ID : MRU_ 436905 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

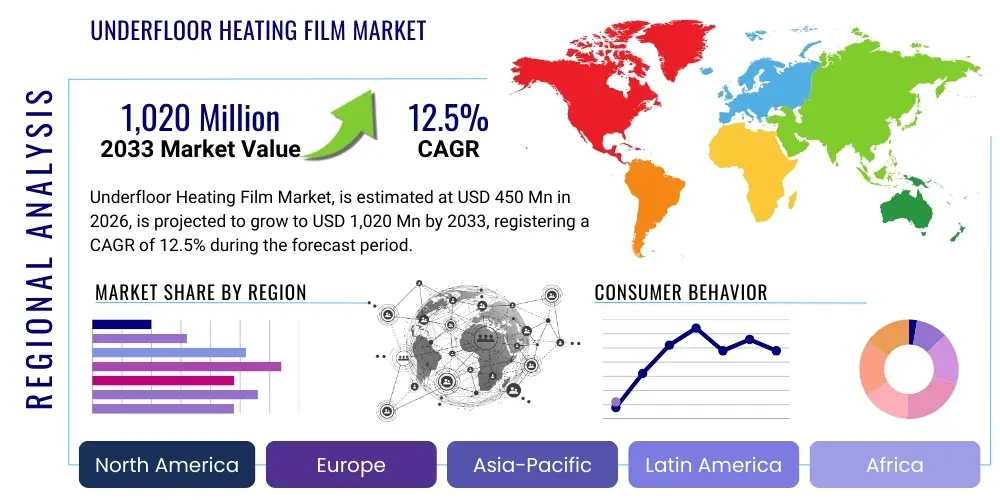

The Underfloor Heating Film Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 1,020 Million by the end of the forecast period in 2033.

The Underfloor Heating Film Market encompasses advanced electric heating solutions utilizing thin, flexible film elements installed beneath floor coverings. These films typically rely on carbon paste or specialized metallic alloys printed onto PET or similar durable substrates, generating radiant heat when electricity is passed through them. The core products are designed for maximizing thermal comfort while minimizing energy consumption compared to traditional convection heating systems. Major applications span residential buildings, where they are favored for new construction and renovation projects, as well as various commercial settings, including offices, hotels, and retail spaces that require discrete, efficient, and evenly distributed heating. The inherent simplicity and robustness of the film structure contribute significantly to their long operational lifecycle and minimal maintenance requirements, further cementing their value proposition in the modern construction ecosystem. Manufacturers are continually innovating to improve the efficiency of conductive inks and the thermal stability of the base polymer films to meet stringent performance benchmarks demanded by regulatory bodies and sophisticated consumers globally.

The primary benefits of utilizing underfloor heating film include exceptional energy efficiency due to precise zone control, aesthetic appeal derived from the elimination of bulky radiators, and the provision of superior indoor air quality by reducing dust circulation often associated with forced-air systems. Furthermore, the low profile and ease of installation in dry environments make heating films particularly appealing for retrofitting projects and installations involving floating floors, laminate, or engineered wood. This flexibility allows for seamless integration into various architectural designs without compromising aesthetic vision or structural integrity. The radiant heating mechanism mimics natural warmth, providing a highly comfortable environment at a lower ambient air temperature than forced air, contributing directly to energy savings while enhancing occupant well-being. This technology provides a future-proof heating solution compatible with low-energy housing models and adheres to modern architectural minimalist trends.

Key driving factors influencing the market trajectory include stringent governmental regulations promoting energy conservation in buildings, increasing consumer preference for smart home technologies integrated with heating systems, and the rising trend of sustainable and aesthetically pleasing interior design. The rapid expansion of the construction sector globally, especially in regions experiencing cold climates and possessing high energy costs, further contributes to the robust demand for energy-efficient heating solutions, positioning underfloor heating film as a critical component in modern building management systems. Moreover, competitive advantages in installation speed over wet systems, coupled with decreasing manufacturing costs through scale economies and technological refinement, are accelerating market penetration beyond traditional European strongholds and into fast-developing Asian metropolitan areas, particularly where quick deployment is valued.

