ID : MRU_ 432435 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

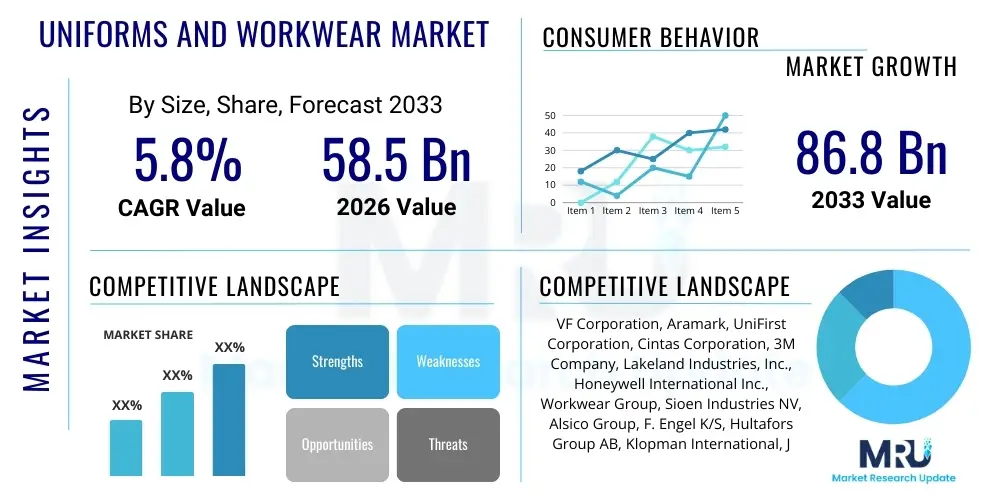

The Uniforms and Workwear Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 58.5 Billion in 2026 and is projected to reach USD 86.8 Billion by the end of the forecast period in 2033.

The Uniforms and Workwear Market encompasses specialized clothing designed to provide protection, enhance corporate identity, and ensure regulatory compliance across various industries. These products range from basic professional attire to highly technical Personal Protective Equipment (PPE) utilized in hazardous environments. Key product categories include industrial workwear, medical scrubs, corporate business wear, and specialized protective clothing for sectors such as oil and gas, construction, and firefighting. The primary objective of workwear transcends mere aesthetics, focusing heavily on functionality, durability, and employee safety, which remains the cornerstone of market demand.

Major applications of uniforms and workwear span extensive end-use industries. Healthcare and hospitality sectors are consistently high-volume consumers, driven by stringent hygiene requirements and the need for standardized professional presentation. Similarly, the manufacturing, construction, and chemical industries necessitate highly durable and protective garments engineered to mitigate risks associated with specific operational hazards, such as cuts, chemical exposure, or extreme temperatures. The rising global emphasis on occupational health and safety standards, particularly in developing economies, is substantially increasing the mandatory procurement of certified workwear, thereby fueling market expansion.

The market growth is primarily driven by mandatory government regulations enforcing worker safety across high-risk occupations. Furthermore, the increasing complexity of industrial processes and the resulting need for specialized protective gear, including fire-resistant, anti-static, and high-visibility clothing, sustain demand. The benefits offered by modern workwear—including enhanced employee morale through comfortable designs, superior brand recognition, and reduced liability risks associated with workplace accidents—contribute significantly to its sustained adoption globally. Technological advancements, such as the integration of smart textiles and sustainable materials, are transforming product offerings and attracting premium segment consumers.

The global Uniforms and Workwear Market is experiencing robust expansion, characterized by a significant shift toward technical textiles, sustainability, and sophisticated supply chain management. Business trends indicate a strong move away from generic apparel towards highly customized, functional garments that integrate advanced features like moisture-wicking capabilities, ergonomic designs, and integrated smart technology for health monitoring and location tracking. Consolidation among major vendors, coupled with increasing outsourcing of uniform management and laundry services, represents a key strategic development. Furthermore, the market is benefiting from the rapid expansion of logistics and e-commerce sectors globally, which necessitates large volumes of standardized, comfortable, and durable uniforms for warehousing and delivery personnel.

