ID : MRU_ 434128 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

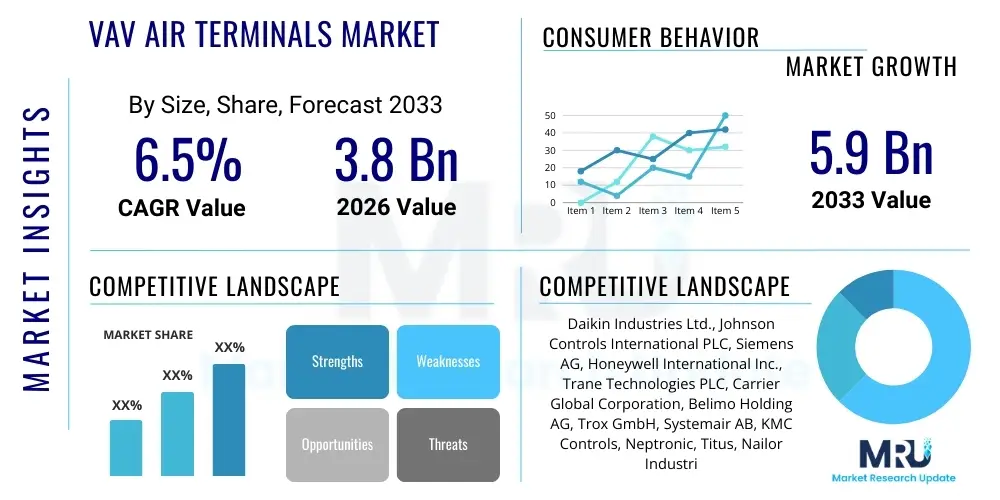

The Vav Air Terminals Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 3.8 billion in 2026 and is projected to reach USD 5.9 billion by the end of the forecast period in 2033. This consistent growth trajectory is primarily driven by the increasing global focus on energy efficiency in commercial buildings, coupled with stringent regulatory standards mandating the implementation of advanced HVAC systems to reduce carbon footprints and optimize operational costs.

The Variable Air Volume (VAV) Air Terminals Market encompasses the manufacturing, distribution, and utilization of VAV boxes and associated components designed to precisely regulate and deliver conditioned air to specific zones within a building. VAV systems are a cornerstone of modern Heating, Ventilation, and Air Conditioning (HVAC) infrastructure, offering significant improvements over traditional Constant Air Volume (CAV) systems by adjusting airflow based on the thermal load requirements of a space, thereby achieving substantial energy savings and enhanced occupant comfort. The primary product description centers around the VAV box, a mechanical device containing dampers, actuators, and often a reheating coil, integrated with sophisticated control logic to modulate air delivery.

Major applications of VAV air terminals span across diverse sectors, including commercial office spaces, educational institutions, healthcare facilities (hospitals and clinics), hospitality complexes, and large retail environments, where fluctuating occupancy levels and varied thermal demands necessitate localized and responsive climate control. The core benefit of VAV technology lies in its energy conservation capabilities; by modulating fan speed and reducing the volume of conditioned air supplied when cooling or heating demands are low, VAV systems drastically cut down on fan energy consumption, which is often the largest energy draw in commercial HVAC operations. Furthermore, VAV terminals contribute to superior indoor air quality and precise temperature control, adapting seamlessly to dynamic environmental conditions.

Key driving factors fueling market expansion include rapid urbanization, leading to an increase in new commercial construction activities globally, particularly in Asia Pacific and the Middle East. Additionally, government initiatives and green building certifications, such as LEED and BREEAM, are pushing developers towards high-efficiency HVAC solutions, making VAV systems the preferred choice. The continuous evolution of control technology, incorporating IoT and sensor integration for smarter, predictive maintenance and operation, further solidifies the market's growth outlook, transforming conventional air terminals into intelligent climate management hubs.

The global VAV Air Terminals Market is experiencing robust expansion, fundamentally driven by pervasive business trends emphasizing sustainable infrastructure development and operational expenditure reduction across the building sector. Current business trends show a strong shift towards intelligent VAV systems featuring integrated advanced controls, connectivity options (BMS integration via protocols like BACnet and Modbus), and enhanced acoustic performance, catering to high-end commercial real estate demanding minimal noise interference and maximum efficiency. Manufacturers are increasingly focusing on modular designs that facilitate easier installation and maintenance, aligning with the industry demand for reduced project timelines and lower life-cycle costs. Furthermore, the necessity for sophisticated air balancing and validation procedures post-installation is driving the demand for VAV terminals equipped with highly accurate flow measurement devices, enhancing system reliability and performance verification.

