ID : MRU_ 432930 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

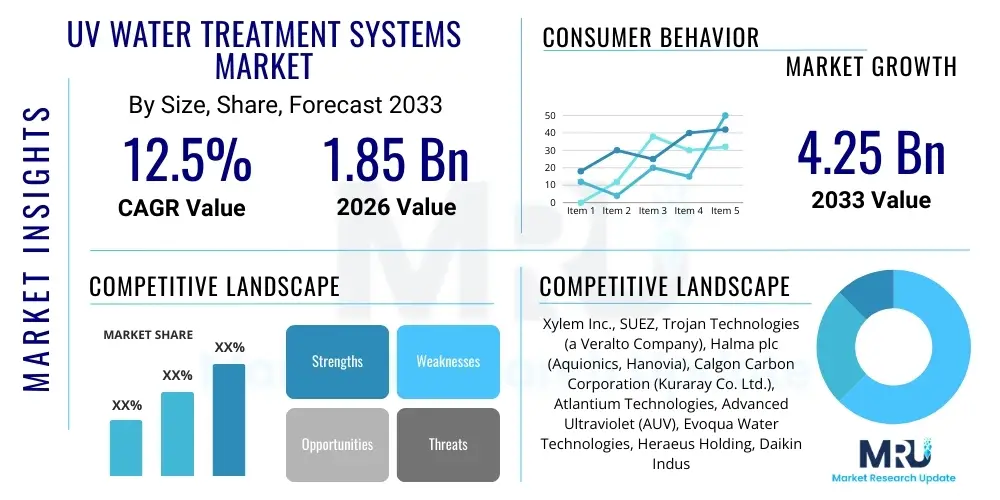

The UV Water Treatment Systems Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at USD 1.85 Billion in 2026 and is projected to reach USD 4.25 Billion by the end of the forecast period in 2033.

The UV Water Treatment Systems Market encompasses the design, manufacturing, and distribution of equipment utilizing ultraviolet light, specifically UV-C radiation, to inactivate microorganisms such as bacteria, viruses, and protozoa without adding chemicals to the water. These systems operate on the principle of DNA disruption, preventing pathogens from reproducing and rendering them harmless. Major applications span municipal water treatment facilities, industrial process water purification, residential drinking water systems, and wastewater recycling plants, driven by increasing global concerns over water scarcity and the resurgence of antibiotic-resistant pathogens. The primary benefit of UV technology is its effectiveness as a chemical-free, rapid, and low-maintenance disinfection method. Key driving factors include stringent government regulations mandating safe drinking water standards, growing public awareness regarding waterborne diseases, and the necessity for sustainable and environmentally friendly water purification solutions across developed and developing economies.

The global UV Water Treatment Systems Market is characterized by robust business trends emphasizing miniaturization, integration of smart monitoring capabilities, and the shift toward energy-efficient UV-C LED technology, replacing traditional low-pressure mercury vapor lamps in many residential and point-of-use applications. Regional trends indicate that Asia Pacific is emerging as the fastest-growing market due to rapid urbanization, massive infrastructure spending on wastewater treatment, and high levels of untapped market penetration potential in countries like China and India. North America and Europe maintain dominance in terms of technology adoption and stringent regulatory frameworks. Segmentation trends highlight that the industrial segment, particularly within electronics manufacturing, pharmaceuticals, and food and beverage industries, accounts for the largest revenue share, driven by the critical need for ultra-pure water. Conversely, the residential segment is expected to exhibit the highest CAGR, spurred by affordability improvements and decentralized water solutions. Overall, market growth is intrinsically linked to global water quality mandates and technological advancements aimed at enhancing system efficiency and lifespan.

User inquiries regarding the integration of Artificial Intelligence (AI) into UV water treatment often center on enhancing predictive maintenance, optimizing lamp dosing based on real-time water quality fluctuations, and ensuring compliance reporting. Users frequently ask how AI can reduce operational expenditure (OPEX) and improve disinfection effectiveness without increasing energy consumption. Key themes emerging from these concerns include the desire for automated system self-diagnosis, optimization of UV lamp intensity to match varying flow rates and turbidity levels, thereby minimizing energy waste, and the use of machine learning algorithms to predict lamp replacement schedules accurately, extending operational uptime. The general expectation is that AI integration will transform UV systems from passive disinfection units into proactive, intelligent water quality management platforms, minimizing human intervention and maximizing regulatory adherence through continuous data analysis and system optimization.

