ID : MRU_ 437201 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

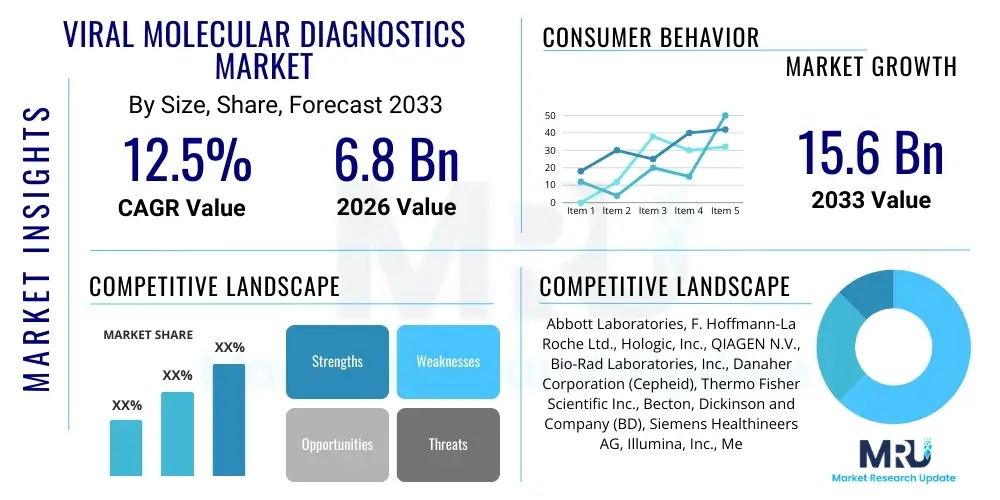

The Viral Molecular Diagnostics Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at USD 6.8 Billion in 2026 and is projected to reach USD 15.6 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the escalating global prevalence of infectious diseases, including recurring pandemics and endemic viral threats, coupled with significant advancements in automation and point-of-care testing technologies. The increasing demand for rapid and highly accurate detection methods, particularly in critical care and public health surveillance settings, solidifies the market's upward trajectory and sustained high growth rate over the projected timeline.

The Viral Molecular Diagnostics Market encompasses the application of molecular biology techniques, such as Polymerase Chain Reaction (PCR), Next-Generation Sequencing (NGS), and Isothermal Amplification, for the qualitative and quantitative detection of viral pathogens in biological samples. These advanced diagnostic tools are crucial for timely disease identification, guiding therapeutic decisions, monitoring treatment efficacy, and supporting epidemiological surveillance efforts. The primary product segments include reagents and kits, instruments, and software, utilized across various settings from central reference laboratories to decentralized point-of-care environments. The reliability, sensitivity, and specificity offered by molecular diagnostics have positioned them as the gold standard, gradually replacing traditional culture-based or serological methods that often lack the required throughput or turnaround time for urgent clinical needs.

Major applications of viral molecular diagnostics span a wide spectrum of infectious diseases, including but not limited to Human Immunodeficiency Virus (HIV), Hepatitis B and C (HBV/HCV), Influenza, Respiratory Syncytial Virus (RSV), Human Papillomavirus (HPV), and emerging infectious agents like SARS-CoV-2. The clinical utility of these tests extends beyond initial diagnosis into areas such as viral load monitoring, resistance testing, and pre-transplant screening, ensuring comprehensive patient management. Furthermore, the capacity for multiplex testing, allowing for the simultaneous detection of multiple pathogens from a single sample, dramatically improves diagnostic efficiency in syndromic testing panels, which is particularly vital during respiratory disease seasons.

Key driving factors fueling market growth include the rising global investment in infectious disease research and diagnostics infrastructure, particularly following recent global health crises, which highlighted the critical need for robust diagnostic preparedness. Technological convergence, leading to highly automated and integrated systems, reduces labor intensity and potential contamination, thereby increasing laboratory throughput. The increasing global awareness among healthcare professionals and policymakers regarding the critical role of early and precise viral detection in preventing large-scale outbreaks, coupled with favorable reimbursement policies in developed economies, ensures sustained market expansion and accelerated adoption of newer, faster molecular diagnostic platforms globally.

The Viral Molecular Diagnostics Market is characterized by intense technological innovation, focusing on transitioning from centralized laboratory testing to rapid, decentralized, and multiplexed platforms. Business trends indicate significant mergers, acquisitions, and strategic partnerships among major diagnostic developers and pharmaceutical companies aiming to consolidate market share and expand geographical reach, particularly in high-growth emerging economies. The competitive landscape is shaped by firms heavily investing in proprietary chemistries and instrumentation to deliver superior performance characteristics, such as shorter turnaround times and minimal hands-on time. The primary objective driving corporate strategy is the development of fully integrated, cartridge-based systems for true point-of-care viral detection, ensuring accessibility and rapid results outside traditional laboratory settings.