Regional trends highlight the dominance of North America and Europe, largely attributed to mature industrial safety regulations and high levels of technological adoption in manufacturing processes. However, the Asia Pacific (APAC) region is projected to register the fastest growth due to rapid industrialization, large-scale infrastructure projects, and the gradual but strict enforcement of occupational safety standards, particularly in China and India. In these emerging markets, rising disposable income and the professionalization of the service sector, including food service and retail, are creating substantial demand for corporate and hospitality uniforms. Conversely, fluctuating currency values and increasing labor costs in traditional manufacturing hubs present minor regional headwinds that influence sourcing decisions.

Segmentation trends reveal strong performance in the specialized protective clothing segment, driven by constant innovations in materials providing superior resistance to extreme hazards. The rental and laundry services segment is also witnessing accelerated growth, as companies across diverse industries opt for outsourced uniform management to reduce capital expenditure and ensure consistent maintenance and compliance. By material type, synthetic fibers continue to dominate due to their durability and cost-effectiveness, but there is a distinct consumer preference trend leaning toward sustainable materials like organic cotton and recycled polyester, especially in the corporate and service segments, aligning with global environmental, social, and governance (ESG) mandates.

User inquiries regarding AI in the Uniforms and Workwear Market commonly center on efficiency improvements, personalization at scale, and inventory management precision. Key themes include how AI can optimize manufacturing lead times, whether it can accurately predict material wastage, and its role in developing "smart" garments that truly enhance worker safety and productivity. Users are particularly concerned with the potential for AI-driven demand forecasting to minimize overstocking and reduce environmental impact, alongside expectations that machine learning algorithms will enable highly customized sizing and fit recommendations based on large demographic datasets, moving beyond traditional standard sizing charts.

The deployment of Artificial Intelligence tools is revolutionizing the traditionally conservative textile supply chain, primarily through predictive analytics and hyper-efficient inventory control. AI algorithms can analyze historical sales data, seasonal variations, and external macroeconomic indicators to generate highly accurate demand forecasts, significantly reducing the risk of both stockouts and excess inventory, which is crucial given the often long lead times for specialized technical textiles. Furthermore, generative AI is accelerating the design process, allowing manufacturers to quickly simulate the performance of new materials under various industrial stress conditions, thus streamlining research and development cycles and accelerating time-to-market for innovative protective wear solutions.

AI also plays a critical role in enhancing the functionality and lifecycle management of workwear. Machine learning is integral to processing data collected from smart uniforms—such as employee vital signs, exposure levels to heat or chemicals, and location data—to provide real-time risk assessments for improved operational safety. In the maintenance cycle, AI-powered systems can analyze wear-and-tear patterns on uniforms to recommend optimal washing cycles, timing for replacements, and repair strategies, extending the lifespan of high-value protective garments and optimizing the total cost of ownership for end-users, thereby injecting high-level operational efficiency into the uniform management ecosystem.

The dynamics of the Uniforms and Workwear Market are governed by a complex interplay of regulatory drivers, economic restraints, and technological opportunities, collectively shaping the direction and pace of growth. The most potent driver is the increasingly stringent global occupational safety legislation, necessitating specialized protective apparel in sectors like oil and gas, construction, and chemical manufacturing. Restraints primarily involve the volatile pricing of raw materials (such as high-performance synthetic fibers), the significant initial investment required for sophisticated smart workwear, and the logistical challenges associated with maintaining compliant uniform programs across large, decentralized workforces. Opportunities are predominantly centered around the integration of Internet of Things (IoT) technology, expansion into emerging markets, and the strong consumer movement toward sustainable and circular textile solutions.

Impact forces on the market are multifaceted, stemming from both internal industry innovations and external socio-economic pressures. The bargaining power of buyers is moderate to high, especially in large tenders from government agencies or multi-national corporations, which demand customized, bulk orders at competitive prices, often leading to competitive pricing pressures. Conversely, the bargaining power of suppliers, particularly those providing specialized technical fibers (like aramid or carbon fiber), is high due to limited alternatives and proprietary manufacturing processes. The threat of substitutes is relatively low, as standard clothing cannot replace certified protective workwear; however, the rise of advanced rental and leasing models acts as a form of substitution for outright purchase, influencing procurement strategies.

