ID : MRU_ 434009 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

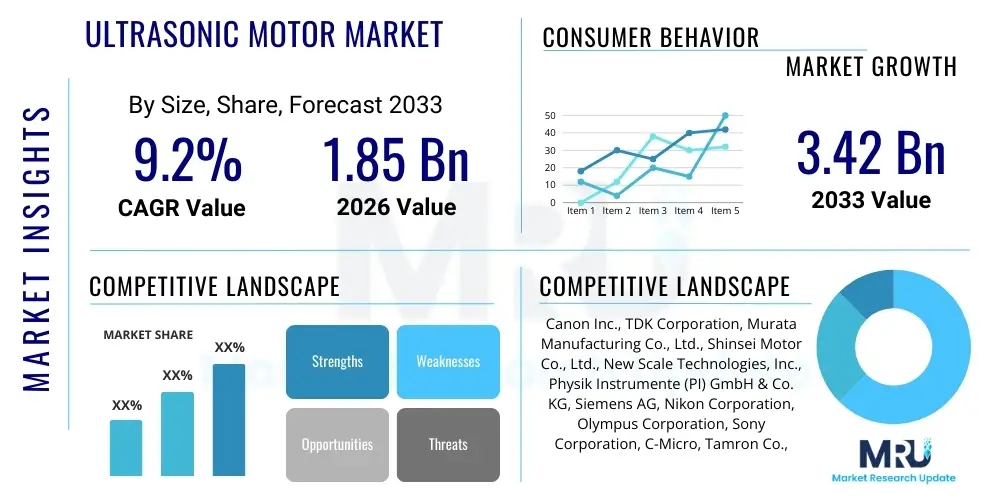

The Ultrasonic Motor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.2% between 2026 and 2033. The market is estimated at USD 1.85 Billion in 2026 and is projected to reach USD 3.42 Billion by the end of the forecast period in 2033.

The Ultrasonic Motor Market encompasses a specialized segment of electric actuators that utilize piezoelectric principles to generate motion, distinguishing themselves through the direct conversion of electrical energy into mechanical energy via ultrasonic vibrations. Unlike electromagnetic motors, ultrasonic motors (USMs) operate by generating high-frequency standing or traveling waves in a stator, which in turn drives a rotor or slider through frictional contact, providing exceptionally high holding torque, rapid response times, and fine resolution. This technology is crucial in applications demanding silent operation and non-magnetic environments, positioning USMs as vital components in sophisticated imaging and precision automation systems. The product description centers on their compactness, often realized as ring-type or linear actuators, built around piezoelectric ceramic materials such as PZT (lead zirconate titanate), which require specific high-frequency drive electronics for operation.

Major applications for ultrasonic motors span across high-tech industries, primarily including advanced camera autofocus mechanisms (where their high speed and silent operation are critical competitive advantages), high-precision medical devices such as surgical robots and MRI-compatible equipment (due to their non-magnetic nature), and specialized instrumentation in aerospace and defense requiring precise angular positioning. The benefits derived from USMs include exceptionally high torque-to-weight ratios, the ability to operate effectively in vacuum environments, zero backlash, and the inherent property of self-locking when power is removed, eliminating the need for external brakes. These performance characteristics make them indispensable where traditional motor limitations regarding size, speed, or electromagnetic interference (EMI) cannot be tolerated.

Driving factors propelling the market forward include the continuous demand for miniaturization across consumer electronics and medical imaging, necessitating smaller, lighter, and more powerful actuation systems. Furthermore, the exponential growth of industrial automation, coupled with the increasing adoption of complex robotic systems in both manufacturing and healthcare, fuels the requirement for actuators offering sub-micron precision. Technological advancements in piezoelectric material science, coupled with improved control circuitry that enhances efficiency and reduces energy consumption, are also widening the applicability of USMs beyond their traditional photography niche, establishing them as foundational technology in the next generation of precision motion control.

The Ultrasonic Motor Market is characterized by robust business trends centered on technological diversification and increasing integration into high-value medical and optical equipment. Key business strategies involve strategic partnerships between motor manufacturers and Original Equipment Manufacturers (OEMs) in emerging fields like augmented reality (AR) and virtual reality (VR) focus modules, where compact, fast actuators are essential. The market structure remains highly competitive, with established Japanese companies dominating the optics segment, while specialized European and North American firms focus on advanced medical and scientific instrumentation requiring customized, high-reliability solutions. A dominant trend is the shift towards traveling wave motors due to their higher efficiency and greater torque output compared to standing wave variants, alongside continuous investment in materials research aimed at developing lead-free piezoelectric alternatives to meet increasingly stringent environmental regulations.