Regionally, North America maintains its dominance due to established healthcare infrastructure, high research and development spending, and the early adoption of advanced molecular technologies, including digital PCR and automated NGS platforms. However, the Asia Pacific (APAC) region is projected to exhibit the highest CAGR during the forecast period, driven by massive population density, increasing prevalence of infectious diseases, improving healthcare access, and substantial government investments in disease surveillance programs, particularly in China, India, and South Korea. Europe remains a strong market, supported by centralized public health systems and rigorous regulatory frameworks promoting high-quality diagnostic standards, though market growth rates may be slightly more moderate compared to APAC.

Segment trends highlight the dominance of the reagents and kits segment, which accounts for the largest market share and drives recurring revenue due to the high volume of testing required for both clinical diagnostics and epidemiological monitoring. Within technology, Real-Time PCR (RT-PCR) remains the foundational technology, but Next-Generation Sequencing (NGS) is experiencing the fastest growth, primarily due to its utility in comprehensive pathogen identification, outbreak tracking, and resistance surveillance, offering unparalleled resolution. End-user dynamics reveal hospitals and clinical laboratories as the primary consumers, although the segment comprising diagnostic centers and academic research institutes is rapidly expanding its adoption of high-throughput molecular platforms for routine screening and research applications.

User inquiries regarding the impact of Artificial Intelligence (AI) and Machine Learning (ML) on the Viral Molecular Diagnostics Market consistently revolve around optimizing diagnostic workflows, enhancing data interpretation accuracy, and accelerating pathogen discovery. Key user themes include the potential for AI to manage the overwhelming data output from high-throughput sequencing (NGS) platforms, concerns about the validation and regulatory acceptance of AI-driven diagnostic algorithms, and the practical implementation of AI tools within existing laboratory infrastructure. Users are particularly interested in how AI can improve clinical decision support by integrating molecular test results with patient clinical data, predicting disease progression, and identifying novel viral variants more efficiently than conventional bioinformatics methods.

AI is fundamentally reshaping the market by moving diagnostics beyond mere detection into predictive and preventive capabilities. AI and ML algorithms are being deployed to analyze complex genomic sequencing data to identify viral mutations quickly, aiding in pandemic preparedness and vaccine design. Furthermore, AI optimizes laboratory operations by predicting sample volumes, scheduling testing runs, and managing instrument maintenance, thus increasing overall laboratory efficiency and reducing turnaround times. This shift allows clinical laboratories to handle larger testing volumes accurately and cost-effectively, positioning AI as a critical enabler for scaling molecular diagnostic capabilities globally, particularly during high-demand periods.

The implementation of AI-driven decision support systems also enhances the clinical relevance of molecular results. By correlating viral load data, genotypic characteristics, and patient demographics, AI models can offer personalized treatment recommendations and track the geographical spread of viral strains in near real-time. This capability is invaluable for public health organizations, transforming passive surveillance into proactive intervention. However, successful integration necessitates robust data infrastructure, standardized data formats, and ethical guidelines governing the use of sensitive patient and genomic data, addressing a major concern frequently raised by potential adopters regarding data privacy and security.

The market is primarily driven by the recurrent emergence of infectious diseases and the increasing need for fast, highly sensitive, and specific detection methods, particularly for high-consequence viral pathogens. Restraints include the high initial capital investment required for sophisticated molecular diagnostic instruments, which can limit adoption in resource-limited settings, and the complexities associated with regulatory clearances for novel molecular assays. Opportunities are abundant in the development of multiplexed, decentralized point-of-care (POC) testing solutions and the integration of advanced technologies like CRISPR-based diagnostics and digital PCR, which offer enhanced performance and portability. The combined forces driving and constraining the market create a dynamic environment where technological innovation acts as the primary impact force, pushing adoption despite cost barriers.

Drivers: Significant global healthcare expenditure on infectious disease management, rapid technological progression leading to automation and miniaturization of devices, and increased government funding for public health initiatives and biosecurity preparedness globally are key drivers. The proven superior clinical performance of molecular tests over traditional methods, offering earlier detection and improved patient outcomes, further accelerates market penetration. Furthermore, the persistent threat posed by antibiotic resistance indirectly boosts the demand for rapid viral identification, ensuring that physicians can accurately distinguish between bacterial and viral infections, thereby curbing unnecessary antibiotic use.

Restraints: The primary restraint is the complex and stringent regulatory landscape, which often slows down the market entry of innovative molecular products. Furthermore, the limited availability of skilled professionals trained in interpreting complex molecular data and operating advanced instrumentation presents a significant challenge, especially in developing countries. Cost constraints related to expensive reagents, capital equipment, and maintenance costs pose a barrier to widespread implementation, necessitating the development of more affordable and scalable solutions for primary care settings.