The Underfloor Heating Film Market is poised for substantial growth, projected to achieve a significant Compound Annual Growth Rate (CAGR) over the forecast period, driven by sustained global emphasis on energy-efficient building standards and heightened consumer awareness regarding thermal comfort and indoor air quality. Current business trends indicate a strong movement toward smart integration, where heating films are linked to sophisticated building management systems (BMS) and IoT platforms, allowing for remote operation, predictive maintenance, and optimized energy usage based on real-time occupancy data. Furthermore, manufacturers are focusing heavily on developing ultra-thin, highly durable, and easily installable products to capture the burgeoning renovation and DIY markets, particularly in European and North American residential sectors. Strategic partnerships between film manufacturers and smart thermostat providers are defining the competitive landscape, creating integrated solutions that simplify the user experience and maximize energy savings, thereby driving product differentiation and enhancing long-term value proposition.

Regional trends highlight that Europe maintains the dominant revenue share, attributed to established regulatory frameworks mandating high levels of energy performance in residential and commercial constructions, coupled with high adoption rates of radiant heating systems. The mature market infrastructure and established distribution networks in countries like Germany and the UK contribute to stable and consistent growth. Critically, Asia Pacific (APAC) is projected to be the fastest-growing region, fueled by rapid urbanization, significant infrastructure development, and increasing disposable income allowing consumers to invest in advanced home comfort technologies, especially in countries like China and South Korea, which have long traditions and high cultural preference for floor heating systems. North America also demonstrates steady growth, propelled by the luxury home market and the desire for customized, zone-specific heating solutions that offer superior efficiency and comfort without the complexity of traditional hydronic systems, catering to the region’s strong focus on technological convenience.

Segment trends reveal that the Residential application segment holds the largest market share, primarily due to the high volume of new housing starts and extensive renovation activity focusing on modernization and enhanced comfort standards. This segment is characterized by demand for simple, safe, and reliable solutions suitable for intermittent use. Within product types, Carbon Films currently dominate due to their cost-effectiveness and proven performance across various floor types, offering the most accessible entry point for consumers. However, the Metal Film segment, specifically Amorphous Metal Films, is gaining critical traction due to superior thermal conductivity and faster heat-up times, appealing increasingly to premium segments requiring rapid heating response and high energy efficiency. Distribution channel analysis indicates a growing importance of specialized distributors who offer technical expertise to contractors, and increasingly, agile online retail platforms, which facilitate easier access for smaller contractors and direct consumers seeking detailed product specifications, comparative pricing, and immediate availability, fundamentally altering the traditional supply model.

Common user questions regarding AI's impact on the Underfloor Heating Film Market primarily revolve around how AI can optimize energy consumption, predict system failures, and seamlessly integrate heating films into broader smart home ecosystems for truly autonomous control. Users seek information on advanced AI algorithms that can learn complex occupant routines and behavioral patterns to preheat specific zones optimally, inquire about AI-powered diagnostics for proactive maintenance and fault isolation within the film matrix, and express significant interest in predictive modeling that dynamically links real-time weather fluctuations and volatile energy pricing signals directly to optimized heating schedules. The key thematic concerns consistently underscore the achievement of verifiable efficiency gains, delivery of highly personalized thermal comfort settings, and the potential for AI to dramatically simplify complex system management while simultaneously reducing overall operational costs, positioning AI as a crucial and transformative enabler for next-generation, intelligent radiant heating solutions.

