ID : MRU_ 432560 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

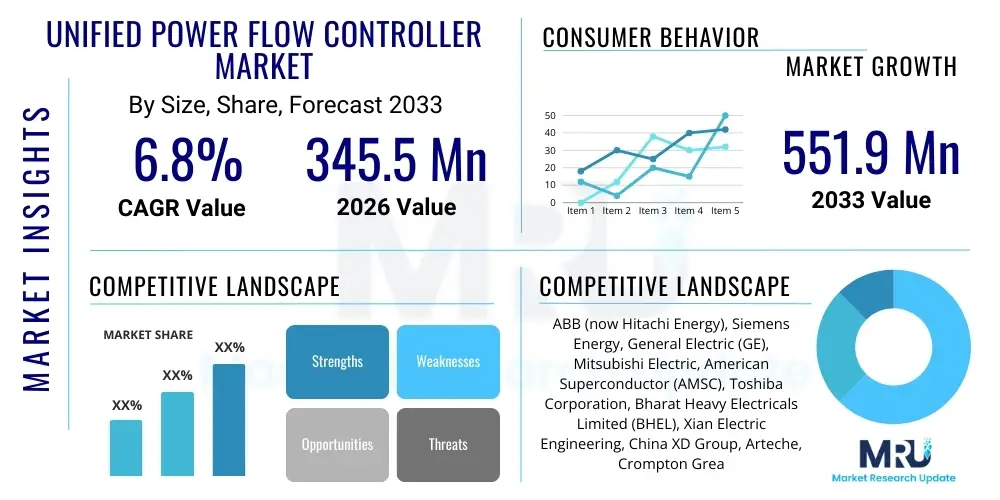

The Unified Power Flow Controller Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 345.5 Million in 2026 and is projected to reach USD 551.9 Million by the end of the forecast period in 2033.

The Unified Power Flow Controller (UPFC) Market is centered around advanced Flexible AC Transmission System (FACTS) devices designed to optimize power flow, enhance transient stability, and maximize the utilization of existing transmission infrastructure. UPFC is recognized as the most versatile and powerful FACTS device, capable of independently and simultaneously controlling three critical transmission line parameters: line impedance, terminal voltage magnitude, and phase angle. This comprehensive control capability allows system operators to effectively manage complex power grids, especially those integrating large volumes of intermittent renewable energy sources, thereby maintaining grid reliability and reducing congestion.

The core functionality of a UPFC involves connecting two voltage-sourced converters (VSCs) back-to-back using a common DC link, with one converter connected in series with the transmission line and the other connected in shunt. The shunt converter primarily controls the voltage magnitude of the DC link and facilitates reactive power exchange with the AC system, while the series converter injects a voltage of controllable magnitude and phase angle in series with the line, providing precise control over active and reactive power flows. Major applications span high-voltage transmission networks where bottlenecks exist or where dynamic stability issues threaten supply security.

The primary benefits driving the adoption of UPFC include significant improvements in power transfer capacity, enhanced system damping of power oscillations, and highly flexible management of loop flow and transmission line loading. Driving factors for market growth include global initiatives toward grid modernization, the mandatory integration of utility-scale renewable energy (such as wind and solar farms), increasing concerns over transmission constraints due to aging infrastructure, and the regulatory push for greater efficiency in power delivery systems across densely populated and industrialized regions. The ongoing deployment of Smart Grid technologies further accelerates the need for sophisticated dynamic controllers like UPFC.

The Unified Power Flow Controller (UPFC) market is undergoing robust expansion, fundamentally driven by the global imperative for transmission system upgrades and the massive influx of distributed and variable renewable generation into existing electrical grids. Business trends show a strategic shift among leading manufacturers towards developing modular, standardized, and high-voltage direct current (HVDC) compatible UPFC systems, enhancing ease of deployment and reducing overall installation costs, addressing one of the primary historical restraints of this complex technology. Furthermore, the market is characterized by increasing R&D investments aimed at leveraging advanced semiconductor materials, such as Silicon Carbide (SiC) and Gallium Nitride (GaN), to improve converter efficiency and reduce the physical footprint of these large installations, crucial for utility acceptance.