Technological impact forces are currently the strongest catalysts for market transformation. The rapid development of wearable technology and sensor integration is elevating workwear from passive protection to active safety monitoring tools. Furthermore, increasing public awareness of environmental accountability places continuous pressure on manufacturers to adopt eco-friendly production methods, use recycled or bio-based materials, and establish robust end-of-life garment recycling programs. This transition to a circular economy model, while presenting initial cost challenges, opens up significant opportunities for competitive differentiation and long-term brand equity enhancement, particularly attractive to corporate clients focused on demonstrating ESG commitment.

The Uniforms and Workwear Market is highly diversified, segmented based on product type, end-use industry, material, and distribution channel, reflecting the varied needs across the global workforce. The analysis highlights that segmentation by product type, primarily categorized into General Workwear and Protective Clothing, demonstrates the difference between aesthetic and functional priorities, with the latter commanding significantly higher average selling prices due to material complexity and certification requirements. End-use segmentation reveals the profound dependency of the market on the performance of the manufacturing, healthcare, and service industries, each dictating unique requirements in terms of durability, hygiene, and corporate branding, respectively.

The value chain for the Uniforms and Workwear Market begins with the highly specialized sourcing of raw materials, which is a critical determinant of the final product's performance and cost. Upstream activities involve textile manufacturers who produce standard fabrics (cotton, polyester) and specialized chemical companies that develop high-performance materials (fire-resistant aramids, anti-microbial treatments). The rising demand for specialized materials increases the complexity and cost at the upstream stage, making strategic partnerships with fiber suppliers essential for ensuring supply stability and proprietary material access. Quality control at this stage, particularly for protective clothing materials, is paramount to meeting stringent regulatory certifications.

Downstream activities focus on the final distribution and service provision. After garments are manufactured (midstream assembly and customization), they move through complex distribution channels. Direct sales are common for large corporate accounts, especially those requiring high degrees of customization or integrated inventory management solutions. Conversely, small to medium enterprises often procure uniforms through wholesalers or specialized distributors. A rapidly growing segment involves uniform rental and laundry services; these providers manage the entire lifecycle of the garment, from fitting and maintenance to replacement, offering companies a comprehensive, operational expenditure (OpEx) model rather than a capital expenditure (CapEx) approach to workwear acquisition.

The distribution network is characterized by both direct and indirect routes. Direct distribution ensures personalized service, quick fulfillment of complex, multi-site orders, and better control over brand representation. Indirect channels, particularly via dedicated market-specific distributors, provide broad market reach, especially in geographically fragmented regions. The increasing influence of e-commerce has introduced a highly efficient indirect route for general workwear and standardized items, enabling end-users to manage ordering and replenishment with greater autonomy. Effective value capture within this chain relies heavily on achieving efficiency in logistics, managing inventory complexity due to numerous sizing and specialization requirements, and delivering reliable after-sales services, particularly for high-value protective gear that requires professional cleaning and certification maintenance.

The primary customers for uniforms and workwear are large organizations across industrial, governmental, and service sectors that mandate standardized attire for compliance, safety, and branding purposes. These end-users typically require large volumes, specialized fitting services, and often long-term contractual agreements for supply and maintenance. The construction and manufacturing industries represent significant buyers, driven by mandatory regulatory requirements for PPE, including high-visibility clothing, flame-resistant materials, and sturdy footwear necessary for ensuring worker safety in hazardous operational environments and minimizing corporate liability risks.

Another major customer cluster is the healthcare industry, encompassing hospitals, clinics, nursing homes, and pharmaceutical research labs. These buyers prioritize uniforms (scrubs, gowns, lab coats) that emphasize hygiene, comfort for long shifts, and infection control properties, often requiring anti-microbial fabrics and easy sterilization protocols. The procurement in this sector is usually centralized and driven by institutional compliance standards and budgeting cycles. The hospitality and retail sectors form the third major segment, where the focus shifts toward durability, corporate aesthetics, and professional presentation, using uniforms as a key tool for enhancing customer experience and reinforcing brand image.

