ID : MRU_ 431484 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

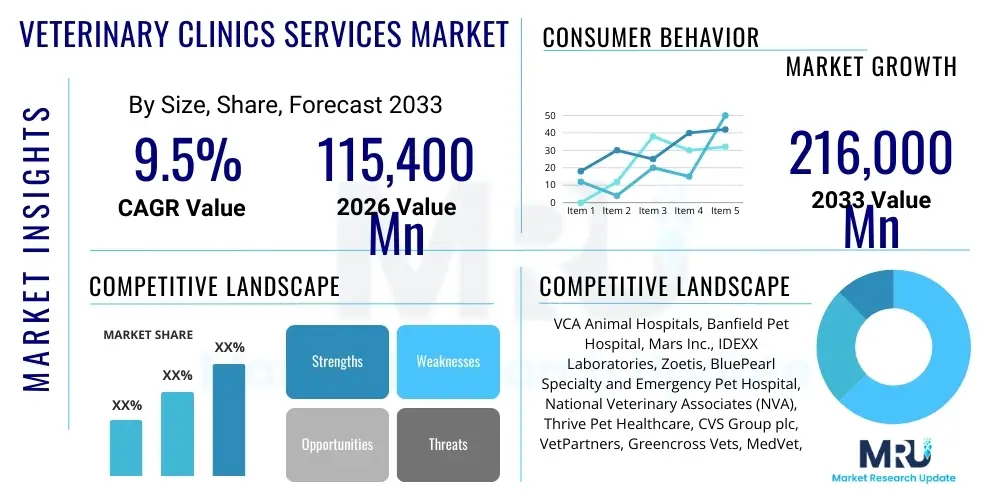

The Veterinary Clinics Services Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 115.4 Billion in 2026 and is projected to reach USD 216.0 Billion by the end of the forecast period in 2033.

The Veterinary Clinics Services Market encompasses a wide spectrum of medical and surgical care provided to companion animals, livestock, and exotic species. This market is primarily driven by the deepening bond between humans and their pets, a sociological phenomenon often termed the 'humanization of pets,' which leads to increased spending on premium healthcare, preventative medicine, and specialized veterinary procedures. The continuous innovation in veterinary technology, including advanced imaging (MRI, CT scans), sophisticated laboratory diagnostics, and specialized surgical techniques (e.g., orthopedic and neurological surgeries), elevates the standard of care offered, thereby expanding the market value. Furthermore, the rise in awareness regarding zoonotic diseases and the critical role of veterinary public health in maintaining food safety contributes significantly to the demand for services related to livestock and agricultural animals, particularly in emerging economies.

Services offered by veterinary clinics range broadly from routine wellness examinations, vaccinations, and parasite control to emergency care, dentistry, specialized internal medicine, oncology, and behavioral counseling. Major applications are centered around maintaining the long-term health and quality of life for companion animals, which constitute the largest revenue segment. However, the market also includes essential services for farm animals, focusing on disease management, reproductive health, and optimizing productivity within agricultural enterprises. The core benefit of these services is improved animal welfare, reduction of disease prevalence, and ensuring the safety of the food supply chain, which collectively strengthens public health outcomes and economic stability in rural sectors.

Key driving factors fueling market expansion include significant demographic shifts, such as increasing disposable incomes in developed and rapidly developing regions, which enable owners to afford higher-cost treatments. Simultaneously, the penetration of pet insurance models, offering financial mitigation against catastrophic health events, encourages earlier and more frequent veterinary visits. Additionally, the industry has seen substantial private equity investment and corporate consolidation, leading to the formation of large clinic networks capable of investing heavily in state-of-the-art equipment and specialized veterinary talent. This corporate structure often facilitates standardized, high-quality care across multiple locations, further enhancing consumer trust and utilization rates across the globe.

The Veterinary Clinics Services Market is characterized by robust business trends centered on consolidation, digitalization, and specialization. A dominant trend involves the aggressive acquisition strategy employed by large corporate entities and private equity firms, leading to highly integrated veterinary care networks (e.g., VCA, NVA). This consolidation trend provides economies of scale, better purchasing power for pharmaceuticals and equipment, and facilitates the recruitment of highly specialized veterinary surgeons and internal medicine experts. Digitalization, driven by the need for efficiency and enhanced client experience, involves the widespread adoption of Electronic Health Records (EHRs), streamlined appointment booking systems, and the proliferation of telemedicine platforms, which offer remote consultation and follow-up services, particularly crucial in addressing geographical barriers to access.