Regional trends indicate that Asia Pacific (APAC) holds the largest market share and exhibits the fastest growth trajectory, predominantly fueled by extensive governmental investments in large-scale power infrastructure projects in countries like China and India, necessitated by rapid industrialization and urbanization. North America and Europe, while representing mature markets, show steady growth driven by the need to replace aging infrastructure and integrate complex renewable energy corridors across wide geographical areas. Regulatory initiatives promoting cross-border power trading and system reliability mandates in Europe further solidify the demand for advanced control devices such as UPFC to manage intricate power transfer paths efficiently.

Segmentation trends highlight that the Component segment is dominated by the Voltage Source Converters (VSCs), which form the technological core of the UPFC, requiring continuous innovation in semiconductor technology and control algorithms. In terms of Application, the High Voltage Transmission segment retains the largest share, as UPFCs are primarily deployed in high-power, critical transmission pathways to enhance stability and power transfer limits. Emerging segments include integration with microgrids and deployment in specialized industrial power systems, although the utility transmission sector remains the backbone of the UPFC market demand.

User inquiries concerning AI's influence on the Unified Power Flow Controller (UPFC) market frequently revolve around how artificial intelligence and machine learning (ML) algorithms can optimize the complex, real-time control decisions inherent in UPFC operations. Users commonly ask about the effectiveness of predictive maintenance schedules informed by AI to reduce UPFC downtime, the ability of ML models to forecast power flow disturbances accurately, and the utilization of deep reinforcement learning (DRL) to dynamically adjust series and shunt injection parameters for maximum system stability and minimal energy loss under fluctuating grid conditions. Key themes center on enhanced operational efficiency, autonomous fault detection, and the transition from reactive control mechanisms to highly predictive and prescriptive grid management enabled by advanced analytics.

The integration of AI significantly elevates the performance ceiling for UPFC systems. Traditional control systems rely on pre-defined models and control rules, which can struggle to adapt instantaneously to unforeseen system contingencies or highly variable renewable generation patterns. AI models, particularly those utilizing deep learning, can analyze massive datasets encompassing historical fault records, weather patterns, real-time sensor data, and grid topology changes to derive optimized control strategies far exceeding human or conventional algorithmic capabilities. This data-driven approach allows the UPFC to transition from a fixed control device to an intelligent, self-optimizing asset within the broader Smart Grid ecosystem, justifying the high capital expenditure associated with deployment.

Furthermore, AI-powered diagnostics enhance the reliability of UPFC equipment, which is critical given the complexity and cost of the converters. Machine learning algorithms can identify subtle, early-stage component degradation—such as anomalies in converter valve temperatures or DC link capacitance fluctuations—that precede catastrophic failures. By accurately predicting component lifespan and scheduling maintenance precisely when necessary, utility operators can maximize the uptime of these crucial grid stabilizing devices, thereby increasing the effective return on investment. This predictive maintenance capability, facilitated by AI, addresses long-standing user concerns regarding the complexity and operational expenditure (OPEX) associated with managing sophisticated FACTS devices.

The dynamics of the Unified Power Flow Controller (UPFC) market are shaped by a complex interplay of powerful drivers, significant restraints, and emerging opportunities, collectively determining the market trajectory. The paramount driver is the worldwide shift toward renewable energy sources, which introduces severe volatility and non-linearity into traditional AC power grids, necessitating sophisticated power electronics like UPFC to ensure stability, power quality, and reliable transmission. Coupled with this is the critical need for grid modernization and increased transmission capacity utilization, often driven by regulatory pressure to defer or eliminate costly new line construction. The primary restraint remains the extremely high capital cost associated with UPFC installation, which includes high-power semiconductor valves and extensive control infrastructure, alongside the complexity involved in integrating these advanced FACTS devices into legacy transmission infrastructure. Opportunities arise from the evolution of Smart Grids, the integration of UPFC with High-Voltage Direct Current (HVDC) systems for hybrid control solutions, and the development of modular and standardized designs that can potentially lower deployment hurdles and complexity.