Regionally, the market dynamics are polarized, with North America and Europe maintaining dominance due to stringent energy regulations and high adoption rates of sophisticated building management systems (BMS). However, the Asia Pacific region is projected to register the highest growth rate, fueled by unprecedented infrastructure investment in developing economies like China and India, coupled with increasing awareness of green building practices and mandatory energy codes. Latin America and MEA are also showing promising potential, particularly within the hospitality and healthcare sectors, although penetration rates remain comparatively lower, often facing challenges related to initial investment costs and skilled labor availability for complex installations. The competitive landscape is characterized by major HVAC giants leveraging their extensive distribution networks and R&D capabilities to introduce next-generation VAV solutions tailored for diverse climatic conditions and local regulatory frameworks.

Segment trends highlight the growing preference for fan-powered VAV boxes, especially in perimeter zones where supplementary heat or airflow circulation is required, ensuring greater thermal stability compared to non-fan-powered units. The application segment sees the commercial office sector remaining the dominant consumer due to its inherent need for multi-zone environmental control and high energy consumption profile. Moreover, within the component segmentation, smart actuators and high-precision airflow sensors are witnessing significant demand growth, driven by the overall digitization of building services. These components are essential for achieving the tight tolerance specifications required by modern energy standards and optimizing the performance envelope of the entire HVAC system in real time, shifting the focus from simple air volume control to comprehensive climate intelligence.

Common user questions regarding AI's impact on the VAV Air Terminals Market frequently revolve around how artificial intelligence can move beyond simple set-point control to achieve predictive optimization, whether AI integration will necessitate hardware overhaul, and the specific cost-benefit analysis of deploying machine learning algorithms for energy management. Users are concerned about data security and the complexity of integrating self-learning algorithms into existing legacy BMS infrastructure. The overarching user expectation is that AI should enable VAV systems to anticipate thermal load changes based on occupancy patterns, weather forecasts, and historical operational data, leading to unprecedented energy efficiency gains and reduced maintenance downtime through anomaly detection. The analysis confirms that the primary themes are predictive maintenance, real-time optimization, and enhanced fault detection, transforming the traditional VAV terminal into an intelligent, autonomous climate management node capable of machine learning-driven decision-making.

The integration of Artificial Intelligence and Machine Learning (ML) algorithms is poised to fundamentally revolutionize the operational paradigm of VAV air terminals. AI moves the control philosophy from reactive modulation to proactive optimization. By analyzing vast datasets gathered from VAV sensors, BMS, external weather APIs, and access control systems, AI models can accurately predict future heating or cooling needs for specific zones hours in advance. This predictive capability allows the VAV terminal to adjust dampers and fan speeds smoothly, minimizing rapid changes, reducing wear and tear on mechanical components like actuators, and maintaining a tighter, more stable temperature band for occupants, thereby enhancing efficiency well beyond standard DDC (Direct Digital Control) systems.

Furthermore, AI significantly enhances the maintenance and fault detection capabilities of VAV systems. ML algorithms can establish a performance baseline for each terminal unit under various conditions. Any deviation from this learned normal operational profile—such as unexpected energy consumption spikes, unusual damper positions, or airflow irregularities—is flagged immediately as a potential fault, often before conventional alarms are triggered. This shift to predictive and prescriptive maintenance allows facility managers to address issues like sticky dampers or sensor drift proactively, optimizing resource allocation, reducing catastrophic failures, and dramatically improving the overall lifespan and reliability of the VAV air terminals throughout the lifecycle of the building.

The market for VAV Air Terminals is influenced by a dynamic interplay of Drivers, Restraints, and Opportunities, collectively forming the key Impact Forces shaping its direction. Key drivers include stringent global energy efficiency mandates (such as ASHRAE 90.1 standards and European Union directives), which necessitate high-performance HVAC systems capable of zone-level energy management. The rapidly increasing adoption of green building standards and certifications, which prioritize systems that demonstrate measurable reductions in utility costs and environmental impact, further pushes the demand for VAV technology. Restraints primarily involve the high initial capital expenditure associated with installing VAV systems, which is significantly higher than basic CAV systems, often deterring small-to-medium-sized developers. Additionally, the complexity of commissioning, balancing, and maintaining these sophisticated systems requires specialized technical expertise, posing a barrier in developing regions with limited skilled labor pools.

