimizing transportation costs and maximizing storage capacity, particularly for large, stable construction sites. Slurried silica fume, an aqueous suspension, is favored by ready-mix concrete operators requiring automated, precise dosing and easier handling without the dust hazards of dry powder, aligning with modern, automated batching plant requirements in developed markets.

The main challenges stem from the supply being intrinsically linked to the cyclical silicon and ferrosilicon metallurgical industries, leading to supply volatility. Quality inconsistencies arise from variations in furnace operation, which affect crucial characteristics such as carbon content and particle size. Manufacturers mitigate this through advanced collection technologies, rigorous quality sorting, and strategic inventory management to ensure a steady supply of specific, high-specification grades demanded by the refractory and specialized construction sectors.

Asia Pacific (APAC), particularly China and India, is projected to show the highest growth rate. This expansion is fueled by massive governmental investments in infrastructure, including extensive high-speed rail networks, massive port developments, and large-scale urban infrastructure renewal programs. These projects rely heavily on high-durability concrete to ensure the structural integrity and long service life required for long-term public works investments in rapidly developing urban centers.

The fastest-growing non-construction application is the refractories industry. Silica fume is essential for creating high-density, ultra-low cement castables used in lining high-temperature furnaces in the steel and aluminum production sectors. This demand is driven by the global requirement for highly durable materials capable of resisting extreme thermal shock and erosion, offering substantial performance improvement over traditional refractory binders, thereby ensuring longer campaign lives for industrial furnaces.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.