ID : MRU_ 434848 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

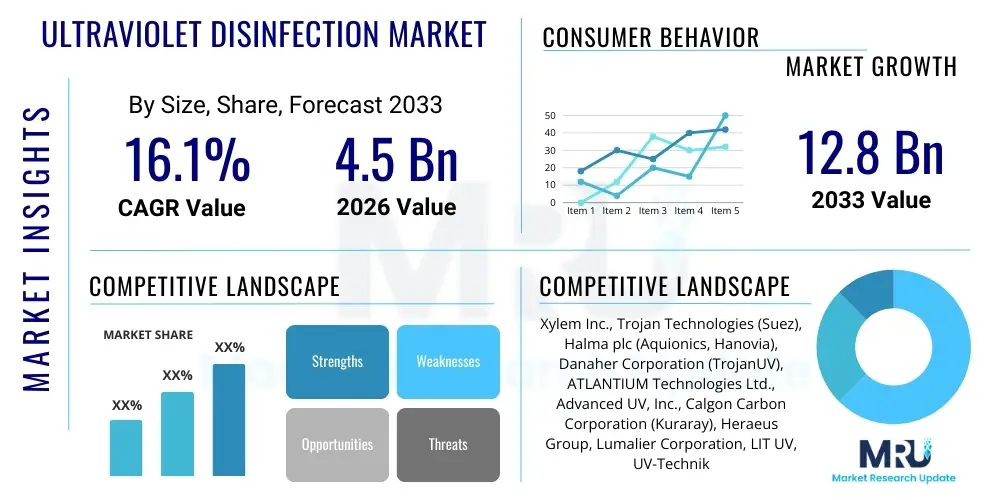

The Ultraviolet Disinfection Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 16.1% between 2026 and 2033. The market is estimated at $4.5 Billion in 2026 and is projected to reach $12.8 Billion by the end of the forecast period in 2033.

The Ultraviolet (UV) Disinfection Market encompasses equipment and services utilizing short-wavelength ultraviolet-C (UV-C) light to inactivate pathogenic microorganisms such as bacteria, viruses, and protozoa. This non-chemical disinfection method is gaining paramount importance across various sectors due to stringent global regulations concerning water and air quality, coupled with increasing public awareness regarding chemical residues associated with traditional methods like chlorination. UV disinfection systems are primarily deployed for the purification of drinking water, wastewater, process water in industrial settings, and air in healthcare and commercial environments. The technology’s core product lineup includes low-pressure (LP), medium-pressure (MP) lamps, and the rapidly growing segment of UV Light Emitting Diodes (UV-C LEDs), offering scalability and sustainability advantages.

The primary applications of UV disinfection span municipal water treatment plants, where it serves as a critical barrier against chlorine-resistant pathogens like Cryptosporidium and Giardia, and in industrial processes, particularly in the food & beverage, pharmaceutical, and electronics industries requiring ultra-pure water. Key benefits driving market adoption include the absence of disinfection byproducts (DBPs), minimal contact time required for effective sterilization, and the ability to operate effectively against a wide spectrum of microorganisms without altering the physical or chemical composition of the treated medium. Furthermore, UV systems are environmentally friendly and require less complex infrastructure compared to chemical treatment processes.

Market growth is significantly driven by escalating concerns over waterborne diseases and the necessity to comply with stricter discharge limits imposed by environmental protection agencies globally. The widespread adoption of UV-C LED technology is also a major accelerator, offering energy efficiency, smaller footprints, and extended operational lifecycles, making the technology suitable for decentralized and point-of-use applications. Additionally, the recent global emphasis on air quality and infection control, particularly post-pandemic, has catalyzed the deployment of UV germicidal irradiation (UVGI) systems in HVAC units and public spaces, positioning UV disinfection as an indispensable technology for public health safety.