The UV Water Treatment Systems Market is primarily driven by the escalating global demand for safe drinking water, underpinned by stringent governmental and international regulatory bodies like the Environmental Protection Agency (EPA) and the World Health Organization (WHO), which enforce microbial standards. Restraints on market growth include the substantial initial capital investment required for installation, particularly for large-scale municipal infrastructure projects, and the perceived technical limitations of UV light, such as its ineffectiveness against dissolved inorganic contaminants and particulates, necessitating pre-filtration. Opportunities are abundant in the burgeoning UV-C LED segment, offering reduced size, longer lifespan, and lower power consumption, appealing to decentralized and residential applications. Additionally, the increasing focus on water reuse and recycling in water-stressed regions presents significant avenues for growth. The major impact forces propelling the market forward include rapid urbanization and industrialization in emerging markets, coupled with persistent environmental concerns over chemical residuals from traditional chlorination methods, making UV disinfection an increasingly preferred, sustainable alternative.

The UV Water Treatment Systems Market is segmented based on component type, application, end-user industry, and light source, providing a granular view of market dynamics and adoption patterns across various sectors. Component segmentation analyzes UV lamps, reactors, control units, and quartz sleeves, which are essential for system function and maintenance. Application areas differentiate between disinfection, TOC reduction, and dechlorination, reflecting the varying operational demands placed on the technology. End-user categorization distinguishes between municipal, industrial, and residential sectors, each with distinct needs regarding volume capacity and water purity levels. The segmentation by light source, notably Low-Pressure (LP), Medium-Pressure (MP), and UV-C Light Emitting Diodes (LED), dictates energy efficiency, operational flexibility, and capital expenditure.

The value chain for UV Water Treatment Systems begins with raw material sourcing and the highly specialized manufacturing of key components, particularly UV lamps (mercury vapor or UV-C LEDs), quartz sleeves, and reactor vessels, which often involve specialized metallurgy or plastics. Upstream analysis highlights the critical role of chemical companies and electronics suppliers providing high-purity quartz and mercury for traditional lamps, or gallium nitride (GaN) substrates for advanced UV-C LEDs. Suppliers must adhere to stringent quality controls as the efficiency and lifespan of the final system are heavily reliant on the quality of these primary inputs. Innovation at this stage, particularly in increasing the efficiency and wattage of UV-C LEDs, directly impacts the competitiveness and adoption rate of finished systems, driving down power consumption and maintenance burdens over time.

The midstream stage involves system design, assembly, and testing. Manufacturers integrate the sourced components into optimized reactor designs tailored for specific flow rates and water quality parameters, often incorporating advanced controls and sensors. Direct distribution channels, where manufacturers sell systems directly to large municipal authorities or major industrial firms, are common for high-capacity projects requiring extensive customization and ongoing service contracts. Conversely, indirect distribution utilizes a network of specialized water treatment distributors, value-added resellers (VARs), and plumbing supply houses, especially for residential and smaller commercial point-of-use (POU) systems. This dual distribution strategy allows manufacturers to penetrate diverse market segments effectively while managing the complexity of technical service requirements.

Downstream analysis focuses on installation, commissioning, operations, and long-term service and maintenance. Maintenance is a significant revenue driver, encompassing the regular replacement of UV lamps and quartz sleeves—consumables essential for maintaining disinfection performance. The effectiveness of the overall value chain is maximized when efficient, localized service networks are established, ensuring rapid response to technical issues and minimizing downtime, which is crucial for compliant water provision. The shift towards IoT and smart monitoring enhances the downstream service offerings, enabling remote diagnostics and predictive maintenance scheduling, further cementing long-term relationships between system providers and end-users and ensuring consistent water safety standards.

Potential customers for UV Water Treatment Systems are highly diverse, spanning three major sectors: municipal, industrial, and residential/commercial. Municipalities are the largest buyers, requiring high-capacity, robust UV systems for disinfecting treated drinking water and wastewater effluent before discharge or reuse. Their purchasing decisions are primarily driven by regulatory compliance, system reliability, and long-term operational costs, prioritizing proven technology and extensive service history from suppliers. As urbanization accelerates and older infrastructure is upgraded, municipal demand remains a stable cornerstone of the market, focusing increasingly on sustainable, chemical-free disinfection solutions to meet ever-tightening discharge limits and water reuse mandates.

The industrial sector represents the most heterogeneous group of buyers, with distinct requirements based on process needs. The pharmaceutical and microelectronics industries demand ultra-pure water (UPW) where UV systems are critical for Total Organic Carbon (TOC) reduction and maintaining sterility, often requiring highly specialized low-pressure lamps and advanced monitoring. The Food and Beverage industry utilizes UV disinfection extensively for product water, bottle rinsing, and syrup preparation to prevent spoilage and ensure consumer safety. These industrial end-users prioritize customized solutions that integrate seamlessly into complex manufacturing processes, focusing on operational uptime and regulatory validation specific to their industry standards, such as FDA compliance for pharmaceuticals.