Emerging segments of potential customers include rapidly expanding logistics, warehousing, and e-commerce fulfillment centers, which require functional, highly durable, and often technology-integrated uniforms for efficient movement and item scanning. Government agencies, including military, police, and municipal services, remain consistent high-value customers for highly technical and durable workwear designed for extreme operational conditions and specific functional demands. Successful engagement with these potential customers requires market suppliers to offer not only high-quality garments but also sophisticated uniform management solutions, including RFID tracking, automated dispensing, and comprehensive repair/replacement programs.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 58.5 Billion |

| Market Forecast in 2033 | USD 86.8 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | VF Corporation, Aramark, UniFirst Corporation, Cintas Corporation, 3M Company, Lakeland Industries, Inc., Honeywell International Inc., Workwear Group, Sioen Industries NV, Alsico Group, F. Engel K/S, Hultafors Group AB, Klopman International, Johnson Service Group PLC, Dickies (A part of VF Corporation), Bulwark Protective Apparel, Carhartt, Inc., Kimberly-Clark Corporation, Wenaas AS, Fristads AB |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Uniforms and Workwear Market is rapidly evolving, driven by the convergence of material science and digital integration, shifting the focus from mere protection to proactive safety and monitoring. One major technological pillar is the advancement in performance textiles. This includes the development of lightweight yet highly protective materials such as advanced composite fibers, high-density polyethylene (HDPE) fabrics, and inherently flame-resistant (IFR) synthetic blends that offer superior comfort, durability, and multi-hazard protection. These innovations address the critical trade-off between protection and breathability, particularly important in hot industrial environments. Additionally, anti-microbial finishes and viral-barrier technologies, significantly accelerated by global health crises, are now standard requirements in healthcare and food service uniforms, emphasizing hygiene functionality.

The second critical technology trend is the integration of Smart Workwear and IoT capabilities. This involves embedding micro-sensors, RFID tags, and other electronic components directly into the fabric or garment structure without compromising comfort or washability. These smart uniforms enable real-time monitoring of various parameters, including worker physiological data (heart rate, body temperature), environmental exposure (gas leaks, extreme heat), and location tracking for lone workers or in emergency situations. The data collected provides actionable insights into operational efficiency and worker fatigue, moving safety protocols from reactive responses to preventative interventions, significantly enhancing enterprise-level risk management strategies and regulatory compliance efforts.

Furthermore, digitalization is transforming how uniforms are produced, managed, and maintained. Three-dimensional (3D) body scanning technology is increasingly used for precise measurement and customization, ensuring optimal fit and maximizing the effectiveness of protective gear, thereby reducing the error rates associated with traditional manual sizing. In the supply chain, technologies like blockchain and advanced RFID tracking ensure traceability, certifying the origin and compliance standards of specialized protective materials throughout the garment's lifecycle. These technological adoptions are not only improving product quality but are also facilitating circular economy initiatives by making the sorting and recycling of end-of-life workwear more efficient and economically viable.

The primary drivers include increasingly stringent global occupational health and safety regulations, rapid industrialization in the Asia Pacific region, and technological advancements leading to the development and adoption of high-performance and smart protective clothing across hazardous industries.

Sustainability is a major trend driving innovation toward circular economy models. This involves using recycled synthetic fibers, organic cotton, and bio-based materials, and implementing robust recycling programs for end-of-life garments, responding to corporate ESG mandates and consumer preference for eco-friendly products.

The manufacturing, construction, and oil and gas sectors currently hold the largest share for specialized protective clothing due to high operational risks and strict compliance requirements necessitating fire-resistant, chemical-resistant, and high-visibility garments for worker safety.

Smart workwear integrates IoT sensors to provide real-time monitoring of worker health, location, and environmental exposure. This technology shifts safety management from reactive to preventative, enhancing operational efficiency, minimizing accidents, and driving premium segment growth through advanced data analytics.

Yes, uniform rental and leasing models are gaining traction, especially in North America and Europe. This shift allows businesses to convert capital expenditure (CapEx) into predictable operational expenditure (OpEx), ensuring consistent inventory, professional maintenance, and guaranteed compliance without the burden of in-house management.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.