The Ultraviolet Disinfection Market is experiencing robust expansion fueled by a convergence of technological advancements and escalating global demands for safe water and air. Business trends indicate a strong shift towards advanced UV-C LED solutions, replacing conventional mercury-vapor lamps due to their enhanced durability, lower maintenance requirements, and alignment with environmental mandates phasing out mercury use. Strategic mergers and acquisitions are common, as large multinational corporations seek to integrate specialized UV system manufacturers to broaden their portfolio, especially in the municipal and industrial wastewater sectors. Furthermore, the development of smart UV systems incorporating IoT sensors and AI-driven monitoring for optimal dosage control and predictive maintenance is creating new value propositions and improving system efficiency and reliability.

Regionally, Asia Pacific (APAC) stands out as the fastest-growing market, largely attributable to massive infrastructure investments in water and wastewater treatment, rapid industrialization, and high population density requiring effective pathogen control solutions. North America and Europe maintain leading market shares, primarily driven by strict regulatory enforcement, high adoption rates in advanced industrial manufacturing (semiconductors, pharmaceuticals), and early integration of energy-efficient technologies. Emerging economies in Latin America and the Middle East & Africa (MEA) are also showing promising growth, primarily focusing on addressing water scarcity and improving municipal sanitation standards through cost-effective UV systems, often supported by international aid and government initiatives.

Segmentation trends highlight the dominance of the Water & Wastewater treatment application segment due to mandatory compliance and high volume processing needs. However, the Air & Surface Disinfection segment is exhibiting the highest CAGR, propelled by increased utilization in healthcare facilities (hospitals, clinics) and commercial buildings (offices, schools) focusing on mitigating airborne viral transmission risks. Technologically, the UV-C LED segment is set to revolutionize point-of-use disinfection and small-scale applications, while medium-pressure (MP) lamps retain their critical role in large-scale municipal operations requiring high power output and broad germicidal spectrum capabilities.

Common user questions regarding AI's impact on UV disinfection technology often center on how automation can improve dosage accuracy, reduce energy consumption, and enhance predictive maintenance capabilities to maximize lamp lifespan. Users are highly interested in integrating AI to analyze real-time water quality data (such as turbidity, flow rate, and UV transmittance) and automatically adjust UV lamp intensity, thereby ensuring continuous compliance while minimizing operational expenditure. Key concerns revolve around the complexity and cost associated with implementing AI-enabled smart sensors and control systems, and the reliability of AI algorithms in handling rapidly changing environmental conditions or treating complex industrial effluents. Users expect AI to transform UV systems from passive disinfection units into proactive, self-optimizing sterilization platforms.

The integration of Artificial Intelligence (AI) and Machine Learning (ML) algorithms is fundamentally shifting the operational paradigm of advanced UV disinfection systems. AI enables sophisticated data processing from integrated sensor networks, allowing the system to learn optimal disinfection dosages based on historical performance data and prevailing water or air conditions. This advanced control minimizes the risk of under-dosing, which can lead to incomplete inactivation, and prevents over-dosing, which results in unnecessary energy wastage and premature lamp wear. Specifically in municipal wastewater treatment, where input variables fluctuate widely, AI models provide the necessary agility for dynamic dose adjustment, ensuring treatment efficiency and regulatory adherence under all operational circumstances.

Furthermore, AI significantly enhances the reliability and maintenance schedule of high-capital UV installations. By continuously monitoring parameters such as lamp voltage, temperature, and UV intensity decay curves, ML models can accurately predict lamp failure or required maintenance intervals long before catastrophic system shutdowns occur. This predictive maintenance capability allows operators to schedule proactive replacements, optimize inventory management for spare parts, and drastically reduce costly downtime. The application of AI also extends to pattern recognition in complex contaminant removal, particularly when UV is coupled with advanced oxidation processes (AOPs), optimizing the chemical injection rates (e.g., hydrogen peroxide) based on real-time target contaminant concentration data.