Impact forces currently favoring market acceleration include governmental mandates supporting energy security and decarbonization goals, which allocate substantial funding towards grid infrastructure capable of managing highly complex bidirectional power flows. The regulatory environment in developed economies, particularly Europe, imposes strict penalties for grid instability or failure to meet reliability standards, compelling utilities to invest in the most effective stabilization technologies available, positioning UPFC as a premium solution. Furthermore, technological advances in power electronics, specifically the commercialization of high-power SiC and GaN devices, are gradually addressing the restraint of cost and physical size, increasing the feasibility of UPFC deployment in constrained substations and facilitating higher efficiency operations, thereby enhancing their attractiveness compared to older FACTS alternatives like Static VAR Compensators (SVCs) or Thyristor Controlled Series Compensators (TCSCs).

Conversely, restraining forces include the highly specialized expertise required for the operation and maintenance of UPFC systems, leading to workforce skill gaps in several developing regions. Competitive threats also arise from alternative, less costly FACTS solutions, even if they offer less comprehensive control capabilities, particularly in budget-sensitive markets. However, the unique ability of UPFC to control both active and reactive power flow simultaneously and independently provides a significant, often necessary, performance advantage in highly meshed and heavily loaded transmission networks where precise power delivery is paramount. The increasing frequency and severity of extreme weather events, which test grid resilience, also act as an indirect driver, forcing utilities to adopt dynamic control technologies that can recover system stability rapidly following transient faults, further cementing the long-term potential of the UPFC market despite high initial costs.

The Unified Power Flow Controller market is comprehensively segmented primarily by component, application, and geographical region. Understanding these segmentation metrics is crucial for identifying areas of highest investment and technological development. The component segmentation dissects the UPFC system into its core hardware elements, with Voltage Source Converters (VSCs) representing the most complex and high-value segment, demanding continuous innovation in high-power semiconductor switches and thermal management systems. The application segment delineates where these powerful devices are primarily utilized, with high-voltage transmission networks dominating the demand landscape, focused on bulk power transfer and grid stability enhancement across long distances. This structure allows market participants to tailor their technological offerings and strategic marketing efforts to specific utility needs and regulatory environments globally.

Within the Component segment, the DC Link Capacitors and Bypass Switches, while less technologically complex than the VSCs, represent essential high-reliability components that significantly impact the overall system footprint and transient response capabilities. The continuous evolution towards higher voltage and current ratings necessitates robust engineering and manufacturing standards across all subsystems. In terms of Application, while transmission remains the core market, the deployment of UPFC technology in specialized industrial applications, particularly those requiring ultra-high power quality and fault ride-through capabilities, is slowly emerging. The complexity of UPFC generally confines its use to major utility projects, making government procurement and long-term infrastructure planning essential elements influencing purchasing decisions across all segments.

Geographical segmentation reveals stark differences in market maturity and growth potential. Developed regions like North America and Europe focus heavily on upgrading existing infrastructure for renewable integration and optimizing cross-border flows, necessitating high-specification UPFC systems. In contrast, the APAC region's growth is volume-driven, fueled by extensive new grid development and the creation of large super-grids to support rapidly expanding industrial and residential energy needs. Successful market penetration therefore requires regionally nuanced strategies, addressing varying grid codes, regulatory frameworks, and local content requirements prevalent in these diverse geographical markets.

The value chain for the Unified Power Flow Controller market is highly specialized and knowledge-intensive, beginning with the upstream supply of critical semiconductor materials and high-power electronic components. Upstream activities involve the procurement of high-voltage Insulated Gate Bipolar Transistors (IGBTs) or emerging Wide Bandgap (WBG) devices like SiC, DC link capacitors, and high-quality magnetics, where supplier relationships with specialized electronic component manufacturers like Infineon, ABB Power Grids, and Mitsubishi Electric are crucial. Due to the stringent reliability requirements of grid-scale equipment, quality control and component longevity verification at this stage are paramount, heavily influencing the final performance and cost of the UPFC system. Technological advancements and availability of newer, higher-efficiency semiconductors directly impact the competitive edge of system integrators.