Regional trends indicate that the Asia Pacific (APAC) region is the primary manufacturing hub and largest consumer market, driven by the massive electronics and automotive manufacturing base in countries like China, Japan, and South Korea, which heavily utilize USMs in digital cameras and vehicle focus systems. North America and Europe, while representing smaller volume markets, lead in terms of technological innovation and expenditure on high-precision, customized ultrasonic motors for the medical device and aerospace sectors. The stringent regulatory environment in these Western regions necessitates motors with exceptional reliability and adherence to strict operational standards, often driving up the average selling price (ASP) per unit compared to high-volume consumer applications in APAC. Investment in R&D remains disproportionately high in these regions, focusing on next-generation control algorithms and structural improvements.

Segmentation trends highlight the critical role of the application segment, with Optics & Imaging dominating the revenue share due to the ubiquitous use of USMs in camera lenses for high-speed autofocus. However, the Medical Devices segment is forecast to exhibit the highest Compound Annual Growth Rate (CAGR), fueled by increasing expenditure on minimally invasive surgery, haptics, and robotic surgical systems that demand MRI-compatible, highly precise, and silent actuation. Furthermore, within the product segment, the traveling wave type motor is steadily gaining market share over the standing wave type due to performance advantages, necessitating manufacturers to retool production lines to optimize for traveling wave designs, thereby affecting material sourcing and manufacturing complexities globally.

User inquiries regarding AI's influence on the Ultrasonic Motor Market frequently center on how machine learning can optimize the delicate control and performance of these piezoelectric systems. Common questions include: Can AI enhance the precision beyond existing limits? How can predictive maintenance be implemented given the motors' reliance on friction? Will AI-driven design tools accelerate the development of specialized USMs for robotics? The prevailing user themes revolve around performance optimization, specifically addressing the inherent challenges of friction wear and temperature sensitivity in USMs. Users expect AI to stabilize performance under varying loads and environmental conditions, transforming USMs from specialized, sensitive components into more robust, general-purpose actuators capable of seamless integration into complex autonomous systems, particularly those requiring real-time adjustment and diagnostic capabilities.

The core expectation is that Artificial Intelligence, particularly reinforcement learning and advanced statistical modeling, will revolutionize the motor control circuitry. Since USMs operate at high frequencies (typically 20 kHz to 200 kHz) and their efficiency is highly sensitive to drive frequency and voltage phase differences, AI algorithms can continuously monitor operational parameters (such as vibrational amplitude and wave propagation characteristics) and make micro-adjustments in real-time. This capability directly addresses one of the primary historical drawbacks of ultrasonic motors: their sensitivity to temperature fluctuations, which affect the material properties of the piezoelectric ceramics. AI-based controllers can compensate for these thermal drifts instantly, leading to significantly improved reliability, better repeatability, and extended operational life, thereby broadening their appeal in critical applications like satellite components or long-term medical implants.

Furthermore, AI is poised to streamline the manufacturing and quality assurance processes for ultrasonic motors, which currently rely heavily on precise assembly and meticulous testing of piezoelectric components. Machine vision systems powered by deep learning can perform ultra-fine defect detection in PZT ceramics or bonding layers, ensuring higher yield rates and superior component consistency. From a strategic perspective, AI tools enable faster material discovery and simulation, allowing engineers to model complex electromechanical interactions more efficiently, shortening the design cycle for custom USMs required for new robotic platforms or next-generation optical equipment. This integration shifts the competitive landscape, where companies successfully leveraging AI for predictive performance and rapid prototyping will gain a substantial market lead, especially in the high-mix, low-volume segments of aerospace and specialized instrumentation.

The Ultrasonic Motor Market is shaped by a confluence of influential factors: robust drivers pushing adoption in precision fields, critical restraints limiting mass-market penetration, significant opportunities in emerging technologies, and external forces impacting market velocity. The primary drivers include the escalating global demand for advanced optical systems, particularly in high-resolution photography and industrial inspection, where the high-speed, silent, and non-magnetic operation of USMs is non-negotiable. Furthermore, the burgeoning field of medical robotics and the necessity for miniature, high-torque actuators in minimally invasive surgical tools strongly support market growth. Conversely, significant restraints include the relatively high manufacturing complexity and cost associated with producing reliable, high-frequency piezoelectric drive electronics, coupled with the inherent challenge of frictional wear between the stator and rotor, which can limit long-term lifespan and require sophisticated control solutions. These restraints constrain the deployment of USMs in general industrial applications where cost and robust durability are prioritized over precision and silence.