Regional trends indicate that North America and Europe remain the principal revenue generators, attributable to high pet ownership rates, mature pet insurance markets, and substantial per-pet spending. North America, in particular, demonstrates a strong inclination towards specialized and emergency care. However, the Asia Pacific (APAC) region is poised for the most rapid growth, driven by burgeoning middle classes in countries like China and India, adopting Western pet care standards and increasingly viewing pets as family members. This demographic shift is catalyzing investment in modern clinical infrastructure in previously underserved urban centers across APAC. Latin America and the Middle East and Africa (MEA) are also experiencing moderate growth, primarily focused on improving livestock health infrastructure and introducing basic companion animal preventative care.

Segment trends highlight the dominance of the companion animal segment (dogs and cats) over the livestock segment in terms of revenue, although the latter remains crucial for volume and disease surveillance. Within companion animal services, specialized procedures (e.g., advanced diagnostics, complex surgeries, oncology) are the fastest-growing sub-segment, reflecting owners' willingness to pursue sophisticated, life-extending treatments. Furthermore, the segmentation by service type shows a significant shift towards preventative and wellness plans, ensuring steady recurring revenue streams for clinics and encouraging routine visits, thereby improving early disease detection and management. The move towards specialized multi-species clinics that offer integrated services, from basic care to complex referrals, represents a key evolutionary pathway in clinical service delivery.

Analysis of common user questions regarding the integration of Artificial Intelligence (AI) in veterinary clinics reveals key themes revolving around diagnostic accuracy, workflow efficiency, and the fear of depersonalization. Users frequently inquire whether AI-powered tools, such as machine learning algorithms for interpreting radiographs or pathology slides, will supersede human expertise, particularly questioning the reliability of automated diagnoses in complex or rare cases. A major area of interest is the potential of AI to automate administrative tasks, such as patient scheduling, billing, and preliminary triage through chatbots, thereby freeing up veterinary staff to focus on direct patient care. Concerns often surface regarding data privacy, the cost of implementing these new technologies, and the necessity for specialized training to effectively utilize AI tools, suggesting that while the market anticipates technological advancement, it also seeks reassurance regarding practical adoption challenges and ethical implications.

The practical integration of AI is expected to revolutionize several operational facets within veterinary clinics. In diagnostics, AI algorithms significantly reduce the time required to analyze large datasets, such as medical images or blood chemistry panels, offering high-precision, rapid second opinions to clinicians, which is critical in emergency settings. Furthermore, predictive analytics, fueled by AI, enables clinics to better manage inventory, predict patient flow, and customize treatment protocols based on vast databases of clinical outcomes. This enhanced precision facilitates personalized veterinary medicine, moving away from generalized treatment paradigms towards therapies optimized for the individual animal's genetic and clinical profile, thus increasing treatment efficacy and client satisfaction.

From an economic standpoint, AI integration is expected to mitigate rising operational costs and partially address the acute global shortage of veterinary professionals. By automating routine documentation, synthesizing patient history, and generating preliminary reports, AI tools allow veterinary technicians and associates to operate at the top of their licenses, optimizing productivity. While the initial investment in AI infrastructure may be high, the long-term benefit includes reduced diagnostic errors, improved patient throughput, and enhanced efficiency in managing chronic conditions through continuous data monitoring. This shift positions clinics not just as service providers, but as data-driven health management centers, fundamentally altering the competitive landscape of the market.

The Veterinary Clinics Services Market is fundamentally shaped by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO) which collectively determine its growth trajectory and competitive intensity. The primary driver is the pervasive trend of pet humanization across developed and emerging economies, where pets are increasingly viewed and treated as family members. This sociological shift translates directly into increased financial commitment toward advanced veterinary care, including specialty treatments, preventative plans, and premium diets. Simultaneously, significant scientific advancements in veterinary medicine, paralleling human healthcare in areas like oncology, advanced surgery, and specialized diagnostics, create an expectation among pet owners for the highest possible standard of care. These factors, coupled with the increasing adoption of pet insurance, mitigate the cost barrier and encourage greater utilization of high-value services, reinforcing the market’s upward growth cycle.

However, the market faces significant restraints that dampen potential growth. The most critical restraint is the perpetually high cost of veterinary services, often viewed as discretionary spending, especially when insurance coverage is absent. This affordability issue can lead to treatment abandonment or reliance on less optimal care options, particularly among lower-income demographics. Furthermore, the global shortage of skilled veterinary professionals—veterinarians, specialists, and certified technicians—is placing immense strain on existing clinics, leading to burnout, increased wait times, and upward pressure on labor costs, which are inevitably passed on to the consumer. Regulatory hurdles related to pharmaceutical sourcing and specialized equipment licensing also pose logistical constraints, particularly in geographically fragmented markets or regions with developing healthcare infrastructures.

