ID : MRU_ 434553 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

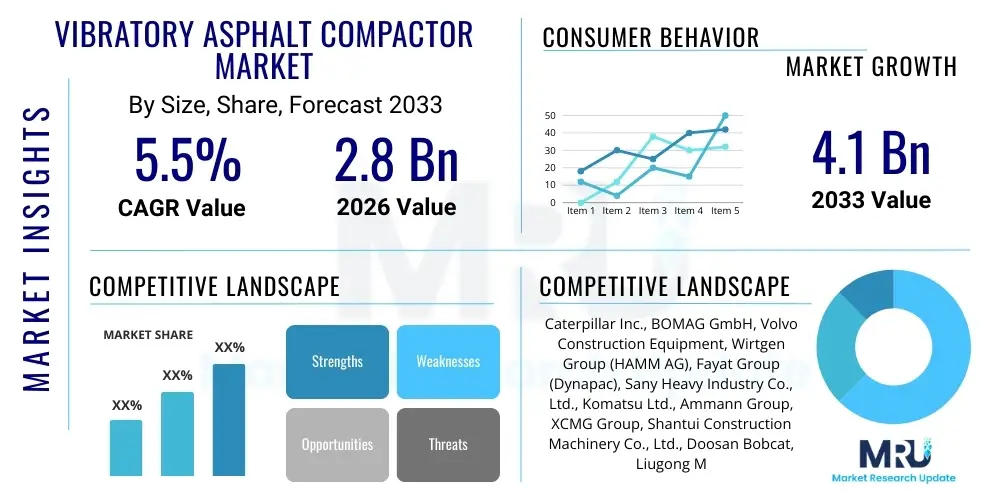

The Vibratory Asphalt Compactor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2026 and 2033. The market is estimated at USD 2.8 Billion in 2026 and is projected to reach USD 4.1 Billion by the end of the forecast period in 2033.

The Vibratory Asphalt Compactor Market encompasses the manufacturing, distribution, and utilization of heavy construction machinery designed specifically for achieving specified density and smoothness in asphalt layers during road construction, paving, and maintenance projects. These machines, often referred to as asphalt rollers, employ vibrating drums to generate dynamic forces, significantly enhancing compaction efficiency compared to static rollers. This technology is critical for ensuring the long-term durability and structural integrity of pavements, thereby supporting global infrastructure development goals. The primary product variations include tandem rollers (used for final surface compaction) and combination rollers (utilizing both steel drums and rubber tires).

Major applications for vibratory asphalt compactors span municipal road repair, large-scale highway construction, airport runway resurfacing, and commercial parking lot development. The inherent benefits of using these compactors include achieving uniform density, minimizing voids, improving load-bearing capacity, and enhancing water resistance of the asphalt pavement. Furthermore, modern compactors often feature sophisticated monitoring systems that optimize the compaction process, leading to reduced fuel consumption and lower operational costs, thereby driving adoption across mature and emerging economies.

Driving factors for this market include substantial government investments globally in infrastructure modernization, particularly in regions like Asia Pacific and North America. The increasing focus on smart city initiatives, coupled with the need to maintain aging transportation networks, fuels demand for high-performance and reliable compaction equipment. Technological advancements, such as the integration of intelligent compaction (IC) systems and telematics for fleet management, are also compelling contractors to upgrade their existing fleets, positioning the market for sustained growth throughout the forecast period.

The Vibratory Asphalt Compactor Market is characterized by robust business trends centered on technological integration and sustainability. Key industry players are focusing heavily on developing hydrostatic drive systems, fuel-efficient engines compliant with stringent environmental regulations (such as Tier 4 Final in North America and Stage V in Europe), and advanced automation features. The trend towards equipment rental, especially for smaller and medium-sized contractors, is reshaping distribution strategies, favoring manufacturers who offer flexible ownership models and comprehensive aftermarket support services. Furthermore, digital services related to machine diagnostics and performance optimization are becoming crucial competitive differentiators, shifting the market paradigm from purely hardware sales to integrated solutions provision.

Regionally, the Asia Pacific (APAC) region remains the powerhouse of market growth, driven by massive infrastructure expansion projects in India and China, alongside rapidly developing road networks in Southeast Asian nations. North America and Europe, while mature markets, exhibit consistent demand primarily due to high frequency of repair and maintenance activities (R&M) and the imperative to replace older fleets with intelligent, emission-compliant machinery. The Middle East and Africa (MEA) are also emerging as significant markets due to large-scale construction programs tied to urbanization and economic diversification, particularly in the Gulf Cooperation Council (GCC) states. These regional dynamics necessitate customized product offerings tailored to varying climate conditions and regulatory environments.