The Underfloor Heating Film Market is propelled by strong Drivers centered around the global mandate for sustainable, low-carbon building practices and a clear rise in consumer investment capacity for premium home comfort systems. Specifically, the regulatory push toward nearly Zero Energy Buildings (nZEB) across the EU and comparable energy efficiency frameworks in North America and Asia necessitates highly efficient heating solutions. The film technology perfectly addresses this need due to its direct radiant nature, low operational temperature requirements, and seamless compatibility with modern renewable energy sources. However, pervasive market adoption faces significant structural Restraints, principally the relatively high initial installation cost compared to simplified baseboard or conventional forced-air heating methods, and the lingering perception of technical complexity in retrofitting existing buildings without significant structural intrusion. This restraint is gradually being mitigated by advanced dry installation techniques and pre-manufactured modular systems. Tremendous Opportunities exist, particularly driven by large-scale smart city initiatives globally and the technological imperative for integrating heating films with renewable energy sources and advanced IoT platforms, which opens new avenues for sophisticated, decentralized, and predictive climate control, thereby maximizing utility efficiency and user satisfaction. These market dynamics are continuously shaped by formidable Impact Forces, including ongoing rapid technological innovation in film materials leading to higher heat output and operational resilience, and the continuously evolving landscape of stringent environmental and electrical safety regulations that preferentially favor certified, electrically sound heating systems.

Primary drivers include the stringent implementation of updated national and regional building codes and the increasing voluntary adoption of green building certifications (e.g., LEED, BREEAM). The film’s intrinsic capacity to provide instantaneous, highly efficient radiant heat is a major market differentiator, perfectly aligning with modern sustainability goals and consumer demand for eco-friendly products that reduce lifetime carbon footprints. Furthermore, the provision of superior, even thermal comfort, emanating uniformly from the floor surface, is a crucial ergonomic and physical benefit highly valued, sustaining robust demand particularly in the high-end residential and commercial hospitality sectors where occupant experience is paramount. The system's optimal efficiency at lower running temperatures also renders it exceptionally well-suited for integration with high-efficiency renewable technologies such as modern air and ground source heat pump systems, representing a significant and powerful long-term catalyst for sustained market growth and technology pairing.

Effectively addressing the core restraints is paramount for realizing the full, scalable market potential. The requirement for specialized electrical or heating installers in certain highly regulated geographies, coupled with the substantial initial investment outlay for advanced materials and certified labor, can be a major deterrent for cost-sensitive developers and consumers in emerging markets. Crucially, a persistent educational barrier exists; many potential buyers and even a significant proportion of general contractors remain insufficiently informed about the substantial, verifiable long-term energy savings and lifecycle cost advantages that decisively offset the initial purchase expenditure over the system's operational lifespan. To counteract these barriers and stimulate wider adoption, leading manufacturers are intensely focusing their efforts on designing standardized, simplified, and pre-packaged DIY-friendly installation kits, offering comprehensive, multi-modal training programs for contractors, and utilizing sophisticated digital tools to provide transparent, comprehensive lifecycle cost-benefit analyses to all prospective customers, effectively demolishing the perception of prohibitively high investment risk and technical complexity. Competitive pressure exerted by traditional forced-air and established hydronic Underfloor Heating (UFH) systems further dictates a relentless pursuit of innovation in film efficiency, safety certification, and radical cost optimization across the entire production and distribution value chain.

The Underfloor Heating Film Market segmentation provides a crucial, granular view of market dynamics based on product type, application, installation method, and distribution channel. Analyzing these segments helps stakeholders understand areas of highest potential growth, competitive intensity, and specialized technological requirements. The market is primarily categorized into Carbon Films and Metal Films, with each type serving distinct performance envelopes and budgetary needs. Carbon films benefit from low manufacturing cost, high flexibility, and wide compatibility across diverse floor finishes, positioning them as the volume leader in many emerging markets. Conversely, metal films target high-performance installations and premium market segments due to their superior efficiency, leading to a competitive dynamic where cost-efficiency battles high-performance capability. Application segmentation clearly delineates the resilient demand originating from the Residential sector, driven by comfort and renovation needs, versus the growing, high-specification requirements of the Commercial sector, which mandates complex system integration and robust warranties. Installation and distribution methods further define the accessibility, speed of deployment, and final cost structure of the product for the end-user, indicating a strong pivot towards standardized dry installation techniques and highly efficient online sales channels that bypass traditional wholesale layers.