Opportunities for growth are vast, centered around the ongoing digital transformation of building infrastructure. The rise of Smart Buildings and the Internet of Things (IoT) provides manufacturers with avenues to integrate advanced sensors, wireless connectivity, and edge computing capabilities directly into VAV boxes, transforming them into networked data points. This creates new revenue streams related to data services, remote diagnostics, and continuous system optimization. Furthermore, the retrofitting market presents a substantial opportunity; as millions of older commercial buildings seek to comply with updated energy codes, replacing outdated HVAC systems with modern VAV technology becomes essential. The development of ultra-low leakage VAV boxes and those designed specifically for critical environments (e.g., laboratories or cleanrooms) also expands the addressable market.

Impact forces indicate that technological advancement is the strongest determinant of market direction. The pressure to reduce energy consumption (a major driver) often overrides the constraint of high initial cost over the long term, as demonstrated by favorable lifecycle cost analyses. The market is evolving towards total building solutions rather than standalone VAV products, meaning systems that offer seamless integration with lighting, security, and enterprise resource planning (ERP) systems will gain significant competitive advantage. The sustained demand for indoor air quality improvements, particularly post-pandemic, also acts as a critical force, driving the integration of advanced filtration and ventilation control strategies within the VAV terminal unit ecosystem.

The VAV Air Terminals Market segmentation provides a granular view of market structure based on product type, operational mechanism, component structure, and end-use application. Analyzing these segments helps stakeholders understand specific demand patterns, technological preferences, and regional adoption rates. The core differentiation often lies between the Fan-Powered and Non-Fan Powered VAV units, reflecting the divergent requirements of interior core zones versus building perimeter zones. The component segmentation, focusing on controllers and actuators, reflects the market's increasing reliance on sophisticated digital controls for optimal performance, moving away from purely mechanical regulation towards DDC and networked solutions.

The Value Chain for the VAV Air Terminals Market begins with Upstream Analysis, focusing on the procurement of raw materials, primarily specialized sheet metals (galvanized steel or aluminum for enclosures), electronic components (microprocessors, sensors, circuit boards), and specialized polymers for insulation and sealing. Manufacturers rely heavily on a stable supply chain for DDC components like controllers and high-precision actuators, often sourced from specialized electronics suppliers. Cost efficiency at this stage is crucial, as material input constitutes a significant portion of the total manufacturing cost, leading companies to establish robust partnerships and long-term contracts with reliable component vendors, often operating under strict quality assurance protocols to meet HVAC industry standards.

The midstream stage involves manufacturing and assembly, where core processes include metal fabrication, coil construction (for reheating options), insulation application, and the crucial integration of pneumatic or digital controls and highly calibrated airflow measuring stations. Quality control is paramount during the assembly of VAV boxes, ensuring minimal air leakage and precise control functionality. Subsequently, the Distribution Channel plays a critical role. Direct distribution involves large HVAC OEMs selling proprietary VAV solutions directly to major construction projects or facility management firms. Indirect distribution relies heavily on an extensive network of independent HVAC distributors, mechanical contractors, and system integrators who specify, procure, and install VAV terminals based on project requirements, often providing value-added services such as system design and commissioning.

Downstream Analysis focuses on the end-user application and post-sales support. The final customer (e.g., building owners, hospital administrators) purchases the system primarily for energy savings and comfort. Post-sales services, including system balancing, software upgrades, and long-term maintenance contracts, form a critical part of the downstream revenue stream. The trend is moving towards digital maintenance contracts facilitated by IoT integration, where manufacturers or specialized service providers remotely monitor VAV performance, preempting failures. This integration ensures optimal system performance throughout the building's lifecycle, solidifying the relationship between the supplier and the end-user.

Potential customers and end-users of VAV Air Terminals are primarily entities involved in the operation and construction of large, multi-zone commercial and institutional buildings where energy consumption and occupant comfort are critical operational priorities. The largest segment comprises commercial real estate developers and owners seeking modern HVAC solutions for high-rise office towers and corporate campuses, driven by the need to attract tenants with certified green buildings offering superior environmental control and lower operational costs. Furthermore, specialized institutional sectors, particularly healthcare providers (hospitals, labs) and educational facilities (universities, K-12 schools), represent key buyers due to their strict requirements for indoor air quality, precise temperature stability, and highly localized climate control within patient rooms, classrooms, and research areas.