The core value addition occurs during the manufacturing and system integration phase, which involves specialized engineering design, precise assembly of the shunt and series converters, and development of sophisticated control and protection software. Major system integrators, such as Siemens Energy and GE, possess the proprietary algorithms and intellectual property necessary to coordinate the real-time operation of the VSCs and integrate the unit seamlessly with existing utility Supervisory Control and Data Acquisition (SCADA) systems. The distribution channel is predominantly direct, involving large-scale public utility providers or transmission system operators (TSOs) acting as the main buyers. Due to the bespoke nature and complexity of high-power UPFC installations, sales are primarily project-based, requiring long tender processes and direct contractual relationships between the manufacturer and the end-user.

Downstream analysis focuses on installation, commissioning, operation, and maintenance (O&M) services, which represent a significant long-term revenue stream. Installation requires highly skilled field engineers, and O&M contracts often span several decades, incorporating software updates, hardware monitoring, and replacement of semiconductor valves. Indirect distribution channels are minimal, typically restricted to consulting engineering firms that act as intermediaries, advising utilities on technology selection and project specifications rather than physically distributing the product. The trend toward modular design aims to simplify downstream logistics and installation, reducing time-to-market and project risk for the utilities, ultimately enhancing the overall value proposition across the entire chain.

The primary and most significant customers in the Unified Power Flow Controller market are large national and regional Transmission System Operators (TSOs) and Independent System Operators (ISOs). These entities are responsible for the reliable and secure operation of high-voltage transmission grids and have a mandated requirement to maintain power quality and stability, particularly in corridors heavily constrained by physics or aging infrastructure. The decision to invest in a UPFC is typically driven by strategic grid planning objectives, such as maximizing the power transfer capability of existing lines (thereby deferring capital expenditure on new line construction) or solving complex loop flow problems that negatively impact surrounding utilities. Therefore, governmental utilities and large private electricity corporations constitute the core buying segment.

A secondary, but growing, customer base includes large industrial complexes or entities involved in the integration of large-scale renewable energy generation into the bulk transmission system. Renewable energy developers, particularly those managing large solar or wind farms located far from demand centers, may require advanced FACTS devices like UPFC to mitigate system impacts and ensure compliance with stringent grid code requirements regarding voltage stability and fault ride-through capability. Furthermore, specialized government agencies managing critical infrastructure, such as high-security research laboratories or defense installations that require extremely reliable and fault-tolerant power supplies, also represent niche, high-value end-users.

In regions like the European Union, where cross-border energy trade is extensive, potential customers include collaborative regional power pools or interconnector owners who utilize UPFCs to precisely control power flow between synchronous zones, avoiding undesirable circulation currents and optimizing market efficiency. For all customer segments, the purchasing criteria are heavily weighted toward system reliability, proven performance history in high-stress environments, vendor expertise in control systems, and the long-term availability of maintenance and technical support, reflecting the mission-critical nature of the installed equipment.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 345.5 Million |

| Market Forecast in 2033 | USD 551.9 Million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ABB (now Hitachi Energy), Siemens Energy, General Electric (GE), Mitsubishi Electric, American Superconductor (AMSC), Toshiba Corporation, Bharat Heavy Electricals Limited (BHEL), Xian Electric Engineering, China XD Group, Arteche, Crompton Greaves, Fuji Electric, Hyundai Electric & Energy Systems, NKT A/S, Schneider Electric, Eaton Corporation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Unified Power Flow Controller market is defined by continuous advancements in power electronics and sophisticated control algorithms, moving towards greater efficiency, smaller footprints, and enhanced dynamic response. At the core of UPFC technology are high-power semiconductor switches, traditionally based on Silicon (Si) Insulated Gate Bipolar Transistors (IGBTs). However, the industry is witnessing a significant transition toward Wide Bandgap (WBG) materials such as Silicon Carbide (SiC) and, potentially, Gallium Nitride (GaN) devices. These materials offer superior switching speeds, reduced power losses, and the ability to operate at higher temperatures and voltages, which directly translates into more compact converter designs and improved overall system efficiency, mitigating the historical bulkiness and energy losses associated with older UPFC designs. This material evolution is critical for achieving the high reliability demanded by utility-scale operations.