Segmentation analysis highlights the dominance of the medium operating weight segment (7 to 15 tons), which offers optimal versatility for both major highway construction and municipal road projects. By product type, tandem vibratory rollers hold a substantial market share owing to their superior finishing capabilities on final asphalt layers. The market is also seeing a surge in demand for machines equipped with Intelligent Compaction (IC) features across all weight classes. This technology segment, which includes integrated measurement, documentation, and control systems, addresses the industry's need for verifiable quality assurance, driving up the average selling price and improving efficiency across the construction vertical.

Common user inquiries concerning the influence of Artificial Intelligence (AI) on the vibratory asphalt compactor domain typically revolve around predictive maintenance, autonomous operation, and optimization of compaction patterns. Users are keen to understand how AI algorithms can improve the longevity and efficiency of the heavy machinery, reduce downtime, and enhance safety on construction sites. Specific concerns focus on the complexity and cost of integrating AI-powered systems into traditional equipment, the reliability of real-time data processing for compaction quality, and the potential displacement of manual labor. The overarching expectation is that AI will transition compaction from a reliance on operator skill to a data-driven, quality-assured process, delivering superior pavement performance.

The impact of AI is primarily concentrated in two areas: operational intelligence and autonomous functions. AI models analyze telematics data, sensor inputs (e.g., compaction meter value, temperature), and geospatial information to determine the optimal speed, amplitude, and number of passes required for perfect density, often exceeding the capabilities of human operators. This operational intelligence minimizes energy waste and prevents over-compaction, which can lead to material damage. Furthermore, AI-driven diagnostics enable highly accurate predictions of component failure, allowing contractors to schedule maintenance proactively rather than reactively, substantially boosting asset utilization rates across the fleet.

Looking forward, AI is foundational to the development of fully autonomous vibratory compactors. These systems use computer vision and machine learning to navigate complex, changing construction environments, coordinate movements with other machinery (e.g., pavers), and maintain strict adherence to predefined compaction plans. While full autonomy is still evolving, AI-enhanced assistance features—such as adaptive vibration control based on real-time surface feedback—are already becoming standard, significantly improving compaction uniformity and overall paving project quality. This integration solidifies AI's role not just as a monitoring tool, but as a core component of future compaction performance.

The market dynamics are governed by powerful structural drivers and restraining factors, balanced by significant opportunities that define future growth trajectories, collectively summarized as DRO & Impact Forces. Key drivers include aggressive global governmental spending on road infrastructure refurbishment and expansion, especially in emerging economies requiring modernization of transport links. The mandatory implementation of stringent quality control standards for road surfaces, demanding verifiable compaction data, further propels the adoption of advanced vibratory compactors featuring Intelligent Compaction (IC) technology. This push for quality, coupled with rapid urbanization necessitating durable municipal road networks, creates continuous demand for efficient paving machinery.

However, the market faces notable restraints, primarily concerning the high initial capital investment required for purchasing modern, technologically advanced compactors, particularly those equipped with IC and low-emission engines. This high cost often acts as a barrier to entry for smaller contractors, leading to a preference for used equipment or rental options. Furthermore, the volatility in raw material prices (especially steel and engine components) and the complexity of maintaining sophisticated electronic and hydraulic systems pose challenges to manufacturers and end-users alike. The market is also sensitive to macroeconomic cycles, with infrastructure projects often being delayed or scaled back during economic downturns, impacting short-term sales volume.

Opportunities for expansion are abundant, centered on the growing global rental market, which lowers the financial burden on contractors and accelerates fleet modernization. Manufacturers can capitalize on this by offering specialized telematics and service packages tailored to rental businesses. Geographically, underserved regions in Africa and Latin America present virgin markets ripe for development through targeted distribution partnerships. Moreover, the focus on sustainable construction practices creates a niche for compactors utilizing alternative power sources (electric or hybrid models) and those designed for highly efficient material use, aligning with global efforts to reduce the carbon footprint of the construction sector. The most influential impact force remains the regulatory pressure for infrastructure quality and environmental compliance, dictating the pace of technological innovation and market entry strategies.