Opportunities within the market are predominantly technology-driven and client-centric. The widespread adoption of veterinary telemedicine represents a transformative opportunity, offering convenience, cost-effectiveness for routine check-ups, and expanding access to specialized opinions for geographically isolated populations. Another major opportunity lies in the development and marketing of comprehensive preventative healthcare packages, providing clinics with predictable, recurring revenue while ensuring continuous patient engagement. Finally, the aforementioned integration of AI and data analytics offers a pathway to operational excellence, allowing clinics to enhance efficiency, reduce diagnostic errors, and utilize predictive models to identify and manage population health risks, thereby securing a competitive advantage in a consolidating market landscape. These forces—pet owner devotion, technological innovation, and cost pressures—create a high-impact environment.

The Veterinary Clinics Services Market is extensively segmented based on Animal Type, Service Type, and End-Use, providing a comprehensive view of service delivery and demand patterns. The segmentation by Animal Type remains the most defining characteristic, where Companion Animals (dogs, cats, birds, small mammals) consistently account for the dominant market share due to the high frequency of veterinary visits and the propensity of owners in affluent regions to invest in chronic and specialized care. In contrast, the Livestock segment (cattle, swine, poultry) drives large-scale service volumes, focusing predominantly on herd health management, vaccination campaigns, and regulatory compliance related to food safety and zoonotic disease control.

The segmentation by Service Type differentiates between General Practices and Specialty/Emergency Services. General practices handle routine check-ups, vaccinations, and minor illnesses, representing the foundational layer of veterinary care. The rapidly growing specialty and emergency segment includes high-value, complex procedures such as advanced orthopedic surgery, internal medicine, oncology, and critical care units, demanding advanced technology and highly specialized personnel. This trend reflects the market's premiumization, as pet owners increasingly seek curative rather than palliative care options. Furthermore, the End-Use segmentation delineates between small-scale independent clinics, large corporate-owned hospitals, and specialized referral centers, noting the increasing shift toward corporate ownership and large, integrated hospital models offering 24/7 care and multispecialty services.

The value chain for Veterinary Clinics Services is complex, starting with upstream suppliers and culminating in the direct delivery of healthcare services to the animal owner. Upstream activities involve key stakeholders such as pharmaceutical companies (providing vaccines and therapeutics), medical device manufacturers (producing diagnostic imaging equipment, surgical instruments), and laboratory service providers. Consolidation in the clinic market has shifted the purchasing power dynamics, allowing large corporate networks to negotiate favorable bulk pricing, which impacts the profit margins of upstream suppliers. Effective supply chain management is crucial here, ensuring the timely and reliable delivery of temperature-sensitive biologics and essential medicines, especially across extensive regional networks.

Midstream activities primarily encompass the core operational functions of the veterinary clinic itself. This segment involves highly skilled labor—veterinarians, technicians, and administrative staff—who transform inputs (pharmaceuticals, equipment, data) into final services (consultation, surgery, diagnostics). Distribution channels within the market are highly diversified. Direct channels involve services provided in the clinic setting (e.g., surgery, X-rays). Indirect channels have expanded rapidly, particularly through the use of external reference laboratories for complex pathology and, increasingly, through digital platforms for telemedicine and remote prescription fulfillment. The effectiveness of the clinic's internal processes, technology adoption (EHR systems), and staff retention are paramount for maximizing value delivery and controlling service costs.

Downstream analysis focuses on the end-user interaction, which is characterized by high levels of emotion and trust. The primary value capture occurs at the point of service delivery, influenced heavily by the quality of clinical outcome, client communication, and overall experience. Large corporate chains often leverage centralized marketing, standardized protocols, and technology to enhance the client experience and build brand loyalty. Referral systems play a vital role, acting as a crucial distribution mechanism where general practitioners refer complex cases to specialty hospitals. The efficiency of this referral network and the integration of data sharing between general and specialty practices are essential components in ensuring seamless and high-quality longitudinal patient care and ultimately maximizing client lifetime value within the highly competitive veterinary landscape.

The primary customer base for the Veterinary Clinics Services Market can be broadly categorized into Companion Animal Owners, Livestock and Production Animal Owners, and Institutional Clients. Companion Animal Owners represent the largest and most lucrative segment, characterized by high emotional investment and significant discretionary spending on premium health services. Within this group, key demographics include high-income households, single professionals, and empty-nesters who frequently prioritize preventative care, specialized surgical interventions, and end-of-life care for their pets. The increasing prevalence of chronic diseases in aging pet populations ensures a steady and growing demand for continuous medical management and specialized geriatric veterinary services.