The performance differential between product segments is highly critical; Carbon Films offer broad market appeal due to their intrinsic cost efficiency and structural flexibility, dominating standard, large-volume installations, particularly under laminate, LVT, and engineered wood. This segment sees fierce price competition, with manufacturers focusing heavily on supply chain optimization and maximizing production scale to maintain margins. Conversely, Metal Films, particularly those utilizing advanced amorphous metals or specialized heating alloys, command a significant price premium due to features such as superior thermal conductivity, higher uniform thermal output per square meter, exceptional product longevity, and significantly faster heat-up times. These attributes appeal specifically to premium residential sectors and commercial spaces where rapid environmental response, low electromagnetic interference (EMI), and highly consistent performance over large areas are mandated. This technological differentiation is a key competitive tool, driving manufacturers to invest heavily in refining metal deposition techniques and composite material science to enhance output while controlling the underlying production costs, thus maintaining high margins in the premium market.

From a demand perspective, the renovation and retrofit market within the Residential application segment represents a significant and steadily increasing revenue stream globally, especially in mature markets like Europe and North America. The film’s ultra-thin profile minimizes floor height buildup—a highly sought-after functional advantage over traditional screed-based heating systems—making it the preferred solution for existing structures where floor level changes are restricted. The competitive landscape in this segment favors companies offering complete, easy-to-install kits with clear instructions and strong consumer support. Conversely, the Commercial sector, spanning modern high-rise office complexes, large format retail venues, and demanding hospitality facilities, requires robust, high-power density systems integrated seamlessly with comprehensive Building Management Systems (BMS). This necessitates heating films with advanced monitoring capabilities, robust safety certification, and centralized control interfaces. The industrial segment, though smaller in volume, requires highly specialized and durable films for specific localized heating needs or robust floor warming in highly corrosive or high-temperature manufacturing or storage environments, mandating materials like polyimide substrates and high-wattage densities, which significantly diversifies the required product portfolio and technological specialization.

The comprehensive Value Chain for the Underfloor Heating Film Market commences with the crucial Upstream Analysis stage, which is centered on the precise procurement and stringent quality processing of foundational raw materials. This stage demands the secure sourcing of high-purity, specified carbon paste (conductive inks), highly specialized metallic alloys (essential for manufacturing high-performance metal films), resilient and thermally stable polymer films such as polyethylene terephthalate (PET) or polyimide (PI), high-tolerance copper electrode strips, and advanced dielectric insulation layers. The consistency, chemical composition, and thermal stability of these raw materials are absolutely fundamental, directly dictating the final product's electrical performance, safety profile, operational lifecycle, and compliance with international standards. Key upstream participants are highly specialized chemical suppliers, niche flexible film manufacturers, and precision conductive printing service providers. Successfully navigating volatility in commodity prices for polymers, copper, and specialized metals, combined with ensuring the ethical and sustainable sourcing of components, presents a continuous operational and financial management challenge to manufacturers' cost structures and long-term margin goals. Establishing strategic, long-term supplier partnerships is necessary to maintain technological advantages in material quality, ensure supply consistency, and achieve cost optimization through volume purchasing.