The Ultraviolet Disinfection Market dynamics are governed by powerful drivers related to global health crises and environmental mandates, offset by specific technological and financial restraints, while significant opportunities arise from technological evolution and application diversification. The primary drivers include the mandatory requirement for tertiary wastewater treatment to comply with increasingly stringent environmental discharge standards and the pervasive fear of waterborne pathogens resistant to traditional chlorine disinfection, such as Cryptosporidium. Conversely, the market faces restraints such as the high initial capital investment required for large-scale municipal UV installations and the requirement for pre-treatment of highly turbid water to ensure UV light penetration efficiency. The key opportunity lies in the rapid commercialization and adoption of energy-saving UV-C LED technology and the expanding demand for air and surface disinfection in post-COVID commercial infrastructure. These forces collectively shape the competitive landscape and strategic direction of key industry players.

Drivers: The most significant driver is the increasing recognition by regulatory bodies, such as the EPA and WHO, that chemical-free disinfection is necessary to combat harmful disinfection byproducts (DBPs) formed during chlorine treatment. The global infrastructure push, especially in developing nations, to upgrade aging water infrastructure and improve sanitation facilities heavily favors UV technology due to its proven efficacy and operational simplicity compared to ozone or advanced chlorination methods. The heightened awareness of microbial resistance, coupled with the need for point-of-use disinfection in residential and commercial settings, particularly in areas affected by aging pipe infrastructure or natural disasters, consistently propels demand for compact UV systems. Furthermore, the industrial demand for ultra-pure water in semiconductor manufacturing and bioprocessing is non-negotiable, positioning UV as the indispensable final polishing step.

Restraints: Despite the benefits, the market faces constraints related to operational complexity under certain environmental conditions. High levels of suspended solids, color, or dissolved organic carbon (DOC) in source water can significantly reduce UV transmittance, necessitating substantial pre-filtration, which adds cost and complexity to the overall treatment train. Another barrier is the perceived operational cost associated with replacing conventional UV lamps (LP or MP) every 6 to 12 months, although this constraint is gradually being mitigated by the longevity and efficiency of modern UV-C LED arrays. Regulatory acceptance in certain niche applications, particularly for highly specialized industrial effluents, can also sometimes lag behind technology readiness, creating market friction.

Opportunities: Major growth opportunities stem from the emergence of new UV sources, particularly Far-UVC (222 nm), which shows promise for safe, continuous disinfection of occupied air spaces, potentially revolutionizing infection control in public settings. The convergence of UV disinfection with other technologies, such as photocatalytic oxidation and ultrasound (sonolysis), creating Advanced Oxidation Processes (AOPs), offers a lucrative pathway for treating emerging contaminants (ECs) like pharmaceuticals and persistent organic pollutants. Furthermore, the growing trend toward decentralized water reuse and recycling systems in drought-prone regions provides a substantial, untapped market for containerized, robust UV disinfection solutions. The increasing regulatory pressure on industries like brewing, beverage, and dairy to minimize water usage while maintaining strict hygiene standards provides a continuous stream of B2B opportunities.

The Ultraviolet Disinfection Market is intricately segmented based on component, application, end-user, and UV lamp type, providing a detailed view of technological preference and deployment patterns. The core segments reflect the fundamental structure of the technology, ranging from the light source itself (UV lamp type) to where it is ultimately deployed (application and end-user). Understanding these segments is crucial for market stakeholders, as growth rates vary significantly; for instance, UV-C LEDs, though currently smaller in market share, exhibit exponential growth compared to traditional low-pressure lamps due to their versatility and sustainability profile. The most impactful segmentation relies heavily on the Application category, where Municipal Water and Wastewater treatment dominates the volume, while the emerging Air and Surface disinfection sectors drive innovation and short-term revenue spikes in response to health crises.

The Component segment, encompassing UV lamps, controller units, reactor chambers, and quartz sleeves, highlights the supply chain reliance on specialized manufacturing. The long-term profitability of the market is increasingly tied to the development of higher-efficiency UV lamps and intelligent controller units that integrate seamlessly with plant SCADA systems. End-user segmentation reveals a consistent pattern where municipal bodies represent the highest investment volume, followed closely by large industrial users like food & beverage and power generation sectors which require pathogen-free process water to maintain product integrity and equipment longevity. These overlapping segments illustrate the comprehensive demand for UV technology across the public health spectrum and high-value industrial operations.