Opportunities: Major opportunities lie in expanding market reach into emerging economies through localized manufacturing and distribution strategies. The development of low-cost, disposable molecular assays for POC testing targeting remote or underserved populations represents a high-growth area. Moreover, leveraging partnerships between technology developers and telehealth providers to integrate remote diagnostic interpretation services opens new avenues for enhancing diagnostic access and efficiency, transforming how viral diagnostics are delivered and managed across diverse geographic areas.

Impact Forces: The most impactful force is the sustained global focus on pandemic preparedness and response, which mandates continuous investment in high-throughput, resilient diagnostic infrastructure. Technological breakthroughs, especially in rapid sample preparation and extraction techniques and the convergence of digital health platforms with molecular testing, exert strong upward pressure on market growth. Conversely, pricing pressure exerted by large group purchasing organizations (GPOs) and public health systems acts as a mitigating downward force, pushing manufacturers to optimize production and streamline supply chains to maintain profitability while enhancing accessibility.

The Viral Molecular Diagnostics Market is comprehensively segmented based on technology, product type, application, and end-user, providing a granular view of market dynamics and adoption patterns across different modalities and clinical settings. The segment breakdown highlights the crucial role of consumables (reagents and kits) in driving market revenue, while concurrently emphasizing the transformational impact of new instrumentation and technology platforms, particularly those enabling decentralized testing. Analyzing these segments is essential for stakeholders to identify lucrative niche areas, understand competitive threats, and tailor product development to specific end-user requirements, ranging from centralized reference laboratories demanding high throughput to small clinics requiring fast, user-friendly solutions.

Technology segmentation clearly reflects the maturity and widespread use of PCR-based methods versus the emerging dominance of NGS, which offers deeper biological insights. Product segmentation is critical for understanding revenue streams, with the recurring nature of reagent sales ensuring market stability and continuous demand, irrespective of instrument purchasing cycles. Application segmentation underscores the market’s response to urgent public health needs, with respiratory viruses and sexually transmitted diseases (STDs) currently constituting the highest volume testing areas. Finally, end-user analysis provides insight into purchasing power and adoption barriers, showcasing the pivotal role of hospitals and diagnostic laboratories as primary market drivers and early adopters of cutting-edge molecular diagnostics technology.

The value chain for the Viral Molecular Diagnostics Market starts with fundamental research and development (R&D) focusing on novel biomarkers, nucleic acid extraction methods, and amplification chemistries. This upstream segment is highly knowledge-intensive, driven by universities, biotech startups, and large research organizations that secure intellectual property. The subsequent stage involves the manufacturing and sourcing of high-purity raw materials, including specialized enzymes, oligonucleotides (primers and probes), and diagnostic plastics. Efficient sourcing and quality control at this stage are crucial, as variations in raw material quality directly impact the sensitivity and reliability of the final diagnostic kits.

The midstream segment involves the core manufacturing, assembly, and quality assurance of finished diagnostic instruments and test kits. Major diagnostic corporations dominate this phase, leveraging economies of scale and sophisticated automated production lines. Key activities include instrument calibration, reagent lyophilization, and regulatory compliance (e.g., FDA, CE marking). This stage is characterized by intense competition to reduce manufacturing costs while ensuring scalability and maintaining rigorous performance standards, which are critical for gaining clinical acceptance and market share in highly regulated healthcare systems worldwide.

The downstream segment, focused on distribution, sales, and service, is highly fragmented but critical for market penetration. Distribution channels are typically complex, involving direct sales forces for large instruments, third-party distributors for reagents in specific regions, and specialized logistics for cold chain management. Direct channels are preferred for high-value strategic accounts like large reference labs, while indirect channels leverage regional expertise to reach smaller clinical sites and developing markets. Post-sales support, including instrument maintenance, technical training, and bioinformatics services, completes the value chain, ensuring the long-term utility and adoption of molecular diagnostic solutions in a demanding clinical environment.

The primary end-users and buyers of viral molecular diagnostics products are centralized reference laboratories and large hospital laboratory networks, which require high-throughput, automated systems to process massive volumes of samples efficiently and cost-effectively. These entities are typically focused on population screening, complex viral load monitoring, and highly specialized tests that necessitate advanced instrumentation and dedicated bioinformatics support. Their purchasing decisions are heavily influenced by regulatory approvals, automation capabilities, total cost of ownership, and proven clinical validation data, demanding robust, high-precision instruments and bulk procurement of reagents.