Midstream activities encapsulate the core manufacturing processes, which involve complex techniques such as high-precision screen printing or advanced vapor deposition of the conductive material onto the polymer substrate, followed by highly controlled lamination, crucial polymer curing cycles, and multi-stage quality control testing. Quality assurance protocols typically mandate rigorous voltage resistance checks, high-pot testing, and infrared thermal imaging to instantaneously detect microscopic defects or inconsistencies that could lead to system failure. The manufactured films are then precisely cut, terminated with connectors, and packaged into specific voltage, width, and length configurations tailored for diverse end-user applications, ranging from small residential zones to large commercial installations. Operational efficiency in manufacturing, particularly minimizing material waste stemming from printing errors or lamination defects, is a major focus area. Industry leaders are making significant capital investments in automated, roboticized, and environmentally controlled manufacturing lines to guarantee product uniformity, high throughput, and minimize human error, which are essential for maintaining the stringent safety and performance credentials required for global exports and market confidence, thereby protecting brand equity and ensuring compliance.

The ultimate market success, brand reputation, and long-term end-user satisfaction of the underfloor heating film product are intrinsically linked to effective, standardized installation practices and highly responsive post-sales technical support. The Downstream phase is characterized by a dual channel approach. Direct channels, involving manufacturer representatives selling directly to large-scale construction firms and specialized system integrators, are vital for high-value commercial projects, as they ensure specialized training, guaranteed system integration guidance, and robust, project-specific warranty coverage, thereby successfully mitigating installation and long-term operational risks. Conversely, indirect channels, leveraging national wholesalers, authorized professional dealers, and large building supply retailers, target the mass market. This channel necessitates the production of standardized, simplified, and extensively tested product designs, accompanied by exceptionally clear, multi-lingual installation guides and online technical resources to minimize installation errors by less specialized residential contractors or DIY end-users. Additionally, managing the crucial integration complexity with peripheral electronic components—such as advanced proportional-integral-derivative (PID) thermostats, floor sensors, and proprietary smart home hubs—mandates robust and continuous collaborative partnerships between heating film manufacturers and specialized smart technology providers to deliver a comprehensive, intelligent, and truly functional climate control solution that maximizes user benefits while streamlining complex system operational management.

Potential customers for Underfloor Heating Film are highly segmented, spanning both the public and private construction domains, and are categorized primarily by their end-use environment, project scale, and procurement drivers. The largest and most robust group of customers is the Residential sector, encompassing individual homeowners engaged in renovation projects—who prioritize minimal floor height increase and quick, non-invasive installation—and large-scale property developers constructing high-end, energy-efficient housing complexes. These residential customers are primarily driven by the desire for superior comfort, enhanced aesthetics (due to invisible heating), long-term operational efficiency, and seamless, intuitive integration with emerging smart home technology platforms. The burgeoning trend of DIY installation in developed markets and the availability of simple pre-wired kits characterize a significant and expanding portion of this essential segment, demanding accessible product packaging and comprehensive online support resources tailored to non-professional installers.

The second major and highly lucrative segment comprises Commercial End-Users, including large multinational corporations developing modern, LEED-certified office buildings, specialized retail chains opening high-traffic outlets, and the expansive hospitality sector, such as luxury hotels and resorts, seeking premium, quiet, and comfortable heating solutions that significantly enhance the overall guest experience. For these customers, the purchasing criteria are highly technical, focusing on proven reliability, mandated low maintenance costs over long cycles, precise zone control (which is critical for efficient energy management across extensive and varied floor plans), and absolute, certified compatibility with centralized Building Management Systems (BMS) for centralized control and diagnostics. Specific high-demand niches within this category include healthcare facilities and senior living residences, where gentle, radiant heat is preferred for its hygienic properties, ease of cleaning, and enhanced patient comfort levels, minimizing air disturbances inherent in forced-air systems.

