ID : MRU_ 439025 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

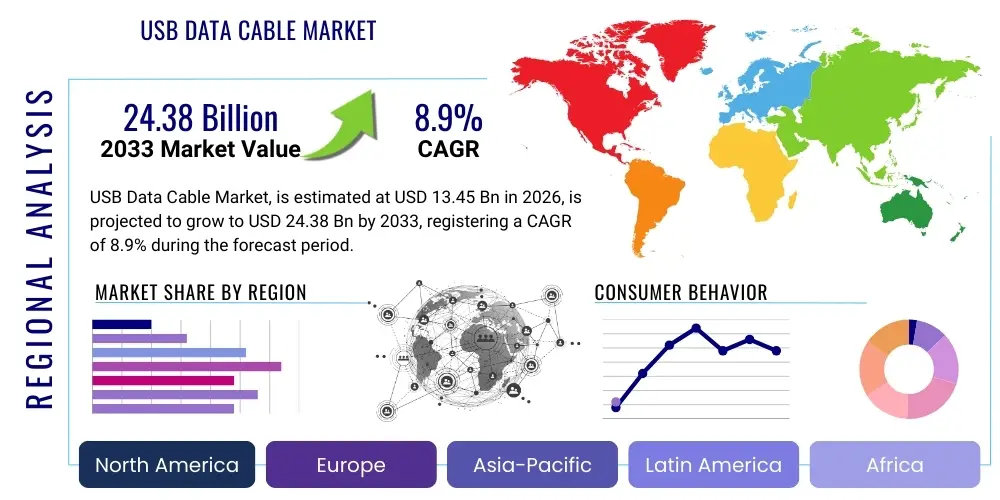

The USB Data Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2026 and 2033. The market is estimated at USD 13.45 Billion in 2026 and is projected to reach USD 24.38 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the pervasive adoption of consumer electronic devices globally, the ongoing standardization efforts around the USB Type-C connector, and the escalating demand for high-speed data transfer and efficient fast-charging solutions across diverse sectors including mobile, computing, and automotive industries. The transition from legacy USB standards to advanced protocols like USB4 and Thunderbolt 4, capable of handling 40Gbps data rates and higher power delivery profiles, reinforces this optimistic market outlook, positioning USB data cables as critical components in modern digital infrastructure.

The USB Data Cable Market encompasses the production and distribution of cables designed to connect devices using Universal Serial Bus (USB) standards, facilitating both power transfer (charging) and bidirectional data communication. These products are fundamental components in the modern technological ecosystem, connecting smartphones, computers, peripherals, consumer electronics, medical equipment, and automotive systems. Product descriptions vary significantly, ranging from standard USB Type-A to Micro-B, proprietary interfaces like Lightning, and the increasingly dominant USB Type-C, which offers reversible connectivity and enhanced power delivery capabilities.

Major applications of USB data cables span personal computing, telecommunications, industrial automation, and professional audio/video integration. The primary benefits derived from these cables include robust connectivity, universally accepted standards ensuring interoperability, high reliability for simultaneous charging and data synchronization, and increasingly rapid data transmission speeds vital for large file transfers and high-definition video output. The evolution of Power Delivery (PD) specifications allows a single cable to handle power requirements up to 240W, making them essential for high-power devices like gaming laptops and monitors.

Key driving factors propelling market growth include the global surge in smartphone and IoT device ownership, governmental mandates promoting connector standardization (especially the EU's push for USB-C), the continuous introduction of newer, faster USB standards (USB 3.2, USB4), and the rising consumer expectation for rapid charging technologies. Furthermore, the expansion of cloud computing and data centers necessitates efficient peripheral connectivity, boosting the demand for high-quality, high-durability USB infrastructure cables.