Livestock and Production Animal Owners, including large commercial farming operations, focus their purchasing decisions primarily on economic efficiency and regulatory compliance. These customers require robust veterinary services centered around herd health management, outbreak prevention, reproductive optimization, and ensuring compliance with stringent food safety and animal welfare regulations imposed by governmental and international bodies. Services provided to this segment are often delivered through contract arrangements and emphasize preventative measures and population medicine techniques rather than individual animal treatment, making long-term advisory contracts a key revenue stream for large animal practitioners and specialized veterinary consultancies.

Institutional Clients, comprising animal shelters, governmental public health agencies, zoos, and research facilities, represent a niche but essential customer segment. Shelters require high-volume, low-cost services focused on spay/neuter campaigns, preventative care for adopted animals, and infectious disease control to maintain facility health standards. Governmental agencies utilize veterinary services for disease surveillance, zoonotic risk assessment, and enforcement of public health mandates, particularly crucial in areas bordering wildlife habitats or international trade routes. The needs of these institutional buyers are often project-based and driven by public mandates or philanthropic funding, demanding specialized expertise in population health and regulatory reporting.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 115,400 Million |

| Market Forecast in 2033 | USD 216,000 Million |

| Growth Rate | CAGR 9.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | VCA Animal Hospitals, Banfield Pet Hospital, Mars Inc., IDEXX Laboratories, Zoetis, BluePearl Specialty and Emergency Pet Hospital, National Veterinary Associates (NVA), Thrive Pet Healthcare, CVS Group plc, VetPartners, Greencross Vets, MedVet, People, Pets & Vets, MWI Animal Health, Covetrus, Heska Corporation, IVC Evidensia, Elanco Animal Health, Addison Biological Laboratory, Inc., Boehringer Ingelheim International GmbH. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Veterinary Clinics Services Market is rapidly evolving, increasingly mirroring the sophistication seen in human medicine. Advanced diagnostic imaging equipment constitutes a cornerstone of modern veterinary practice, encompassing digital radiography, high-resolution ultrasound, Computed Tomography (CT), and Magnetic Resonance Imaging (MRI). The shift from conventional film-based systems to digital platforms enhances image quality, accelerates diagnostic timelines, and facilitates easy sharing of images for referral consultations. Furthermore, the miniaturization and improved cost-effectiveness of these technologies are making previously inaccessible tools viable for integration into larger general practice clinics, moving them beyond the exclusive domain of specialty referral hospitals. This technological investment is critical for attracting specialized veterinary talent and meeting the elevated expectations of pet owners.

Information technology platforms, particularly comprehensive Electronic Health Record (EHR) systems, are indispensable for managing complex patient data, streamlining practice workflow, and ensuring regulatory compliance. Modern EHRs are integrated with inventory management, billing systems, and client communication portals, creating a holistic operational platform. Crucially, the rise of telehealth platforms, including video conferencing tools and remote monitoring devices (such as continuous glucose monitors or wearable activity trackers for pets), allows veterinarians to extend their care outside the physical clinic setting. These technologies improve adherence to chronic care protocols and provide valuable longitudinal data that informs treatment adjustments, enhancing patient outcomes and convenience for the client.

Laboratory diagnostics have also seen significant technological advancements, moving towards Point-of-Care (POC) testing capabilities. POC devices allow clinics to perform rapid blood chemistry, hematology, and infectious disease screening in-house, significantly reducing turnaround times for critical diagnoses. This speed is vital for emergency and critical care scenarios. Additionally, the increasing use of robotics in complex orthopedic and soft tissue surgeries, although still nascent, signals a future where precision and minimally invasive techniques become standard. Technology adoption requires significant capital outlay and specialized staff training, but these investments are crucial for clinics aiming to position themselves as providers of premium, advanced veterinary care in a highly competitive and consolidated market structure.

The primary drivers are the increasing humanization of pets, leading to higher spending on advanced medical care and preventative wellness plans, coupled with technological advancements in veterinary diagnostics and the growing penetration of pet insurance across mature economies.

Corporate consolidation is rapidly integrating independent practices into large, managed networks, providing benefits such as better resource access, centralized management, and standardized protocols, but it also increases competition and operational pressure on remaining independent local clinics.

Telemedicine expands access to veterinary care, particularly in rural or underserved areas, facilitating remote consultations, post-operative follow-ups, and preliminary triage. It improves client convenience and enhances efficiency for managing chronic conditions, acting as a crucial complement to in-person visits.

The Asia Pacific (APAC) region is forecasted to exhibit the highest CAGR due to rapid urbanization, increasing pet ownership among the growing middle class, and a massive shift towards investing in comprehensive, high-quality companion animal healthcare services, particularly in countries like China and India.

The most significant restraint is the high cost of specialized veterinary services, which, despite rising incomes and insurance availability, remains a financial barrier for many pet owners, sometimes leading to difficult decisions regarding advanced or long-term therapeutic care.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.