A rapidly growing customer segment includes decentralized healthcare settings, such as small community hospitals, urgent care clinics, and physician office laboratories (POLs). These customers prioritize ease of use, rapid turnaround time (STAT testing), and compact, portable instrumentation, favoring cartridge-based, point-of-care (POC) molecular platforms. For these users, the value proposition lies in enabling immediate clinical decision-making without reliance on external reference laboratories, significantly improving patient flow and reducing the time to treatment initiation, especially in emergency and critical care scenarios.

Furthermore, academic and research institutions, along with major pharmaceutical and biotechnology companies, constitute a significant but distinct customer base. These organizations utilize viral molecular diagnostics, particularly Next-Generation Sequencing (NGS) platforms, for fundamental research into viral pathogenesis, drug target identification, vaccine development, and large-scale clinical trials. Their demand centers around flexibility, high analytical resolution, and the ability to customize assays, focusing on high-end instruments and specialized bioinformatics services tailored for genomic surveillance and translational medicine applications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 6.8 Billion |

| Market Forecast in 2033 | USD 15.6 Billion |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Abbott Laboratories, F. Hoffmann-La Roche Ltd., Hologic, Inc., QIAGEN N.V., Bio-Rad Laboratories, Inc., Danaher Corporation (Cepheid), Thermo Fisher Scientific Inc., Becton, Dickinson and Company (BD), Siemens Healthineers AG, Illumina, Inc., Meridian Bioscience, Luminex Corporation, PerkinElmer Inc., DiaSorin S.p.A., Grifols, S.A., bioMérieux SA, Agilent Technologies, Inc., Canon Medical Systems Corporation, Co-Diagnostics, Inc., Quidel Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the viral molecular diagnostics market is dominated by Nucleic Acid Amplification Technologies (NAATs), with Polymerase Chain Reaction (PCR) serving as the fundamental backbone. Real-Time PCR (RT-PCR) continues to be the most widely adopted method due to its high sensitivity, quantitative capabilities (viral load monitoring), and established clinical utility. Recent advancements in PCR focus on multiplexing capabilities, enabling the simultaneous detection of dozens of respiratory pathogens in a single assay, significantly improving diagnostic throughput and clinical value, particularly in syndromic testing panels, thus catering to the urgent need for comprehensive and rapid infectious disease screening during high-prevalence seasons.

A significant disruptive force is the emergence of Next-Generation Sequencing (NGS) as a diagnostic tool. While traditionally confined to research, NGS is moving into clinical microbiology, offering unparalleled power for unbiased, comprehensive pathogen identification, genetic variation analysis, and tracking viral evolution. This application is crucial for public health surveillance and understanding the transmission dynamics of novel and emerging viruses, providing high-resolution genomic data essential for effective epidemiological interventions. Furthermore, the integration of automation and simplified library preparation protocols is lowering the barrier to entry for NGS adoption in routine clinical settings, making it increasingly competitive with traditional high-throughput methods.

Other vital technologies driving innovation include Isothermal Nucleic Acid Amplification Technology (INAAT), such as Loop-mediated Isothermal Amplification (LAMP) and Nucleic Acid Sequence-Based Amplification (NASBA). INAAT platforms eliminate the need for thermal cyclers, making them ideal for rapid, portable, and low-cost point-of-care testing in remote areas or resource-constrained settings. Additionally, highly specialized areas like Digital PCR (dPCR) are gaining traction, providing absolute quantification of nucleic acids with superior sensitivity compared to standard RT-PCR, finding specialized applications in extremely low viral load detection, residual disease monitoring, and non-invasive prenatal testing, further diversifying the technological portfolio available to healthcare providers globally.

The market growth is primarily driven by Polymerase Chain Reaction (PCR) technologies, particularly Real-Time PCR (RT-PCR) due to its high sensitivity and quantitative accuracy. However, Next-Generation Sequencing (NGS) is rapidly becoming pivotal for genomic surveillance and comprehensive pathogen identification, representing the fastest-growing segment.

Hospitals and Clinical Laboratories collectively represent the largest end-user segment. These institutions utilize high-throughput automation platforms for routine viral screening, viral load monitoring, and specialized diagnostics, driven by large patient volumes and established infrastructure.

Centralized molecular diagnostics offer high throughput, extensive multiplexing, and greater complexity, typically handled by large reference labs. POC diagnostics focus on speed, portability, and ease of use, enabling rapid results outside the central lab, crucial for emergency room settings and remote locations.

AI significantly influences the market by optimizing data analysis from complex platforms like NGS, accelerating the detection of viral variants, improving workflow efficiency in labs, and enhancing clinical decision support systems through integrated data interpretation.

The primary restraining factors in developing regions include the high initial capital expenditure for advanced instruments, the recurring cost of proprietary reagents, and the limited availability of specialized technical expertise required to operate and maintain sophisticated molecular diagnostic platforms.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.