The Value Chain of the Ultraviolet Disinfection Market is a highly specialized sequence beginning with the manufacturing of core components and culminating in complex system integration and aftermarket services. Upstream analysis focuses heavily on the production of specialized materials, notably high-purity quartz glass for sleeves and reactors, and the fabrication of UV-C emitters (either mercury vapor lamps or advanced semiconductors for LEDs). Innovation at this stage is critical, specifically in developing more energy-efficient and long-lasting UV sources. Key upstream suppliers include material science firms and specialized electronic component manufacturers who dictate the fundamental performance metrics and cost structure of the final UV system. The transition towards UV-C LEDs is placing greater emphasis on semiconductor fabrication expertise within the upstream segment.

The middle segment involves the core manufacturers who design, assemble, and test the complete UV reactor systems, including the integration of specialized power supplies, sensor technology, and automated cleaning mechanisms (wiper systems). Direct distribution channels are predominantly used for large, bespoke municipal projects, where manufacturers often engage directly with engineering procurement and construction (EPC) firms and municipal utility operators to provide tailored solutions and specialized installation expertise. Conversely, indirect channels, relying on distributors, wholesalers, and specialized water treatment dealers, are more common for smaller industrial, commercial, and residential point-of-use systems, capitalizing on their established logistics networks and local service capabilities.

Downstream activities are dominated by installation, commissioning, validation, and crucial aftermarket services, including routine maintenance and the supply of consumable components like replacement lamps and quartz sleeves. The profitability in the long term for manufacturers is increasingly derived from these high-margin aftermarket services. Specialized engineering consulting firms play a critical role downstream by designing and validating the system integration into existing water treatment facilities, ensuring regulatory compliance and optimal performance. The effectiveness of the overall UV system highly depends on robust downstream support, particularly for complex industrial and critical healthcare installations.

Potential customers for Ultraviolet Disinfection systems span a vast range of public and private sector entities requiring effective, chemical-free microbial inactivation to protect public health, ensure product integrity, or comply with strict environmental mandates. The largest volume buyers are municipal water treatment utilities, which are mandated to provide potable water and safely discharge treated wastewater, often requiring high-capacity, multi-lamp medium-pressure systems. These utilities prioritize longevity, low operational complexity, and regulatory validation (e.g., USEPA-validated systems). Industrial process users, particularly in the pharmaceutical, beverage, and electronics sectors, form the second major customer base, where ultra-pure water is essential for manufacturing processes, preventing contamination, and avoiding product recalls. Their purchasing decisions hinge on validation protocols, precise dosing control, and system reliability.

Beyond these primary segments, the healthcare sector represents a rapidly expanding customer base, utilizing UV disinfection for both water (dialysis, laboratory) and critical air and surface sterilization in operating rooms and isolation wards. Hospitals are increasingly adopting pulsed UV light systems and UVGI units for room disinfection and HVAC integration to combat hospital-acquired infections (HAIs). Furthermore, commercial building owners, motivated by post-pandemic safety protocols and improved indoor air quality (IAQ) standards, are significant potential customers for upper-room UVGI and in-duct air disinfection systems. Residential customers, driven by concerns over tap water safety or well water contamination, represent the mass market for compact, point-of-entry (POE) or point-of-use (POU) UV systems, typically favoring the compact and low-maintenance attributes of UV-C LED products.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $4.5 Billion |