Opportunities for market expansion are predominantly found in the convergence of ultrasonic motor technology with next-generation applications such as haptic feedback systems, micro-robotics, and space exploration equipment, where the unique benefits of high holding torque and vacuum compatibility provide a distinct advantage over conventional electromagnetic motors. Furthermore, there is a substantial opportunity in developing standardized, cost-effective USM components and integrated driver chips that lower the barrier to entry for mid-sized electronics manufacturers. Addressing the friction and durability restraint through the development of advanced, low-wear materials, such as specific ceramic coatings or improved contact mechanisms, represents a critical area for R&D investment that promises significant competitive gains and market penetration into more demanding, high-cycle environments. Strategic collaborations focused on application-specific motor designs tailored for emerging platforms like commercial drones and adaptive headlights in the automotive sector also present viable avenues for substantial revenue growth.

Impact forces on the market include technological advancements, particularly in solid-state electronics and power management, which are reducing the size and cost of the required high-frequency controllers, thus making USMs more attractive for portable devices. Regulatory forces, especially those governing medical device standards (e.g., FDA approvals in North America and CE marking in Europe), significantly influence the design and testing protocols for motors used in healthcare, driving up quality requirements but also guaranteeing premium pricing for certified products. Competitive intensity remains high, primarily centered on intellectual property related to drive mechanisms (traveling wave vs. standing wave) and material science optimization. Economic impact forces, such as fluctuations in the supply chain for PZT ceramics and rare-earth materials, can affect production costs. Finally, the environmental push toward lead-free piezoelectric materials (to replace traditional lead zirconate titanate) poses both a challenge in R&D and an opportunity for manufacturers who successfully transition to environmentally sustainable alternatives, aligning with global AEO trends toward green technology adoption.

The Ultrasonic Motor Market is systematically analyzed across key dimensions, primarily delineated by the motor type, the mechanism of wave propagation, and the varied industrial applications where precision actuation is essential. This multi-faceted segmentation allows stakeholders to accurately gauge demand trends and strategic opportunities within specific technical niches and end-user markets. The core segmentation by motor type—Standing Wave and Traveling Wave—reflects fundamental differences in operational mechanics and performance characteristics, dictating suitability for high-speed versus high-torque requirements. Furthermore, segmentation by application, which includes Optics & Imaging, Medical Devices, Aerospace & Defense, Consumer Electronics, and Automotive, reveals the economic value derived from each sector, highlighting the dependence on USMs for performance advantages in specialized equipment. Understanding these segments is crucial for allocating R&D resources effectively and optimizing sales strategies towards sectors exhibiting the highest growth potential, such as robotics and advanced haptics, which are often classified within the Medical or Consumer Electronics segments.

The Standing Wave Ultrasonic Motor (SWUM) segment generally finds utility in applications requiring very high positioning resolution and low speeds, such as micro-positioning stages and some microscope focusing mechanisms. SWUMs use two orthogonally polarized standing waves to achieve motion, often resulting in complex drive circuitry but offering unparalleled precision control at the micro-scale. Conversely, the Traveling Wave Ultrasonic Motor (TWUM) segment, which employs a continuous wave to drive the rotor, dominates the high-volume market, particularly in camera lens autofocus systems. TWUMs offer smoother motion, higher torque density, and simpler control compared to SWUMs, making them the preferred choice for consumer and industrial applications where rapid response and reliability are key. The dynamic shift in market share between these two technical segments reflects the industry's continuous balancing act between maximum achievable precision (SWUM) and high-speed, reliable performance (TWUM).

Analyzing the market geographically reveals distinct regional demand patterns; for instance, Asia Pacific dominates the volume of TWUM production due to its strong consumer electronics manufacturing base, while North America and Europe lead in the procurement of high-reliability, customized SWUMs and TWUMs for highly regulated industries like aerospace, military, and specialized medical imaging. This differential demand structure mandates varied supply chain management and product standardization approaches depending on the targeted region. Furthermore, segmentation by power output (low, medium, high power) is increasingly important, as innovations push USM technology into higher load applications previously monopolized by conventional motors, specifically in industrial automation and heavy-duty robotic manipulation, demonstrating the technology's evolving maturity and capability to handle greater mechanical work.