Furthermore, government and institutional buyers, such as public housing authorities, educational establishments, and municipal facilities, represent highly influential bulk purchasers. Their procurement decisions are often driven not only by initial capital cost but also by strict adherence to regulatory energy performance standards, documented long-term operational sustainability metrics, and comprehensive lifecycle costing models, favoring products with verifiable efficiency certifications and extended warranties. Finally, specialist market segments, including manufacturers of modular housing units, temporary disaster relief shelters, and specialized transportation (e.g., high-speed rail or marine vessel construction), rely heavily on the film’s unique properties: its lightweight nature, high performance-to-volume ratio, robust electrical safety features, and resistance to environmental factors. Effectively targeting these varied customer profiles requires highly tailored marketing, product specifications, and distinct distribution strategies, ranging from simple standardized film rolls for residential use to bespoke, high-voltage film mats delivered through direct, long-term contracts for commercial and institutional developments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 1,020 Million |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | REXVA, ThermoSphere, Daewoo E&C, EasyHeat, Warmup, Devi (Danfoss), Raychem (TE Connectivity), Uponor, Heatcom, Sunjo, Fenix, Energoonz, Electrolux, Stemme, Greenheat, Caleo, Warmfloor, Flexel, Warm-On, OJ Electronics |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Underfloor Heating Film market is currently undergoing dynamic evolution, primarily defined by relentless advancements in conductive materials, precision manufacturing techniques, and sophisticated control systems, all aimed at achieving superior energy efficiency, enhanced durability, and significant reductions in unit manufacturing cost. The foundational and still most widespread technology relies on specialized screen-printed carbon paste which is precisely applied onto robust polyethylene terephthalate (PET) or sometimes polyimide (PI) films, providing a thin, highly flexible, and structurally sound heating element. Recent innovations within the carbon film segment specifically focus on enhancing the uniformity and consistency of the carbon coating geometry and composition to ensure even heat distribution and prevent localized hot spots, thereby maximizing system safety and efficiency. Furthermore, substantial development is concentrated on integrating advanced safety features directly into the film architecture, such as embedded thermal cut-offs, over-current protection mechanisms, and utilization of non-halogenated, fire-retardant materials within the lamination layers, ensuring strict compliance with increasingly demanding global electric heating safety standards like UL and CE certifications, critical for market access and consumer trust.

A significant technological vector driving market differentiation is the increasing adoption of amorphous metallic alloys, often presented as ultra-thin ribbons or foils, used for the construction of premium-grade heating films. These specialized metallic materials exhibit vastly superior thermal conversion efficiency and substantially faster heat-up rates compared to standard carbon films. This high performance is attributed to their unique crystalline structure, low heat capacity, and optimized electrical resistance properties. While the production process for amorphous metal films is inherently more complex and costly than screen-printing carbon, commanding a price premium, they are highly favored in high-performance or rapid-response applications, such as high-end commercial offices or custom residential installations where rapid temperature modulation is essential. To make this technology more accessible, leading research and development efforts are concentrated on pioneering highly cost-effective and scalable deposition techniques, including advanced vacuum sputtering and refined chemical vapor deposition (CVD) methods, with the explicit goal of driving down unit production costs and expanding market share penetration into broader commercial applications.

Beyond the core heating element material science, critical technological advancements are deeply rooted in the peripheral control and management infrastructure. This involves the ubiquitous integration of modern wireless communication standards, including low-power protocols like Zigbee, Z-Wave, and ubiquitous Wi-Fi, directly into smart thermostats and sophisticated control panels specifically engineered for the electric film heating ecosystem. This advanced integration is vital, enabling seamless remote operation, granular energy consumption monitoring, and critical compatibility with voice assistants and large-scale smart grid infrastructure, facilitating Demand Response management. The future technology trajectory points definitively toward the integration of functional printed electronics capabilities, allowing for the embedding of highly sensitive temperature and performance sensors directly into the film structure. This breakthrough would enable hyper-localized temperature monitoring, real-time fault detection, and sophisticated predictive maintenance functions powered by continuous AI-driven data analytics, transforming the system from a passive heating element into an active, intelligent, and self-optimizing climate control network.