In addition to new construction projects, the vast market of existing building stock undergoing retrofits constitutes a significant customer base. Facility management firms and energy service companies (ESCOs) actively seek VAV solutions to upgrade outdated CAV systems, driven by pressures to meet tightening municipal energy mandates and realize rapid returns on investment through reduced utility bills. Government agencies, managing public buildings and large administrative complexes, are also prominent customers, often prioritizing durable, standardized, and highly efficient VAV systems compatible with centralized building management platforms for large-scale deployment and centralized monitoring, ensuring consistent performance across diverse portfolios.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.8 Billion |

| Market Forecast in 2033 | USD 5.9 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Daikin Industries Ltd., Johnson Controls International PLC, Siemens AG, Honeywell International Inc., Trane Technologies PLC, Carrier Global Corporation, Belimo Holding AG, Trox GmbH, Systemair AB, KMC Controls, Neptronic, Titus, Nailor Industries Inc., Krueger International Inc. (KI), VTS Group, FlaktGroup. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the VAV Air Terminals Market is characterized by a significant transition from pneumatic and analog controls to advanced Direct Digital Control (DDC) and networked intelligence. Contemporary VAV systems rely heavily on high-precision electronic actuators that offer finer movement resolution and faster response times compared to older pneumatic systems, leading to superior temperature control and reduced hunting (overshooting and undershooting the setpoint). Crucially, the integration of advanced airflow sensing technology, such as thermal dispersion sensors or multi-point averaging pitot tubes, ensures highly accurate measurement of variable air volume, which is fundamental to achieving prescribed energy performance metrics and maintaining air balance across complex distribution networks. The reliability and accuracy of these sensors are major technological differentiators among leading manufacturers.

A key trend dominating the technological evolution is the mandated compatibility with modern Building Management Systems (BMS). This necessitates VAV controllers to support open communication protocols, primarily BACnet IP and Modbus TCP/IP, allowing seamless integration with centralized building automation platforms. Manufacturers are embedding microprocessors capable of local decision-making (edge computing) within the VAV controller itself, enabling rapid response to zone conditions without constant dependence on the central BMS server. This distributed intelligence architecture improves system resilience and speeds up data processing, supporting complex control strategies like optimum start/stop and demand-controlled ventilation (DCV) based on CO2 sensor inputs integrated directly or wirelessly connected to the VAV terminal unit.

Furthermore, attention is increasingly being placed on minimizing energy wastage within the VAV box itself, driving innovations in materials science and mechanical design. This includes the development of ultra-low leakage damper assemblies and superior insulation techniques, ensuring conditioned air is delivered efficiently without unnecessary loss, especially during minimum airflow settings. The rising popularity of wireless communication technologies (e.g., Zigbee or proprietary mesh networks) is simplifying installation and reducing wiring complexity, particularly beneficial for retrofit projects. The technological roadmap points toward self-commissioning VAV boxes that use embedded intelligence to automatically verify and adjust their parameters post-installation, drastically reducing commissioning time and minimizing the need for specialized technicians and complex, time-intensive balancing procedures.

Non-Fan Powered (or passive) VAV terminals simply modulate the primary supply air volume. Fan-Powered VAV terminals (either series or parallel) include an integral fan, typically used near building perimeters, to ensure continuous air circulation and mix primary conditioned air with ceiling plenum air for localized reheating or consistent airflow, improving comfort and reducing potential cold drafts in low-load conditions.

VAV terminals achieve energy savings by reducing the volume of air supplied to zones when cooling or heating demands decrease. This modulation minimizes the energy required by the central air handling unit (AHU) fan, which adheres to the Fan Affinity Laws (power consumption is proportional to the cube of the speed), resulting in exponential power reduction and significant operational cost savings compared to Constant Air Volume (CAV) systems.

Key advancements include the adoption of high-resolution digital electronic actuators and DDC controllers compatible with open protocols like BACnet, enabling seamless BMS integration. Furthermore, advancements in highly accurate airflow sensors and embedded intelligence for self-commissioning and predictive fault detection are rapidly increasing system efficiency and reducing maintenance complexity.

Modern VAV actuators, particularly digital electric models, typically have a robust lifespan exceeding 10 to 15 years, depending on usage cycle and environment. Maintenance is generally minimal, focusing primarily on periodic checks of calibration, connectivity, and ensuring proper operation of the damper mechanism. Predictive maintenance facilitated by FDD software helps identify potential failures, such as excessive running time or current draw, before the component fails entirely.

The Asia Pacific (APAC) region, specifically emerging economies like China and India, is projected to register the highest growth rate due to rapid expansion in commercial real estate, increasing investments in modern infrastructure, and growing governmental enforcement of energy conservation codes across new building construction projects.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.