The value chain for the Ultrasonic Motor Market begins with the highly specialized upstream segment, dominated by the sourcing and refinement of piezoelectric materials, predominantly PZT ceramics, and increasingly, lead-free alternatives. This segment involves high-precision material synthesis, sintering, and polarization processes, critical steps that determine the motor's ultimate efficiency and reliability. Key upstream suppliers include specialized chemical and ceramic manufacturers who provide the raw piezoelectric components, as well as manufacturers of high-purity metals and advanced polymers used for the stator, rotor, and mechanical housing. A tight control over material quality is paramount, as even minor inconsistencies in the piezoelectric constants or ceramic density directly impact the wave generation capabilities and overall motor performance. The complexity of these materials often creates a dependency on a limited pool of specialized suppliers, leading to potential supply chain vulnerability and high input costs for motor manufacturers.

The midstream segment involves the core manufacturing process carried out by the Ultrasonic Motor OEMs. This stage encompasses the intricate assembly of the stator and rotor, the integration of high-frequency drive electronics, and meticulous quality control (QC) checks, including vibration testing and precise performance calibration. The manufacturing requires cleanroom environments and highly skilled labor due to the miniature size and precision requirements of the components. Distribution channels for USMs are bifurcated into direct and indirect routes. Direct sales are predominant for large-volume OEMs, particularly in the consumer electronics sector (e.g., major camera manufacturers) and for highly customized, high-specification projects in aerospace and medical devices. These direct relationships involve significant technical consultation and long-term supply agreements, necessitating robust technical support infrastructure from the motor manufacturer.

Indirect distribution primarily utilizes specialized technical distributors or value-added resellers (VARs) who possess the expertise to integrate complex motion control solutions into smaller or diversified end-user projects, such as specialized research labs or small-scale robotics firms. These indirect channels manage inventory, provide localized support, and aggregate demand from diverse application segments. Downstream, the value chain culminates with system integrators and the final end-users across various sectors, where the USMs are incorporated into finished products like optical lenses, robotic arms, or diagnostic imaging machines. The performance and reliability of the USM are critical to the final product's market success, creating a powerful feedback loop where downstream application requirements drive upstream innovation in material science and motor design. Efficient inventory management and the ability to quickly deliver highly customized solutions are key competitive advantages in the downstream segment, especially in the rapidly evolving medical technology field.

Potential customers for the Ultrasonic Motor Market are diverse, encompassing technologically advanced industries that demand high precision, miniaturization, and specialized operational characteristics unattainable by conventional electromagnetic motors. The primary end-users are concentrated in sectors where silence, speed, and zero electromagnetic interference (EMI) are critical performance criteria. These buyers include major Original Equipment Manufacturers (OEMs) in the optical industry, such as global leaders in camera and lens manufacturing, who rely exclusively on USMs for their high-speed, silent autofocus mechanisms, often branding them as a premium feature. Furthermore, the medical device industry represents a rapidly expanding customer base, particularly manufacturers of robotic surgical systems, advanced diagnostic imaging equipment (including MRI systems where non-magnetic actuators are mandatory), and miniature implantable devices requiring fine, reliable motion.

Another significant group of potential customers includes specialized manufacturers within the aerospace and defense sectors. These buyers procure USMs for satellite component alignment, precise sensor positioning in guidance systems, and airborne surveillance equipment, where resistance to vacuum conditions, low power consumption, and high repeatability under extreme temperature variations are essential requirements. Additionally, the emerging market of high-end consumer electronics and advanced haptic feedback systems, particularly in AR/VR headsets and specialized mobile device components, is rapidly becoming a high-volume customer segment. These buyers prioritize compactness and rapid response for creating immersive, highly realistic sensory experiences, making the miniature, high-frequency characteristics of USMs highly desirable.

Finally, the industrial automation and scientific instrumentation sectors represent a constant demand stream, albeit often for lower volume, highly customized products. Research institutions, university laboratories, and manufacturers of semiconductor inspection equipment utilize ultrasonic motors for ultra-fine positioning stages (nanopositioning) necessary for micro-manipulation and high-resolution material analysis. For these customers, the zero backlash and inherent self-locking capabilities of USMs offer a technical advantage over traditional linear stages. The decision-makers within these customer groups are typically R&D managers, lead system engineers, and procurement specialists who prioritize technical specifications, long-term reliability data, and compliance with stringent quality standards (like ISO certifications or medical regulatory approvals) over sheer cost minimization, reflecting the value attached to precision and operational integrity.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.42 Billion |