The USB Data Cable Market exhibits robust growth propelled by critical business trends centered around standardization, premiumization, and capacity enhancement. Business trends are dominated by the global transition toward USB Type-C, which simplifies supply chains and encourages accessory consolidation. Furthermore, key manufacturers are focusing on premium, specialized cables (e.g., active optical cables, Thunderbolt-certified cables) to cater to high-end computing and professional segments, driving up the average selling price (ASP). Regional trends indicate that Asia Pacific maintains its dominance in manufacturing volume and consumer consumption due to its massive electronics production base and dense population of mobile users. North America and Europe lead in the adoption of high-speed protocols (USB4, Thunderbolt) and sustainable product design, often featuring cables with recycled materials or enhanced durability ratings.

Segment trends highlight significant momentum within the USB Type-C segment, which is rapidly displacing Micro-USB and proprietary connectors across mid-range and high-end devices. The application segment is heavily weighted towards smartphones and mobile accessories, but the Automotive and Industrial segments are exhibiting the fastest growth rates, driven by in-vehicle infotainment systems and the proliferation of industrial sensors and machine vision requiring stable, high-speed data connections. Material trends show a continuous shift towards enhanced shielding and more flexible polymer jackets to meet the rigorous demands of professional use and increased longevity expectations. The market structure is moderately fragmented, with large semiconductor and electronics giants competing fiercely with specialized cable manufacturers and high-volume, cost-competitive Asian producers.

Overall, the market is characterized by rapid technological refresh cycles, driven by the continuous improvement in USB specifications regarding both data throughput and power delivery capability. While competition from wireless charging and data transmission technologies poses a minor long-term restraint, the undeniable need for fast, reliable, and high-bandwidth wired connections for complex tasks—such as external display support, high-speed backup, and power delivery to high-consumption devices—ensures the sustained relevance and expansion of the USB data cable sector through the forecast period.

User inquiries regarding AI's influence on the USB Data Cable Market primarily revolve around three key themes: whether AI will replace the need for physical cables (via advanced wireless protocols), how AI-driven devices (like edge computing hardware) increase the demand for high-performance cables, and how AI can optimize cable manufacturing and logistics. Analysis suggests that while AI supports the development of more efficient wireless charging and transmission standards, it simultaneously intensifies the demand for ultra-high-speed, low-latency physical interconnects. AI processing, particularly in data centers, high-performance computing (HPC), and advanced machine vision applications, requires consistent, high-bandwidth data pipes that current wireless technologies cannot reliably match. Furthermore, AI is being leveraged by manufacturers for predictive quality control, optimizing material usage, and streamlining complex assembly processes unique to high-speed USB cables, thereby ensuring higher manufacturing yields and improved product durability, directly impacting market quality standards and production costs.

The USB Data Cable Market is influenced by a dynamic interplay of Drivers (D), Restraints (R), and Opportunities (O), which collectively define the Impact Forces shaping the industry's trajectory. Key drivers include the accelerated shift towards USB Type-C standardization globally, spurred by legislative actions like those in the European Union, making USB-C the universal connector for a vast array of devices. Concurrently, the proliferation of 5G networks and bandwidth-intensive applications such as 8K streaming, VR/AR, and large-scale data transfers mandate the use of high-speed cables (USB 3.2 Gen 2x2 and beyond), providing strong impetus for market growth. The escalating consumer demand for rapid charging capabilities, supported by advanced USB Power Delivery (PD) standards up to 240W, further solidifies the market's positive outlook, ensuring that wired connections remain essential for demanding power applications.

However, the market faces significant restraints, notably the growing competition from increasingly efficient wireless charging and data transmission technologies, which offer greater convenience, potentially diminishing the need for physical cables in low-power and slow-data applications. Moreover, environmental concerns surrounding electronic waste (e-waste) and the frequent replacement cycles of low-quality or obsolete cables pose regulatory and public relations challenges for the industry. Counterfeit products and non-compliant cables, often sold at lower prices, dilute market value and can damage connected devices, creating challenges for premium manufacturers striving for quality and compliance with high-power standards.