In parallel with hardware advancements, the market emphasizes the development of highly resilient and intelligent control systems. Modern UPFC systems utilize advanced control theories, including predictive control and adaptive control mechanisms, often enhanced by artificial intelligence, to manage the complex interaction between the series and shunt converters in real time. The integration of advanced digital signal processing (DSP) platforms allows for sub-cycle response times, crucial for damping low-frequency power oscillations and rapidly restoring stability following major system faults. Furthermore, significant research is focused on modular multi-level converter (MMC) topologies for UPFC applications. While MMCs are widely used in HVDC, their application in FACTS devices, particularly UPFCs, offers advantages in harmonic performance and modular redundancy, enabling higher system availability and simplified scalability compared to traditional two- or three-level converters.

Another crucial area of innovation is the development of reliable cooling and protective mechanisms. As power density increases due to WBG devices, efficient thermal management, often relying on advanced liquid cooling systems, becomes essential to ensure the longevity of semiconductor switches. Protection systems are also evolving, incorporating advanced fault detection and isolation schemes to prevent damage during severe transient events. Finally, interoperability standards and communication protocols (such as IEC 61850) are central to the seamless integration of UPFCs into modern utility substation automation and Smart Grid architectures, allowing TSOs to leverage these assets for comprehensive, grid-wide optimization and flow management.

North America is characterized by a mature energy infrastructure and stringent regulations concerning grid reliability and resilience. The region's UPFC market growth is primarily driven by the ongoing modernization of the aging transmission grid and the significant challenges associated with integrating massive volumes of intermittent renewable energy, especially wind power from the Midwest and solar energy from the Southwest, into distant load centers. Utilities in the U.S. and Canada utilize UPFC technology strategically to mitigate power flow bottlenecks, increase the transfer capacity of existing rights-of-way, and enhance the dynamic stability of long-distance transmission corridors, addressing the limitations imposed by physical grid constraints.

Investment in UPFC deployment is heavily influenced by state-level Renewable Portfolio Standards (RPS) and federal initiatives aimed at developing a resilient Smart Grid. The high average age of transmission equipment necessitates advanced solutions to maximize utilization without incurring the massive capital costs and regulatory delays associated with building new lines. Furthermore, the increasing interdependence of regional grids (managed by ISOs like PJM, CAISO, and ERCOT) demands high-precision flow control capabilities, making UPFC an optimal, albeit expensive, solution for managing scheduled and unscheduled power transfers and preventing cascading failures across large interconnections.

Europe’s UPFC market is defined by the massive Energy Transition (Energiewende) and the highly interconnected nature of its national grids. The necessity for advanced FACTS devices stems from the high penetration of decentralized generation, particularly offshore wind, and the regulatory push for increased cross-border power trading. UPFCs are strategically deployed at critical interconnections and transmission boundaries to manage complex loop flows, ensure contractual power exchange fulfillment, and maintain system stability despite fluctuating internal and external power flows.

The European market benefits from strong governmental support and EU directives promoting grid optimization and resilience. Countries like Germany, the UK, and Spain, facing significant challenges in balancing supply and demand from variable sources, are early adopters of advanced FACTS technologies. While the high initial cost remains a barrier, the cost of grid failure and the penalties associated with non-compliance with ENTSO-E grid codes often justify the investment in comprehensive solutions like UPFC. R&D in Europe also focuses heavily on standardized, modular solutions to accelerate deployment across diverse national networks.

The Asia Pacific region represents the fastest-growing market globally, characterized by unprecedented demand for electricity driven by rapid industrialization, urbanization, and ambitious national electrification programs, particularly in China and India. The market dynamics here are volume-driven, necessitating massive investment in new transmission infrastructure, often involving the construction of high-power super-grids and long-distance transmission links to bridge the vast distances between generation sources (e.g., hydro and remote renewable energy zones) and coastal industrial hubs.