| Market Forecast in 2033 | $12.8 Billion |

| Growth Rate | 16.1% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Xylem Inc., Trojan Technologies (Suez), Halma plc (Aquionics, Hanovia), Danaher Corporation (TrojanUV), ATLANTIUM Technologies Ltd., Advanced UV, Inc., Calgon Carbon Corporation (Kuraray), Heraeus Group, Lumalier Corporation, LIT UV, UV-Technik Speziallampen GmbH, Sensor Electronic Technology, Inc. (SETi), Crystal IS, Inc., Seoul Viosys Co., Ltd., Osram GmbH, Siemens AG, Evoqua Water Technologies, Dürr Group, and Green UV LLC. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Ultraviolet Disinfection Market is currently undergoing a transformative technological shift driven primarily by the transition from conventional mercury vapor lamps to solid-state UV Light Emitting Diodes (UV-C LEDs). Traditional systems utilize Low-Pressure (LP) lamps, known for their monochromatic output at 254 nm, ideal for standard germicidal irradiation, or Medium-Pressure (MP) lamps, which offer a polychromatic spectrum and higher power output suitable for larger flows and advanced oxidation processes (AOPs). However, UV-C LEDs represent the future, offering advantages like instant on/off capabilities, minimal heat generation, greater longevity (upwards of 10,000 operational hours), and most critically, they are mercury-free, aligning with global environmental treaties like the Minamata Convention. While LEDs currently face challenges in achieving the same power output as MP lamps for high-flow municipal applications, their rapidly decreasing cost and increasing efficiency are accelerating their adoption in point-of-use and decentralized systems.

Beyond the light source, the technology landscape is being shaped by advancements in reactor design and integrated monitoring systems. Modern UV reactors are engineered using Computational Fluid Dynamics (CFD) modeling to ensure optimal hydraulic conditions, minimizing short-circuiting and ensuring uniform UV dose delivery across the entire water flow, a critical requirement for regulatory validation. Integrated smart sensors (UV intensity sensors) and sophisticated control algorithms are now standard, ensuring that the applied dose is always sufficient regardless of fluctuations in source water quality (turbidity or UV transmittance). Furthermore, self-cleaning mechanisms (mechanical wiper systems) are essential for maintaining the clarity of the quartz sleeves, crucial for maximizing UV penetration, thereby guaranteeing continuous operational efficacy without manual intervention.

Another significant technological trend involves the exploration of novel wavelengths and specialized UV applications. Far-UVC technology (specifically 222 nm) is gaining substantial attention due to research suggesting its germicidal efficacy against airborne pathogens while posing minimal risk to human skin and eyes, potentially allowing for continuous, low-level air disinfection in occupied spaces. This technology could fundamentally reshape infection control in schools, offices, and transport hubs. Concurrently, the use of UV technology in synergistic AOPs (e.g., UV/Peroxide, UV/Ozone) is expanding the market’s reach into tertiary treatment, offering solutions for complex contaminants like endocrine-disrupting chemicals, taste-and-odor compounds, and resistant industrial micro-pollutants that standard chlorination or UV alone cannot effectively neutralize. These integrated systems require advanced chemical dosing and sensor feedback loops for successful implementation.

Regional dynamics play a crucial role in shaping the demand and technological adoption within the Ultraviolet Disinfection Market, driven by differential regulatory pressures, industrial concentration, and infrastructure spending patterns.

The primary advantage is that UV disinfection is a non-chemical process, effectively inactivating pathogens like Cryptosporidium and Giardia without producing harmful disinfection byproducts (DBPs), which are common concerns associated with chlorine treatment methods. It offers immediate microbial inactivation with minimal contact time.

UV-C LED technology is driving market growth by providing smaller, more energy-efficient, and mercury-free disinfection solutions. It facilitates modularity, instant on/off operation, and extends system lifespan, making UV disinfection viable for compact, point-of-use (POU) residential systems and specialized industrial applications.

UV in AOPs (e.g., UV/Peroxide) leverages UV light to generate highly reactive hydroxyl radicals. This process is crucial for tertiary wastewater treatment and the degradation of emerging contaminants (ECs) like pharmaceuticals, pesticides, and industrial micro-pollutants that are resistant to standard UV or conventional treatment processes.

The Air and Surface Disinfection segment, particularly utilizing UV Germicidal Irradiation (UVGI) in healthcare, commercial HVAC systems, and public transportation, is expected to exhibit the highest CAGR due to heightened global focus on airborne infection control and indoor air quality post-pandemic mandates.

The main restraining factors include the substantial initial capital investment required for high-capacity municipal systems and the necessity for effective pre-treatment (filtration) to reduce turbidity and dissolved organic carbon, which can severely diminish the UV light transmittance and system efficacy.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.