Opportunities for expansion lie primarily in the emerging applications of USB technology within niche, high-growth sectors. The automotive industry, moving towards fully integrated infotainment systems and relying on robust internal data networks, presents a major avenue for specialized, automotive-grade USB cables. Furthermore, the adoption of USB4 and Thunderbolt protocols in enterprise and medical imaging equipment necessitates higher margin, technologically sophisticated cables (e.g., active and optical USB cables). These complex interconnects, which overcome length limitations and maintain high signal integrity, represent a significant opportunity for market players investing in advanced material science and signal processing technologies.

The USB Data Cable Market is extensively segmented based on connector type, application, standard, and material, reflecting the diversity of uses and performance requirements across the global electronics industry. The connector type segmentation, which includes USB Type-C, USB Type-A, Micro-USB, Mini-USB, and proprietary interfaces like Lightning, clearly demonstrates the industry’s shift, with USB Type-C emerging as the dominant growth driver due to its versatility and superior performance characteristics in power and data transfer. Application-based segmentation reveals that consumer electronics, particularly smartphones and personal computers, constitute the largest revenue generating segments, while emerging applications in automotive electronics and industrial machinery are showing the most accelerated adoption rates as they integrate complex digital systems.

The value chain for the USB Data Cable Market is complex, beginning with raw material extraction and concluding with retail distribution and end-user consumption, with efficiency at each stage being crucial for profitability. The upstream segment involves the sourcing of critical materials such as high-purity copper, insulation polymers (PVC, TPE, silicone), and semiconductor chips necessary for active cables and integrated power delivery circuitry. Key suppliers in this phase often dictate cost structure and quality parameters, particularly concerning signal integrity components and shielding materials required for high-speed protocols like USB4. Manufacturing—the core midstream process—involves original equipment manufacturers (OEMs) and original design manufacturers (ODMs) primarily based in Asia, who specialize in highly precise extrusion, assembly, and rigorous quality testing, ensuring compliance with stringent USB-IF (Implementers Forum) standards for data rate and power handling.

Downstream activities focus on market penetration and delivery. The distribution channel is bifurcated into direct and indirect routes. Direct sales involve large volume transactions with major electronics manufacturers (Apple, Samsung, Dell) who often bundle cables with their primary devices. Indirect distribution, which accounts for the aftermarket and replacement segment, utilizes extensive networks including traditional brick-and-mortar retail stores, specialized electronics outlets, and, most significantly, global e-commerce platforms (Amazon, Alibaba). The dominance of e-commerce has led to increased price transparency and intensified competition, necessitating robust branding and certification to differentiate genuine, compliant products from lower-quality generic alternatives.

Effective value chain management demands close collaboration between material suppliers and manufacturers to maintain consistent quality, especially given the continuous evolution of USB standards. The rapid technological shifts mean that inventory obsolescence is a constant threat, forcing manufacturers to adopt lean production methods. Furthermore, the increasing regulatory emphasis on sustainability and e-waste reduction is compelling the entire value chain to adopt more environmentally friendly materials and ensure longer product lifecycles, ultimately influencing sourcing decisions and manufacturing processes.

Potential customers for the USB Data Cable Market are highly diversified, encompassing massive institutional buyers (OEMs) and individual consumers seeking replacement or upgrade accessories. The primary end-users fall into four major categories: Consumer Electronics, Enterprise & Computing, Automotive, and Industrial/Medical. Consumers represent the largest volume segment, purchasing cables for charging and syncing smartphones, tablets, and gaming peripherals. These buyers prioritize affordability, durability, and compatibility with the latest fast-charging standards.