In APAC, UPFC adoption is tied to large-scale government-backed projects focused on establishing ultra-high-voltage (UHV) transmission networks and enhancing power quality in burgeoning industrial corridors. While cost sensitivity is higher than in Western markets, the sheer scale of infrastructural development allows for the integration of UPFCs into foundational grid planning. Japan and South Korea, possessing highly advanced but geographically constrained grids, focus on utilizing UPFCs to maximize power density and stability within urban and existing industrial areas, while China remains the largest installer due to its extensive transmission build-out.

The Latin American market for UPFC technology is developing, driven primarily by investments in hydroelectric power transmission and mineral extraction industries requiring reliable power supplies. Countries like Brazil, with expansive transmission networks linking remote hydropower generation to dense urban centers, face significant challenges related to line reactance and power oscillation damping, making advanced FACTS devices necessary for stability. However, the market faces restraints related to economic volatility and reliance on foreign technology providers.

Market penetration relies heavily on governmental concessions and large private utility investments focused on enhancing the resilience of critical infrastructure. While the overall adoption rate is slower compared to APAC or North America, specific high-value projects aimed at maximizing the export capacity of large generation facilities provide consistent demand for UPFC technology. Improving local manufacturing capabilities and financing options are critical steps for sustained growth in this region.

The MEA region exhibits heterogeneous market characteristics. The Middle East, particularly the Gulf Cooperation Council (GCC) nations, shows increasing adoption driven by ambitious solar power initiatives and the need to stabilize interconnected national grids. High temperatures and harsh environmental conditions necessitate robust, specially engineered UPFC systems. Investment is strong due to high energy revenues supporting major infrastructure projects focused on reducing dependence on oil-fired generation and building resilient future grids.

In Africa, the market is nascent but holds high potential, mainly driven by large-scale cross-border transmission projects designed to create regional power pools and integrate newly commissioned generation assets, often financed through international development banks. South Africa is a key player, focusing on stabilizing its existing grid infrastructure while integrating new utility-scale renewable energy. Challenges include inconsistent regulatory environments and funding difficulties, requiring project-specific financing solutions before UPFC technology can see widespread deployment.

A Unified Power Flow Controller (UPFC) is the most comprehensive type of Flexible AC Transmission System (FACTS) device, utilizing two back-to-back voltage-sourced converters (VSCs) connected in shunt and series. Its key distinction lies in its ability to independently and simultaneously control active power, reactive power, and the voltage profile of a transmission line, offering superior dynamic control compared to single-converter FACTS devices like SVCs or STATCOMs, which typically only control reactive power or voltage.

The primary drivers include the urgent necessity for grid stabilization due to the high integration of variable renewable energy sources (wind and solar) and the global mandate for transmission system operators (TSOs) to maximize the power transfer capacity of existing lines. UPFC deployment allows utilities to enhance stability, prevent congestion, and defer costly construction of new transmission corridors, addressing infrastructure aging and capacity constraints efficiently.

UPFCs are expensive due to the requirement for high-power, high-voltage semiconductor converters, complex control systems, and extensive substation infrastructure. Manufacturers are mitigating these costs by investing heavily in R&D focusing on Wide Bandgap (WBG) semiconductors (like SiC) which enable smaller, more efficient, and less complex cooling systems. Furthermore, modular design and standardization initiatives aim to reduce engineering and installation complexity, lowering overall project expenditure.

The Asia Pacific (APAC) region currently dominates the UPFC market in terms of deployed capacity and projected growth rate. This growth is predominantly fueled by extensive governmental investments in large-scale transmission infrastructure expansion, particularly in China and India, aimed at supporting rapid industrialization, urbanization, and the integration of massive remote generation sources into nascent super-grids.

AI, particularly machine learning, enhances UPFC operations by enabling predictive control and maintenance. AI algorithms analyze complex real-time grid data to predict potential instabilities and dynamically adjust the UPFC's control parameters (voltage magnitude, phase angle) faster and more accurately than conventional systems. This capability maximizes system stability and reduces downtime through precise predictive diagnostics of critical components.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.