The global Underfloor Heating Film Market exhibits distinctly heterogeneous regional growth patterns, which are primarily dictated by local climate demands, the maturity of energy efficiency regulations, and the dynamics of the local construction industry. Europe currently maintains the dominant revenue share and overall market maturity, a position rooted in the continent’s aggressive and long-standing regulatory commitment to high energy efficiency standards, exemplified by initiatives like the nearly Zero Energy Building (nZEB) mandate, which favors highly efficient radiant heating solutions like heating film. Countries such as Germany, the UK, and the Nordic region show high penetration rates, effectively leveraging the film’s suitability for timber frame construction, minimalist aesthetics, and the substantial volume of residential renovation projects where minimal floor height build-up is critical. The consistent demand is heavily concentrated in the residential renovation segment, supported by high consumer disposable income and robust governmental schemes promoting home energy improvements and advanced climate control technologies, ensuring sustained market stability.

Asia Pacific (APAC) stands out as the primary growth engine and is projected to achieve the fastest Compound Annual Growth Rate (CAGR) globally over the forecast period. This rapid acceleration is a direct consequence of massive, unprecedented urbanization, expansive infrastructural development, and a substantial rise in middle-class disposable income, enabling greater consumer investment in modern home comfort systems across the region. South Korea, in particular, maintains a massive and culturally influential domestic market driven by the traditional preference for "ondol" (floor heating), which makes it a natural and high-volume environment for heating film adoption. The significant construction boom in China, coupled with increasing environmental awareness and supportive government subsidies for certified energy-saving appliances, is fueling a decisive switch from outdated centralized heating methods to modern, decentralized electric film systems, particularly within large multi-family residential complexes and newly built commercial towers seeking international green building certifications.

North America demonstrates strong, consistent growth, primarily concentrated around the high-end residential market and regions experiencing significant seasonal temperature extremes, particularly the Northeast and parts of Canada. The ease and speed of dry installation—a method strongly preferred for the ubiquitous wood subfloors in the U.S. and Canada—makes heating film an extremely attractive and less labor-intensive alternative to complex hydronic systems. Market expansion is further augmented by the region's technological leadership, with high rates of integration of these film systems into sophisticated smart home management platforms, appealing to a consumer base highly receptive to automation and data-driven energy optimization. Conversely, the Middle East and Africa (MEA) and Latin America currently represent smaller, but strategically important, market shares. Growth in these regions is highly localized, driven primarily by luxury real estate development in high-income hubs (like the GCC nations) and selective adoption in temperate areas requiring energy-efficient auxiliary or primary heating solutions during specific cooler seasons, suggesting high future potential once regulatory environments mature and focus shifts toward sustainable building practices.

Underfloor heating film offers superior energy efficiency, achieves silent and uniform radiant heat distribution, eliminates visible components like radiators for aesthetic benefit, and significantly reduces dust circulation, thereby improving indoor air quality. Its low profile is ideal for installation beneath thin floor coverings without substantially raising floor height.

Underfloor heating film typically operates at lower temperatures than conventional convection systems while maintaining equivalent comfort levels. Savings vary but can range from 15% to 40% on heating bills, especially when coupled with smart thermostats that enable precise zone control and AI-driven predictive scheduling based on occupancy and external temperature fluctuations.

Yes, underfloor heating film is highly suitable for renovation and retrofit applications due to its thin design, which minimizes required floor buildup compared to wet screed systems. This feature makes it particularly advantageous for older homes or projects where preserving ceiling height is a priority, allowing for quick, dry installation beneath laminate or engineered wood floors.

High-quality underfloor heating film systems are designed for exceptional durability, often offering lifespans exceeding 25 to 30 years, matching or exceeding the structural life of the building itself. Once properly installed and electrically connected, they are virtually maintenance-free, as they contain no moving or consumable parts, ensuring long-term operational stability.

Carbon Film is generally more cost-effective and flexible, utilizing printed carbon paste for heat generation, making it dominant in mass-market residential applications. Metal Film (often amorphous alloys) offers higher thermal conductivity and faster heat-up times, positioning it as a premium option for installations demanding rapid response and superior energy performance, often required in high-end commercial settings.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.