Enterprise and computing customers are critical buyers of high-specification cables, including IT departments procuring peripherals for corporate laptops, data centers requiring reliable interconnection for storage arrays, and professional users (e.g., videographers, graphic designers) demanding high-bandwidth cables (Thunderbolt/USB4) for high-resolution displays and rapid external SSD transfers. The automotive industry represents a high-value segment, requiring specialized, temperature-resistant, and vibration-proof USB cables integrated into vehicle infotainment systems and advanced driver-assistance systems (ADAS) for stable data connectivity within the vehicle structure. Finally, the medical and industrial sectors require certified, often shielded, cables for connecting diagnostic equipment and precise industrial control sensors, where failure tolerance is extremely low, driving demand for premium, highly robust products.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 13.45 Billion |

| Market Forecast in 2033 | USD 24.38 Billion |

| Growth Rate | 8.9% CAGR ( Include CAGR Word with % Value ) |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Anker Innovations, Belkin International, Foxconn Technology Group (Hon Hai Precision), Luxshare Precision Industry Co., Ltd., Amphenol Corporation, TE Connectivity, Molex LLC, Volex plc, Sumitomo Electric Industries, Ltd., Lotes Co., Ltd., Prysmian Group, Shenzhen Kaiboer Technology Co., Ltd., Ugreen Group Limited, CE-Link, Winstar Cable & Wire, ZAGG, Inc., JCE Group, StarTech.com, Monster Cable Products, Inc., PNY Technologies. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the USB Data Cable Market is defined by continuous innovation focused on increasing data transfer speeds, enhancing power delivery capabilities, and improving signal integrity over longer distances. The primary technological pillars include the adoption of sophisticated integrated circuits (ICs) within active cables, advanced shielding materials, and the evolution of the core USB specifications themselves. The rollout of the USB Power Delivery (PD) standard, which now supports Extended Power Range (EPR) up to 240W, necessitates specialized cable construction with enhanced thermal management and compliant electronic marking (e-marker) chips. These e-markers communicate the cable’s capabilities (data speed, power handling) to the connected devices, ensuring safe and optimal operation, a critical technological advancement differentiating high-quality compliant cables from generic alternatives.

Furthermore, the high-speed protocols, particularly USB4 and Thunderbolt 4, demand extremely tight tolerances in cable manufacturing. These standards utilize advanced signal processing techniques, including active electronic components (retimers or redrivers) embedded within the cable assembly, transforming passive cables into active optical or electrical components. Active Optical Cables (AOCs) are increasingly crucial for enterprise and professional AV applications, where data rates of 40Gbps and higher must be maintained over distances exceeding standard copper cable limits (typically 3 meters for high-speed protocols). AOCs convert electrical signals to optical signals for transmission and back again, ensuring maximal performance without electromagnetic interference (EMI) issues, representing the forefront of physical connectivity technology.

Material science also plays a significant role, with manufacturers developing more durable, flexible, and sustainable jacketing materials (e.g., bio-based TPE) to meet consumer and regulatory demands. Technological differentiation is highly sought after through features like reinforced stress points (anti-fray technology), magnetic connectors for quick attachment, and robust shielding (braided copper and aluminum foil) to prevent crosstalk and external interference, essential for maintaining signal integrity in dense computing environments. The commitment to backward compatibility while pushing the limits of speed and power remains the central technological challenge and driver for market innovation.

The primary factor driving growth is the mandatory global standardization and widespread adoption of the USB Type-C connector, coupled with the increasing consumer demand for rapid charging technologies enabled by the USB Power Delivery (PD) specification, supporting up to 240W.

USB4 and Thunderbolt 4 protocols mandate higher-quality cables, often requiring active components (retimers or e-markers) to reliably achieve ultra-high data transfer rates (up to 40 Gbps) and support complex features like simultaneous 8K video output and high-power delivery over a single connection.

The Smartphones and Tablets application segment currently holds the largest market share, driven by high volume sales, frequent cable replacement cycles, and continuous demand for faster charging and synchronization capabilities across the massive global mobile device installed base.

While wireless charging reduces the need for constant physical connection in low-power scenarios, it is not a complete threat. Wired USB cables remain essential for high-speed data transfer (e.g., professional data backup, display output) and delivering high power levels (over 60W) efficiently, where current wireless technology is often insufficient or slower.

The EU's mandate requiring USB Type-C as the common charging port across most portable devices significantly accelerates market consolidation around Type-C, boosts demand for compliant accessories, and encourages manufacturers to streamline production and adhere to stricter quality standards across the continent.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.