The Vibratory Asphalt Compactor Market is broadly segmented based on product type, operating weight, and application, providing a granular view of demand patterns across different end-user needs. This segmentation allows manufacturers to tailor their product development and marketing strategies to specific niches within the construction industry. Product types differentiate between machines based on their configuration and primary compaction method, ranging from specialized single-drum rollers used for sub-base layers to versatile tandem rollers optimized for achieving smooth, high-density asphalt surfaces. Operating weight classification is crucial as it determines the machine's efficiency and suitability for various project scales, spanning from lightweight utility compactors to heavy-duty rollers required for major highway construction.

The key driver behind strategic segmentation is the evolving complexity of paving projects. For instance, urban revitalization projects typically require smaller, maneuverable compactors, whereas large airport or highway projects necessitate heavy, high-amplitude machines capable of processing large volumes of material quickly and efficiently. The application segment, therefore, further refines the market view by categorizing demand across specific construction verticals such as highway and road construction, airport paving, commercial and residential construction, and dam and reservoir projects. This multidimensional segmentation ensures that market analysis accurately reflects the specialized requirements and procurement behaviors of different construction entities globally.

Technological advancement, particularly the adoption rate of Intelligent Compaction (IC) systems, is increasingly becoming an informal segmentation factor, influencing procurement decisions regardless of weight class. Contractors often seek machines that offer integrated data logging, real-time feedback, and GPS mapping capabilities, indicating a market shift towards verifiable, quality-assured compaction outcomes. Consequently, equipment offering superior technology and connectivity features commands premium pricing, effectively creating a high-end segment focused on operational excellence and digital integration within the broader market structure.

The value chain for the Vibratory Asphalt Compactor Market is complex, beginning with upstream raw material suppliers and extending through manufacturing, assembly, distribution, and comprehensive aftermarket services. The upstream segment involves the sourcing of critical components, including specialized high-grade steel for drums and chassis, advanced hydraulic systems, powerful engines (often procured from specialized industrial engine manufacturers complying with emission standards), and complex electronic components necessary for telematics and Intelligent Compaction systems. Reliability and quality control at this stage are paramount, as the durability and performance of the final machine are directly linked to the quality of these sourced inputs. Manufacturers strive for strategic, long-term relationships with key component suppliers to mitigate supply chain risks and ensure regulatory compliance.

The midstream stage focuses on manufacturing and assembly. Leading Original Equipment Manufacturers (OEMs) typically maintain sophisticated assembly plants where components are integrated using precision engineering techniques. This stage includes complex processes such as welding, heat treatment of drums, installation of vibration mechanisms, and integration of control electronics and software. Manufacturers often invest heavily in Lean manufacturing principles and robotic automation to enhance production efficiency and maintain consistent quality across large-scale production runs. Product customization, such particularly modifications for extreme climate operation or specific regulatory requirements, also occurs extensively at this stage before final quality assurance testing.

The downstream segment encompasses distribution channels and customer service, which are pivotal in market penetration. Distribution primarily utilizes a network of authorized regional dealers who manage inventory, sales, and localized marketing. Direct sales to major governmental agencies or very large construction firms also occur, but the dealer network is essential for localized support. Aftermarket services, including spare parts supply, routine maintenance contracts, and advanced technical support, form a significant revenue stream and directly impact customer retention. The rise of the equipment rental market has also introduced specialized rental fleet operators as a key distribution channel, demanding robust service and maintenance support to ensure high utilization rates of the compactors.

The potential customer base for vibratory asphalt compactors is diverse, primarily encompassing governmental bodies, private construction contractors, and specialized rental agencies. Governmental agencies, including federal, state, and local departments of transportation (DOTs), are often the largest direct or indirect buyers, as they mandate and fund the vast majority of large-scale public road and infrastructure projects. Their procurement decisions are heavily influenced by regulatory compliance (emissions, safety), machine reliability, and the availability of advanced features like Intelligent Compaction systems required for verifiable project quality documentation.

Private construction companies constitute the most active segment of end-users. These range from large, multinational civil engineering firms undertaking massive highway contracts to smaller, local paving contractors focused on municipal roads, parking lots, and residential streets. Their purchasing decisions are driven by factors such as total cost of ownership (TCO), fuel efficiency, ease of operation, and the versatility of the equipment to handle different types of asphalt mixes and project sizes. Contractors often update their fleets to maintain a competitive edge by adopting newer, more efficient models that reduce operational costs and accelerate project completion timelines.