| Growth Rate | 9.2% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Canon Inc., TDK Corporation, Murata Manufacturing Co., Ltd., Shinsei Motor Co., Ltd., New Scale Technologies, Inc., Physik Instrumente (PI) GmbH & Co. KG, Siemens AG, Nikon Corporation, Olympus Corporation, Sony Corporation, C-Micro, Tamron Co., Ltd., Precision Microdrives Ltd., MKS Instruments, Inc., Micromo (Faulhaber Group), AURA Motor Co., Ltd., Dynamic Micro-Devices, Inc. (DMD), Beijing Ultrasonic Motors Co., Ltd., Nanomotion Ltd., Samsung Electro-Mechanics. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Ultrasonic Motor Market is fundamentally anchored in advanced piezoelectric material science and sophisticated high-frequency electronic control systems. The core technology involves the precise generation and management of ultrasonic standing or traveling waves in a solid elastic body (stator) using piezoelectric ceramics, most commonly PZT derivatives. Current technological innovation is focused heavily on optimizing the electromechanical coupling coefficient of these ceramic materials to maximize energy transfer efficiency, thus increasing the motor's power output while minimizing heat generation. Furthermore, research is intensifying in developing lead-free piezoelectric materials to comply with environmental regulations, seeking alternatives like Bismuth Sodium Titanate (BNT) or Barium Titanate (BT) composites, which must match the performance characteristics of PZT while being manufacturable at a competitive cost. The performance of USMs is inextricably linked to the structural design of the stator, where finite element analysis (FEA) and computational fluid dynamics (CFD) are routinely used to optimize vibration mode shapes and friction interfaces, ensuring maximal contact force transmission and minimal energy loss.

Beyond the material science, a critical technological differentiator lies in the motor drive electronics and associated control strategies. Ultrasonic motors require specialized power amplifiers capable of generating high-voltage, high-frequency (typically 20 kHz to 200 kHz) sinusoidal or square-wave signals with precise phase control between the driving electrodes. Advances in solid-state electronics, particularly the miniaturization and efficiency improvement of MOSFETs and ASICs (Application-Specific Integrated Circuits), are enabling the integration of these complex drivers directly onto the motor housing or within the end-user system, significantly reducing the overall footprint and complexity for system integrators. The implementation of advanced digital signal processing (DSP) and field-programmable gate arrays (FPGAs) allows for real-time adjustments of the driving frequency and phase angle to maintain peak performance despite temperature or load variations, directly addressing historical limitations related to performance drift and environmental sensitivity.

The future technology trajectory is moving towards fully integrated micro-motors and leveraging microelectromechanical systems (MEMS) fabrication techniques for ultra-miniature applications, particularly in advanced ophthalmology and micro-robotics. Hybrid USMs, combining aspects of both traveling wave and standing wave principles, are also emerging to achieve the best combination of speed, torque, and precision in a single unit. Furthermore, the integration of advanced sensors (e.g., encoders or hall sensors) directly into the motor structure provides closed-loop feedback, allowing for highly accurate positional control crucial for high-end scientific instruments and industrial automation tasks. The development of non-contact USM technologies, though still nascent, also represents a long-term goal, aiming to eliminate frictional wear and dramatically extend operational life, thereby opening up USMs to rugged, high-cycle industrial applications where current friction-based designs are often unsuitable.

The main advantage of ultrasonic motors (USMs) is their high holding torque when de-energized (self-locking feature), silent operation, exceptionally fine positional resolution (often sub-micron), and their non-magnetic nature, making them ideal for MRI environments and applications sensitive to electromagnetic interference (EMI).

The Optics and Imaging segment, particularly professional and consumer camera lens autofocus systems, constitutes the largest demand volume, capitalizing on the USMs' rapid response time and silent operation necessary for high-quality, high-speed photography.

The primary constraint is the relatively high manufacturing cost and complexity of the high-frequency drive electronics required for stable operation, coupled with the susceptibility of friction-based designs to wear and sensitivity to performance drift caused by temperature variations over long operational cycles.

The market is actively investing in research and development of lead-free piezoelectric materials, such as Bismuth Sodium Titanate (BNT) and Barium Titanate (BT) composites, to replace traditional PZT (lead zirconate titanate) in compliance with stricter global environmental regulations like RoHS and REACH.

AI is crucial for enhancing USM performance by providing real-time adaptive control algorithms. These algorithms continuously monitor operational conditions and adjust the driving frequency and phase, thereby compensating for performance degradation due to thermal changes and frictional wear, significantly increasing reliability and precision.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.