Residential and smaller commercial establishments constitute a rapidly expanding customer base, primarily utilizing point-of-entry (POE) or point-of-use (POU) systems for decentralized water safety. This segment includes individual homeowners, restaurants, hotels, schools, and hospitals seeking supplementary or primary disinfection against well water contamination or post-filtration microbial growth. Purchasing drivers here are often affordability, ease of installation and maintenance (DIY capability), and system compactness, favoring the newer, smaller, and more efficient UV-C LED systems. The growing consumer concern over pathogens in municipal supply lines and the trend towards self-reliance in water treatment further fuels adoption in this high-growth segment, making it crucial for market expansion strategies focused on mass-market penetration.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 4.25 Billion |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Xylem Inc., SUEZ, Trojan Technologies (a Veralto Company), Halma plc (Aquionics, Hanovia), Calgon Carbon Corporation (Kuraray Co. Ltd.), Atlantium Technologies, Advanced Ultraviolet (AUV), Evoqua Water Technologies, Heraeus Holding, Daikin Industries, Ltd., Lit Controls, Inc., Luminor Environmental, Inc., Ideal Horizons, Inc., RENA Technologies GmbH, Safe Water Technologies Inc., UV Pure Water, Inc., Severo Technologies, Watermark Solutions, PWS GmbH, Pure Aqua, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the UV Water Treatment Systems Market is defined by a dynamic transition from conventional mercury vapor lamps to solid-state UV-C Light Emitting Diodes (LEDs), alongside advancements in reactor design and integration with smart monitoring platforms. Traditional low-pressure (LP) and medium-pressure (MP) UV lamps remain dominant in high-flow municipal and industrial applications due to their proven reliability, high output power, and cost-effectiveness at scale. LP lamps, which emit a monochromatic wavelength (254 nm), are highly efficient for germicidal disinfection, while MP lamps emit a polychromatic spectrum, making them effective for destroying complex chemical compounds like TOC and addressing photoreactivation in some organisms. However, these systems require larger footprints, involve the environmental hazard of mercury disposal, and suffer from efficiency loss during prolonged use.

The most significant technological evolution is the rapid commercialization and adoption of UV-C LED technology. UV-C LEDs offer numerous advantages, including instant on/off capability, eliminating warm-up time; highly focused wavelengths allowing for tailored disinfection; a compact form factor ideal for point-of-use and portable systems; and, critically, being mercury-free, addressing environmental concerns. Although initial capital costs for UV-C LED systems are currently higher, their substantially longer operational lifespan, reduced power consumption, and minimal maintenance requirements are driving rapid adoption in residential, commercial, and small decentralized industrial applications. Continued research focusing on increasing the power output and wall-plug efficiency of UV-C LEDs is crucial for their eventual penetration into the large-scale municipal sector, which currently relies heavily on MP systems.

Beyond the light source itself, technological advancements in system intelligence are paramount. Modern UV systems incorporate sophisticated control units featuring validated fluence (UV dose) monitoring in real time, utilizing advanced UV sensors and algorithms to automatically adjust lamp output based on water quality fluctuations (e.g., changes in UV transmittance or flow rate). This 'smart dosing' ensures optimal disinfection while conserving energy and extending lamp life. Furthermore, integration with IoT platforms enables remote diagnostics, cloud-based performance tracking, and seamless integration into broader water treatment SCADA systems, improving overall operational efficiency, reducing labor costs, and ensuring proactive compliance with strict governmental water quality standards across all end-user segments.

The primary advantage of UV treatment is that it provides effective, chemical-free disinfection, eliminating the risk of forming harmful disinfection byproducts (DBPs) like trihalomethanes, which are associated with chemical disinfectants such as chlorine. UV is also instantly effective against chlorine-resistant microorganisms like Cryptosporidium and Giardia.

LP systems offer higher electrical efficiency for basic microbial disinfection and TOC reduction in ultra-pure water applications. MP systems, utilizing a broader light spectrum, are typically preferred for high-flow municipal or industrial wastewater applications where a higher UV dose is needed, or where complex organic contaminants must be broken down.

UV-C LEDs represent the future of residential water purification due to their compact size, long lifespan, instant operation, and mercury-free composition. These characteristics facilitate their integration into small, point-of-use appliances, making UV disinfection more accessible, energy-efficient, and environmentally safe for decentralized home use.

Market growth is primarily restrained by the significant initial capital investment required for large-scale municipal infrastructure and the fact that UV light cannot treat dissolved chemicals, inorganic contaminants, or particulate matter; therefore, extensive pre-treatment (filtration) is mandatory, increasing system complexity and total cost of ownership.

The Asia Pacific (APAC) region is expected to lead market growth due to rapid urbanization, immense population density, and crucial governmental mandates focused on combating widespread waterborne diseases. Large-scale investments in new municipal water and wastewater treatment infrastructure across countries like China and India are the core drivers of this accelerated growth.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.