Equipment rental companies represent a rapidly growing customer segment. These companies purchase large fleets of compactors to lease to contractors who prefer not to commit to heavy capital expenditure or who require temporary capacity for peak seasons. Rental houses prioritize machines known for their robust build, minimal maintenance requirements, and high residual value. Manufacturers often develop specific product lines or service agreements tailored to the intense operational demands and utilization rates typical of rental fleets, viewing them as crucial intermediaries for market access, especially to smaller and geographically dispersed contractors.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 2.8 Billion |

| Market Forecast in 2033 | USD 4.1 Billion |

| Growth Rate | 5.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Caterpillar Inc., BOMAG GmbH, Volvo Construction Equipment, Wirtgen Group (HAMM AG), Fayat Group (Dynapac), Sany Heavy Industry Co., Ltd., Komatsu Ltd., Ammann Group, XCMG Group, Shantui Construction Machinery Co., Ltd., Doosan Bobcat, Liugong Machinery Co., Ltd., Sakai Heavy Industries, Ltd., CASE Construction Equipment, JCB, Astec Industries. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological evolution within the vibratory asphalt compactor market is primarily driven by the need for verifiable quality, operational efficiency, and environmental sustainability. A foundational technology is the hydrostatic drive system, which provides smooth, infinitely variable speed control, crucial for achieving uniform rolling speeds and avoiding surface irregularities. Coupled with advanced hydraulic vibration systems, modern compactors allow operators precise control over amplitude and frequency, optimizing the energy transfer to the asphalt mix based on material temperature and layer thickness. The continued refinement of these core hydraulic and drive technologies ensures high-performance compaction while minimizing fuel consumption.

The most transformative technology in recent years is Intelligent Compaction (IC). IC systems integrate accelerometers in the drums to measure the stiffness or Compaction Meter Value (CMV) of the pavement in real-time, coupled with high-precision Global Positioning System (GPS) mapping and data logging. This allows operators to monitor the compaction effort and density results instantaneously, ensuring that every pass contributes optimally to the desired final pavement quality. IC eliminates guesswork, prevents over or under-compaction, and provides documented proof of quality to project owners, which is increasingly mandatory for government contracts. Manufacturers are focusing on making IC systems user-friendly and fully integrated into the machine’s operating interface.

Furthermore, telematics and connectivity platforms are standard features, significantly enhancing asset management. Telematics systems allow fleet managers to remotely track machine location, operational status, fuel consumption, and diagnostic trouble codes. This real-time data flow supports predictive maintenance strategies, maximizing machine uptime. Additionally, adherence to stringent emission standards, such as Tier 4 Final/Stage V, necessitates advanced engine technology, including selective catalytic reduction (SCR) and diesel particulate filters (DPFs). The focus is increasingly shifting towards automation features, such as compaction assist or autonomous functions, utilizing AI to further optimize rolling patterns and ensure coordinated movement in multi-machine paving trains, improving overall project throughput and safety.

Intelligent Compaction (IC) is a technological system that uses integrated sensors, GPS mapping, and an onboard data recorder to measure, document, and control the compaction process in real-time. It benefits projects by ensuring uniform pavement density, preventing material damage from over-compaction, minimizing energy consumption, and providing verifiable quality assurance data to meet project specifications effectively.

Tandem rollers feature two smooth drums and are primarily used for achieving the final density and smooth finish on asphalt layers (binder and surface courses). Single drum rollers typically feature one large drum and are generally utilized for compaction of soil, aggregate base layers, or deeper asphalt layers due to their higher static weight and ability to generate greater impact forces.

The shift towards electric and hybrid compactors is gaining significant momentum, particularly in Europe and North America, driven by urban construction regulations restricting noise and emissions. While representing a niche segment currently, demand is growing due to their reduced operational costs, compliance with strict environmental standards, and suitability for sensitive municipal and indoor construction environments, signaling future market direction.

The Asia Pacific (APAC) region is projected to exhibit the highest Compound Annual Growth Rate (CAGR). This acceleration is directly attributed to massive infrastructure investments, extensive road network expansion, high rates of urbanization, and substantial governmental funding allocated to transportation development projects across countries like China, India, and emerging Southeast Asian nations.

The primary restraining factor is the high initial capital expenditure associated with purchasing technologically advanced vibratory asphalt compactors, especially those featuring Intelligent Compaction systems and compliance with the latest emission standards (Tier 4 Final/Stage V). This cost barrier often leads smaller and medium-sized contractors to rely heavily on equipment rental options or procurement of used machinery.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.